Ihor Lukianenko/iStock through Getty Pictures

We began covering Accelleron Industries (OTCPK:ACLLY) even earlier than its spin-off from ABB (OTCPK:ABBNY) and when it began buying and selling, we remarked it was off to a great begin, noting that we notably appreciated the companies section due to its resilient recurring income. Nonetheless, in our final article, we downgraded the corporate as we thought the valuation had gotten comparatively excessive. We had been clearly too early with our downgrade, as shares have outperformed the S&P 500 index (SPY) and gained roughly 36% in about 4 months, regardless of there being no main information popping out from the corporate. Lastly, a serious replace got here on March twenty seventh, when the corporate revealed its 2023 outcomes. We’re revisiting our evaluation primarily based on the just lately revealed outcomes, and the now a lot greater valuation.

Fiscal Yr 2023 Outcomes

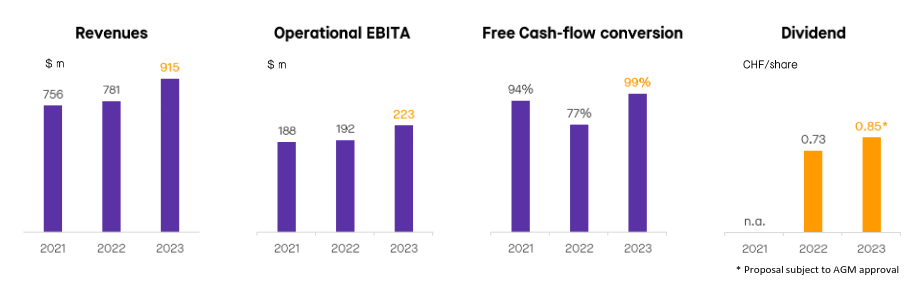

Outcomes had been strong, however we don’t assume they justify the form of worth appreciation seen within the shares the previous couple of months. Natural income elevated ~15.5%, principally by means of worth will increase to compensate a number of the inflation seen in its enter prices. Whereas it’s good to see that the corporate has the pricing energy to guard its revenue margins, we’d warning traders to not depend on this stage of income progress going ahead, as it would get more durable to justify to prospects any future vital worth will increase. We consider quantity progress is extra sturdy progress, and in that respect, efficiency was mainly flat.

The corporate did do a great job additional rising its free money movement conversion to 99%, which enabled a dividend enhance.

Accelleron Industries Investor Presentation

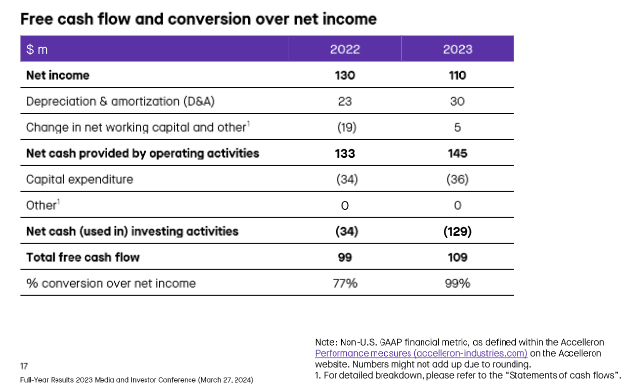

Whereas operational EBITA noticed a corresponding enhance, internet revenue was really decrease attributable to one-time prices, principally associated to the corporate’s separation and arrange as an impartial entity. Free money movement was additionally helped by adjustments in working capital, and a better depreciation and amortization quantity.

Accelleron Industries Investor Presentation

It is very important word that given the decreased internet revenue, the dividend payout ratio elevated to 93% of reported internet revenue after minority pursuits. We anticipate internet revenue to rebound in 2024, given the operational EBITA enchancment and the truth that the one-time prices ought to now not influence the underside line. Nonetheless, we expect the payout ratio will stay excessive, and traders shouldn’t anticipate a lot dividend progress long run.

Steadiness Sheet

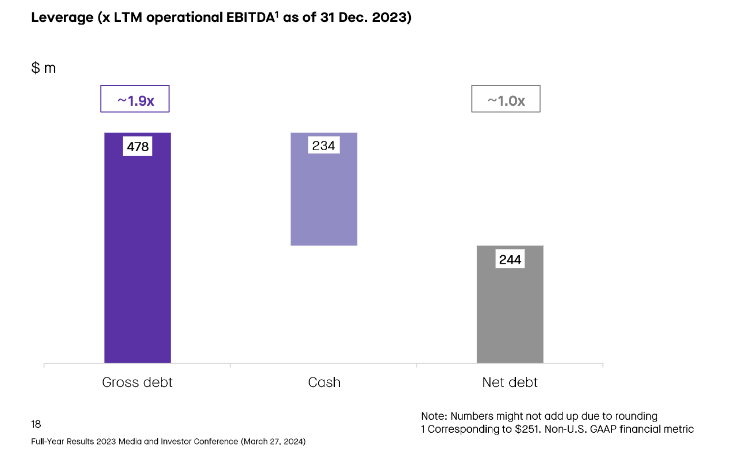

Accelleron Industries stays dedicated to a strong steadiness sheet, and up to now it has maintained very respectable leverage. Web debt to operational EBITDA ticked up as a result of OMT acquisition however stays at a really wholesome ~1x leverage ratio. The elevated money holdings additionally give the corporate optionality to pursue some further bolt-on acquisitions if the chance presents itself.

Accelleron Industries Investor Presentation

Analysis & Growth

We like that the corporate continues to spend cash on analysis and improvement, particularly, to have options prepared for coming emissions necessities that its prospects will quickly be dealing with. It’s also additional bettering the efficiency of its turbochargers, that are already a number of the finest performing.

That is vital, as it’s a sign that the corporate nonetheless sees some progress alternatives, even when the longer term might be very difficult for them if the world goes absolutely electrical. Within the meantime, the corporate is seeing some tailwinds from elevated demand from knowledge facilities (for his or her backup energy turbines), and from new extra sustainable fuels within the delivery trade.

Accelleron Industries Investor Presentation

Outlook

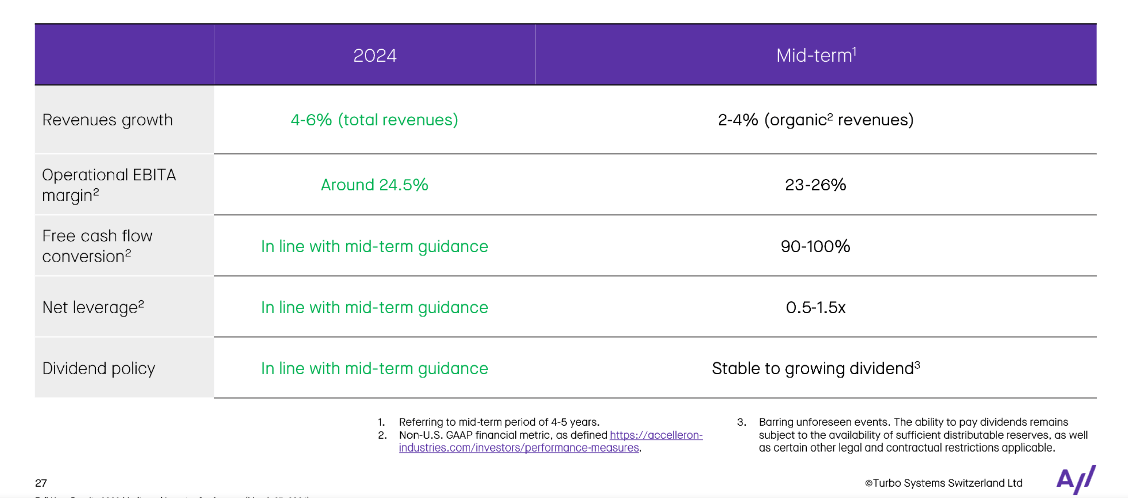

Within the medium time period, there are some tailwinds that may present progress alternatives for the corporate, together with robust knowledge middle progress a lot of which use turbochargers for his or her emergency backup energy turbines. The corporate can also be benefiting from some hard-to-decarbonize sectors, comparable to delivery, the place stricter rules are pushing shipowners to order dual-fuel vessels.

These twin gasoline engines have a constructive influence on Accelleron provided that they require a better quantity and extra superior gasoline injectors, and the demanded elevated effectivity and gasoline flexibility necessities make including turbochargers extra enticing, and in some circumstances even important. Regardless of these tailwinds, the mid-term natural progress goal shouldn’t be notably enticing at solely 2% to 4%. Longer-term we consider the corporate would possibly even expertise adverse progress if sectors like delivery begin electrifying.

Accelleron Industries Investor Presentation

Valuation

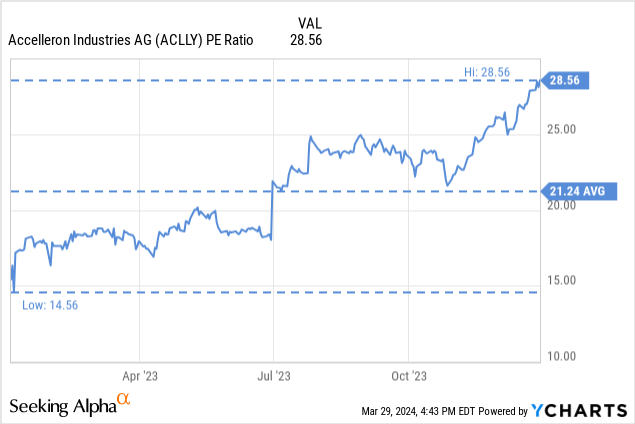

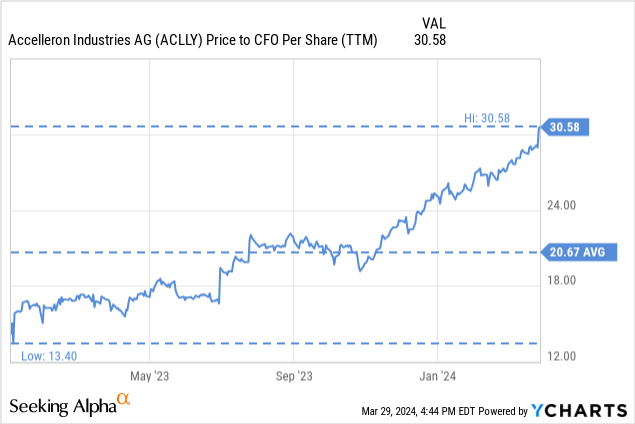

Many of the worth appreciation has clearly been the results of a number of growth, and now we have a tough time understanding why traders could be keen to pay expertise firm multiples for an industrial enterprise with comparatively poor progress prospects.

We discover the latest run-up in worth of the final 3-4 months notably tough to elucidate, as there have been no main developments from the corporate throughout this era.

Given the poor mid-term progress prospects of two% to 4% natural progress, mixed with a worth to money movement from operations above 30x, we’re additional downgrading the shares to “Strong Sell”.

With the corporate paying out most of its earnings as dividends, and the ahead dividend yield presently at ~2.5%, we don’t see a lot to get enthusiastic about. The dividend yield is low and given the excessive payout ratio and low natural progress, the prospects of seeing the dividend develop meaningfully going ahead should not nice.

Dangers

We see two main dangers for Accelleron Industries traders, one is the elevated valuation for an industrial firm with mediocre progress prospects. The second is probably ten or twenty years forward, however we do consider that even industries like delivery will finally electrify. Battery prices proceed to see vital worth declines and efficiency enhancements. It’s due to this fact solely a matter of time for electrical ships to turn into a actuality. The query is usually when, not if, and that’s the reason we consider traders ought to pay a low a number of for the enterprise.

Conclusion

After reviewing full 12 months 2023 outcomes for Accelleron Industries, we’re downgrading our ranking to “Strong Sell”. Monetary efficiency was not notably dangerous, and we didn’t discover something notably troubling with the outcomes. It’s merely a matter of valuation multiples increasing, whereas enterprise outcomes clearly don’t warrant such will increase. The corporate is already paying out most of its earnings as dividends, the dividend yield is comparatively low, and we don’t see a lot room for dividend progress sooner or later.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please concentrate on the dangers related to these shares.