GrandviewGraphics/iStock through Getty Pictures

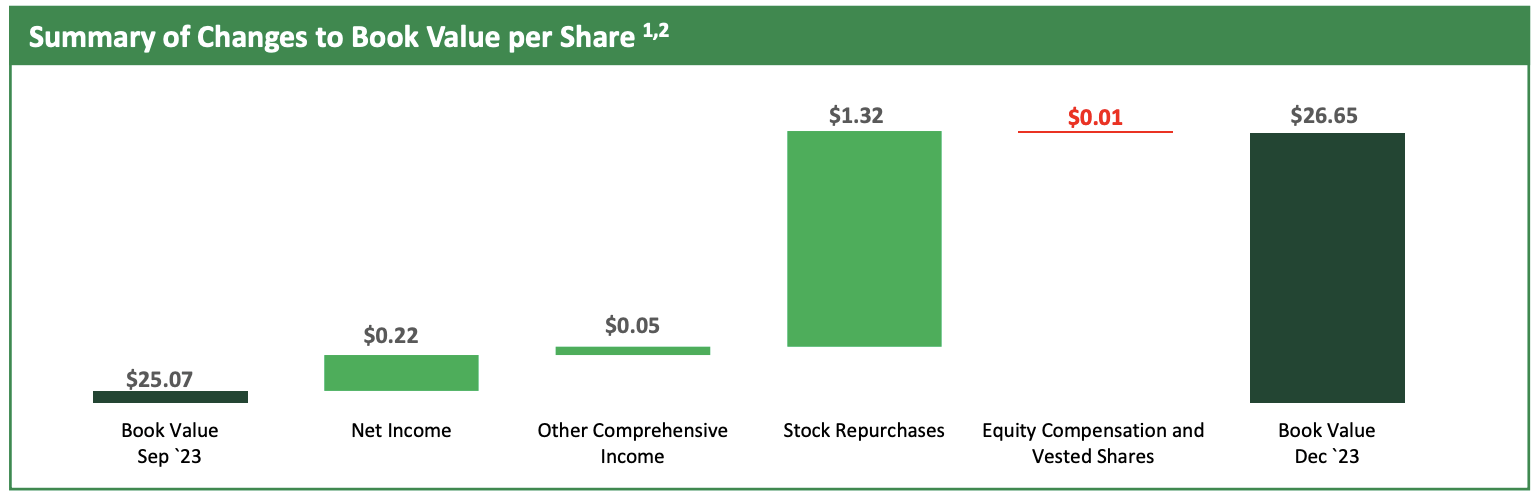

ACRES Business Realty’s (NYSE:ACR) exceptional low cost to its e-book worth stays steep even after its 50% 1-year rally. The business mortgage REIT final reported a GAAP e-book worth per share of $26.65 at the top of its fiscal 2023 fourth quarter, this was a sequential enhance of $1.58 per share totally on the again of the mREIT’s inventory buyback program that noticed its weighted common variety of excellent shares finish the fourth quarter dip 2.78% year-over-year to eight,566,058. ACR at its present $14.09 inventory worth is swapping arms at a big 47% low cost to e-book worth. This system has roughly $9.8 million left after the buyback authorization was expanded by $10 million in November.

ACRES Business Realty Fiscal 2023 Fourth Quarter Presentation

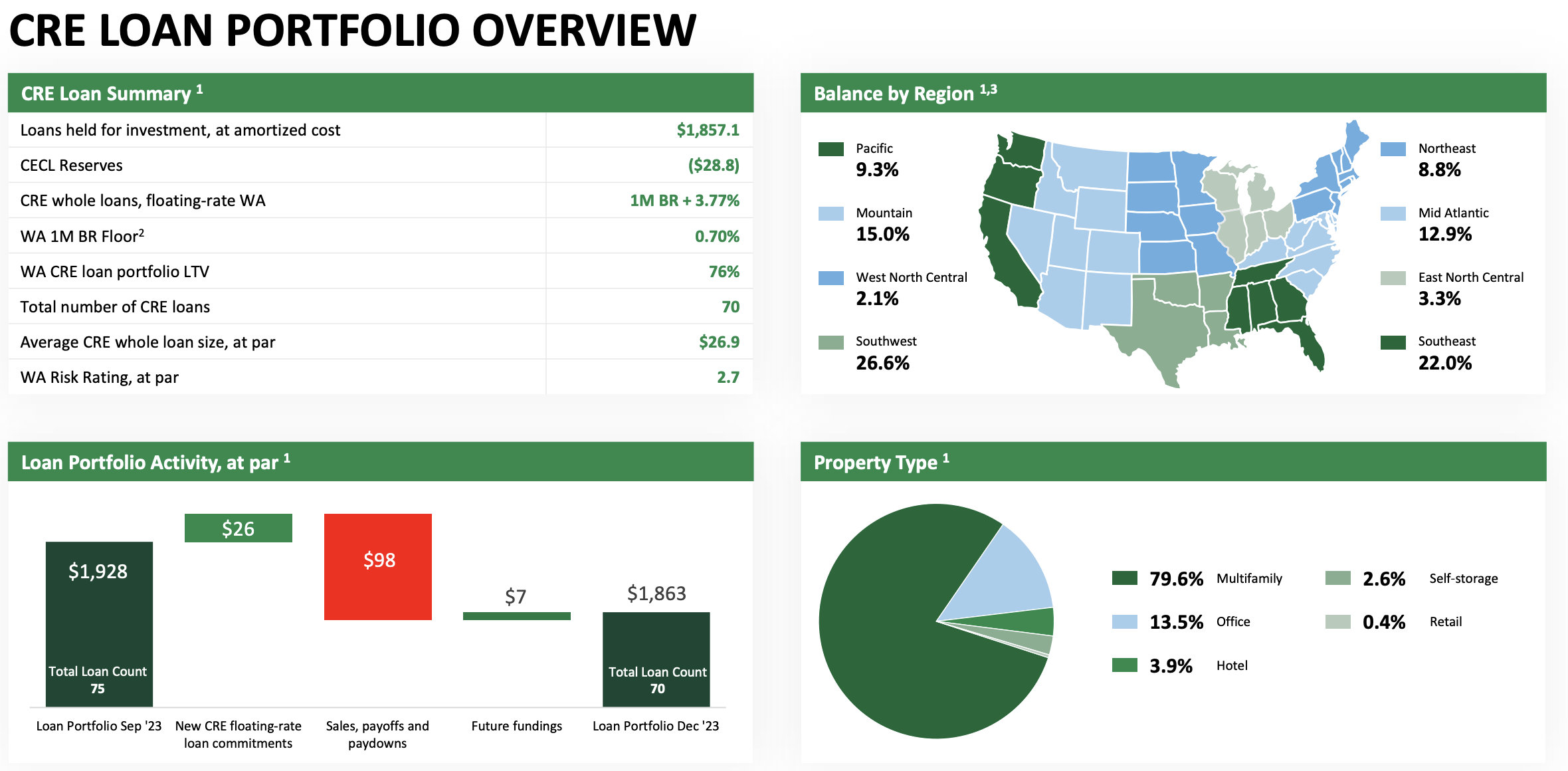

ACR’s mortgage portfolio on the finish of the fourth quarter stood at $1.86 billion earlier than a $28.8 million allowance for credit score loss. The mREIT is heavy on multifamily loans which represent 79.6% of its CRE mortgage portfolio with workplace loans the second largest section at 13.5%. There’s additionally broad US geographic diversification with 70 loans on the finish of the fourth quarter priced at 3.77% over the one-month benchmark charges. The funding play right here is that ACR will be capable of shut the low cost to e-book worth on the again of robust underwriting high quality, its buyback program, and the continued development of e-book worth per share. Holding allowance for credit score losses and nonperforming loans low will kind essential tenets of the bull case.

ACRES Business Realty Fiscal 2023 Fourth Quarter Presentation

Underwriting High quality, Threat, And Liquidity

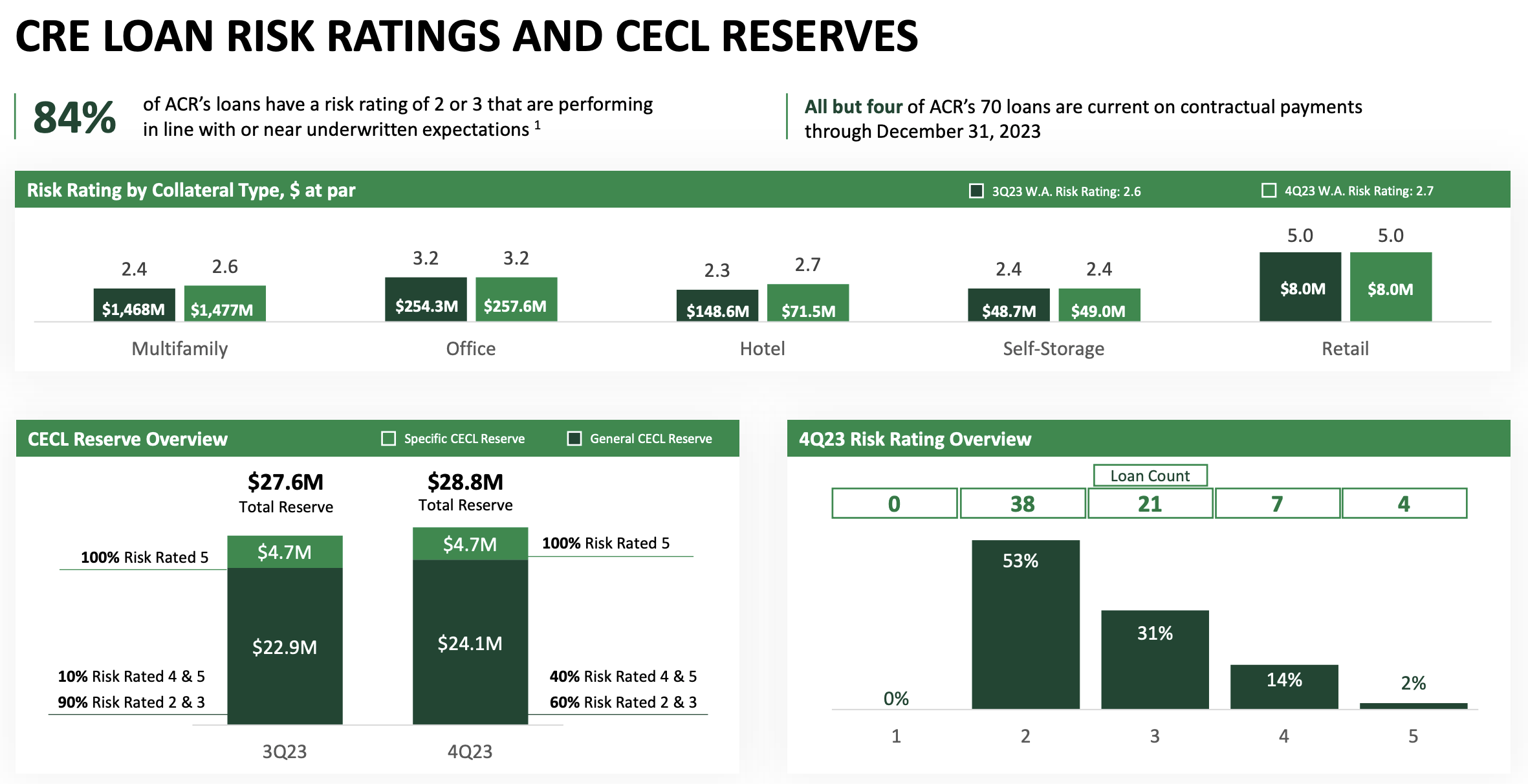

The market has discounted ACR by 50% due to uncertainty over the path of US CRE. This a part of the economic system has turn out to be the inventory market boogeyman and in keeping with bears the harbinger of doom for all the US monetary system. Nevertheless, ACR’s intrinsic concentrate on multifamily loans means its portfolio is best shielded from the uncertainty wrought by the rise of work-from-home workplace emptiness charges. Roughly 84% of ACR’s loans had a danger ranking of two or 3 on the finish of the fourth quarter with 4 loans not performing in step with contractual obligations. This was a sequential deterioration from 92% of loans with a danger ranking of two or 3 on the finish of the third quarter.

ACRES Business Realty Fiscal 2023 Fourth Quarter Presentation

ACR’s CECL reserve at $28.8 million was up $1.2 million from the third quarter as the chance ranking of its multifamily loans worsened barely, rising to 2.6 from 2.4 on the finish of the third quarter. Nevertheless, CECL reserves at simply 1.55% of ACR’s mortgage portfolio spotlight the advantages of the mRETI’s concentrate on multifamily properties and wholesome underwriting requirements. ACR’s complete funding portfolio stood at $2.02 billion on the finish of the fourth quarter, up marginally sequentially with the mREIT holding $158.9 million in internet investments in actual property and properties held on the market. Accessible liquidity on the finish of the fourth quarter stood at $108 million, shaped from $83 million of money and $25 million of projected financing out there on unlevered belongings.

ACRES Business Realty Fiscal 2023 Kind 10-Ok

The Preferreds And The Fed

| Most popular sequence | Low cost to liquidation worth ($25) | Annual distribution | Yield on price % | Floating date |

| 8.625% Mounted-to-Floating Collection C Cumulative Preferreds (NYSE:ACR.PR.C) | -3% ($24.20) | $2.16 | 8.91% | 7/30/2024 |

|

7.875% Collection D Cumulative Redeemable Preferreds (NYSE:ACR.PR.D) |

-14.2% ($21.45) | $1.96875 | 9.18% | N/A |

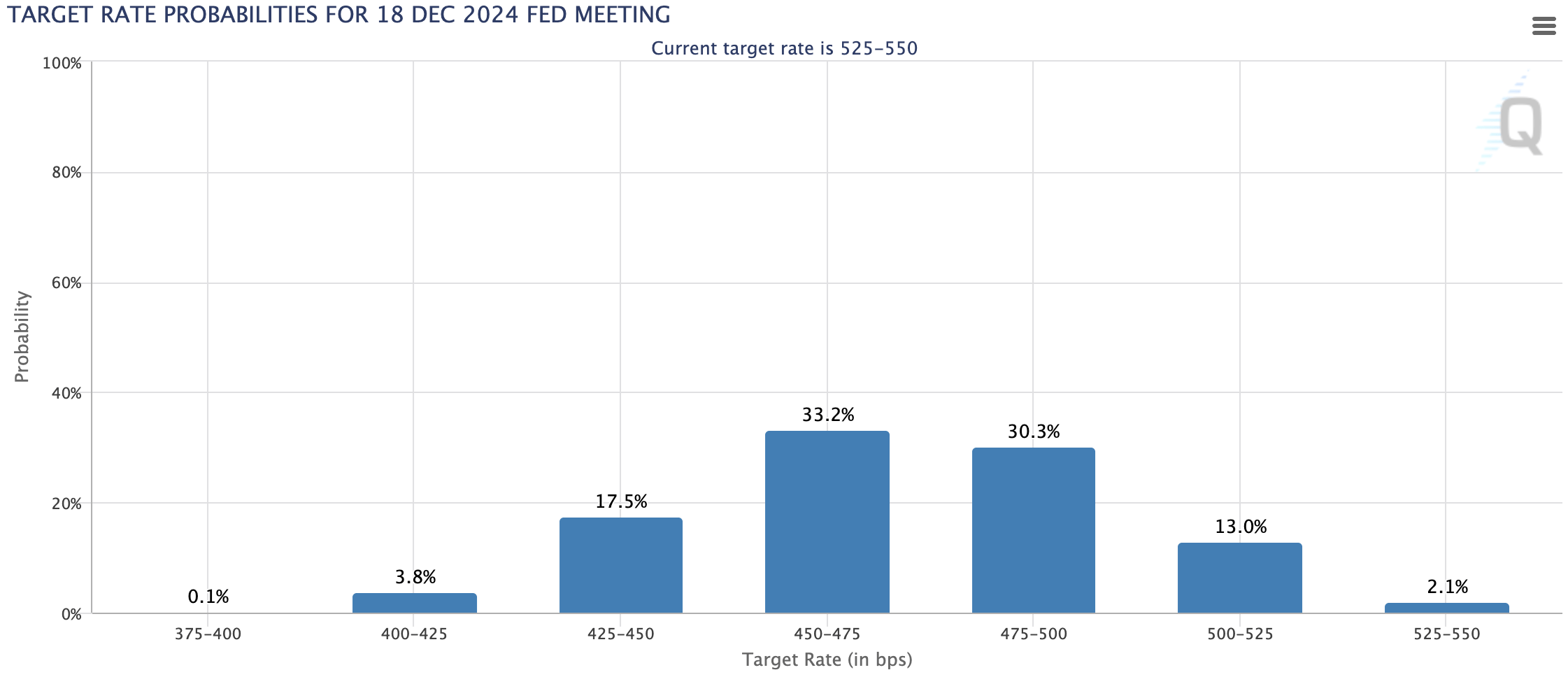

ACR has two excellent preferreds (ACR.PR.C) and (ACR.PR.D) providing wholesome funding profiles. The Collection D is buying and selling at a double-digit 14.2% low cost to their $25 per share liquidation worth and presently pays a $1.96875 annual coupon for what works out to be a 9.18% yield on price. I am closely leaning towards the Collection C right here although. The low cost to liquidation is decrease at 3% however they’re floating fee from the top of July. This will likely be at a fee equal to three-month SOFR plus an expansion of 5.927% per yr and topic to a ground of 8.625%. Three-month SOFR is presently at 5.34775% with an extra 0.26161% adjustment to be added because the preferreds have been initially priced utilizing LIBOR. Therefore, the combination coupon assuming no Fed fee cuts by this date can be 11.5%.

CME FedWatch Device

The Fed is anticipated to chop charges by at the least 75 foundation factors via 2024 with the CME FedWatch Device pricing in base rates of interest at 4.50% to 4.75% on the finish of the yr. Therefore, this floating coupon on the Collection C ought to nonetheless be double-digit on the finish of the yr with the potential low cost additionally closed because of the constructive period impact of pending Fed fee cuts. I am ranking each the commons and the preferreds as buys right here and I am going to look to take a place within the Collection C someday in April. The close to 50% low cost to e-book of the commons is much too steep for ACR’s multifamily heavy portfolio and the market has bought off the inventory too cheaply in what can solely be classed as an overreaction to CRE angst.