santosha/E+ through Getty Photographs

Thesis

I price Adecoagro S.A. (NYSE:AGRO) a Maintain with an end-of-year worth goal of $14.41, which represents a possible 30% upside to its present worth of ~$10.80/share.

Utilizing an EV/EBIT a number of of 10x and estimating the EBIT throughout AGRO’s three largest segments, Sugar & Ethanol, Rice, and Dairy, my mannequin suggests AGRO’s share worth to be price upwards of $14.41 by the top of 2024, contingent on sugar costs round or above 20 cents/lb. In comparison with years prior, Adecoagro has diversified its earnings sources away from its sugar and ethanol enterprise, but, I’m unconvinced this can suffice in opposition to a heavy downturn in sugar costs.

Enterprise Overview

Adecoagro is an built-in producer of uncooked and processed agricultural items in South America. The corporate is headquartered in Luxembourg, however operates farms in Brazil, Argentina, and Uruguay. In Argentina, the corporate owns and operates: 18 farms, 4 diary milking amenities, 2 milk processing amenities, 4 rice mills, 1 peanut plant, 1 sunflower plant and a pair of grain dealing with crops. In Brazil, AGRO holds 7 farms and three sugar and ethanol processing mills. In Uruguay, AGRO holds one rice farm, and one rice mill. Roughly 45% of AGRO’s belongings are situated in Argentina, 46% in Brazil and 4% in Uruguay. Adecoagro’s core enterprise is its Sugar and Ethanol division (S&E) which flexibly produces sugar and/or ethanol to maximise earnings, and sells extra power provides to the Brazilian grid. The corporate focuses on a round enterprise mannequin that returns farming byproducts, like sugarcane bagasse and cow manure methane, again into the manufacturing course of.

Gross sales

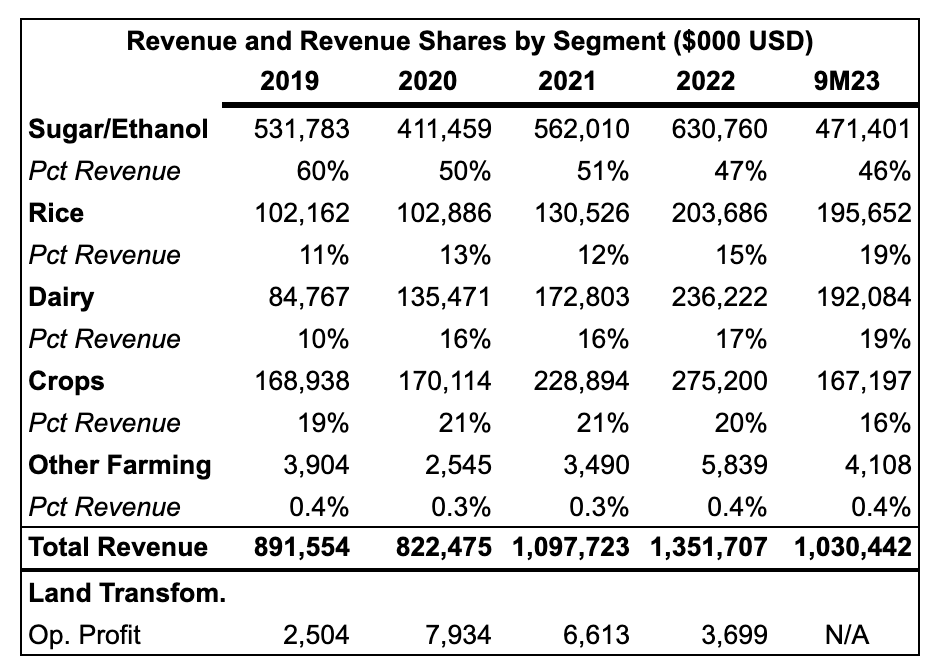

AGRO reviews 5 core segments: Sugar and Ethanol (S&E), Dairy, Rice, Crops, and Land Transformation. The desk under summarizes the distribution of gross sales throughout these segments.

SEC Filings, AGRO Investor Relations

Sugar and Ethanol

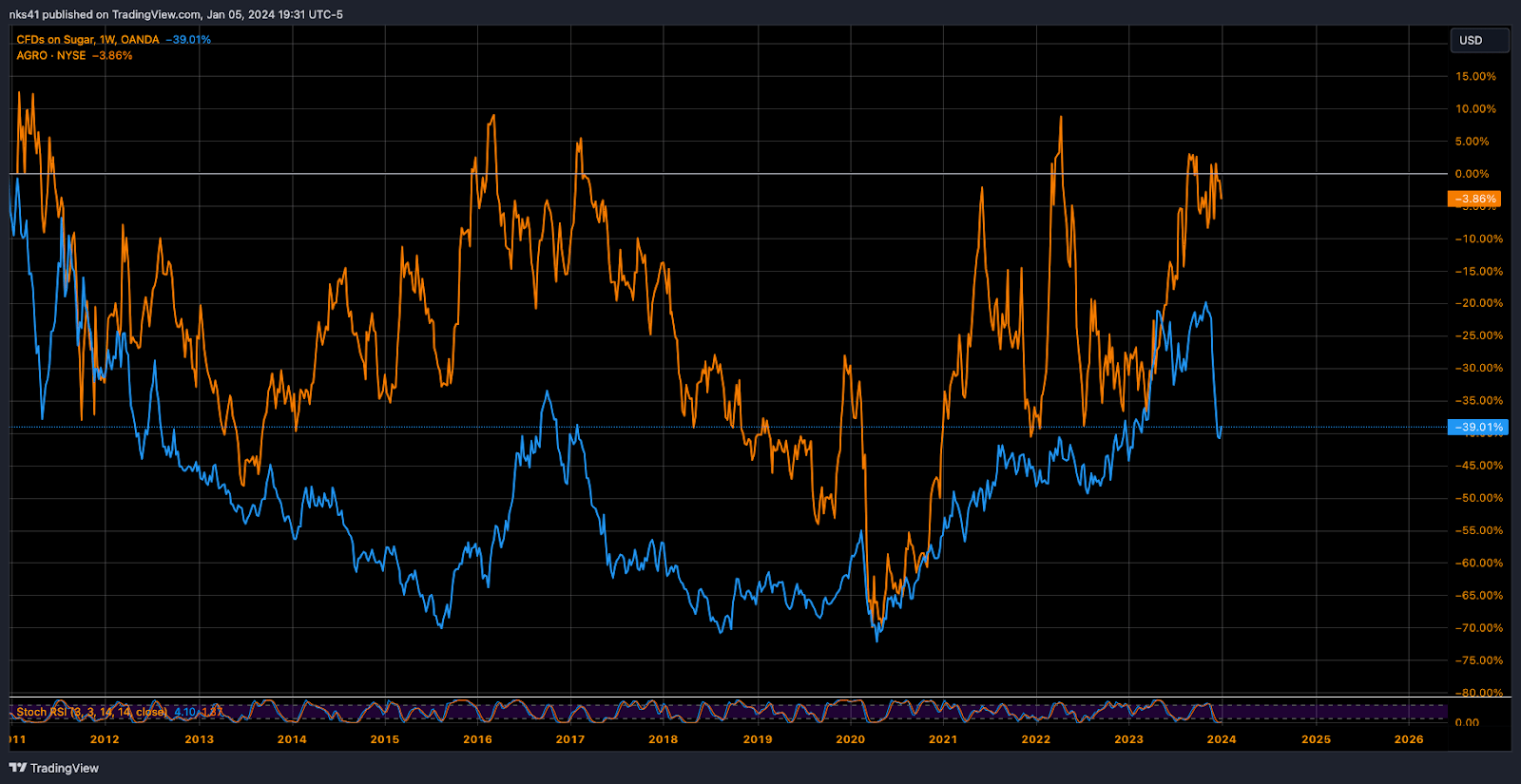

AGRO inventory versus sugar spot costs (Tradingview)

Adecoagro grows sugarcane yr spherical to provide sugar or ethanol. The chart above captures the connection between sugar costs and AGRO’s inventory worth. he costs of sugar, ethanol, petroleum and AGRO’s inventory are positively correlated, which makes AGRO, in some sense, an power play. In spite of everything, sugarcane is mom nature’s best transformer of photo voltaic power. Brazil, together with the US, is among the largest producers of ethanol, due to nationwide transportation legal guidelines. The Brazilian sugar manufacturing market is very aggressive and benefits between producers are scarce; AGRO owns solely 3 of the roughly 240 sugar mills in Brazil. A part of Adecoagro’s technique and working effectivity turns sugar milling byproducts into ethanol to energy its mills, vehicles and farm gear. Within the first 9 months of 2023, AGRO milled 9.6 million tons of sugarcane, up 30.6% yr over yr, and elevated yields by 28% as a consequence of enhancing climate.

Rice

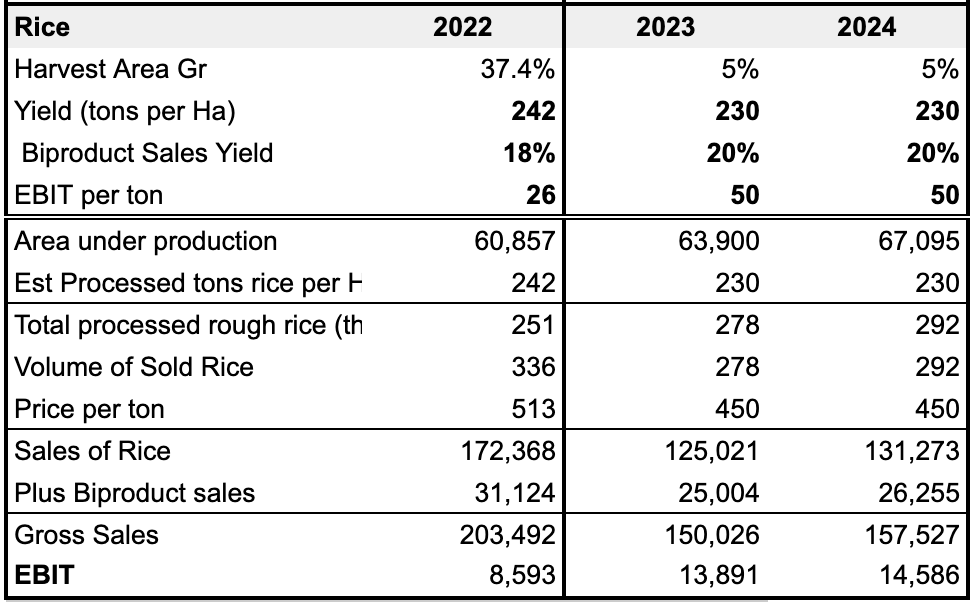

Adecoagro grows Indian and Japonica rice underneath 4 manufacturers: Adecoagro, Molinos Ala, Apostoles, 53 and Monte Alegre. In line with the corporate, Uruguay “is internationally recognized as being of the highest quality standards,” however my palate is simply too unsophisticated to note any distinction. In line with firm filings, Adecoagro sells roughly 13% of its rice within the Argentine retail market by means of three manufacturers, which collectively have a 15.3% market share. Moreover, the corporate urged within the Q2 2023 earnings call that they’re uniquely positioned to learn from a, “lack of water in many rice producing countries of the world, which are cutting their rice exports. This means that there will be a very clear need for South American rice”. Whereas this may occasionally have been true in 2023, I’ll depart the climate forecasting as an train to the readers. AGRO has been buying extra rice belongings during the last 2 years, and I see this as a internet optimistic, as direct-to-consumer (DTC) merchandise are a lot ‘stickier’ in pricing than promoting sugar on worldwide markets.

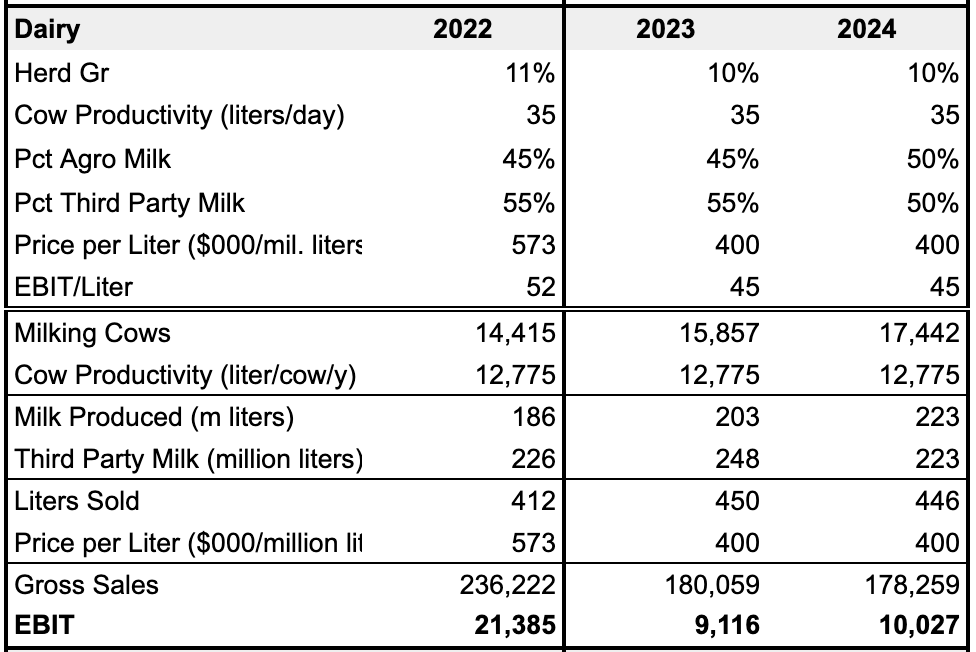

Dairy

Supplementing the rice merchandise, Adeco additionally sells milk DTC. AGRO was the primary firm in South America to implement free-stall milking, and in 2019 the corporate bought two milk processing crops in Argentina from SanCor, the biggest producer of dairy merchandise in South America. Via the Las Tres Ninas and Agelita manufacturers, AGRO affords a number of milks, lotions and cheeses. Of those merchandise, powdered milk and UHT fluid milk comprise 80% the dairy unit’s revenues. Roughly 40-50% of AGRO’s complete milk gross sales originate from the corporate’s herd whereas the remaining portion is bought from native producers and processed in AGRO’s amenities.

Crops, Land Transformation and Different

All different farm product revenues are consolidated in AGRO’s Crops division, grown largely in Argentina. This consists of soybean, corn, wheat, peanut, sunflower and cotton. Of those merchandise, corn, soybean, and peanuts make up the majority of the unit’s gross sales. As talked about in its annual report, “Argentina is positioned among the most important players in the production and export of peanuts, with high technological levels both in terms of production as well as processing. Argentina exports more than 90% of the peanuts it produces and its main market is the E.U.”

Along with farming, AGRO manages a “Land Transformation” division that buys and develops property for agricultural use. The corporate’s three transformation methods/targets are: Undeveloped land (savannahs and pure grasslands), Undermanaged or underutilized farmland (cultivated pastures and poorly managed agriculture), and Ongoing transformation of arable land. In September 2023, the corporate offered its 6,302 hectare “El Meridiano” farm for $48 million USD, or $7,681/hectare, 30% above the assessed worth carried on its books. In complete, AGRO owns 233,941 hectares assessed at a price of $745,301 USD, or $3,186/Ha.

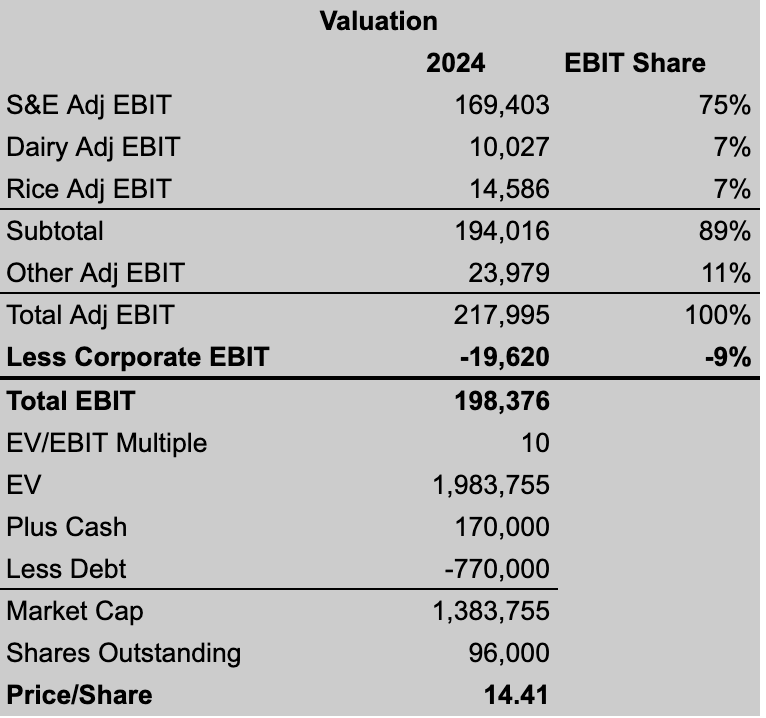

Valuation – Adecoagro

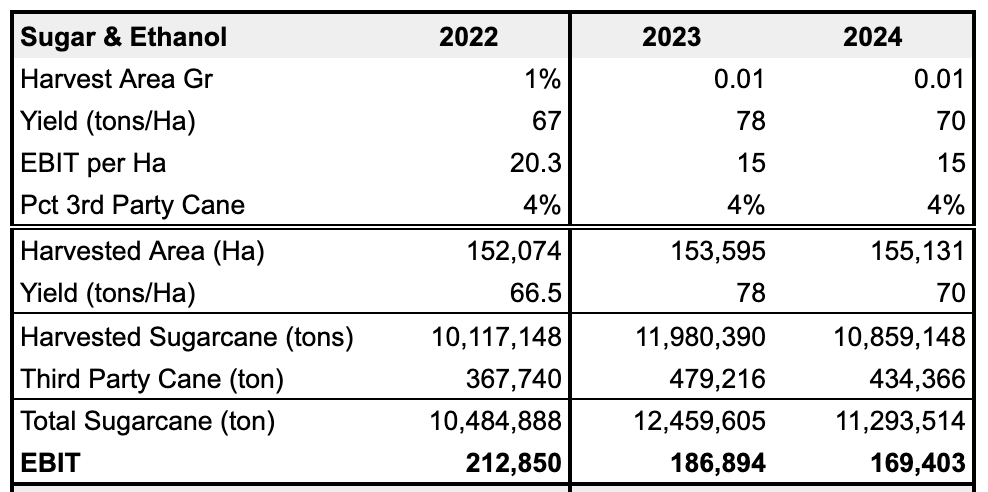

To worth AGRO, I exploit a SOTP evaluation to estimate 2024 EBIT numbers from the three largest and quickest rising segments, Sugar & Ethanol, Dairy, and Rice. From there, I deduce the remaining share of EBIT from the opposite segments, Crops, and Land Transformation, to achieve my full 2024 estimation.

AGRO Investor Relations, Creator’s Work AGRO Investor Relations, Creator’s Work

AGRO Investor Relations, Creator’s Work

AGRO Investor Relations, Creator’s Work

Beneath these assumptions I calculate an intrinsic worth of $14.41. After all, that is only a near-term view. Shares may commerce increased if commodity costs transfer in a good route (up), AGRO makes extra accretive acquisitions within the Dairy and Rice areas, or the corporate buys again shares extra aggressively.

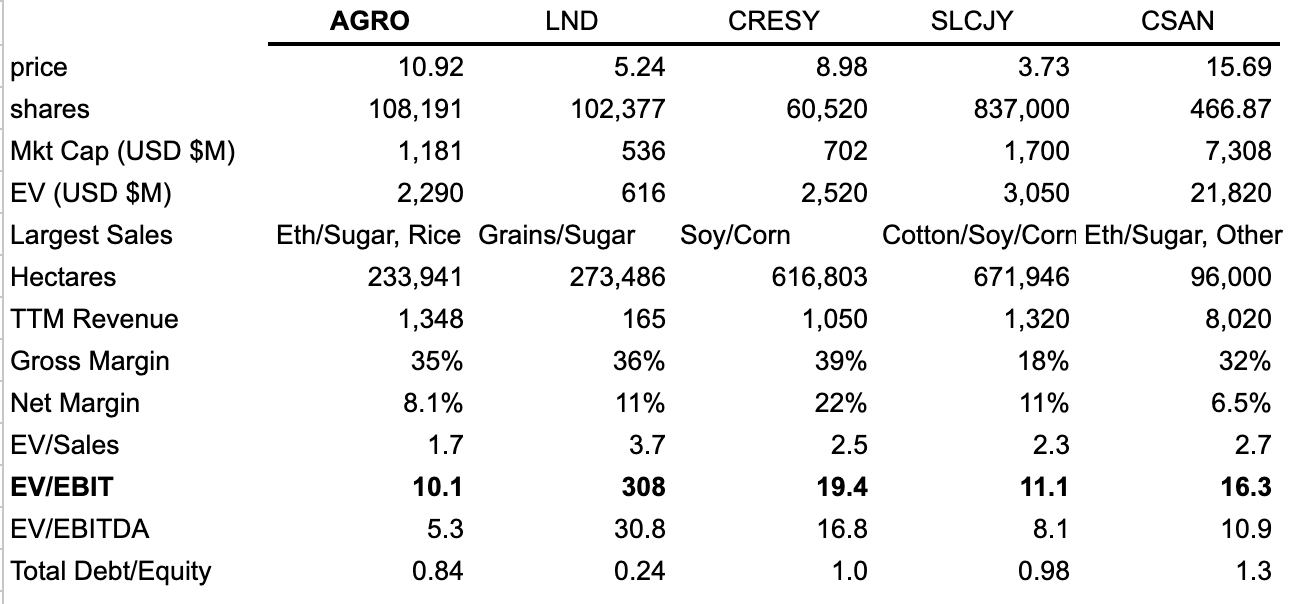

Comparables

Looking for Alpha, Tradingview, AGRO Investor Relations

The Brazilian sugar and ethanol trade is fragmented and aggressive. Meals manufacturing in South America is very industrialized and just a few firms are traded on American exchanges. Essentially the most comparable enterprise fashions to Adecoagro are: BrasilAgro (LND), Cresud (CRESY), SLC Agricola (OTCPK:SLCJY), and Cosan (CSAN). Of the businesses within the desk above, AGRO competes most instantly with CSAN’s Raizen subsidiary, a three way partnership between Shell and Cosan, the main particular person exporter of sugar on the planet. Raizen sometimes mills 4 to five occasions the quantity of sugar of AGRO. Nevertheless, the place AGRO lacks in dimension, it makes up for in crop flexibility and product range. Moreover, AGRO has increased present margins, much less leverage and is cheaper on all the supplied metrics.

One other focal point is the connection between AGRO, LND and CRESY. Soros’ Quantum fund was an preliminary investor in AGRO and managed the agency’s IPO in 2011. In 2017, Quantum exited the place on the prime, and the inventory declined from its excessive of $12 to $3.30 by March of 2020. Equally, LND IPO’d in 2011, too, however as a derivative to consolidate Cresud’s agriculture belongings in Brazil. Cresud’s founder, Argentine actual property mogul Eduardo S. Elsztain, is a former protege of Soros, who personally seeded Cresud with a $10 million greenback funding over three a long time in the past. On the identical time Quantum exited AGRO, Cresud’s subsidiary LND inventory was exiting a painful backside. Since Quantum’s divestment in 2017, AGRO’s share worth has barely made a spherical journey again to $12 whereas LND has returned practically 140%. I have no idea why Quantum divested from AGRO in 2017, however I discover this collection of occasions curious and related in contemplating the place the ‘large cash’ is positioned. Nonetheless, Alan Leland Boyce, former portfolio supervisor at Quantum, stays on AGRO’s board and holds a 1.1% share of the corporate.

Dangers

Mannequin Weak spot

My valuation depends closely on EBIT margins, or the EBIT per ton I assign to every phase. That is much less a weak point of the mannequin, and extra a weak point of the enterprise. A lot of Adecoagro’s prices are mounted, so within the quick time period, margins are decided extra by downstream costs than technical improvements. Maybe the expansion of the Dairy and Rice companies can complement AGRO’s different crops to the purpose the place the likelihood of a uniform decline in costs throughout a number of agricultural commodities is much less possible. Nonetheless, miscalculated hedging may end in vital losses. Within the 3Q conference call, “82% of [AGRO’s] sugar position remains open”. Since then, sugar costs have declined precipitously, and the corporate has communicated that they’ve hedged 31% of manufacturing at 24.1 ct/lb. Equally, managing 4 foreign currency echange presents separate hedging dangers.

Sugar is among the most risky ‘gentle’ commodities. (Tradingview)

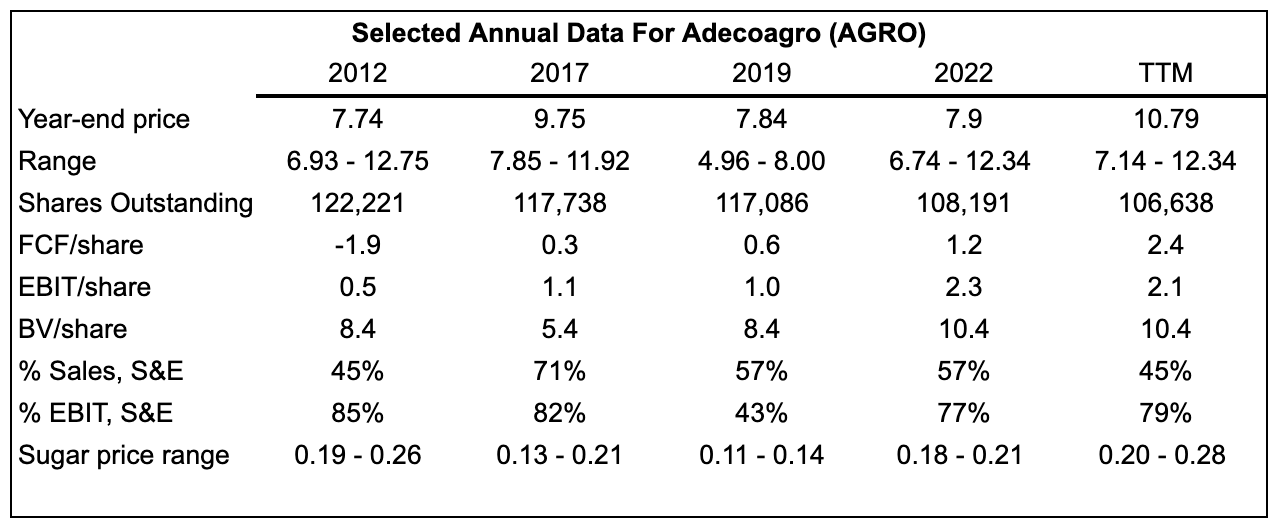

However let’s take one other take a look at 2017-when Soros & co exited their place on the prime. In 2016, southern India had considered one of its worst droughts in 140 years, decimating crops and eradicating Indian sugar from World markets (India confronted one other drought in 2023, once more driving up sugar costs). This monsoon-drought sample happens roughly each 7 years, and is a big pressure within the sugar worth cycle. Costs peaked above 23.50 c/lb within the Fall of 2016, and started 2017 at 20 c/lb, solely to say no to a low of 12.50 c/lb that summer season. Together with the worth of sugar, AGRO’s shares fell from $12 in January 2017, to $5 in September of 2019.

A snapshot of AGRO’s efficiency throughout numerous years throughout the sugar cycle. 2019 was one of many weakest years for shares for the reason that IPO. (Creator’s work, SEC filings)

In 2017 AGRO’s Sugar and Ethanol division accounted for 82% of EBIT and 71% of gross sales. In 2022, S&E accounted for 77% of EBIT and 57% of gross sales. Within the trailing twelve month interval, Sugar and Ethanol accounted for 79% of EBIT and 45% of gross sales. Regardless of sugar’s majority affect on the underside line, since 2017 the corporate has lowered share rely by 9%, initiated an annual dividend of $0.33 per share, and steadily elevated FCF per share.

Argentina

New president Javier Milei’s free-market philosophy bodes properly for AGRO, the place the corporate sells its common shopper milk, sugar and rice manufacturers and pays >30% company earnings tax. Milei’s presidency may usher in an financial growth for Argentina-or one other financial disaster-but it is nonetheless too quickly to inform. I think Milei’s first yr to be the bellwether for the next three years, so financial enhancements would translate to AGRO’s backside line no earlier than This autumn 2024.

Brazil, Ethanol Mixing, and Electrical Automobiles

Many developed international locations complement gasoline with ethanol to scale back emissions and to assist home sugar industries. In Brazil, the CIMA Decision No. 1, handed in 2015, established an ethanol mix in common gasoline of 25% to 27% %, the best on the planet. For context, different international locations’ fuel mix necessities are: UK 10%, US 10%, Argentina 12%, Canada 5%. India has focused a 20% requirement by 2025, and extra international locations are contemplating such insurance policies. Though this adoption of flex-fuel is a tailwind for AGRO, if EVs are the terminal resolution for clear transportation, the sugar trade could be in for a impolite awakening. Within the close to future, although, Brazil appears set on quietly supporting ethanol gas over EV adoption.

Remaining Ideas

My evaluation right here outlines Adecoagro’s place within the South American industrial agriculture house, and supplies a 12-month worth goal. Wanting past the following yr or two, I’d slot AGRO in Charlie Munger’s notorious ‘too laborious’ pile. For lots of the top-down justifications of AGRO, there are less complicated performs. Bullish on sugar? Simply purchase sugar futures. Suppose the Age of Argentina is upon us? MELI has you lined. Enthusiastic about Selic price cuts? The IBZL ETF will do. There are lots of inherent dangers for an Argentine industrial farmer, not less than trying in from the USA. Finally, what makes me nervous about Adecoagro’s enterprise is its place as a price-taker promoting to a world market. After all, there are numerous industrial farmers who’ve change into very rich, so I (most likely) basically misunderstand the enterprise.

My mannequin means that, based mostly on 2024 revenues, the inventory must be price round $14 or $15 {dollars} a share. This situation is, I’ve little or no information of the sugar markets, and can’t suggest shopping for this late within the sugar cycle. Bulls will say that AGRO is a basically higher enterprise than when it IPO’d in 2011. AGRO actually is extra superior than it was over a decade in the past when evaluating crop yields, that is true. So, was Adecoagro a special firm in 2017? I am going to depart the reply as much as you.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please concentrate on the dangers related to these shares.