We Are

The ADBE Funding Thesis Is Even Extra Engaging After The Latest Pullback

Adobe (NASDAQ:NASDAQ:ADBE) together with Autodesk (ADSK) are two shares that doesn’t require an introduction certainly, provided that I’m a licensed architect with almost twenty years of cumulative schooling and expertise.

With ADBE providing a properly diversified SaaS choices throughout picture, design, and video functions generally used within the enterprise and business markets, it’s unsurprising that sure platforms are nearly synonymous to the corporate, together with Adobe Photoshop and Adobe Acrobat Professional – PDF.

As a enjoyable reality, Paramount’s Prime Gun: Maverick (PARA) and Disney’s Avatar: The Means Of Water (DIS) had been completely edited on Adobe Premiere Pro, additional highlighting its globally profitable SaaS platform.

ADBE’s shift from one-time perpetual license enterprise mannequin to the month-to-month/ annual subscription enterprise mannequin since 2011/ 2012 was extremely strategic as properly, because it had contributed to its double digit progress over the previous decade.

This has additionally defined the SaaS firm’s double beat FQ1’24 earnings name, with revenues of $5.18B (+2.7% QoQ/ +11.3% YoY) and adj EPS of $4.48 (+4.9% QoQ/ +17.8% YoY).

The high-margin SaaS enterprise mannequin can be noticed within the firm’s rising working margins of 36.8% (+2.3 factors QoQ/ +2.7 YoY) and adj Free Money Circulate margins of 41.1% (+10.4 factors QoQ/ +6.9 YoY), after accounting for the $1B termination cost associated to the abandoned Figma acquisition.

A lot of ADBE’s strong Free Money Circulate technology has been put to nice use certainly, as noticed within the 3.2M or the equal -0.6% of its float retired over the past twelve months, and 35.3M/ -7.1% since FY2019.

That is additional demonstrated by the outsized $25B share repurchase program by way of 2028, implying the administration’s confidence of constantly producing strong money flows forward.

On the identical time, the SaaS firm reported a more healthy stability sheet, with a internet money state of affairs of $4.12B (+17.3% QoQ/ +103.9% YoY) by the most recent quarter, additional underscoring why the deserted Figma acquisition has been a blessing in disguise, attributed to the overly hefty price tag of $20B.

As a SaaS firm, we imagine that ADBE is one that’s extremely worthwhile, with a wholesome stability sheet and wonderful shareholder returns to date.

ADBE’s AI Monetization Is On The Proper Path – Sluggish & Regular Wins The Race

Whereas ADBE has met its share of generative AI delays by way of the supposedly ethical Firefly platform as its rivals forge on, readers could wish to be aware that it’s not the one firm going through this challenge.

For context, the market seems to be overly essential about ADBE’s AI monetization path, with a lot of the generative AI capabilities being incremental enhancements within the shopper engagement and value-add companies.

The administration has additionally opted to introduce a credit pricing plan for Firefly, as a substitute of a standalone subscription platform, whereas integrating the AI functionality throughout its current enterprise choices.

On the one hand, we will perceive why the market could have been dissatisfied with ADBE’s slower monetization path, particularly when in comparison with the double digit growths reported by different generative AI SaaS suppliers, akin to Palantir (PLTR), Microsoft Azure (MSFT), and CrowdStrike (CRWD).

Alternatively, given the breadth of ADBE’s enterprise choices together with the potential intellectual property headwinds, we imagine that the administration’s prudence by way of the moral Firefly platform is extremely strategic to the longevity of its enterprise certainly.

That is particularly since as much as 59% of its customer base employs over 5K staff and as much as 64% generates over $1B in annual income, the place copyright infringement is just not an possibility.

Whereas we could also be mistaken, during which ADBE’s Firefly could fail to achieve traction in addition to how its begin up friends have, together with Secure Diffusion, Midjourney, and OpenAI’s DALL-E 3, we preserve our perception that it’s extra essential that the previous to safeguard its core enterprise clients’ pursuits.

With Alphabet’s Gemini (GOOG) and Microsoft-backed OpenAI’s GPT-4 (MSFT) nonetheless reporting hallucination points to date, we imagine that the trail towards a really sustainable AI monetization stays bumpy and prone to be fraught with authorized challenges.

For now, ADBE could have provided a supposedly softer FQ2’24 steerage, with revenues of $5.275B (+1.8% QoQ/ +9.6% YoY) and adj EPS of $4.375 (-2.3% QoQ/ +11.8% YoY) lacking the consensus estimates of $5.31B (+2.5% QoQ/ +10.3% YoY) and $4.38 (-2.2% QoQ/ +12% YoY), respectively.

Nevertheless, we’re not overly involved certainly, given the strong moat attributed to the rising demand for its SaaS choices and the inherent stickiness of its shopper base. This has been demonstrated by the rising multi-year Remaining Performance Obligations of $17.58B (+2% QoQ/ +15.5% YoY) by FQ1’24.

That is on prime of the strong progress reported in ADBE’s Digital Media Annualized Recurring Income [ARR] to $15.76B (+3.8% QoQ/ +15.2% YoY), Inventive ARR to $12.78B (+3.3% QoQ/ +13.2% YoY), and Doc Cloud ARR to $2.98B (+6% QoQ/ +24.6% YoY) within the newest quarter.

These numbers show that its core customers are unfazed by the generative AI headwinds, notably attributed to the SaaS firm’s strong moat throughout the picture, design, and video functions, with it commanding the market leading share of 80.1% within the international enterprise course of administration (graphics) software program distributors as of February 2024.

Shifting ahead, readers could wish to monitor ADBE’s AI technique, for the reason that slower monetization has instantly triggered the administration’s softer ahead steerage and the market’s discounting of its FWD valuations, triggering dangers to its long-term funding thesis within the quick tempo generative AI race.

Nevertheless, with the generative AI beta companies nonetheless within the ramping stage by way of Q2’24, we imagine that it could be extra prudent to attend for excellent news in H2’24 as a substitute, primarily based on the CFO’s latest commentary within the FQ1’24 earnings name:

We’re ramping Firefly Companies and Specific and Enterprise. As we talked about, we noticed an excellent starting of that rollout on the — towards the tip of Q1. We additionally count on to see the second half ramping with Specific Cell and AI Assistant coming by way of. So now we have a number of the back-end capabilities arrange in order that we will begin monetizing these new options that are nonetheless largely in beta beginning in Q3 and past…

As now we have now launched the brand new pricing for CC with Firefly, and total, the roll-off of the prior pricing is extra important than the brand new pricing that we have launched. (Seeking Alpha)

So, Is ADBE Inventory A Purchase, Promote, or Maintain?

ADBE 5Y Inventory Worth

Buying and selling View

For now, ADBE has retraced dramatically from its 2024 prime, whereas buying and selling manner beneath its 50/ 100/ 200 day transferring averages because it seems to retest the earlier help ranges of $470s.

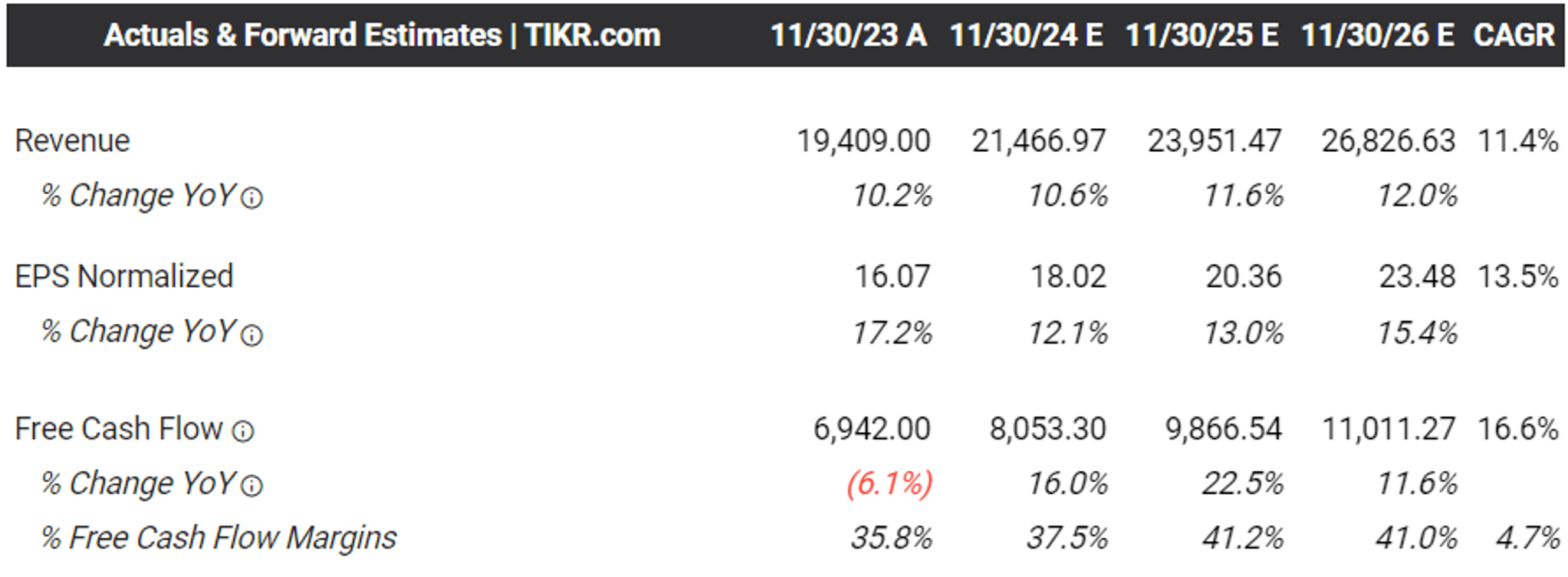

The Consensus Ahead Estimates

Tikr Terminal

Because of the administration’s softer FQ2’24 earnings steerage, we will additionally perceive why the consensus have quickly downgraded their ahead estimates, with ADBE anticipated to generate a decelerating prime/ backside line growth at a CAGR of +11.4%/ +13.5% by way of FY2026.

That is in comparison with the earlier estimates of +12.9%/ +14.1% and the historic progress of +18.7%/ +27% between FY2016 and FY2023, respectively.

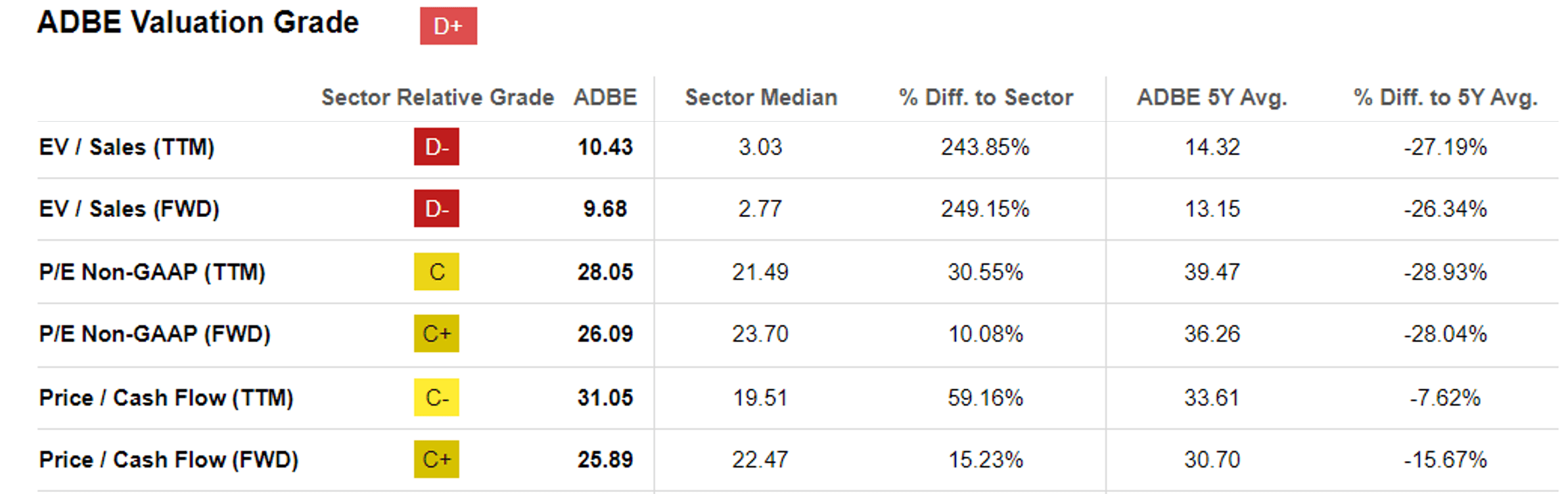

ADBE Valuations

Searching for Alpha

In consequence, we will perceive why the market has reasonably discounted ADBE’s FWD P/E valuations to 26.09x and Worth/ Money Circulate valuations to 25.89x, in comparison with its 1Y imply of 30.33x/ 28.50x and 3Y pre-pandemic imply of 32.68x/ 28.51x, respectively.

Nevertheless, because the SaaS enterprise matures from excessive double digit growths throughout the pre-pandemic to low double digits growths throughout the hyper-pandemic, we imagine that ADBE’s valuation normalization is to be anticipated.

Even when in comparison with its different enterprise SaaS friends, akin to Microsoft (MSFT) at 35.35x/ 27.96x, Oracle (ORCL) at 21.46x/ 17.46x, ADSK at 28.43x/ 33.23x, we imagine that ADBE seems to be pretty valued right here.

That is particularly after evaluating ADBE’s ahead estimates to MSFT’s projected prime/ backside line progress at a CAGR of +14.7%/ +16.9%, ORCL at +8.4%/ +11.7%, and ADSK at +10.4%/ +11.2% by way of 2026, respectively.

For now, primarily based on the LTM adj EPS of $16.76 and the discounted FWD P/E valuations of 26.09x, ADBE seems to be buying and selling above our truthful worth estimates of $437.20, with a notable premium of +8.9% at present ranges.

Regardless of so, primarily based on the consensus FY2026 adj EPS estimates of $23.48, there appears to be a superb upside potential of +28.6% to our long-term worth goal of $612.50, due to the SaaS firm’s double digit EPS progress by way of FY2026.

Because of the comparatively engaging danger/ reward ratio after the latest pullback, we’re cautiously ranking ADBE as a Purchase, although with no particular entry level because it depends upon particular person investor’s greenback value common and portfolio allocation, given the large differential between the truthful worth and long-term worth goal.

Given the market’s over-reaction to the supposedly softer FQ2’24 steerage, it could be extra prudent to look at the inventory’s motion for a bit of longer, earlier than including as soon as a flooring has materialized, possible between the earlier buying and selling ranges of between $420s and $450s for an improved margin of security.