germi_p/iStock Editorial by way of Getty Photos

Introduction

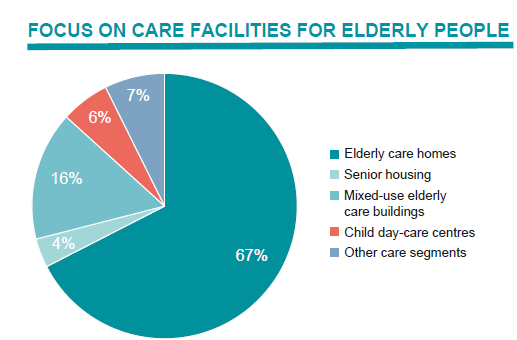

Aedifica (OTCPK:AEDFF) is a Belgian REIT specializing in healthcare actual property, with a really particular give attention to nursing properties and different services for the getting older inhabitants.

Aedifica Investor Relations

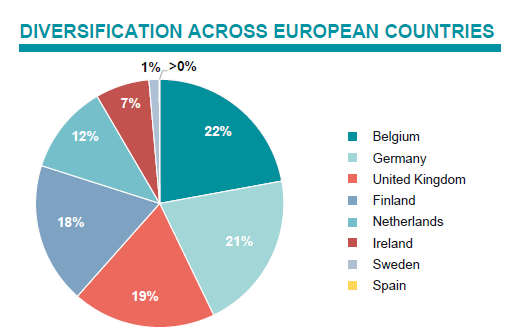

The REIT is energetic in a number of nations and as you’ll be able to see beneath, there aren’t any main variations between the 4 largest markets of Aedifica as Germany, Belgium, the UK, and Finland are all accounting for roughly 20% of the portfolio.

Aedifica Investor Relations

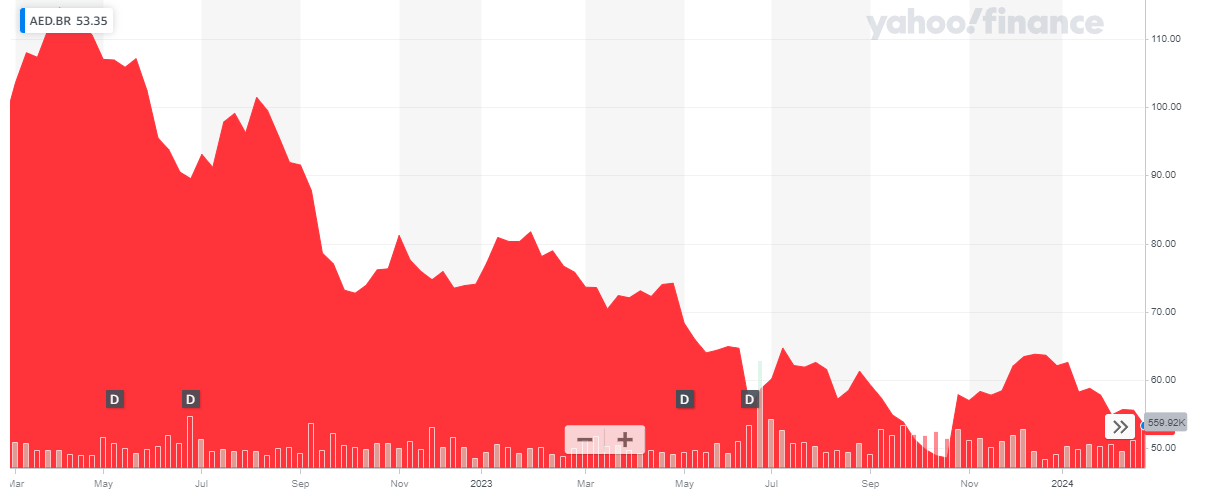

Aedifica’s main itemizing is on Euronext Brussels, the place the corporate is listed with AED as its ticker image. The average daily volume in Brussels is 64,000 shares, and one of many benefits of the primary itemizing is that there are alternatives accessible. There are at the moment 47.55M shares excellent, leading to a market capitalization of simply over 2.5B EUR based mostly on the present share value of simply over 53 EUR.

Yahoo Finance

The 2023 outcomes point out the dividend is absolutely coated

One of many causes I like Aedifica probably the most is its CPI-linked indexation. This enables the REIT to regularly improve its rental revenue and means Aedifica is usually not too uncovered to the influence of inflation apart from a ‘timing’ concern: it normally hikes its lease simply as soon as per 12 months. A second motive I’m charmed by Aedifica is the truth that its leases are triple web leases, which significantly reduces the capital expenditures required to maintain the properties in form.

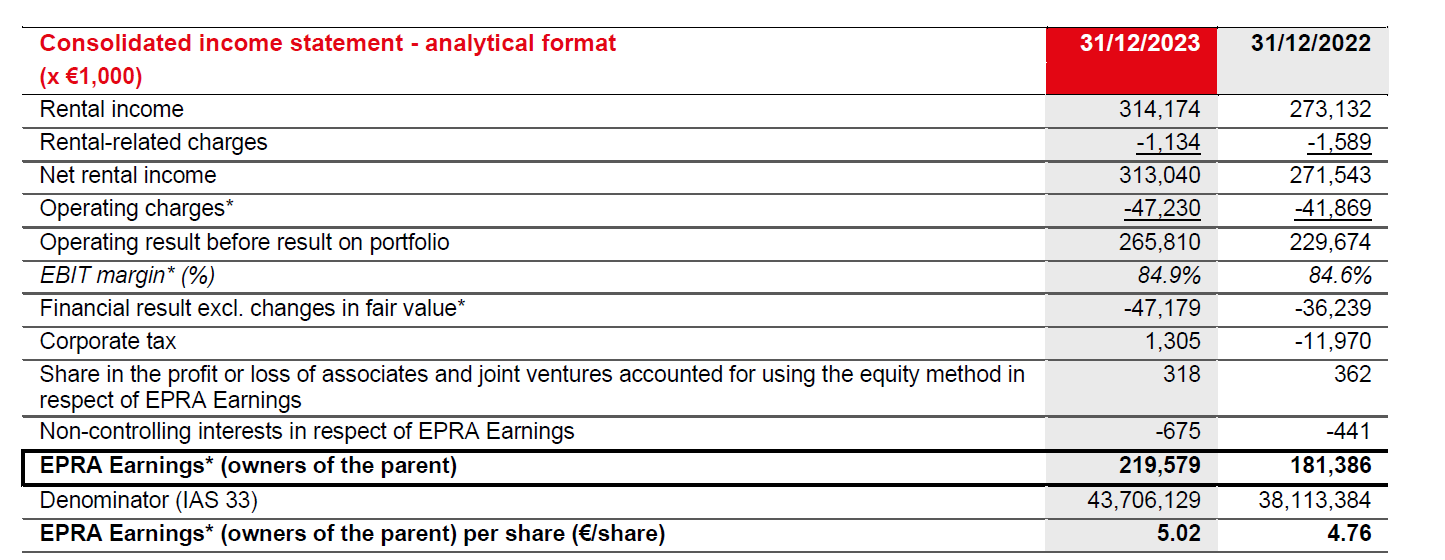

As you’ll be able to see beneath, Aedifica generated a total rental income of 314M EUR leading to a web rental revenue of 313M EUR. The EPRA earnings got here in at virtually 220M EUR, which resulted in an EPRA EPS of 5.02 EUR per share utilizing the weighted common share depend all year long.

Aedifica Investor Relations

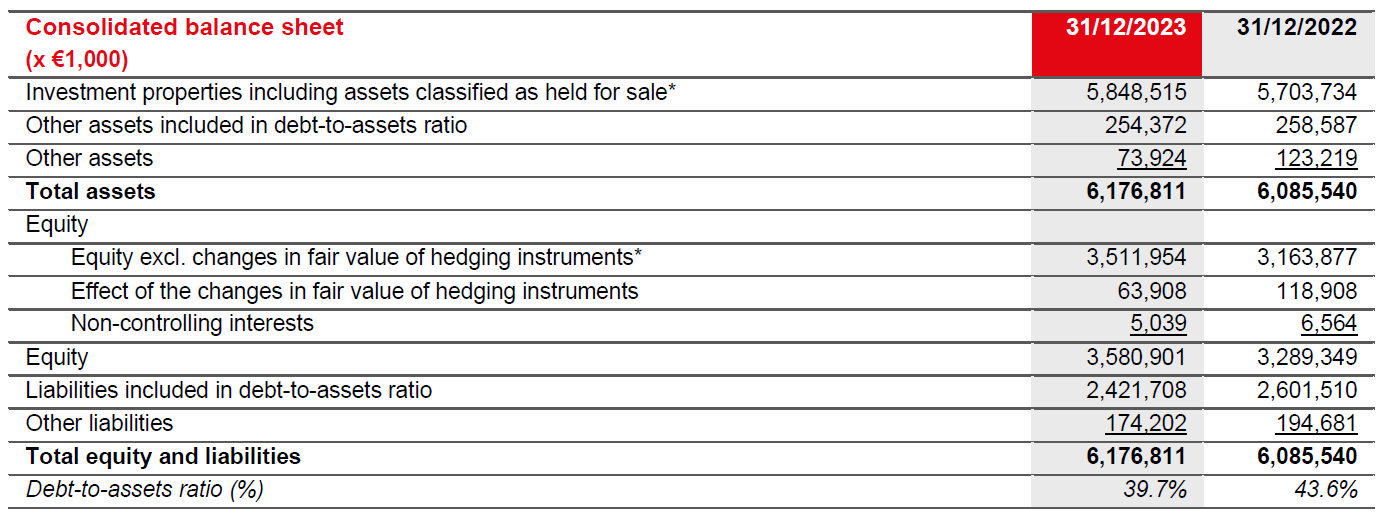

A sturdy set of earnings (though the per-share consequence will lower in 2024) whereas holding the stability sheet secure: on the finish of 2023, the debt to belongings ratio got here in slightly below 40%. This may assist the REIT to finish its funding program

Aedifica Investor Relations

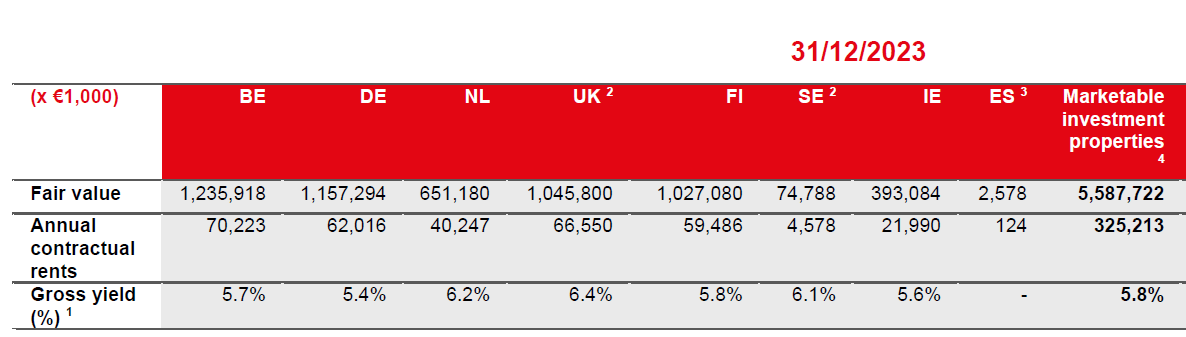

And searching on the truthful worth of the actual property asset base, Aedifica’s belongings are valued at 5.59B EUR, utilizing a rental yield of 5.8%.

Aedifica Investor Relations

Aedifica is guiding for a rental revenue of 330M EUR this 12 months, and even in the event you would apply a cap fee of 6.5% the truthful worth would lower by simply over 500M EUR which might end in an replace NAV/share of roughly 62-63 EUR.

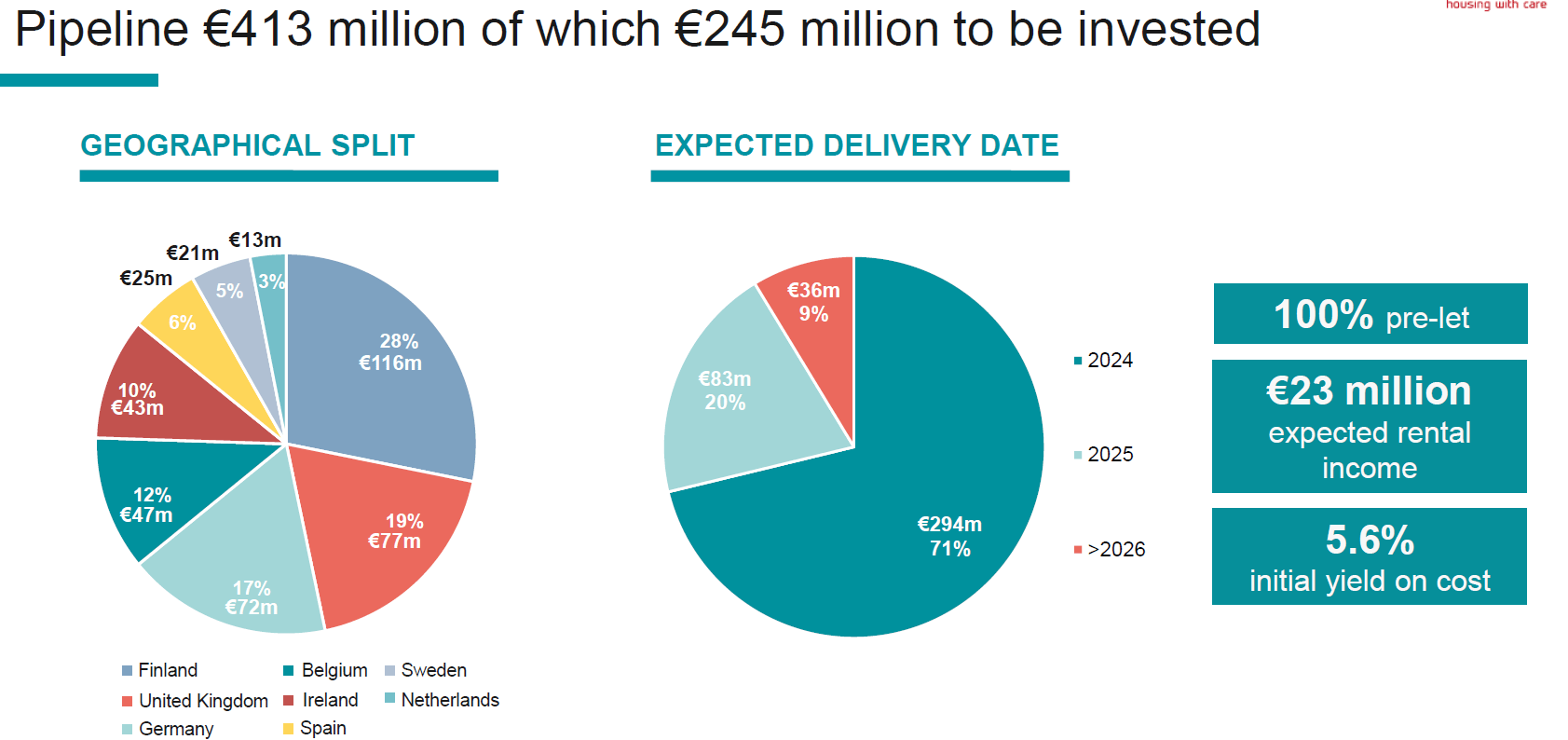

Aedifica additionally continues to advance its pipeline and about 294M EUR of development assets ought to be accomplished in 2024. Your complete funding portfolio will add 23M EUR to the rental revenue foundation, representing a yield on value of 5.6%. I feel Aedifica wouldn’t prefer to see greater returns earlier than committing to new tasks.

Aedifica Investor Relations

Essential: the REIT solely has to speculate 245M EUR in 2024-2026 to finish these belongings. Because the REIT will retain roughly 50M EUR per 12 months in earnings (the distinction between the EPRA earnings and the dividends payable to its shareholders), it should not have any points to safe funding to finish the event pipeline.

Though the outcomes might be weaker in 2024, Aedifica will improve the dividend

I’ve the utmost respect for administration groups who let a dividend fluctuate based mostly on earnings. In spite of everything, that’s precisely what a dividend is meant to be: a distribution of (a portion of) the earnings of an organization to its shareholders.

In the case of 2023, there isn’t a concern in any way: the REIT reported earnings of 5.02 EUR per share and pays a dividend of three.80 EUR, for a payout ratio of roughly 76%. That’s tremendous. Nonetheless, for 2024, the REIT is already guiding for a dividend of three.90 EUR per share (+2.5%) though the earnings will lower by 6% to 4.70 EUR per share. Based mostly on the steering for 2024, the payout ratio will improve to 83%. The decrease earnings result’s predominantly attributable to the upper share depend. Throughout 2023, the share depend elevated from 39.9M shares to 47.5M shares, however the weighted common share depend was 43.7M shares, and that was the quantity used to calculate the EPRA earnings of 5.02 EUR per share.

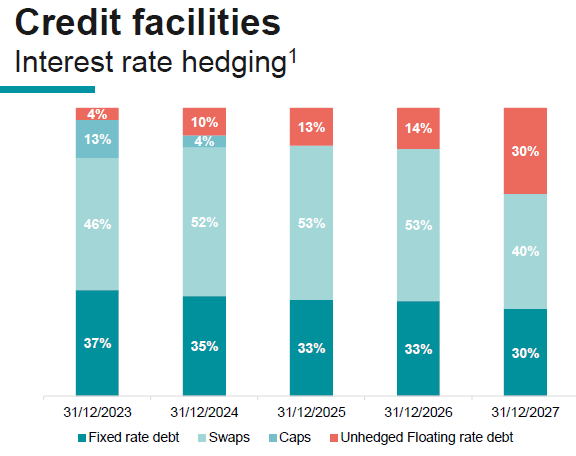

Whereas that certainly means the dividend remains to be well-covered by the earnings, 2024 might not be the final 12 months Aedifica must cope with stress on the earnings. As of the tip of 2023, Aedifica’s common value of debt was 1.9%. Luckily, the REIT has hedged the overwhelming majority of its rate of interest publicity and as you’ll be able to see beneath, there is also a considerable portion of fastened fee debt.

Aedifica Investor Relations

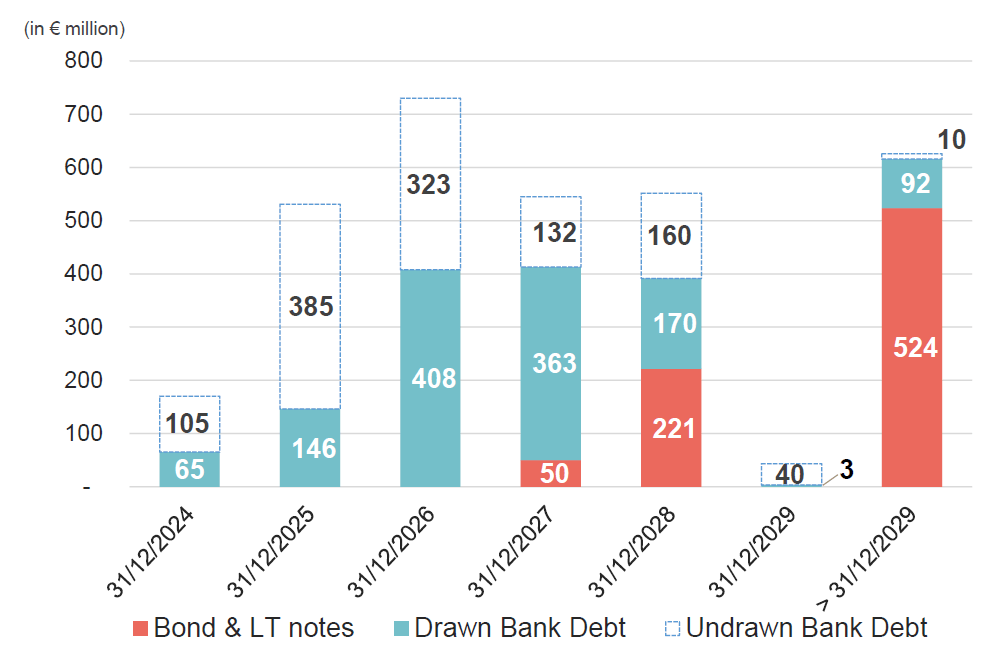

Nonetheless, the rate of interest hedging clearly solely takes the hedging under consideration till the maturity date has been reached. As you’ll be able to see beneath, Aedifica might face some headwinds going into 2026. The 211M EUR of maturing debt in 2024 and 2025 can simply be refinanced, and the anticipated improve in the price of debt will probably be absolutely compensated for by greater rental revenue.

Aedifica Investor Relations

The actual take a look at might be in 2026 and 2027 whereby a mixed 820M EUR of debt must be refinanced. Luckily, there are two issues working in Aedifica’s favor. The primary aspect is the anticipated rate of interest decreases over the subsequent few years. I like the percentages of Aedifica’s value of debt to be decrease in 2026 than the place they’re at at present. Secondly, 2026 remains to be two years away, which provides Aedifica loads of time to ‘right-size’ the portfolio and push by way of just a few lease hikes by then and to finish its funding portfolio which is able to add simply over 20M EUR to the rental revenue (a portion of the complete run fee of 23M EUR is already included within the 2024 steering).

In principle, and that is only a principle and assuming all different prices and bills stay unchanged, a median improve within the web rental revenue of two% per 12 months would cowl a refinancing at 4.5%. An rate of interest, which I feel is unquestionably achievable if the ECB certainly begins to cut back its benchmark rates of interest later this 12 months.

Funding thesis

I’ve an honest sized lengthy place in Aedifica, and I used to be ready for the annual outcomes earlier than deciding if I ought to add to this place (which at the moment is barely underwater). I wasn’t fairly positive how the REIT would navigate by way of the risky waters, however my fears have been put to relaxation by the clear 2023 replace. Whereas the earnings will lower in 2024, that is primarily as a result of full influence of a capital increase in 2023, and odds are we’ll see an earnings improve once more in 2025 because the REIT ought to be capable to proceed to extend its rental revenue whereas the influence of debt refinancings ought to stay comparatively restricted.

An added bonus is that Aedifica’s dividends are topic to a withholding tax of simply 15% as an alternative of 30% (though this profit might disappear in just a few years because the UK portfolio will now not depend as European residential healthcare actual property. Aedifica may resolve to cut back the scale of its UK portfolio whereas investing in different European belongings to satisfy the requirement to have 80% of its belongings as European residential actual property. All of it is dependent upon how essential the decreased dividend tax is to the REIT.

Aedifica is buying and selling at a reduction of 25% to its NAV based mostly on a 5.8% cap fee and a reduction of 15% based mostly on a 6.5% cap fee. Moreover, the well-covered dividend yield of seven.3% may be very enticing as nicely.

I’ve a protracted place and can proceed so as to add to this place.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please concentrate on the dangers related to these shares.