Edwin Tan /E+ by way of Getty Photos

We’re initiating Aehr Check Methods (NASDAQ:AEHR) with a buy-rating. AEHR is a number one supplier of check programs for burning-in and testing reminiscence and logic built-in circuits with a novel place within the semiconductor trade and publicity to the EV market. The corporate introduced 2Q24 outcomes and outlook earlier this week, reporting a strong quarter however revising FY24 steerage by 15-25% to the vary of $75M to $85M and GAAP internet revenue between 20-25% of income. Our optimism on the inventory relies on our perception that the draw back in EV has been realized, now being priced into each the outlook and inventory with the post-earnings sell-off. We see an increasing marketplace for Silicon Carbide or SiC demand from EV and industrial markets within the longer-run because the trade penetration fee expands over the following 2-3 years. SiC demand from EVs and industrial is at present comfortable because the auto and industrial markets endure a correction. Nonetheless, traders should not be too involved about this because the buyer capability and manufacturing pushouts because of the correction are mirrored in AEHR’s FY24 outlook. We see continued Y/Y progress in SiC demand and count on finish demand restoration post-correction to additionally act as a catalyst for AEHR’s top-line progress. Canalys forecasts the worldwide EV market will develop by 27.1% in 2024, hitting 17.5M models; we predict the present comfortable EV demand is non permanent because the EV market continues to be within the early innings of its progress. Reflecting this in a giant means is the truth that even after the FY24 outlook reduce, the FY24 progress fee stays within the double-digit vary of 15-30% Y/Y. We expect the underside is forming now with the pullback throughout the EV peer group and even semi gamers with auto and industrial publicity like On Semiconductor (ON). ON administration guided for a gross sales decline of 6-11% QoQ to $1,950-2,050M, trailing consensus. We’re seeing slower progress throughout the peer group, with trade EV chief Tesla (TSLA) solely barely outpacing its FY unit steerage after it already reduce in 2023. We expect the market is present process a correction, which must be full in 1H24, as we’re seeing a number of EV gamers reduce on manufacturing.

For the quarter, AEHR reported internet income of $21.4M, up 45% Y/Y, slower than the 93% Y/Y progress 1 / 4 prior however nonetheless within the double-digit vary. The corporate’s proven a strong progress trajectory with its reported internet income of $42.1M for the primary six months of FY24, a 65% enhance from 1H23. Moreover, the corporate’s stability sheet stays robust and has a backlog of $3M, reflecting future income stream. We expect AEHR is now higher positioned to outperform after the macro weak point has been priced into the outlook and inventory.

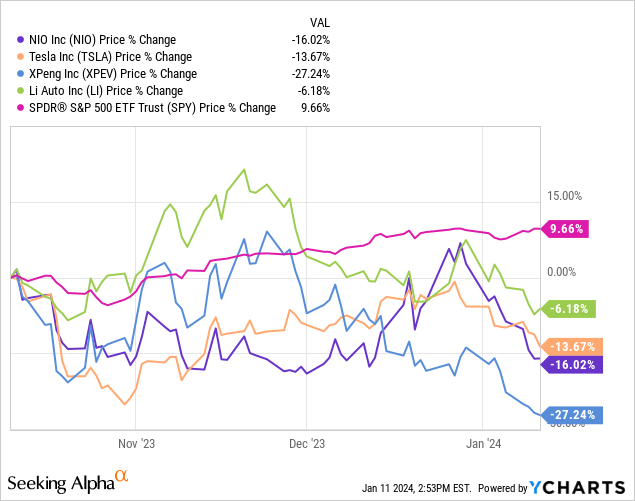

Gayn Erickson, AEHR CEO and President famous on the earnings call, “In the last sixty days, we have seen how the slowing of the growth rate of the electric vehicle market has had a negative impact on the timing of several current and new customer orders and capacity increases for silicon carbide devices used in them.” We count on prospects to work by means of oversupply over the approaching quarter and see an finish demand rebound starting in 2H24 for the EV and industrial markets, because the correction must be full in 1H24 in accordance with our estimates monitoring the peer group. All EV gamers have been buying and selling decrease over the previous three months; the next outlines NIO (NIO), Tesla, XPeng (XPEV), Li Auto Inc (LI), and the S&P 500.

YCharts

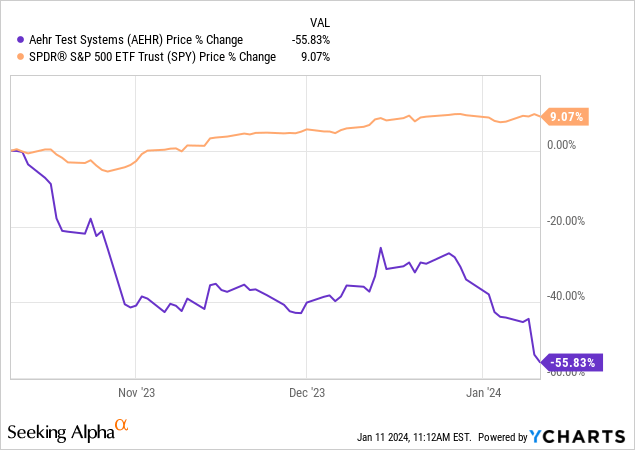

We expect AEHR inventory now costs within the macro weak point, and we do not see additional steerage cuts in 2HFY24; the explanation we do not see extra draw back revision in FY24 steerage is that SiC demand must proceed for auto and industrial markets to maintain progress forecasts. We see an increasing progress alternative for AEHR in 2024 and 2025 as soon as EV demand rebounds; the EV market is estimated to develop at 20% CAGR by means of 2030, and an important a part of making certain the EV provide wants are met is the provision of SiC. As Erickson places it, “For clarity, we do not see the silicon carbide market decreasing, only a temporary slowing of the growth rate.” After the pullback this week, we see a extra favorable risk-reward profile for AEHR, down 19% over the previous 5 days, versus the S&P 500, up 2%. Over the previous three months, the inventory has underperformed the S&P 500 by 65%.

The next outlines AEHR inventory towards the S&P 500 over the previous three months.

YCharts

Whereas the rebound might take longer than anticipated post-inventory correction cycle with out momentum to drive it, we predict it is a matter of when not if the demand will rebound and drive top-line progress. In our opinion, the largest threat factor for the EV rebound is extended macro weak point within the Chinese language market, as mainland China is by far the biggest EV market, with 55% of the worldwide EV gross sales in 1H23. We expect EV demand will proceed to be comfortable within the near-term as prospects cope with order pushouts because of weaker-than-expected client spending. We see finish demand rebounding post-correction as supply-demand dynamics come again into stability. We do not see China recovering within the close to time period, however we imagine the trade will see an increasing penetration fee regardless. Our perception of a rebound in SiC demand can also be based mostly on our expectation that finish demand in U.S. and European markets ought to rebound post-correction as macro uncertainty eases. We suggest traders discover entry factors at present ranges.

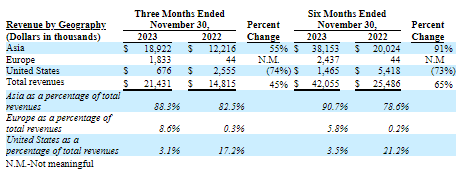

The next chart outlines AEHR’s income by geography, highlighting the corporate’s increased publicity to Asia.

AEHR 10Q

Valuation

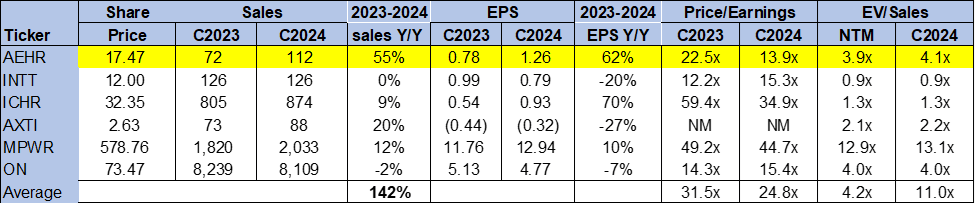

The inventory is pretty valued, in our opinion, for the expansion potential in SiC demand from EV and industrial markets. The sock is buying and selling at 4.1x EV/C2024 Gross sales versus the peer group common of 11.0x. On a P/E ratio, the inventory is buying and selling at 13.9x C2024 EPS $1.26 versus the peer group common of 24.8x. We expect AEHR’s valuation is digestible compared to the check programs peer group. We worth AEHR as a progress inventory and see extra room for upside potential because the trade penetration fee expands.

The next outlines AEHR’s valuation towards the peer group.

TSP

Phrase on Wall Road

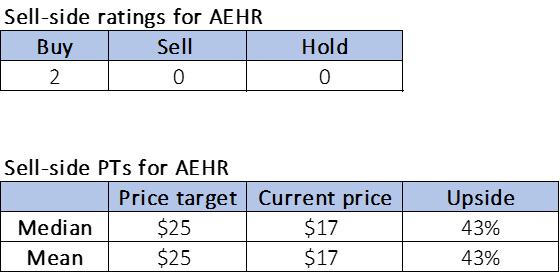

Wall Road shares our bullish sentiment on the inventory. AEHR is basically an under-the-radar sort of inventory; the 2 analysts overlaying the inventory share our buy-rating. The inventory is at present priced at $22 per share. The median and imply sell-side targets are $25, with a possible upside of 12%. We expect AEHR will get extra traction after the large pullback that signaled how unhealthy the EV hunch is. Therefore, we additionally imagine outperformance will probably be partially pushed by investor confidence within the inventory as soon as EV and industrial markets start to rebound.

The next charts define AEHR sell-side scores and value targets.

TSP

What to do with the inventory

We provoke AEHR with a buy-rating. 2Q24 outcomes and outlook lead us to imagine the draw back in EV and correction in auto and industrial markets have been priced into the outlook and inventory value. We strongly imagine SiC demand will not be going wherever; the market is estimated to develop at a CAGR of 26% between 2022-2030. We suggest traders benefit from the pullback and soar in on the backside.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a significant U.S. trade. Please pay attention to the dangers related to these shares.