kontrast-fotodesign

Earlier in the year, renewable natural gas and renewable fuels company Aemetis, Inc. (NASDAQ:AMTX) popped up on my radar thanks to being one of a handful of clean energy stocks to finish in the green in 2023. AMTX is up 113.0% over the past 12 months, a sharp contrast to the -28.0% return by iShares Global Clean Energy ETF (ICLN) over the timeframe. ICLN is the largest renewable energy ETF and a popular catch-all bet on clean energy while Aemetis is California’s largest producer of biofuels. The company returned an impressive Q1 2024 scorecard on May 9, with the report containing several notable milestones. The company reported revenue of $72.6M, $0.48M above the Wall Street consensus and good for a huge 3,276.7% Y/Y jump, thanks in large part to easy comps.

All three of Aemetis’ operating segments posted strong growth.

The California Ethanol segment posted revenue of $36.1 million from virtually zero in Q1 2023. Last year, Aemetis decided to idle its 65 MMgy corn ethanol plant located in Keyes, California, during the first five months of 2023 after gas prices rocketed 500%. The company says it used the break to perform several important ethanol plant energy efficiency upgrades.

The India Biodiesel segment realized revenue of $32.7 million, incomparable to $1.5 million for Q1 2023. Aemetis owns and operates a 50 million gallon per year production facility on the East Coast of India producing high quality distilled biodiesel and refined glycerin for customers in India and Europe. The company holds a portfolio of patents and exclusive technology licenses to produce renewable fuels and biochemicals.

Aemetis’ budding Dairy Renewable Natural Gas segment produced 60,300 MMBtu from eight operating dairy digesters, sold its first Low Carbon Fuel Standard (LCFS) credits and reported $3.8 million of revenue. That’s a big improvement from a year ago when the dairy segment produced 21,300 MMBtu from six dairy digesters, but the RNG was placed in underground storage to preserve the carbon credits. The company is expanding a California biogas digester network and pipeline system to convert dairy waste gas into RNG. Aemetis has already gained approval by the California Environmental Quality Act (CEQA) for a total of 60 miles of public right of way for a biogas gathering pipeline that will collect biogas from an aggregate of 38 dairies.

The company achieved significant milestones under the previous 2023 Five Year Plan, including:

-

Transitioned to receiving revenue and positive operating cash flow from the biogas-to-RNG upgrading facility and dairy digesters

-

Received Use Permit and CEQA approval for the SAF/RD plant at the Riverbank site

-

Completed construction and commissioning of the 1.9 megawatt solar microgrid with battery backup

-

Received the first private carbon sequestration characterization well drilling permit by the State of California

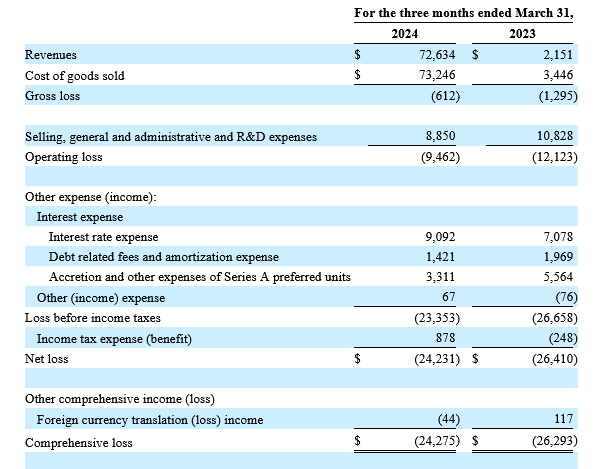

Unfortunately, Aemetis is yet to become profitable, mainly due to high Cost Of Goods Sold (COGS). However, there were some positive profit trends that I observed in that report, including the fact that Q1 2024 gross loss clocked in at -$612,000 compared to a loss of -$1,295,000 for Q1 2023 despite sales being more than 20x higher. Selling, general and administrative (SG&A) fell to $8.9 million from $10.8 million during the similar period in 2023, which the company attributed to a reduction in fixed COGS and lower charge to SG&A expenses due to the extended maintenance carried out in the first quarter of 2023. Q1 2024 operating loss narrowed to -$9.5 million compared to an operating loss of -$12.1 million for Q1 2023 while net loss clocked in at -$24.2 million (-$0.58 per share) from a net loss of -$26.4 million (-$0.73 per share) for the first quarter of 2023.

AEMETIS, INC. CONSOLIDATED CONDENSED STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS

Aemetis Income Statement (Aemetis Form 10-Q)

Big Growth Ahead

Back in February, Aemetis provided its 5-Year Growth Plan wherein it laid out how it intends to grow the topline from the current annual run-rate of ~$300 million to $1.95B by 2028, good for a nearly 600% increase. The plan calls for revenue to grow at a compound annual growth rate of 38%, and adjusted EBITDA is expected to expand at 83% CAGR for the years 2024 to 2028.

Aemetis plans to meet these ambitious targets by, among other things, growing its RNG segment from the current crop of eight dairies to 75 dairies by 2028, potentially increasing dRNG production to over 2 million MMBtu per year. The company’s renewable natural gas segment, in particular, appears to have really attractive growth runways thanks to California’s ambitious 2022 Scoping Plan. According to Aemetis CEO and Chairman Eric McAfee, CEQA has signaled RNG will be an important feedstock for renewable hydrogen. McAfee says the company is well positioned to supply RNG to the renewable hydrogen and renewable electricity markets, both forecast to grow via the California Air Resources Board (CARB) expected adoption of a 20-year mandate to achieve carbon neutrality by 2045. To achieve the objectives of the 2022 Scoping Plan, the world’s 5th largest economy requires a 4x increase in the current solar and wind capacity by 2045 as well as an enormous 1,700x the amount of current hydrogen supply.

In terms of near-term plans for the RNG segment, Aemetis CEO Eric McAfee reported that the company plans to close on $60 million of new private financing and secure additional USDA loan guarantees in a bid to accelerate the rate of its biogas digester development in 2024.

Aemetis’ shareholders can also expect a new revenue stream to come online, possibly in the not-too-distant future. McAfee reported that Aemetis received final Authority to Construct air permits for a 78 million gallon per year sustainable aviation fuels (SAF) production facility. The company is currently developing a SAF biorefinery in California that will utilize renewable oils, renewable hydrogen and hydroelectric power to produce low carbon intensity renewable jet and diesel fuel.

I believe the SAF segment has strong growth prospects, too. Two years ago, Aemetis signed a multi-year agreement with International Airlines Group (IAG) to supply 78,400 tonnes of sustainable aviation fuel to help power both British Airways and Irish flag carrier Aer Lingus’ flights from San Francisco Airport from 2025. The SAF will be produced at the Aemetis Carbon Zero designed to sequester CO2 from the production process. The SAF plant, currently under development in Riverbank, California, will be powered by 100% renewable electricity. SAF can reduce emissions by up to 80% during its full lifecycle.

More such deals could be on the way for Aemetis.

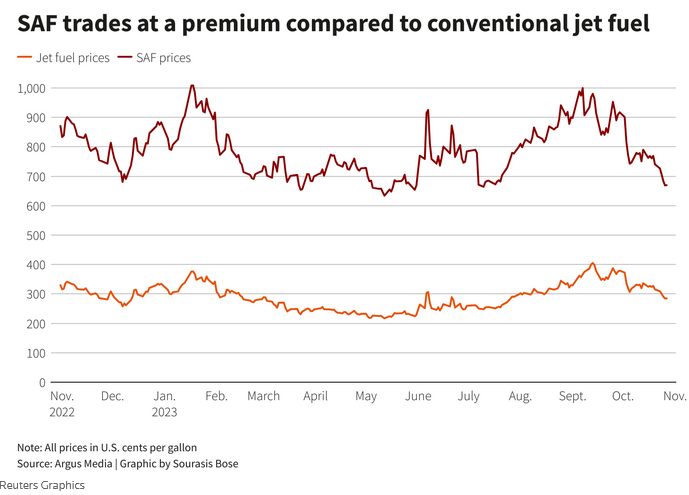

SAF adoption by U.S. and global airlines has been disappointing, mainly due to high costs. Last November, commodities and energy pricing agency Argus Media reported SAF prices at $6.69 per gallon, more than double $2.85 for a gallon of U.S. jet fuel. Just 15.8 million gallons of U.S. SAF was sold in 2022 compared to 11.9 billion gallons of conventional jet fuel–a long way off Biden’s target to supply at least 3 billion gallons of SAF annually by 2030. Fuel typically accounts for 25% of an airline’s operating costs, suggesting that replacing just 10% of ordinary jet fuel with SAF would have a major impact on airlines’ bottom lines. The economics are equally bad for SAF producers, with a tax credit of up to $1.75 per gallon provided under the Inflation Reduction Act (IRA) not enough to offset poor margins.

“At the moment, it’s maybe a hard decision for producers to put additional capital in to produce SAF rather than renewable diesel,” Wood Mackenzie analyst Gordon McManus told Reuters, noting that renewable diesel can be made from the same feedstocks as SAF.

However, European airlines might soon have little choice in the matter. Last year, European regulators introduced a mandate to ensure SAF constitutes 2% of fuel available at EU airports by 2025, a figure set to increase to 6% in 2030, 20% in 2035 and 70% in 2050. The EU parliament approved the mandate in January, although member states are yet to vote on it.

Policy changes might be needed to goad the United States in the direction of its European peers. Thankfully, some major airlines are already onboard, with Delta Air Lines (DAL) and Southwest Airlines (LUV) having committed to replace 10% of their jet fuel with SAF by 2030. Seven technical pathways currently exist in creating different types of SAF; however, most SAF brands are ‘drop-in’ fuels, designed to be mixed with traditional fuels, meaning no changes or extra investments are needed from airports.

SAF vs. Jet Fuel Prices (Reuters)

The large cost differential between conventional jet fuel and SAF is largely attributable to SAF’s small production runs; however, that gap is projected to contract as the industry scales up and adopts more robust supply agreements. Although global SAF production was only 600 million liters in 2023, the aviation sector has already committed to six billion liters of SAF in forward purchase agreements, an encouraging trend.

Takeaway

Over the last 5 years, Aemetis has seen its revenue expand at an anemic 4.8% per year clip while profits have remained elusive. Thankfully, the company’s renewable natural gas and SAF appear poised to finally help the company achieve sustained top-and bottom-line growth for 4-5 years at the very least, which should help the shares not only grow into their steep valuation but, potentially, return 15-20% per year share price growth over the period. The fact that California appears poised to adopt its ambitious 20-year decarbonization plan is definitely a major tailwind for Aemetis.

I consider execution the biggest risk for Aemetis at this juncture, especially now that the company has set such ambitious growth targets. The shares tanked wildly a year ago when the company decided to idle its ethanol plant due to an unusually large natural gas price spike. Any such major revenue disappointments are likely to prove damaging for AMTX. I rate these shares a Buy with a view to hold over the long term.