DutchScenery

Plenty of instances with frequent sturdy items, we simply take them with no consideration and don’t ask the place they arrive from, who made them, or what the enterprise surrounding that manufacture appears like. A major instance of that is college buses.

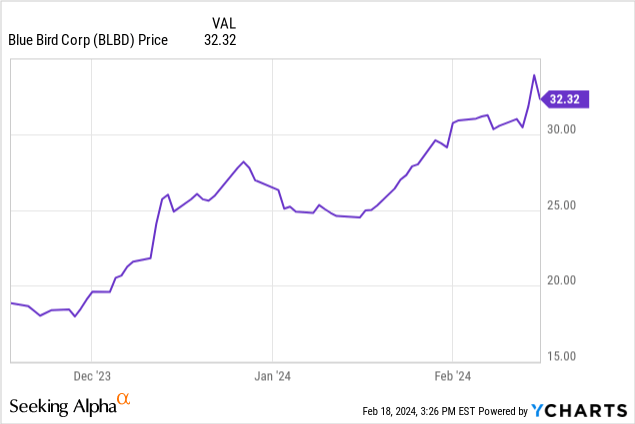

At present we’ll be taking a look at a long-time school bus manufacturer, Blue Chicken Company (NASDAQ:BLBD). A bus-maker because the 1930’s, the fashionable incarnation of Blue Chicken is within the technique of reinventing its trade, lengthy making the old school belchers of diesel smoke and now one of many leaders within the creation of other powered buses, together with electrical autos.

Blue Chicken only in the near past launched earnings for Q1 decisively beating the estimates not just for that quarter, however providing new, larger steering for the remainder of fiscal 2024. The inventory worth surged, after all, however even at a 52-week excessive, there’s nonetheless worth to be discovered right here. Let’s look deeper.

Higher Steering

Seasonality implies that Q1 is historically the weakest quarter for Blue Chicken, however once we begin throwing around terms like “record” earnings, we are able to see why the inventory worth has performed what it did this month.

However that is much less about what already occurred, admirable although it’s, and extra about what’s going to occur by 2024, a subject that was heavily focused on in the earnings transcript.

These document leads to This autumn and Q1 are certainly spectacular, and with a backlog of 4,600 college buses the remainder of the yr is wanting extraordinarily promising. We don’t understand how quick these orders will likely be stuffed, but it surely appears positive to maintain the workforce busy.

Full yr steering is one other document, $130 million EBITDA, a continued give attention to electrical autos. In Q1 a document 206 EV was bought. Between EV, propane, and gasoline, the collected alternative-powered autos of their portfolio, they amounted to 66% of their gross sales in 2023. Higher nonetheless, the sale worth was some 26% larger in Q1 than beforehand realized in 2023.

The massive order to maintain a detailed eye on is from the LA Unified colleges, which needs 180 EV buses, the expectation is that they’ll be delivered in late 2024 and the deal, in contrast to plenty of them, was not in any approach EPA-funded.

The EPA’s Clear College Bus program is offering a rising quantity of funding for colleges to purchase the extra environmentally pleasant various buses, together with each EV, for which there’s competitors, and propane-powered buses, which none of their substantial competitors produces anymore.

| 2021 | 2022 | 2023 | Q1 | |

| Working FCF | ($54 million) | ($24 million) | $120 million | $217,000 |

| Investing FCF | ($11 million) | ($6 million) | ($9 million) | ($2.9 million) |

| Financing FCF | $33 million | $30 million | ($43 million) | $995,000 |

(supply: 10-Ok and most up-to-date 10-Q from SEC)

A stable 2023 was a superb yr totally free money movement, whereas the expectations for a robust 2024 ought to make issues even higher. Money movement is vital right here, as the cash isn’t just for paying down the debt, lowered by $15 million over the previous yr, and paying for a considerable share buyback program put into place.

By the Numbers

| Money and Equal | $77 million |

| Inventories | $142 million |

| Complete Present Belongings | $243 million |

| Complete Belongings | $431 million |

| Complete Present Liabilities | $188 million |

| Lengthy-Time period Debt | $93 million |

| Stockholder Fairness | $75.6 million |

(supply: most up-to-date 10-Q from SEC)

Money available rose fairly a bit on account of a juicy free money movement in 2023. Lengthy-term debt, paid down over the previous yr, can be down a bit, a really optimistic signal.

Sadly, the worth/e-book worth of Blue Chicken is extraordinarily excessive, particularly after the just lately introduced secondary public offering, which means the corporate is buying and selling at an enormous premium to property. That’s not essentially unwarranted after such robust performances, but it surely means the worth we’re on the lookout for has to return from some place else.

| 2021 | 2022 | 2023 | Q1 | |

| Internet Gross sales | $684 million | $801 million | $1.1 billion | $318 million |

| Gross Revenue | $72 million | $37 million | $139 million | $64 million |

| Working Income | $6.5 million | ($40.7 million) | $51.6 million | $38 million |

| diluted EPS | (1¢) | ($1.48) | 74¢ | 81¢ |

(supply: most up-to-date 10-Ok and 10-Q from SEC)

In 2021 and 2022, gross sales had been down after all, resulting from COVID. Like every little thing else, the COVID-19 pandemic hit the economic system laborious and had many municipalities transferring to postpone shopping for new buses.

Blue Chicken is essentially going to must deal with being in a cyclical trade. The excellent news is correct now, since 2023, they’re in a robust market situation. Analyst estimates for 2024 and 2025 are even higher, with EPS of $2.35 and $2.51, respectively.

Meaning a PE ratio of 14 and ahead PE of 13.1, each of which match neatly into the worth vary, particularly when one considers how a lot web gross sales are rising yr over yr. The web gross sales going ahead will, per analysts, be 1.25 billion and 1.41 billion, so the expansion into a robust cycle is barely going to proceed.

The Dangers

Sadly even with every little thing seemingly going proper, there are dangers like a brand new pandemic that might scare these college districts into laying aside gross sales, or simply plain an financial downturn that impacts gross sales.

Provide chain disruptions, as soon as once more a perform of COVID-19 at first, stays a priority. Transport prices are coming down and provides appear to be out there, at the very least for now.

Reliance on single-source suppliers might simply turn into an issue although. Plenty of components go into the creation of college buses, whether or not diesel or in any other case, and if some half scarcity occurs, it might delay plenty of deliveries, which might significantly affect the underside line.

The unionization of their workforce may also be a long-term concern, as labor stoppages might delay issues badly, and will elevate a value of manufacturing.

Two different issues talked about in official firm reviews are the reliance on dealerships to promote buses, and the considerably substantial debt making the underside line susceptible to rate of interest fluctuations.

Conclusion

Blue Chicken’s trade may not be enormous, however with 146,000 buses in service for 15 years or extra, and the rise usually of scholar inhabitants means there are going to be loads of alternatives to maintain making gross sales at any fee, and the rising give attention to environmentally pleasant various energy sources ought to assure Blue Chicken is below severe consideration for the brand new gross sales.

Q1 specifically was simply spectacular, and whereas excellent news appears at the very least considerably baked into the worth at these ranges, I wouldn’t be afraid to pay 13-14 instances earnings for any firm that’s so properly poised for development.

I’m going to place Blue Chicken as a particular purchase. Diversification is vital, and faculty buses are undoubtedly a distinct segment trade that I’d be snug to be in. It clearly can be good to purchase in at a cheaper price than present out there, however even now it isn’t unreasonable, and billions of EPA funds meant for clear college buses ought to discover their approach into Blue Chicken’s coffers.