Solskin/DigitalVision through Getty Pictures

Be aware: This can be a Brazilian firm. Aside from the inventory value and valuation the place the forex used is in USD, Brazilian Actual (BRL) was used.

Introduction

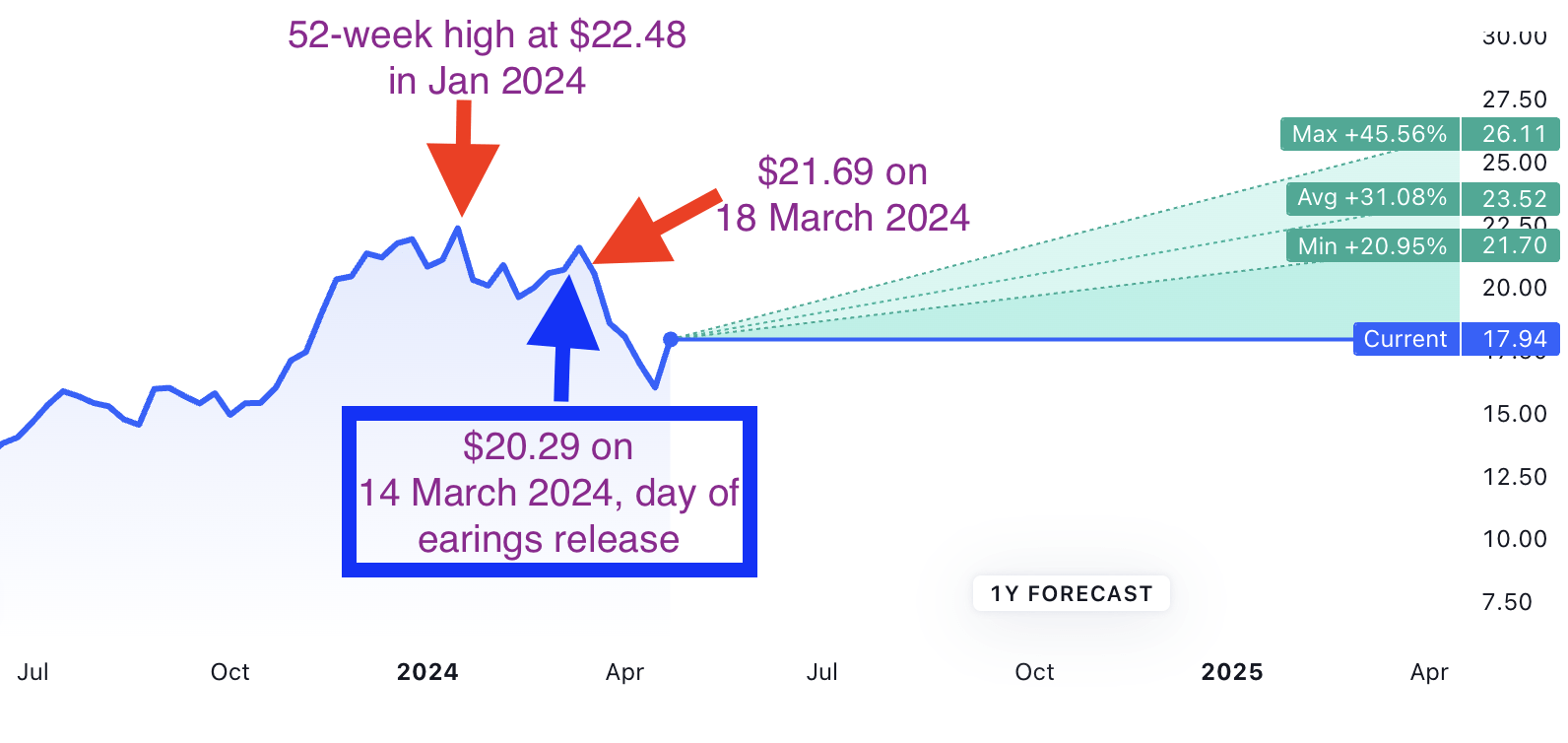

I lined AFYA (NASDAQ:AFYA) 10 months in the past in this text, Afya: An Undiscovered Gem With High Return Potential. The inventory gained 45% in six months however since January 2024, it has crashed 25.89% in comparison with SPY which gained 4.64% year-to-date (as of 19 April 2024).

FAST Graphs

Extra particularly, the inventory value gained nearly 7% after the This autumn 2023 earnings convention name on 14 March 2024. Nevertheless, it began plunging after 18 March and has fallen 26%. Was AFYA’s decline a part of the broader selloff that started in March 2024 (i.e., not company-specific points) and due to this fact we’d like not be overly apprehensive?

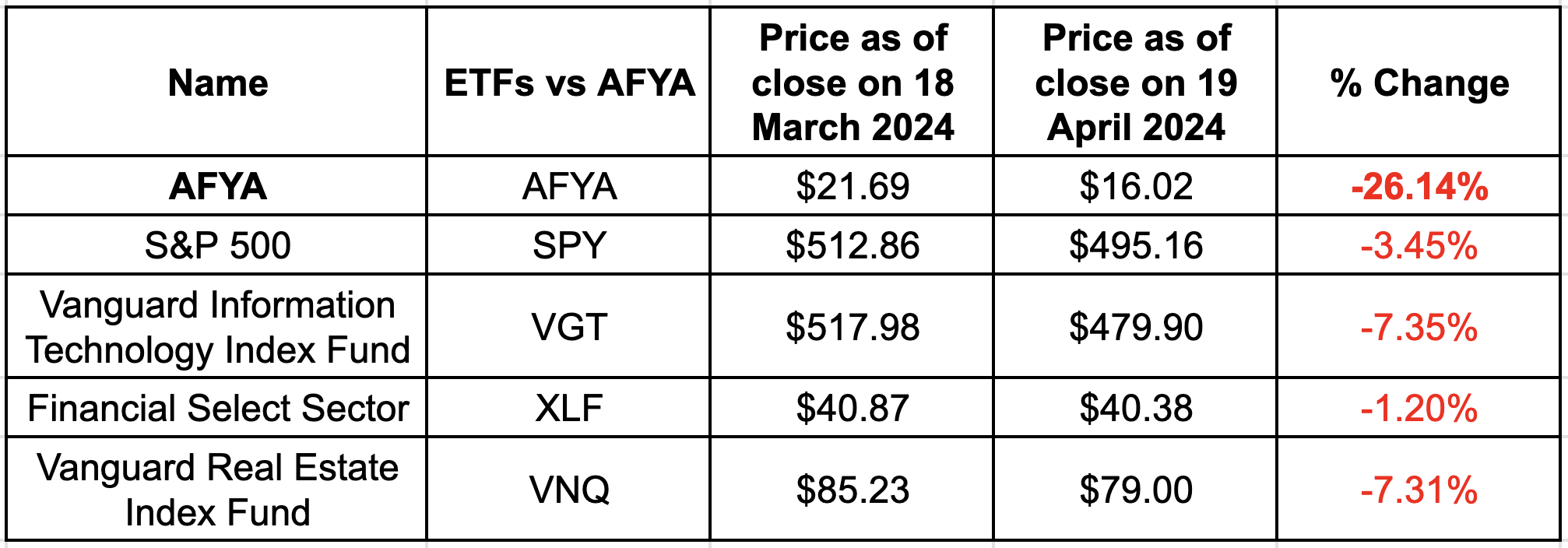

That won’t appear to be the case. The desk under compares the value modifications of AFYA towards among the main ETFs available on the market.

Writer’s compilation of value modifications of AFYA vs ETFs

The decline in costs of some main ETFs is far smaller in diploma and extent in comparison with the crash in AFYA’s inventory value, indicating that the issues traders have are company-specific, and the value decline was not merely a part of the broader selloff.

But, the complicated half (to me) was that AFYA’s inventory value rose following the earnings name on 14 March 2024, gaining 7% between 14 March and 18 March. Earnings and steering should have been nice or adequate to present traders confidence to purchase extra.

Finviz

Analysts AFYA’s consensus value goal is $23.52 with a most estimate of $26.11 and a minimal estimate of $21.70, with a “strong-buy” ranking.

So what induced the 26% decline in a single month? These will likely be examined within the subsequent part. As an AFYA shareholder, I have to determine whether or not to speculate extra, maintain my shares, or promote.

With the complete 12 months 2023 outcomes accessible to us to research, let’s start.

Enterprise Fundamentals

2023 earnings and income

The earnings highlights could be discovered here. Based on the Form 6K,

FY23 Adjusted Internet Income elevated 23.9% YoY to R$2,874.1 million. Adjusted Internet Income excluding acquisitions grew 13.3% to R$2.626.9 million.

FY23 Adjusted EBITDA elevated 21.2% YoY reaching R$1,165.7 million, with an Adjusted EBITDA Margin of 40.6%. Adjusted EBITDA excluding acquisitions grew 9.5% to R$1,052.8 million with an Adjusted EBITDA Margin of 40.1%.

FY23 Adjusted Internet Revenue elevated 10.5% YoY, reaching R$591.1 million, with an adjusted EPS progress of 11.5% in the identical interval.

Money conversion of 97.1% producing R$1,088.8 million of money stream from working actions that resulted in a money place of R$553.0 million.

Round 268 thousand month-to-month energetic physicians and medical college students utilizing Afya’s Digital Service, an improve of two.8% over the identical interval final 12 months.

In a sentence, AFYA did nicely in 2023.

There’s nothing incorrect there.

Steering

I like an organization that provides good (i.e., reliable) steering, since that tells me two issues. One, administration is aware of their enterprise. Two, the enterprise is predictable.

AFYA’s administration has supplied correct income steering since its IPO in 2019; its precise income usually exceeded analysts’ estimates.

In search of Alpha Earnings Web page

The corporate exceeded the excessive finish of its personal 2023 internet income steering and met its adjusted EBITDA estimates.

2023 Type 6K web page 3

This isn’t an remoted case. Administration additionally met its beforehand guided adjusted internet income and adjusted EBITDA.

2022 Type 6K web page 4

Equally spectacular is how usually administration has exceeded analysts’ earnings estimates.

In search of Alpha Earnings Web page

All these give me a excessive diploma of confidence that administration can ship their steering for 2024.

2023 Type 6K web page 3

AFYA’s administration is assured that it could actually proceed to spice up internet income and adjusted EBITDA in 2024.

There’s nothing incorrect there.

Till we take a better take a look at the projected progress.

Dangers of Declining Progress

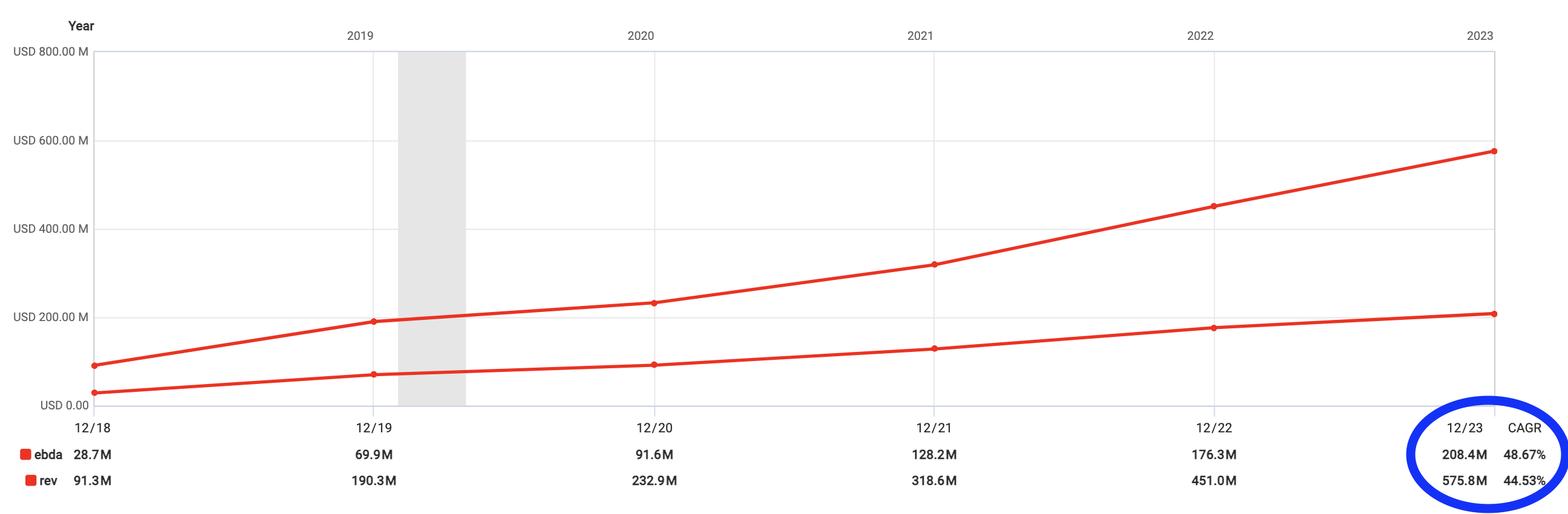

Though AFYA’s had been rising quickly over the previous few years, the corporate’s progress charges have been declining.

The rise in income, internet working money stream, and internet earnings from 2018 to 2023 was a powerful 44.53%, 57.22%, and 26.78%, respectively.

AFYA’s progress from 2018 to 2023 in BRL (not USD)

Nevertheless, when in comparison with the interval from 2018 to 2022 when the rise in income, internet working money stream, and internet earnings have been 53.85% (versus 44.53%), 67.36% (versus 57.22%), and 34.96% (versus 26.78%) respectively, it’s clear that the expansion charges have declined considerably.

That may very well be the rationale for sensible cash abandoning AFYA in droves, which is the fading progress story. Based on Morningstar, 13 of the highest 20 institutional traders have bought 50% to 100% of their stake in AFYA from September 2023 to December 2023. From July 2023 to March 2024, of the highest 20 funds that personal AFYA, 11 dumped 100% of their shares. A complete of seven,195,250 shares, or 8% of the entire variety of shares excellent, has been bought by the highest 20 fund and institutional traders. The opposite extra benign cause may very well be sensible cash eager to lock of their large capital beneficial properties from AFYA for 2023.

The most recent steering confirms the declining progress narrative. The projected progress in 2024’s internet income and adjusted EBITDA equate to a lot decrease progress than earlier than. The decrease finish of the 2024 income projection implies a 9.6% progress, whereas the upper finish of the income projection signifies a 13.08% progress. These are good figures for a lot of corporations however hardly for one which boasted an EBITDA and income CAGR of 48.67% and 44.53%, respectively.

FAST Graphs

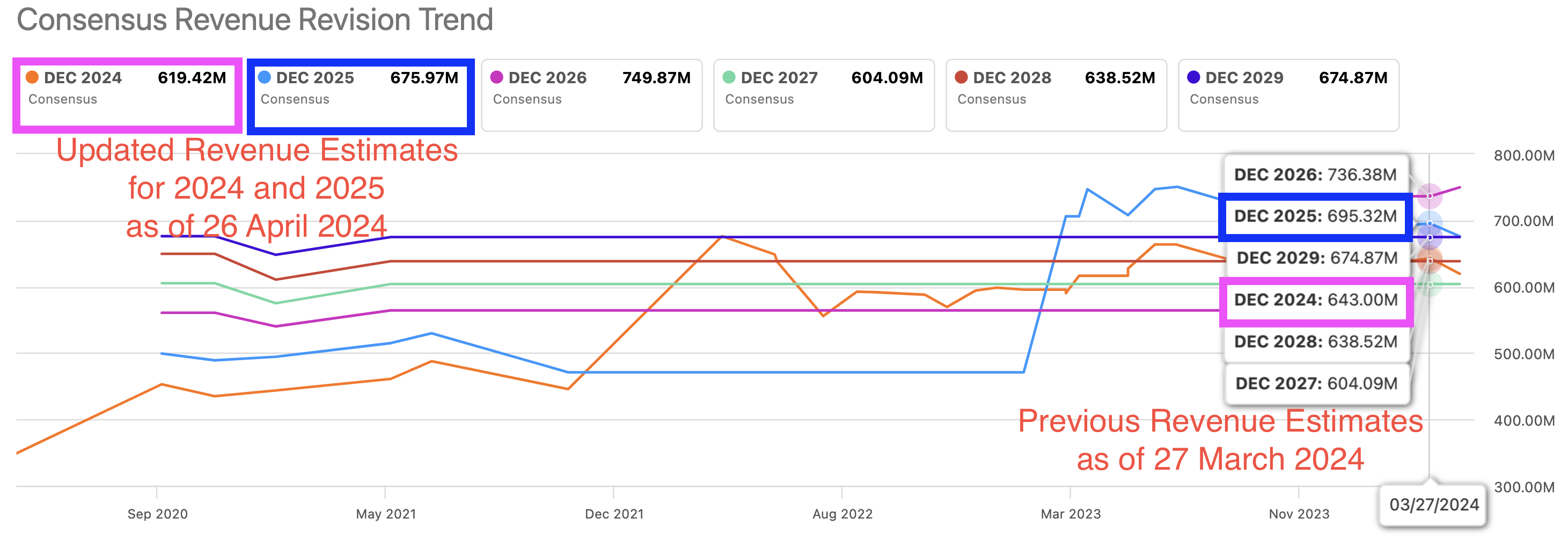

That should have been the rationale for analysts’ current downward revision of AFYA’s income and earnings.

In search of Alpha AFYA’s income estimates In search of Alpha AFYA’s Earnings estimates

Don’t get me incorrect. Regardless of the downward revision, analysts didn’t downgrade the corporate (they stored their “STRONG BUY” ranking) they usually nonetheless anticipate AFYA to develop income and earnings in 2024 and 2025.

So why is AFYA’s progress story altering?

Dangers From Regulatory Challenges

The trigger is past AFYA’s arms. CEO Virgilio Gibbon defined within the earnings call relating to the regulatory change that has affected AFYA’s outlook,

So for the second query in regards to the Mais Médicos 3 schedule. So we predict to ship the proposal now by the present schedule by July of this 12 months. And the reply will likely be solely starting of 2024 with the brand new change 2025. I am sorry.

And by the brand new altering we’ve, the change was from the earlier one. We received 36 alternatives to bid with a purpose to take part on the general public bid. And now with the change that every establishment can solely supply for one state that is decreased to 36 from 36 to 23 campuses that will likely be allowed to bid for the Mais Médicos 3. In order that’s all of the updates on this entrance, okay.

What Nonetheless Do I Like About AFYA

The decline in progress charges is one thing I’m involved about, and if double-digit progress charges are all I care about, AFYA would now not be a part of my portfolio. Nevertheless, to anticipate an organization to proceed its blistering progress fee of 40-50% indefinitely is simply unrealistic.

What I care about is proudly owning good companies which might be rising, can increase costs, have a moat, are supported by robust tailwinds, and have potential for future progress. I nonetheless see these in AFYA.

Rising Enterprise

Administration is assured that AFYA can proceed to develop its income and earnings. Analysts agree too.

AFYA’s income progress projections by FactSet (in USD) AFYA’s EPS progress projections by FactSet (in USD)

There are over 5 candidates for each medical faculty seat in Brazil, so the demand is actually there, and powerful demand comes the flexibility to boost costs.

AFYA is the biggest medical schooling service in Brazil. In 2020, Brazil has roughly 35, 000 medical faculty seats unfold over 345 medical colleges. Afya has 3,203 authorized medical seats, near 10% of all of the seats in Brazil.

That is set to develop as considered one of AFYA’s progress methods is thru acquisitions. Though the regulatory modifications to restrict the variety of seats will pose an issue, it impacts all of the medical schooling suppliers equally. Being a dominant market participant, I might argue that AFYA is greatest positioned to profit from the change, as such challenges can present extra alternatives for it to amass different seats at favorable costs.

Rising Tailwinds and Moat

AFYA’s moat comes from its distinctive enterprise mannequin that rides on the numerous wants that present the tailwinds. Within the phrases of AFYA’s CEO, he desires the corporate “to become reference on medical education in Brazil and create a lifelong learning experience that is extraordinary for our physicians, and we are serving every stage of the medical career, starting [with] the medical school, passing through the residence prep courses in all continuum and education programs that will fulfill these professional needs along their career“. In different phrases, AFYA goals to serve physicians from the time they’re college students till the purpose once they retire – and generate income all through a doctor’s skilled profession.

The Brazilian authorities continues to wish to broaden its doctor inhabitants. The CEO explains,

So, what I imagine is that the mix between the general public coverage that they are aiming to broaden extra medical seats for countryside by the medical road, mixed with any different method that may be from the authorized aspect, if that’s, would be the last resolution, could be mixed what the Minister of Training is anticipating to have as a complete enlargement for the sector… I feel will probably be the biggest influence round 9 to 10,000 seats in all the cities that the Minister of Training is aiming to have extra program or extra seats as a rise of provide for the whole nation.

This isn’t a hypothetical, “what-if” state of affairs. Brazil must develop not simply the doctor inhabitants to serve its folks, however it wants to enhance doctor high quality too.

The variety of medical colleges in Brazil has elevated dramatically. In 2000, there was a boom in the opening of latest medical colleges. The issue lies in figuring out the standard of the physicians who graduate from these colleges. Firstly, admission is predicated on the outcomes of qualifying exams and every medical faculty decides on its qualifying examination. Secondly, though there’s a standardized curriculum with the Nationwide Curricular Pointers, the rules aren’t obligatory, and solely about 85% of faculties have been compliant with this rule in 2014. Thirdly, there may be all kinds of evaluation strategies used throughout colleges.

As an educator and curriculum designer myself, all these are pink flags. How can a fundamental degree of high quality of the graduated medical practitioners be assured if the entry necessities, curriculum, and evaluation are so assorted?

Let’s assume that the totally different strategies (admission, curriculum, and evaluation) are equally good, a easy post-graduation evaluation could make that dedication if graduates from the totally different medical colleges can cross a standardized take a look at. Nevertheless, based on the authors of this paper on the medical schooling science in Brazil,

Though there have been some makes an attempt to manage nationwide exams after the pre-clinical stage, the medical stage, and upon commencement, sadly, none of those efforts have been sustainable. Though nationwide exams have been additionally theoretically part of the “More Physicians” regulation, till now, they weren’t enforced in follow.

The above results in the subsequent tailwind, which comes within the type of AFYA’s Persevering with Training and Digital Companies enterprise. The authors on the medical education scene in Brazil continue,

With a view to hold the physicians present of their information and follow a number of establishments, similar to universities, specialty medical societies, hospitals and facilities of excellence supplies programs, conferences, and lectures in every specialty. Usually, these conferences and scientific manufacturing are transformed into factors. The accountability to trace these factors acknowledging sufficiency within the efficiency of the doctor persevering with medical schooling is centered in every specialty medical societies and authorized by the Scientific Council of the AMB. This method has the benefit to be unified, nonetheless, there may be some criticism in regards to the growing prices for the doctor personally to keep up these factors.

As soon as physicians graduate, they needn’t apply for recertification, though that’s inspired. Whereas recertification is voluntary, all medical doctors in Brazil are legally required to take part in CME (Persevering with Medical Training) to keep up their license, following Federal Council of Drugs’s (CFM) Decision No. 1.984/2012 which straight addresses the duty of physicians in Brazil to take part in Persevering with Medical Teaching programs.

AFYA’s Persevering with Training fills this want for the rising doctor inhabitants.

On the identical time, AFYA’s Digital Companies fills one other want. Thus far, 265,000 customers, representing greater than 34% of all medical college students and physicians in Brazil, are utilizing AFYA’s Digital Companies. As extra folks use it, the stickier it turns into and the stronger the moat, since physicians would discover it handy to speak and share vital affected person data by a standard and safe digital platform just like the one AFYA gives. In an atmosphere the place the standard of physicians is unsure (as a result of non-standard nature of the best way medical colleges admit, train, and assess their college students) being in an ecosystem the place graduated physicians can proceed to work together and be taught from different physicians extra skilled and educated than them might help everybody degree up.

Rising Margins

CFO Luis Blanco mentioned,

As an entire, we see in our three segments, margin expansions throughout 2024. Beginning with the continued instructional, what we see that we’ll broaden margins as a result of we’re having leverage, leveraging, operational leverage operations…

Concerning our digital service, what we see that with the expansions of our service, the expansions in our B2B customers and the brand new B2B contracts, we’re going to see growing in margins 12 months over 12 months as nicely.

And in undergrad, we’ve the truth that we finalized the integrations of UNIT in final November. So will probably be the primary 12 months that will likely be 100% of FITS having UNIMA/FITS FCM Jabotão being 100% built-in…

So with these situations, we’re comfy to present this steering of 2024, whereas implied expansions by way of EBITDA margins for 2024, for those who examine to 2023.

And the margin enlargement is throughout all three enterprise segments. The CFO added,

… by way of high line, we are able to anticipate round 10% within the undergrad section, round 20% within the persevering with instructional, and round 30% by way of digital service enlargement in high line.

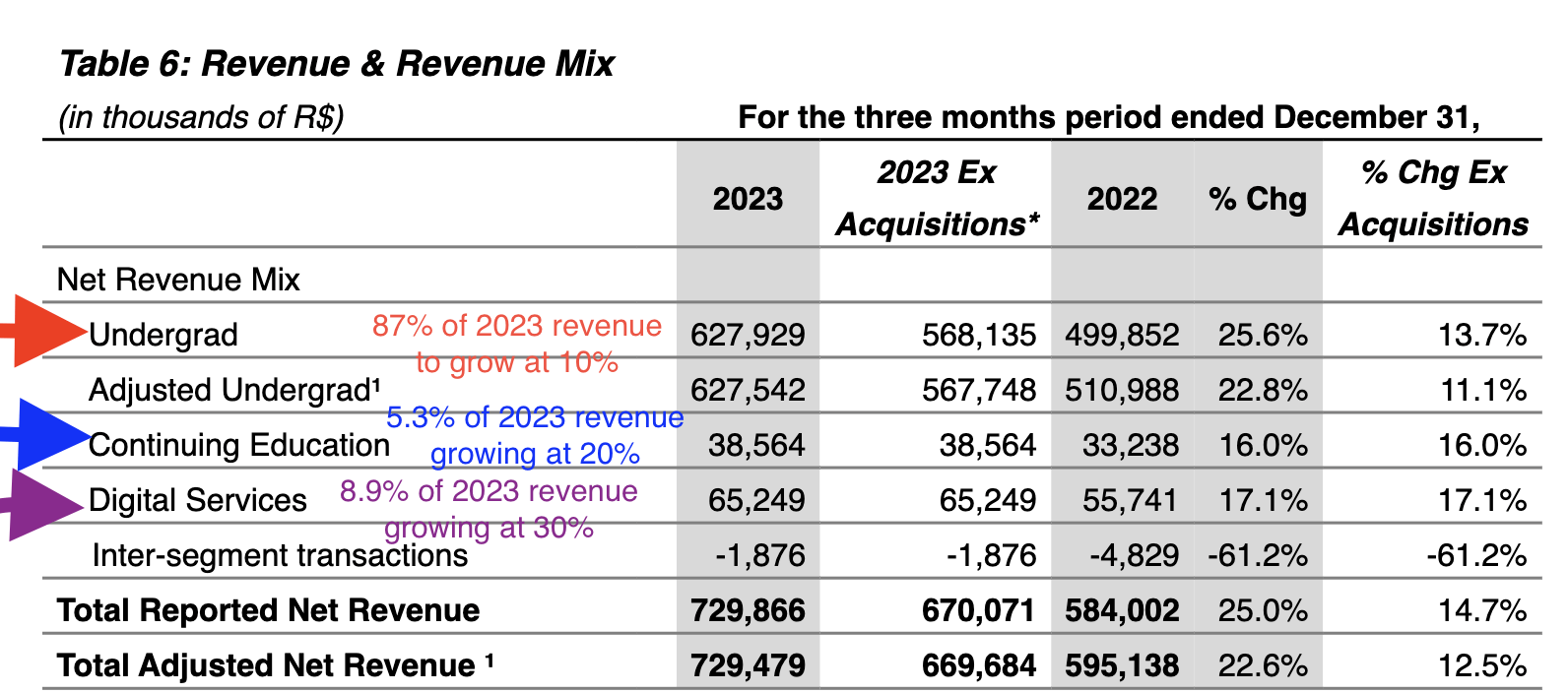

The 20% and 30% progress charges for Persevering with Training and Digital Companies sound nice, however these are the smallest revenue-generating segments. The biggest income contributor – Undergrad – is the slowest rising at 10%. Within the brief time period, having the biggest income section rising the slowest isn’t factor, and traders are naturally involved.

AFYA Type 6K web page 7

Nevertheless, if we are able to mission the expansion for every section a number of years out, the narrative modifications.

Writer’s Income Contribution Projection

Assuming the expansion charges of 10% for Undergrad, 20% for Persevering with Training, and 30% for Digital Companies stay fixed for 2024, 2025, and 2026, the income contribution from the 2 smallest segments that made up a complete of 13% of 2023’s income would contribute 20% in 2026, and if projected additional out to 2028, these two segments may contribute as much as 25% of AFYA’s complete income.

Sure, the Undergrad section would nonetheless be its largest income contributor, however an more and more giant portion of the income could be coming from the Persevering with Training and Digital Companies segments.

Earlier, I wrote,

The Undergrad Section supplies instructional providers by undergraduate programs associated to drugs, and different well being sciences in addition to different undergraduate applications.

The Persevering with Training Section supplies specialization applications and graduate programs for licensed physicians.

The Digital Companies supplies content material and know-how for medical schooling, medical selections software program, follow administration instruments (that embody digital medical data, telemedicine and digital prescription for physicians), and doctor-patient relationship and supplies entry, demand, and effectivity for the healthcare gamers.

The present uncertainty from the regulatory challenges impacts the Undergrad section, however not the Persevering with Training and Digital Companies section. I might add that there’s much less volatility within the earnings and income anticipated from these two smaller segments since they arrive from current physicians and enrolled medical college students, and as long as AFYA can present applications, programs, and software program options to value-add a rising inhabitants of medical doctors, these section would proceed to develop, by cross-selling and upselling AFYA’s plethora of providers.

This speaks to the foresight the present administration has, to broaden its capabilities to generate extra income streams which might be much less prone to be disrupted by regulatory modifications.

Rising Potential For Future Progress

The CEO talks up the B2B engagement,

This consequence underscores the huge alternative in digital providers, pushed by the ramp-up in B2B engagements, securing new contracts with pharmaceutical business corporations, and the continual enlargement in B2B contracts…

Concurrently, we’re increasing our ecosystem to facilitate new interactions and income streams past physicians, together with engagements with pharmaceutical gamers, hospitals, labs, and drugstore chains. Proof of this enlargement is seen within the progress of our B2B technique, fortifying our market presence and increasing our attain. Consequently, we achieved a 64% year-over-year progress in our B2B revenues.

Presently, AFYA is holding its B2B enterprise to the Brazilian market, however this can be a scalable resolution, so as soon as AFYA is able to supply its Digital Companies to the worldwide market, it’s straightforward to think about the a lot bigger complete addressable market that AFYA’s B2B resolution can serve.

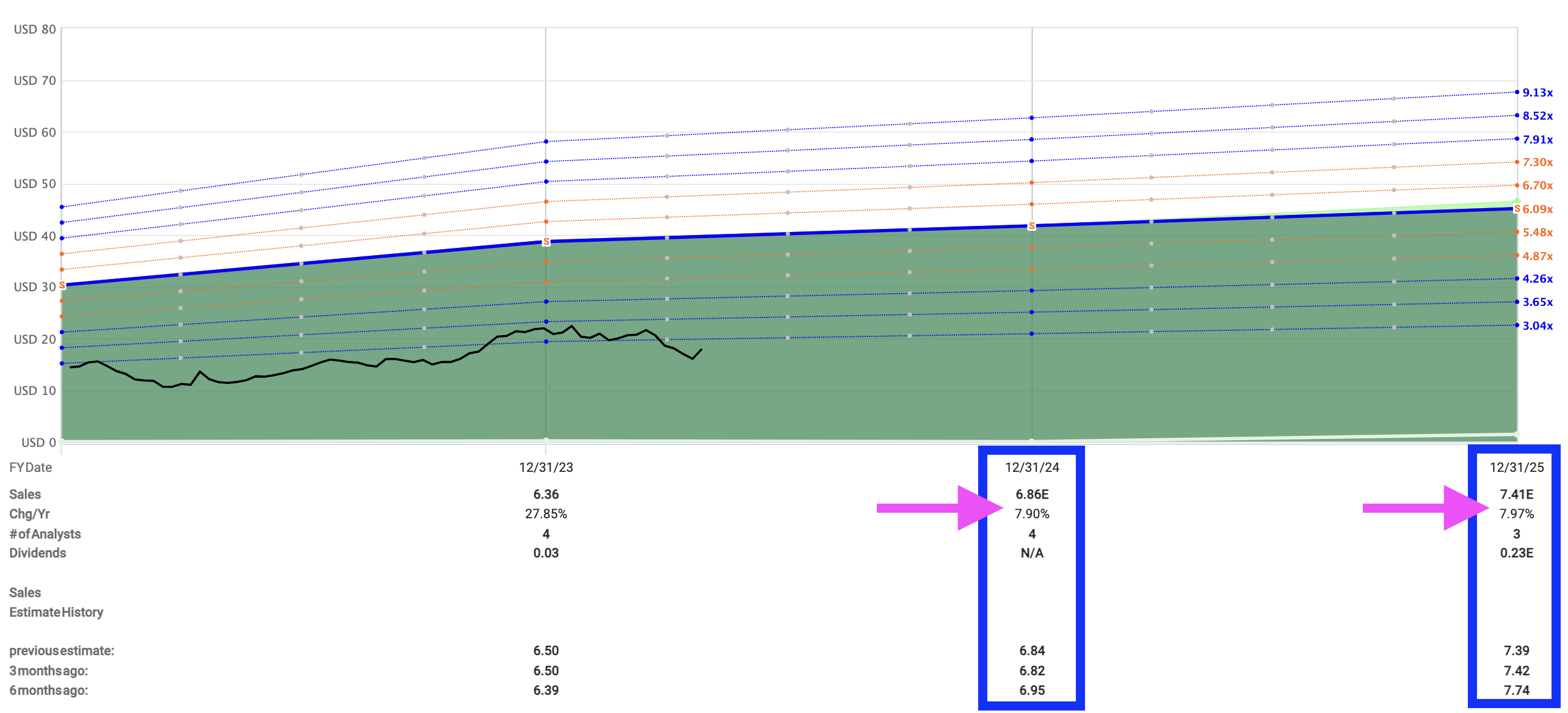

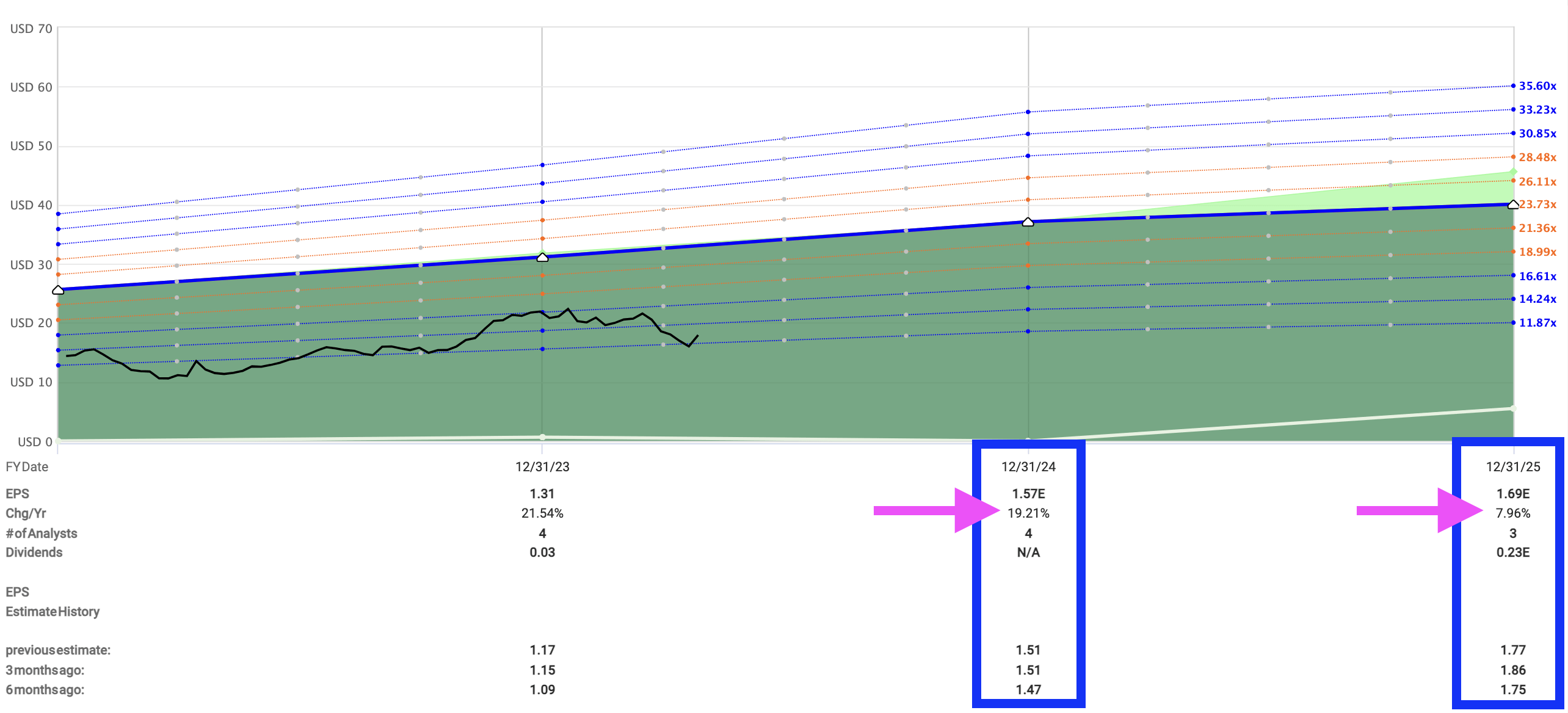

Valuation

My valuation for AYFA ranges from $18.46 per share in my bear case state of affairs of simply 5% progress in earnings, which is decrease than the 5.8% value improve that AFYA can levy on their undergrads (based on Renata Couto in the course of the earnings convention) and assuming a a number of compression to 10, to a excessive of $37.08 per share in my best-case state of affairs. In different phrases, even in my unlikely bear case, AFYA could be buying and selling round its truthful worth at its closing value of $17.94 on 26 April 2024. If AFYA’s truthful worth is near my estimate of $22.01, which was near the place it reached its 52-week-high, and near consensus analysts’ value goal of $23.52, shopping for AFYA on the present value gives no less than a 37% margin of security.

Even when I’m incorrect and AFYA is pretty valued now, paying truthful worth for a enterprise that’s nonetheless rising income and earnings, can increase costs, has a moat, is supported by robust tailwinds, and has potential for future explosive progress within the digital providers section, doesn’t sound too unhealthy. The chance and reward of investing in AFYA appear good to me.

Writer’s truthful worth estimate

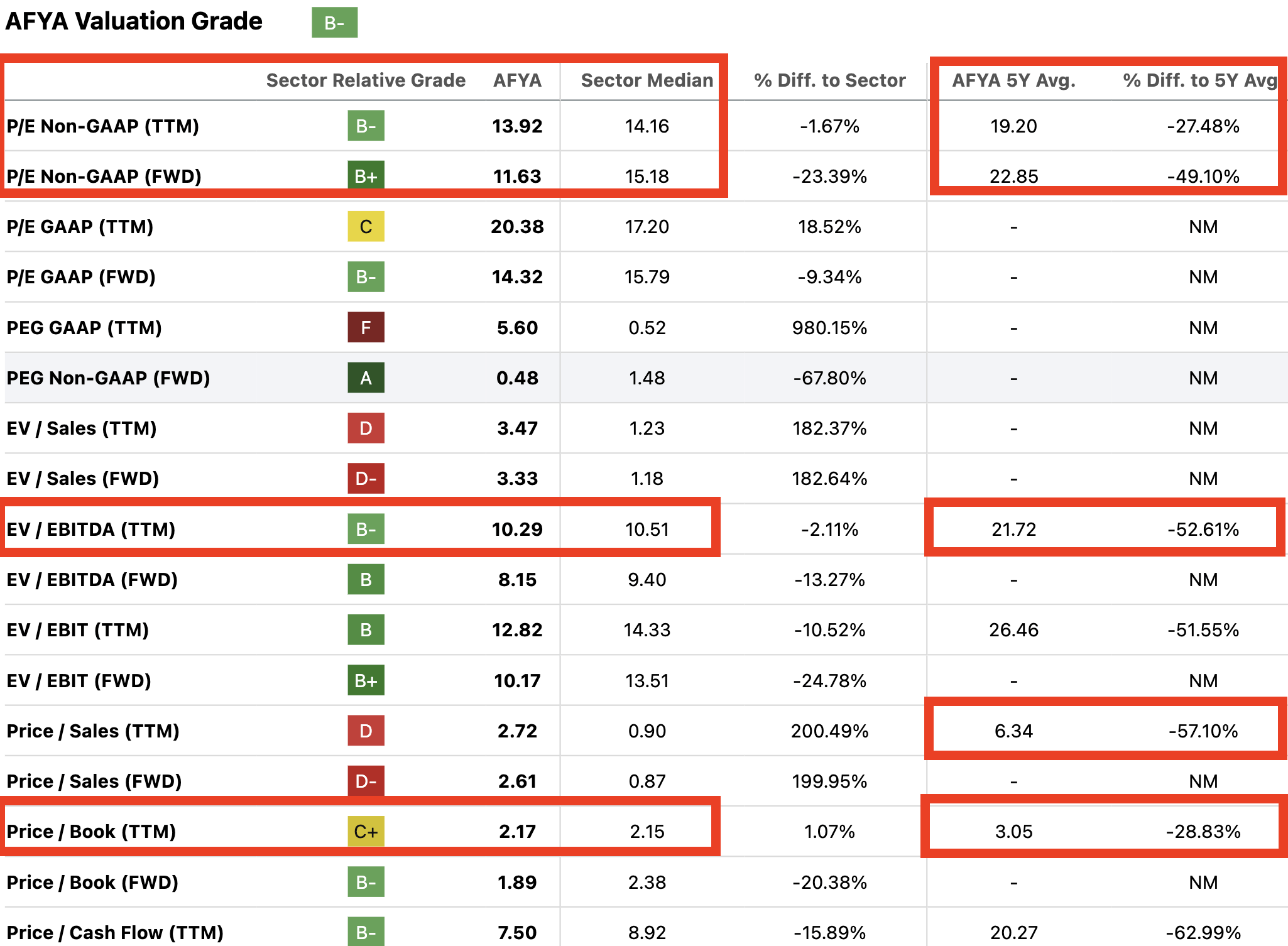

By relative valuation, AFYA can also be low-cost on the present value. On a P/E, P/B, and EV/EBITDA foundation, AFYA is buying and selling under each its 5-year common in addition to its friends.

In search of Alpha AFYA Valuation Metrics

Conclusion

AFYA has been battered because of a mix of things. It’s going through regulatory modifications in Brazil. Its income and earnings progress charges are declining. And institutional traders have largely deserted it.

Nevertheless, as an investor seeking to personal a enterprise that has a dominant place, continues to develop earnings and earnings, can increase costs, has a moat, is supported by robust tailwinds, and has the potential for future explosive progress within the digital providers section, AFYA is a possible candidate.

Plus, AFYA’s quickest rising segments, Persevering with Training and Digital Companies, can turn out to be main income contributors in time to return, which can present much more predictability and stability within the firm’s income and earnings progress.

After the large value decline over the previous 1 month, AFYA appears attractively valued once more. With that vast margin of security as a result of depressed value, even a slight blended P/E enlargement from 12.87 to 13.99 which is extra in keeping with its slower progress fee may nonetheless supply traders a 31% capital achieve in two years.

FAST Graphs

After the value ran up by 45% within the six months after my first article was revealed, I beat myself up for not growing my place. Due to Mr Market, who has been very detrimental about AFYA recently, I managed to double my place. I imagine Mr Market is mistaken about AFYA. Sure, progress has declined, but when AFYA could be considered as a reliable and good enterprise that may develop at round 10% a 12 months, then it actually deserves a better a number of and is a BUY. In case you are AFYA as a enterprise that’s now not in progress mode, and explosive progress is all that issues, then AFYA could be a SELL for you.

It’s nonetheless a comparatively small place in my portfolio, and as Brazil is a geographical location that I’m not conversant in, I’m assigning a BUY reasonably than a STRONG BUY.

Another excuse for the BUY reasonably than a STRONG BUY lies within the lower in its money place, from $201 million in 2021 to $113.8 million in December 2023. For an organization that seeks progress through acquisition in addition to organically, having much less money could imply it has to borrow extra and at greater rates of interest. Having much less money will put a lid on its growth-via-acquisition technique.

FAST Graphs

That is one thing I’ll take into account, however I might not be overly apprehensive as the corporate is rising income and internet working money stream properly, and extra importantly, the expansion of the working money stream (43.11%) exceeds the expansion of its complete debt (35.87%), which tells me that this can be a enterprise that may develop organically and is not only depending on spending to amass extra income. I’m glad that administration is being financially prudent and is making efforts to pay down debt reasonably than taking over extra debt to go on an all-out acquisition frenzy. CFO Luis Blanco mentioned,

The money stream from working actions was allotted to earnings tax and lease funds, CapEx actions, for the service of the monetary debt, for our share buyback program, alongside the extra acquisitions of 15% of FMIT. Excluding the enterprise mixtures of UNIMA, we have been in a position to generate R$391 million as free money and scale back our internet debt within the 12-month interval… We proceed to keep up a low price of debt that continues to be under the CDI charges.

Please do your due diligence and determine your place sizing.