Dimensions/E+ by way of Getty Pictures

Agilysys, Inc. (NASDAQ:AGYS) is within the enterprise of creating experiences for a lot of vacationers all over the world smoother and extra environment friendly. AGYS is within the candy spot between progress and profitability, with 21% income progress mixed with a stable 13% EBITDA margin. Within the present surroundings, the main focus continues to be on the businesses with distinctive progress and people with progress on the proper worth (GARP). ASYS falls into this bucket with an extended observe report of progress and earnings progress, albeit a bumpy trajectory till lately.

The corporate continues to develop its hospitality cloud providing, pushing for an elevated subscription element to maximise buyer life cycle revenues. This push has additionally resulted in elevated R&D bills to enhance product choices and supply a holistic providing for hospitality shoppers. The corporate has some main shoppers with massive pockets, together with the most important casinos in america, giving a stable earnings outlook and good visibility. Wanting into the main points, you’ll be able to see why it is a stable decide for a progress investor portfolio.

Q1 Investor Presentation (AGYS IR)

Fiscal Q3 – Sturdy finish to Calendar 2023

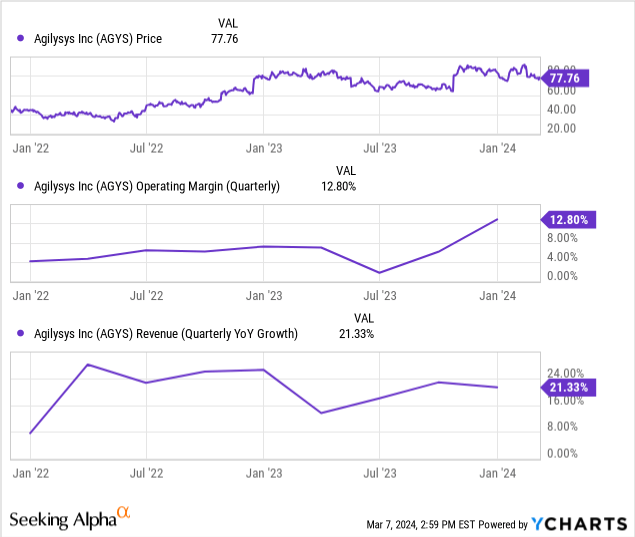

This small-cap firm is seeing continued power even throughout this era of macroeconomic uncertainty, with each improved income and margins. Revenue was 60.6m, of which a report 35.1m was recurring income. This 21% income progress is sort of stable, with 29.9% progress of their subscription options. This progress is highlighted by a powerful 90% of their 81 properties added within the quarter had been subscription-based.

This momentum in promoting their recurring options means larger margins and higher long-term worth going ahead. Gross margins had been up 0.8% y/y to 62.5%. The corporate continues to maneuver in the direction of a subscription mannequin to extend its recurring income as a portion of complete income. This can improve margins in the long run, though for now there may be variability in margins quick time period.

As you’ll be able to see under, working margins have improved for the reason that post-COVID hospitality recession, enhancing to 12.8% in the latest quarter. This has led to a stable $20.1m of working earnings for the previous 12 months. Income progress has been inconsistent however stabilizing now within the excessive teen % vary with the bulk now subscription revenues. Product income from their InfoGenesis POS system is doing effectively regardless of changing into extra standardized throughout working techniques and cell choices, hurting their product income progress (much less required POS techniques attributable to enhancing the product). That is decrease margin income, nonetheless, and is one other tailwind for margins on the subscription portion of the enterprise.

A extra streamlined providing from AGYS is a purpose they’ve been in a position to upsell very effectively of their current buyer base, together with including a number of new properties and resorts inside these clients. Their property administration system additionally had a powerful quarter, including 11 clients, top-of-the-line quarters ever for AGYS. Energy has been coming from Europe and North America, with weak spot nonetheless current in Asia with tourism persevering with to select up by way of 2024. Giant corporations proceed to maneuver in the direction of a subscription mannequin at the same time as software program stays on-premise. AGYS is providing a full stack of options together with bodily choices,

Gross sales backlog is up 6% in comparison with a yr in the past, with the sturdy current conversion of shoppers slowing pipeline progress for the approaching fiscal yr. They’re nonetheless guided to a stable 17.5% progress of income however the upside to that quantity is probably going as service areas proceed to strengthen. After full-year income progress of 21.8% in F2023 to $198.1 million, AGYS is not seeing a major slowdown in demand like different software program corporations. They elevated steering after the Christmas quarter as much as $236.5m on the midpoint for F2024 ending after the present quarter.

The corporate continues to put money into advertising, cloud infrastructure, and assist for future progress, however will nonetheless hit 15% EBITDA margins for the yr. Contemplating the corporate is a small dimension persevering with to concentrate on longer-term alternatives is important to creating long-term worth. Additionally they want to remain forward of the competitors, particularly as a result of small nature of their goal market in hospitality. They’re leaning right into a full subscription mannequin which has helped enhance margins, and managed to proceed to develop at a gentle cadence all of the whereas. Mixed with a current pullback from an all-time excessive of $91 to now $77, the inventory has develop into fairly fascinating from a valuation perspective.

As you’ll be able to see above, working margins have continued to tick larger and income progress has stayed sturdy even after minor hiccups in 2023. Even amid the stable efficiency, the inventory has lagged with -an 11% return over the previous yr. Current underperformance has been attributable to a brief downswing from promoting shareholders unloading shares. Normally, conditions corresponding to this are good shopping for alternatives as the basics stay unchanged however costs are decrease.

The shareholders bought 3.4% of excellent shares in February, however the worth has fallen 15% exhibiting an overdone response. It is a nice alternative for brand spanking new cash to build up shares, and different funds are possible shopping for now based mostly on short-term weak spot.

Conclusion – Providing creating alternative

Agilysys, Inc. inventory is a good buy now as funds begin to rotate out of mega-cap names into smaller corporations by way of 2024. In the event you imagine in that chance, corporations like Agilysis ought to do effectively with its mixture of progress, profitability, and affordable valuation. The inventory is above current assist and has been at all-time highs in 2024, with the potential to push by way of these ranges in spring or summer time. That is one that may stay underneath the radar attributable to its B2B nature and small dimension, however shouldn’t be ignored for sturdy capital achieve potential for 2024.