winhorse/iStock Unreleased by way of Getty Photos

AIA Group (OTCPK:AAIGF) has come down considerably since my first coverage of it in June 2023 when it shouldn’t have. Regardless of the Group’s sturdy monetary efficiency, the market has been cautious of its Chinese language publicity. These “exogenous factors”, nonetheless, by no means had a lot of an influence on the basics of the enterprise which at current look as sound as ever.

Monetary replace

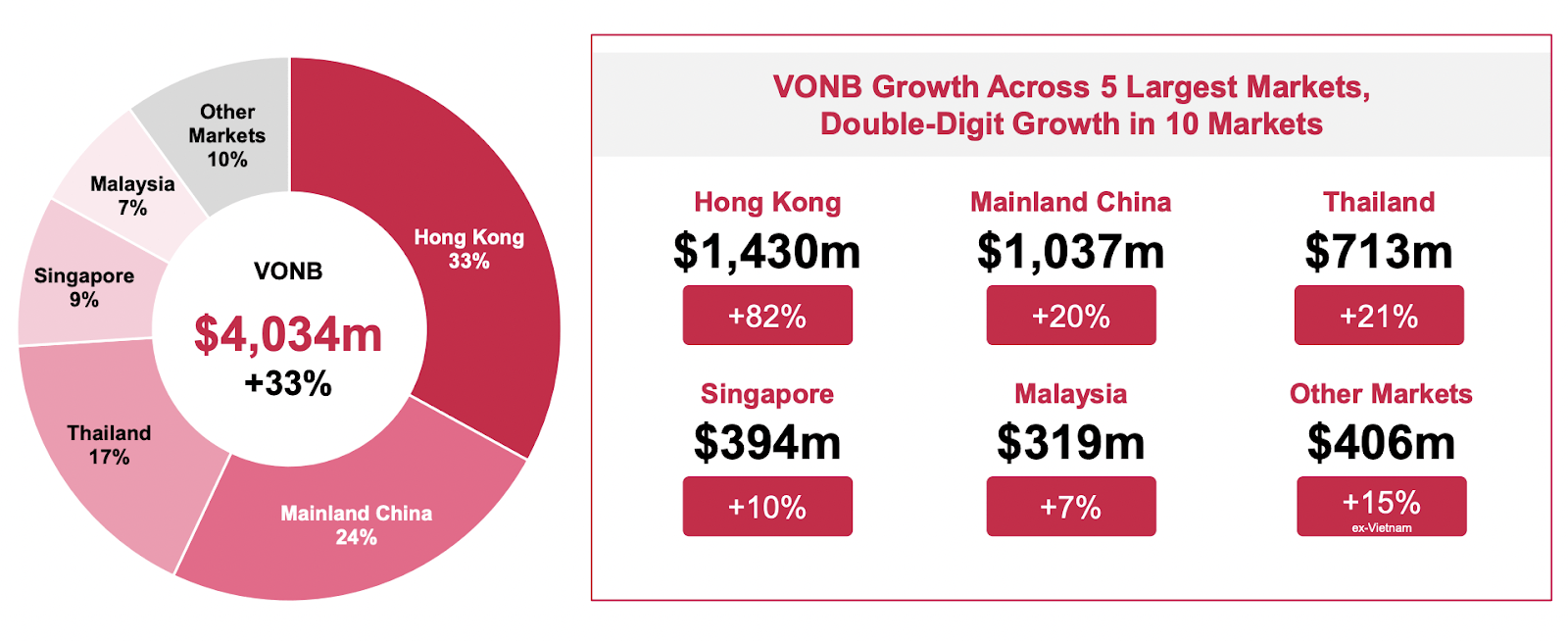

AIA Group reported its financial results for the 12 months ended 31 December 2023 on March 14th. The outcomes had been decisively optimistic, notably growth-wise. Worth of recent enterprise (VONB), a key efficiency metric, hit US$4,034m, lastly nearing the pre-pandemic excessive of $4,154m reached in 2019. Actually, Annualized New Premiums (ANP), one other development metric, added 45% and reached a file excessive of US$7,650m. For context, the very best earlier than COVID-19 was US$6,585m recorded in 2019. VONB margin, a measure of profitability, got here to 52%.

All 4 principal markets — Mainland China, Hong Kong, ASEAN, and India (i.e., TATA AIA Life) — delivered double-digit VONB development numbers in 2023. ASEAN, the most important market total comprising Thailand, Singapore, and Malaysia (this time sans Vietnam the place the insurance coverage business is reeling from a trust crisis)— was up 14% and introduced ⅓ of the Group VONB, equal to about US$1.5b. The unique AIA Hong Kong recorded the very best development determine of all, 82%, including US$1.4b. Mainland China ended up at plus 20% and US$1b.

AIA Group

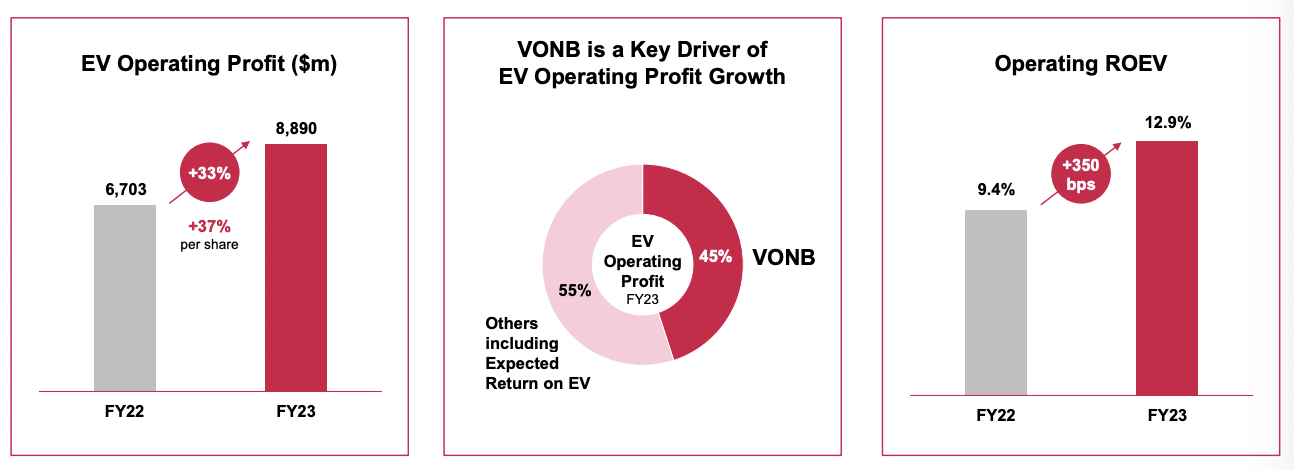

Earnings, because of this, rose too. Particularly these primarily based on embedded worth (EV), an insurance-specific measurement of whole shareholder worth: EV working revenue was up by 37% per share to US$8,890m. Return on EV working revenue elevated from 9.4% to 12.9%. Although conventionally reported working revenue after tax at US$6,213m stayed flattish, plus 2% per share, as a result of greater medical claims in the course of the 12 months.

AIA Group

The AIA distinction

The Group added over 1.5m new clients in 2023, 10% greater than final 12 months. The commonest factor cited for driving growth is larger productiveness from each company and bancassurance, throughout markets.

Even in China, the place most different insurers have lost agents, AIA claims to have augmented its workforce as a substitute. AIA China elevated new recruits by 59% final 12 months, with agent productiveness twice the peer common. Elsewhere too, the group-wide focus is on elevating the professionalism of agents while supporting them with digital solutions — precisely the place the business is meant to be shifting. Bancassurance is rising briskly, led by ASEAN.

“We have the world’s most professional agency that has been number one MDRT globally for the last nine years. We are also individually the number one in Mainland China, Hong Kong, ASEAN and India. And we have grown MDRT qualifiers by a further 20% in 2023, proving the success of our high quality model.”

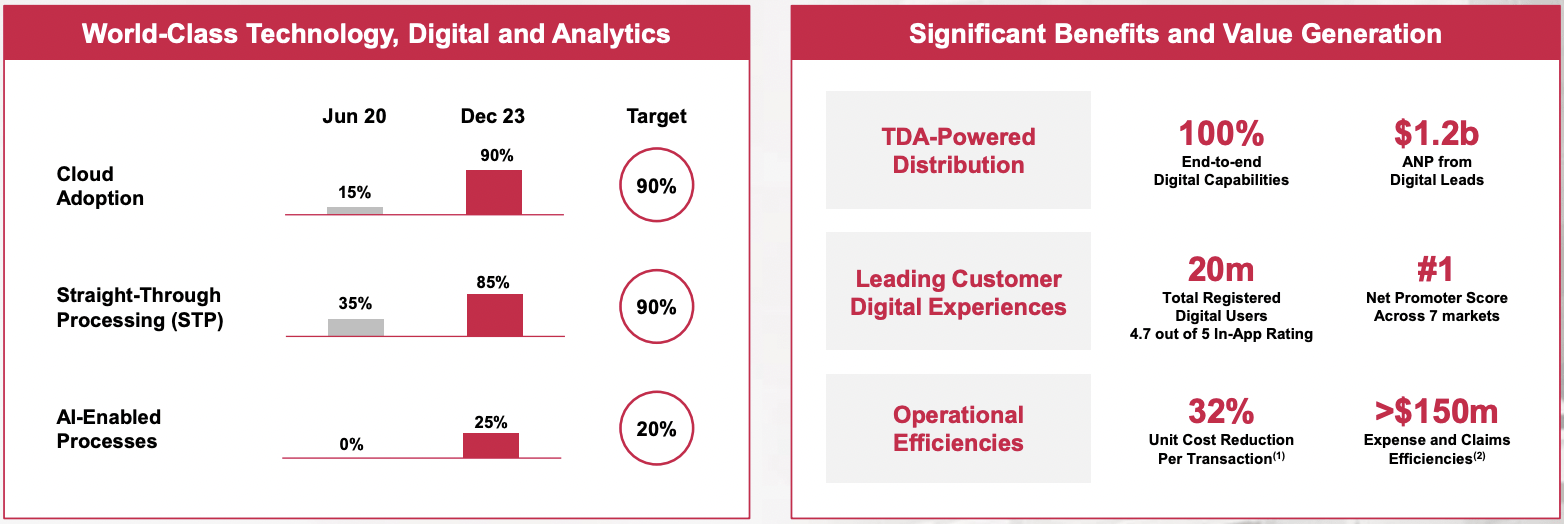

One other technique on the middle of AIA is in depth software of technology, digital (solutions) and analytics (TDA). Greater than US$800m invested over the previous three years has elevated lead era, buyer expertise, and operational effectivity. AI is being leveraged for each company and buyer administration, resulting in higher productiveness and therefore greater gross sales.

11 markets out of 18 in whole have been totally digitized, with merchandise turning into out there on-line and brokers with the ability to attain clients on digital platforms. AIA’s lead in TDA helps it win over youthful digitally savvy clients, to accumulate them and get them to stay round. (To that I can attest as a buyer myself.)

AIA Group

Valuation

After dropping 31% (30% with dividends) over the previous 12 months and 41% (38%) within the final three years (AAIGF returned -25% and -39% in whole in the identical intervals), SEHK:1299 is the most affordable in 5 years, at a Value/EVPS of 1.41. The consensus price target is excessive, with 12-month forecast at HK$96.80, greater than 70% up from HK$55.95 as of March 23.

|

SEHK:1299 |

FY2023 |

FY2022 |

FY2021 |

FY2020 |

FY2019 |

|

Value |

HK$68.5 |

HK$86.8 |

HK$78.6 |

HK$95.0 |

HK$82.2 |

|

EV per share |

US$6.26 |

US$5.87 |

US$6.03 |

US$5.41 |

US$5.14 |

|

Value/EV per share |

1.41 |

1.89 |

1.68 |

2.27 |

2.06 |

Supply: Annual reviews 2020 and 2022, monetary outcomes 2023

Dividend

At 2.9%, the yield is just not a lot for a Hong Kong inventory however payments have been growing consistently, by about 14% per 12 months since 2014. The dividend coverage is secure, and since earnings (and money flows) cowl funds comfortably, the yield might be anticipated to continue to grow.

Dangers

The primary concern on everybody’s thoughts is China. It’s geopolitics, actually an indelible a part of investing in China and/or Hong Kong. Additionally it is the debt state of affairs and underwhelming financial restoration thus far — issues that might take longer to resolve. It’s value remembering although that AIA is as diversified all through Asia as might be, and China (the place it owns simply 1% of the market) is just not its largest territory by worth contribution.

Conclusion

I consider the efficiency momentum AIA has constructed for the reason that finish of COVID-19 will proceed. The AIA benefit in brokers and TDA might show to be the suitable mixture for continued development in Asia’s dynamic insurance coverage markets. Issues won’t be excellent given the inherent issues of working in China, however different markets, ASEAN particularly, can simply decide up the slack. (And the smaller base in China might assist maintain AIA’s development numbers in the long run.) Total, AIA is a strong development revenue inventory with a optimistic outlook.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please concentrate on the dangers related to these shares.