eternalcreative

Alarum Applied sciences Inc (NASDAQ:ALAR) reported its newest quarterly outcomes capping off a transformative 12 months for the Israel-based software program firm. A call to exit the cybersecurity enterprise and different non-core segments in 2023 to deal with its “NetNut” net knowledge assortment platform has paid off evidenced by sharply greater gross sales and profitability. The introduction of latest synthetic intelligence-based instruments has represented a brand new progress driver.

The corporate with a market cap of simply $120 million continues to be tiny, however proving it has some actual worth supported by spectacular working developments and stable fundamentals. Shares of ALAR are up greater than 1,100% over the previous 12 months and deserve a better look.

ALAR Financials Recap

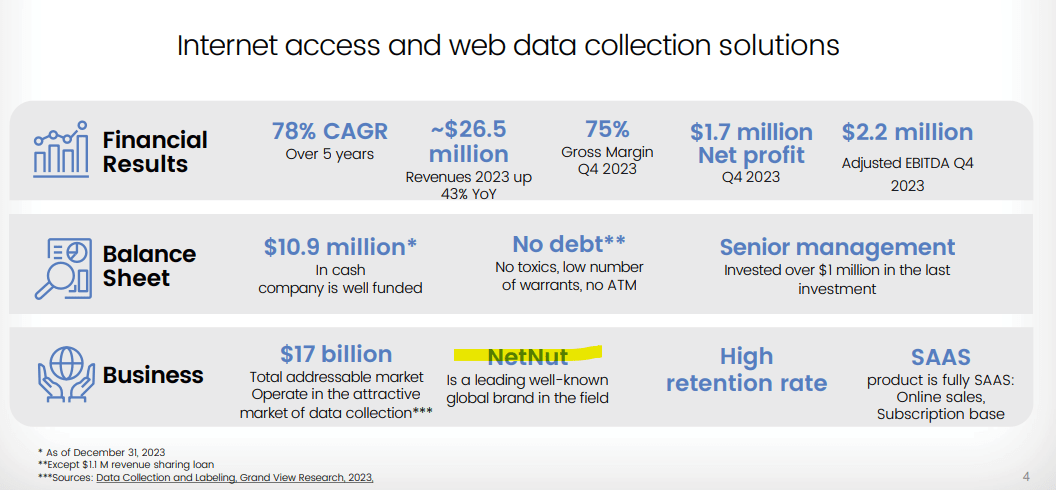

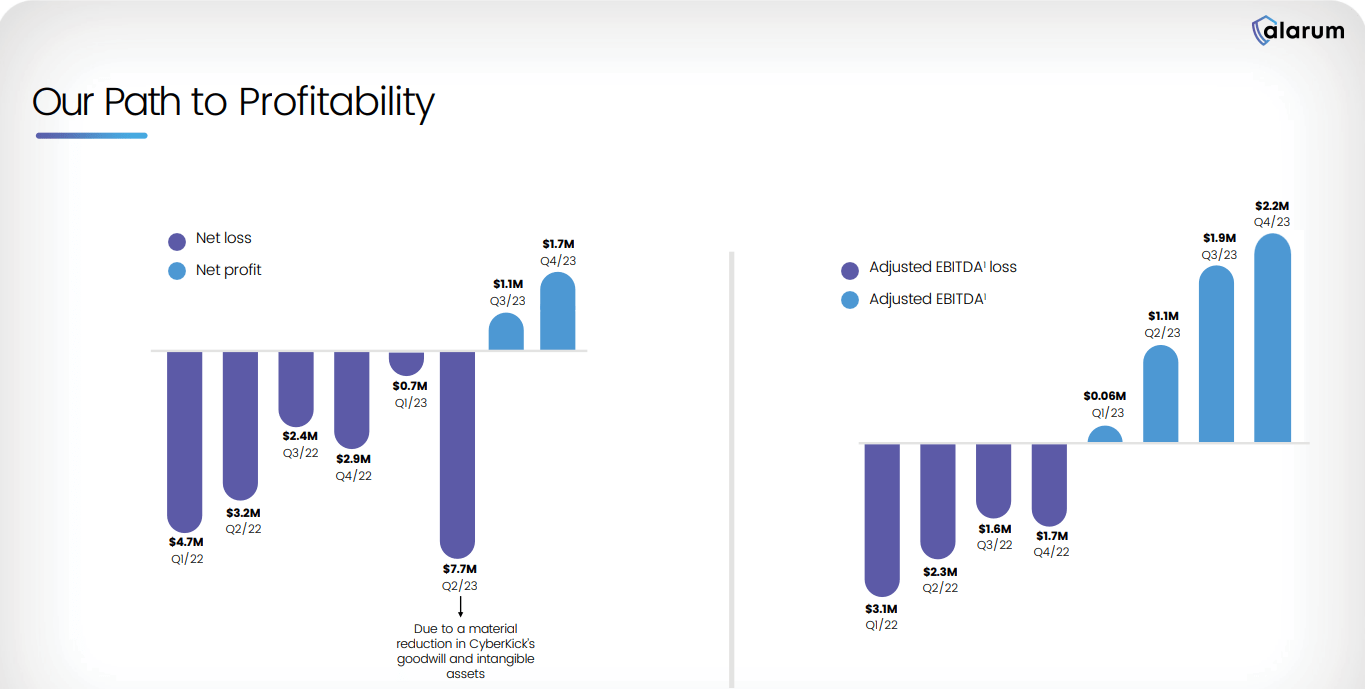

ALAR reported Q4 net profit of $1.7 million, reversing a lack of -$2.9 million within the interval final 12 months. Income of $7.1 million, climbed by 38% year-over-year, and likewise sequentially greater from $6.75 million in Q3. Full-year income of $26.5 million was up 43% y/y.

supply: firm IR

This was the second consecutive quarter of profitability with internet earnings of $1.7 million climbing from $1.3 million in Q3. For the total 12 months, there was a big write-off associated to the “CyberKicks” divestiture and accounting cost on goodwill in Q2 dragging decrease the outcomes. However, 2023 adjusted EBITDA at $5.2 million has climbed sequentially for the previous 4 quarters, together with $3.2 million in This autumn highlighting the underlying earnings momentum.

supply: firm IR

We talked about the robust progress story. NetNut full-year income of $21.3 million representing 80% of the general enterprise climbed by 150% y/y. By this measure, the underlying developments are even stronger than the headline measures counsel contemplating NetNut is now the first focus.

A part of that NetNut surge displays the launch of latest merchandise together with a SERP Scraper API whereas gaining new prospects within the fintech market. Administration notes that AI options have acquired a constructive response.

The metric that stands out is the web retention ratio which reached 153% this quarter, up from 144% in Q3. The interpretation right here is that current prospects are spending extra on numerous instruments provided, properly past the impression of normal churn.

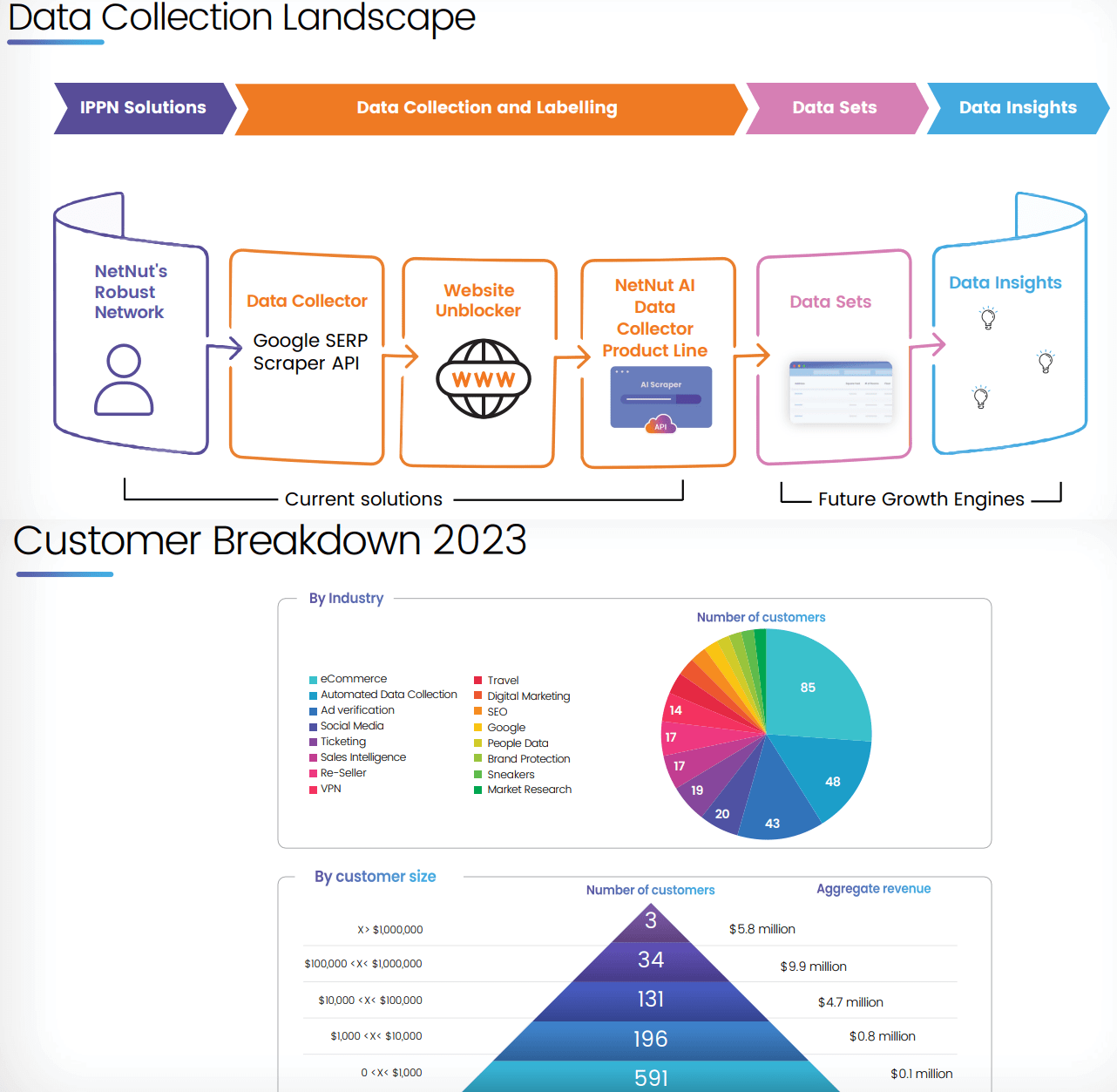

For context, the goal marketplace for Alarum are web-based companies that want to gather analytics on site visitors developments or buyer perception. By way of use circumstances, the sorts of instruments provided embrace promoting verification, model safety, search engine marketing (search engine optimisation) monitoring, and net knowledge extraction.

supply: firm IR

One instance that explains the worth proposition considers how web sites usually must current a distinct touchdown web page and even pricing choices relying on the place customers are geographically positioned. NetNuts’s Web Protocol Peering Networks (IPPN) instrument can navigate the online as a simulated consumer which is a crucial facet of competitor evaluation.

We discover that Alarum has comparatively good diversification by business protecting eCommerce prospects, social media websites, and ticketing platforms amongst others. Whereas the vast majority of accounts contribute lower than $1,000 a 12 months in income, 37 prospects are famous as driving greater than $100,000 in annual gross sales, together with 3 clearing greater than $1 million.

Lastly, we word ALAR ended the 12 months with $11 million in money towards zero debt. We view the steadiness sheet as a powerful level of the corporate’s funding profile. Whereas not providing official monetary steerage for 2024, feedback in the course of the earnings convention name projected confidence that the developments can proceed with optimism for the 12 months forward.

What’s Subsequent For ALAR?

With a present market cap of round $110 million, Alarum Applied sciences is within the micro-cap class however an outlier to any unfavorable connotation that classification carries primarily based on the newest developments. The attraction right here is that after we put the numbers collectively, it is clear to us that ALAR is greater than only a speculative “penny stock” or climbing merely attributable to AI hype.

Annualizing the This autumn earnings to $6.8 million or adjusted EBITDA to a run-rate of $8.8 billion, ALAR is buying and selling at an implied ahead P/E round 17x or 12x as an EV to ahead EBITDA a number of. In our view, these multiples are very enticing for a corporation that simply delivered 43% income progress over the previous 12 months. A baseline right here is that the corporate can a minimum of develop gross sales by 20% in 2024.

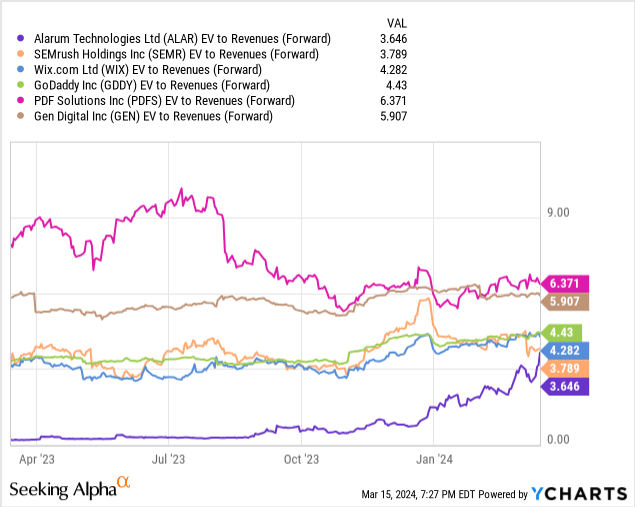

Notably, ALAR’s EV-to-revenue a number of of three.6x stays under the typical nearer to 5x for a bunch of what we might take into account to be comparable web entry, net knowledge providers suppliers together with SEMrush Holdings Inc (SEMR), Wix.com Ltd (WIX), GoDaddy Inc (GDDY), PDF Options Inc (PDFS), and Gen Digital Inc (GEN).

Naturally, Alarum with its considerably smaller scale warrants some stage of small-company low cost however we merely do not see something to counsel the inventory is materially overvalued or a “bubble” even after rallying 140% YTD.

Then again, the warning we have now is that this phase of on-line instruments geared toward web web site builders might be fragile by way of going through the aggressive atmosphere.

Administration feedback in the course of the earnings conference call famous its patents within the area in addition to established relationships as representing obstacles to entry. There may be additionally a side of excessive switching prices for patrons making an attempt to transition to a distinct product.

Nonetheless, it is a side of an organization this dimension that must be thought of throughout the danger backdrop. With a vital eye, we might additionally cite the restricted variety of massive prospects driving greater than $1 million in annual income as a weak level, in a state of affairs the place Alarum loses a contract for any variety of causes that may have an outsized impression on quarterly outcomes.

Ultimate Ideas

We charge ALAR as a purchase, with a way that the inventory stays underneath the radar, and has room to seize an enlargement of valuation multiples going ahead as the following a number of quarterly earnings affirm the monetary momentum. Monitoring factors by 2024 embrace developments within the gross margin, posted buyer internet retention ratio, money stream, and adjusted EBITDA.

We already coated a number of the dangers to think about, however we’ll add to that with an expectation for shares to stay risky and delicate to shifting progress expectations. A broader market-wide selloff or weak point within the tech sector has the potential to push shares decrease.