Andrew Burton

Introduction

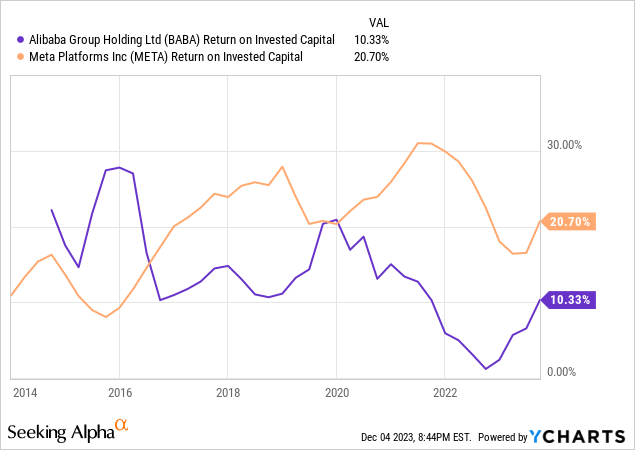

I typically hear it acknowledged that Alibaba (NYSE:BABA) is a Meta (META) like alternative, which after all will get my grasping neurons firing. The aim of this text then, is to check and distinction this chance introduced on a quantitative foundation. Maybe one would argue Meta deserves a slight premium to Alibaba, given its aggressive place and being an American firm making return of capital to shareholders just a little extra sure and fewer convoluted. Honest sufficient, and maybe the historic ROIC of the 2 firms helps the concept META has a stronger moat. Alibaba is after all just a retailer (Okay I do know it has different enterprise segments) because the late Charlie Munger lamented. The query is, is now the precise time to get grasping? Let’s discover out.

Profitability and Development

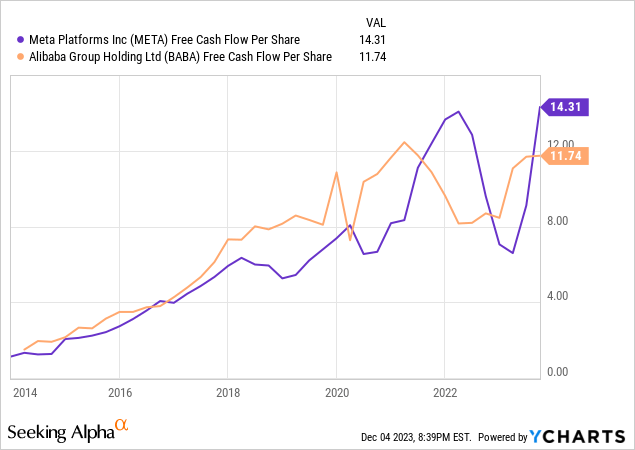

I like to have a look at per share free money stream, as tech firms are inclined to have giant quantities of inventory dilution to pay workers, with these two being no exception. Curiously sufficient, the FCF of the businesses have grown equally over time, with META extra not too long ago outperforming BABA. If that is simply cyclical in nature for BABA or if it’s a signal of the altering occasions, is but to be seen. However, I’m inclined to consider it’s short-term till confirmed in any other case, as most firms skilled a macroeconomic associated hiccup submit 2021.

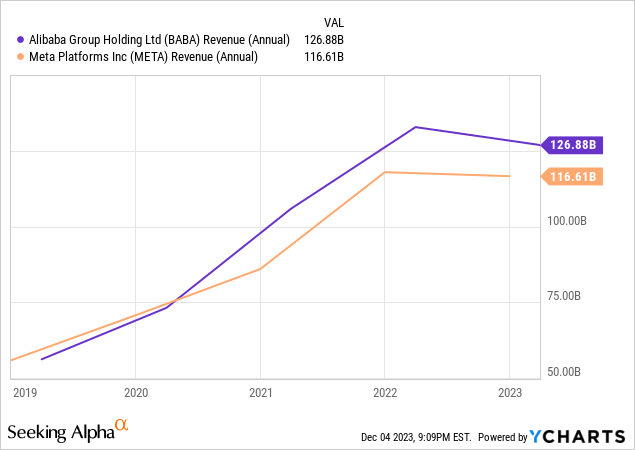

It’s fairly weird evaluating these firms, and seeing how comparable a few of the numbers are by coincidence. Income of the 2 has additionally just about elevated in lockstep over the previous couple of years, with BABA barely outperforming on this metric. In fact, as a retailer it usually has a lot decrease margins than META and each greenback of income will most likely be much less accretive.

Capital Return To Shareholders

Do you assume META is a shareholder pleasant enterprise? If sure, there may be little cause to say that BABA is just not. I wished to have a look beginning on the finish of 2021 / starting of 2022 to see how properly these two have taken benefit of the beat down in respective share value.

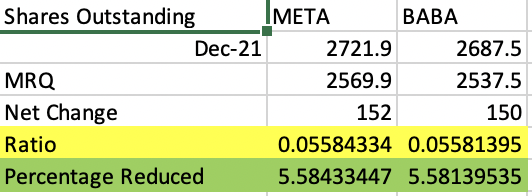

BABA shareholders might not be feeling too fortunate proper now, however in the long term, a protracted underperformance in share value mixed with inventory buybacks is after all a optimistic. Meta is utilizing a a lot bigger proportion of its free money stream to buyback inventory. The costs at which they’re executed although, makes all of the distinction. One other uncanny similarity could be demonstrated beneath, the place I took a have a look at the proportion of shares excellent lowered over the past 2 years. As is demonstrated, each firms have been capable of cut back share rely by roughly 5.6%.

This Author, SA information

Along with having comparable efficiency to META on this regard, BABA additionally authorised an upcoming $2.5 billion dividend, or $1.00 per ADS. A sound critique of the dividend coverage is how come the corporate does not simply buyback extra inventory at these ridiculously low costs? I’d are inclined to agree with this sentiment, however I suppose dividends may get pleasure from attracting new traders to the corporate and going in opposition to the narrative that capital simply is not getting returned to shareholders properly.

It is All In regards to the Value

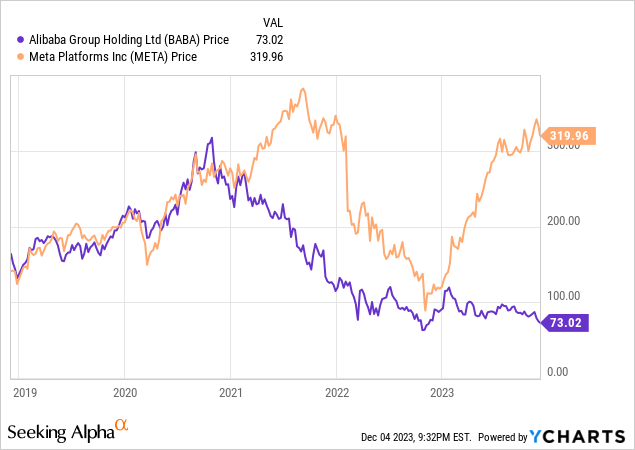

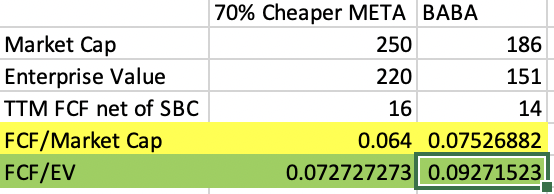

In order a comparability to see how low-cost BABA actually is, I wished to check it to if you happen to had been capable of purchase META immediately 70% cheaper or at round $96 per share, a market cap of round $250 billion and an enterprise worth of about $220 billion. Like shopping for on the trough of final yr however higher, as operations have improved. That is extra simply demonstrated in a chart, so lets have a look:

This author, SA information

As we are able to see primarily based on these information, even when META had been to miraculously drop 70% immediately, BABA nonetheless seems higher on a trailing free money stream degree, with a 9.2% yield when money web of debt is subtracted out of the market cap. The distinction turns into much more stark, whenever you notice the above calculation represents a 2% yield on Meta’s enterprise worth at present market costs.

Dangers/Limitations

Geopolitical Dangers

That is everybody’s favourite to tout when Alibaba is underperforming. Relations between the west and China may decline, leading to unfavorable therapy of overseas traders. I believe that is unlikely, as I consider the US and China are locked in a prisoner’s dilemma. If they do not cooperate, everybody suffers.

Strictness of the Chinese language Authorities

Jack Ma was not careful with his comments about Chinese language regulators, leading to a crackdown on him and his firm. The federal government must be handled with a sure diploma of decorum, and if executives at Alibaba are unable to do that, shareholders could possibly be adversely affected.

Decrease Margins, ROIC, and Development than Meta

These ought to be taken under consideration when valuing the 2 enterprise. Although development has been comparable, BABA’s decrease ROIC may point out a narrower moat. Between 2014 and now, BABA has been capable of develop FCF/share 6x, whereas Meta has grown it 7x.

Conclusion

It is best for the clever investor to recollect at occasions like these that volatility is a chance, not a threat. If you’re investing for the long run in Alibaba, the protracted low share value is definitely helpful, as the corporate will be capable to buyback extra shares and enhance your proportional possession. Additionally it is good to do not forget that occasions of financial stress are a few of the solely occasions the very best firms can be found for cut price costs. This type of alternative solely presents itself each decade or so and I consider now could be a type of occasions.

When in comparison with META, even when META had been buying and selling at trough ranges and performing because it does immediately, BABA could be buying and selling at a big low cost when TTM FCF web of inventory primarily based compensation. Moreover, Alibaba has demonstrated it may be as shareholder pleasant and maybe even extra so than Meta, given its comparable share rely reductions over the past 2 years and the addition of a $2.5 billion dividend. I believe persistence, equanimity and a long run focus are necessities of traders in BABA, however I hope they are going to be rewarded handsomely. I’ve continued so as to add shares of BABA to my portfolio since my last article.

Editor’s Observe: This text was submitted as a part of Searching for Alpha’s Top 2024 Long/Short Pick investment competition, which runs by December 31. With money prizes, this competitors — open to all contributors — is one you do not need to miss. If you’re thinking about turning into a contributor and participating within the competitors, click here to search out out extra and submit your article immediately!

Editor’s Observe: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please concentrate on the dangers related to these shares.