JHVEPhoto

AllianceBernstein Holding LP (AB) is an asset administration firm with a robust historical past of delivering outcomes for its personal shareholders. AB stands out as totally different from its friends in that it’s a partnership, has a big personal wealth enterprise, and has a key strategic accomplice.

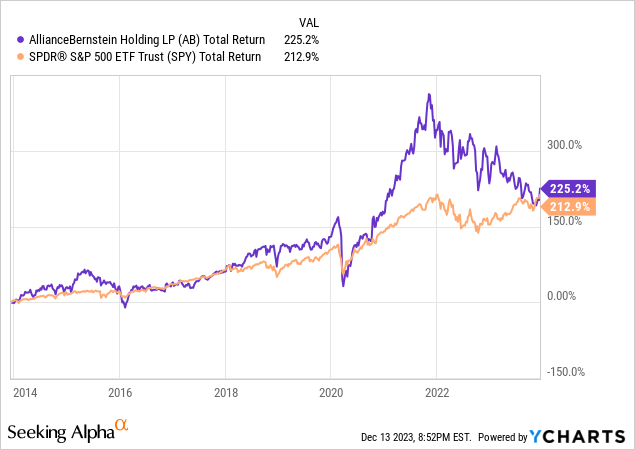

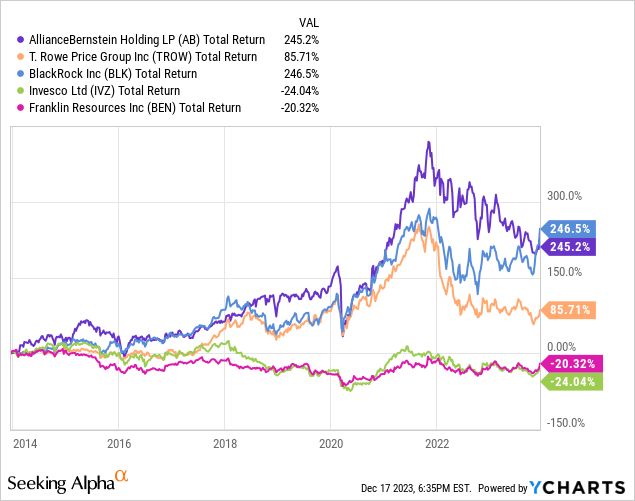

Over the previous 10 years, AB has delivered a complete return of 225% in comparison with a complete return of 213% delivered by the S&P 500. AB has additionally posted robust efficiency relative to most of its friends over the identical time interval.

There are six the explanation why I imagine buyers ought to think about shopping for the inventory at present ranges:

1. Partnership construction offers tax benefits

2. Personal wealth enterprise represents a key a part of the corporate’s enterprise

3. Robust efficiency monitor file offers aggressive benefit vs friends

4. Robust and quickly rising options enterprise

5. Strategic partnership with Equitable Holdings offers key benefits

6. Enticing valuation

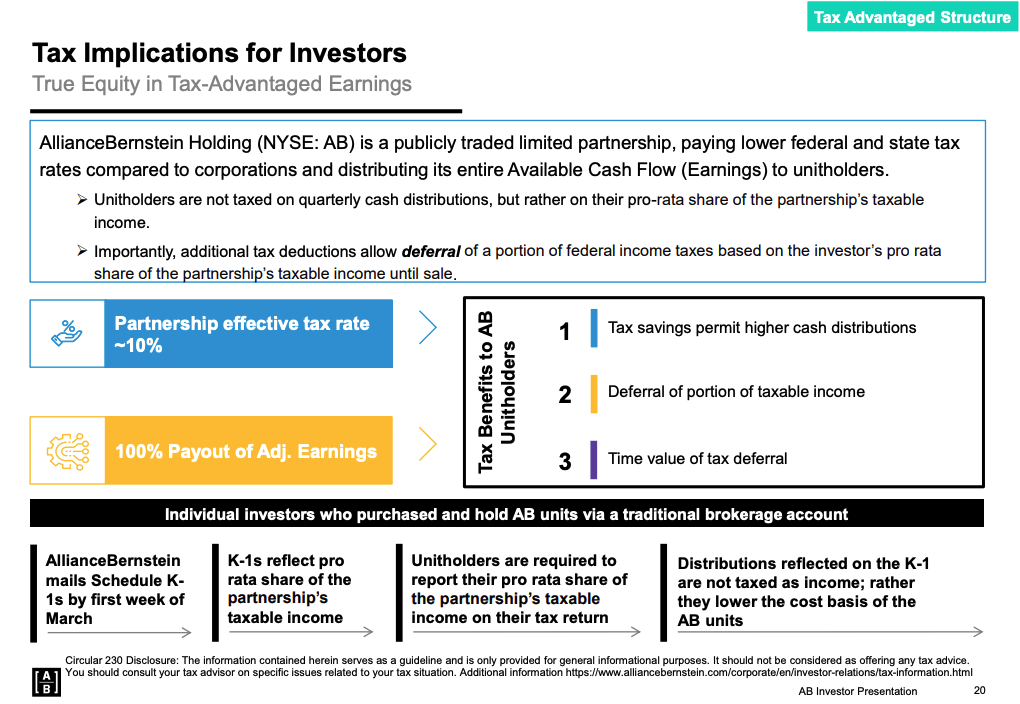

1. Partnership construction offers tax benefits

AB is totally different from its friends in that it’s structured as a partnership. Sure, this implies buyers should cope with the dreaded Ok-1. Nevertheless, the partnership construction offers quite a few key benefits.

Probably the most important tax benefit associated to AB’s partnership construction is that its efficient tax price is way decrease. For FY 2022, AB’s efficient tax price was simply 10.3% in comparison with a 21% U.S. Federal Company Tax price.

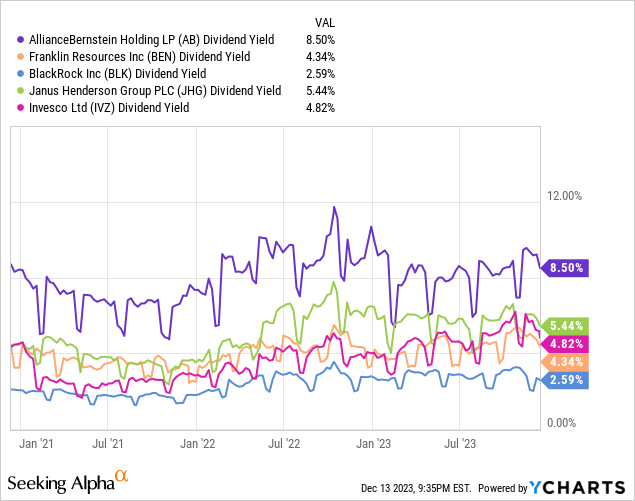

As a partnership, AB is required to payout the overwhelming majority of its earnings annually to shareholders. This leads to AB having a really excessive dividend yield which grows over time with earnings progress. As proven by the chart under, AB nearly at all times provides a a lot better dividend than its friends.

Unitholders are usually not taxed on the total quantity of the distribution and are in a position to defer fee of taxes till sale. This permits buyers to compound their investments on a tax-deferred foundation, which is a key profit for buyers associated to this construction. One other key profit is that if models are held till dying, the premise will usually step up and tax could also be completely prevented. This represents a main tax benefit in comparison with investments held in AB’s friends, that are C companies.

For that reason, AB is a very engaging funding for people in excessive tax brackets who might be able to maintain AB shares till dying.

AB Investor Presentation

2. Personal wealth enterprise represents a key a part of the corporate’s enterprise

AB’s personal wealth enterprise has ~$113 billion in AUM which accounts for 17% of the agency’s whole AUM. Nevertheless, the enterprise accounts for 34% of the corporate’s base charges. This is because of the truth that personal wealth charges are typically larger than funds charged on funding funds. The corporate’s personal wealth enterprise has been a vibrant spot lately and has posted three straight years of natural progress.

The personal wealth enterprise offers a key distribution channel for AB’s merchandise and is a differentiator vs rivals who shouldn’t have a captive wealth administration enterprise. Whereas massive banks comparable to UBS (UBS), Goldman Sachs (GS), J.P. Morgan (JPM), and Morgan Stanley (MS) have their very own wealth administration companies which function a distribution channel for its merchandise, impartial asset managers comparable to Franklin Sources (BEN), Invesco (IVZ), and T. Rowe Value (TROW) have very small or non-existent personal wealth companies. TROW’s personal wealth business has ~$6 billion in belongings whereas BEN and IVZ aren’t within the enterprise.

The personal wealth enterprise is usually relationship-driven and tends to be extra proof against the threats associated to passive low price choices in comparison with the standard asset administration enterprise. A latest instance of the endurance of the standard advisor-based wealth administration enterprise might be seen in J.P. Morgan’s latest choice to wind down its Robo-Advisor enterprise.

With $113 billion in AUM, AB just isn’t one of many massive gamers within the trade and thus I imagine has important progress potential. For FY 2023, the corporate is on monitor to extend whole advisor headcount by ~5%.

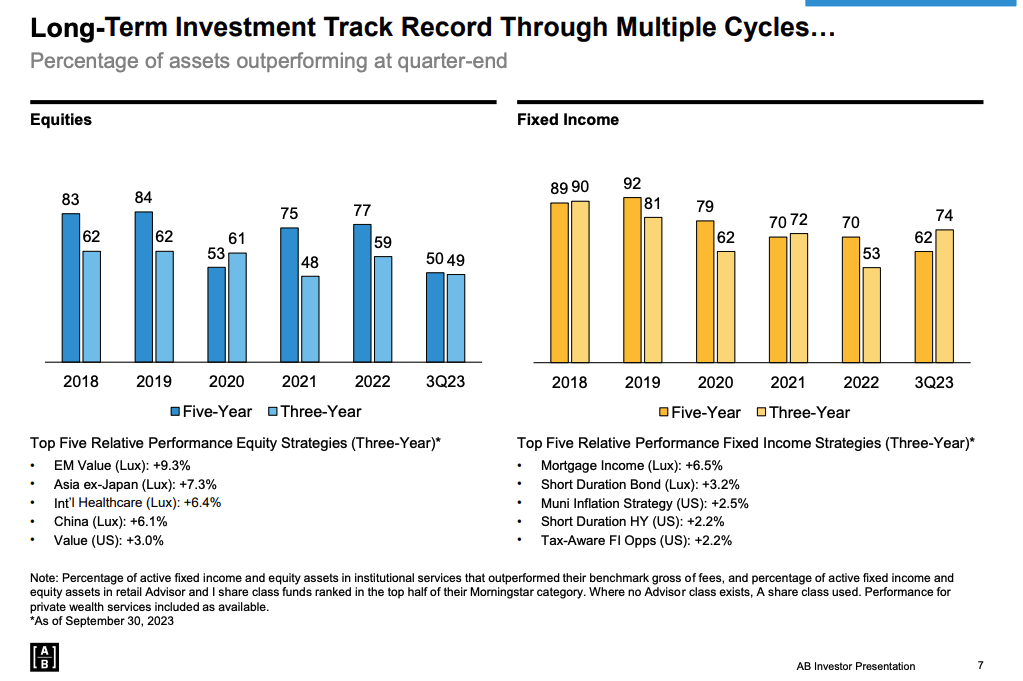

3. Robust efficiency monitor file offers aggressive benefit vs friends

It’s no secret that the overwhelming majority of actively managed funds have didn’t beat their benchmarks over lengthy intervals of time. In line with Morningstar, over the previous 5 years, simply 29.5%, 29.5%, and 30.8% of energetic U.S. Massive Mix, U.S. Massive Worth, and U.S. Massive Development funds have crushed their benchmarks.

AB advantages from a reasonably robust monitor file. That is very true in mounted earnings which accounts for ~39% of the agency’s whole AUM.

The corporate’s robust efficiency monitor file is a vital promoting level with clients and serves as an essential a part of the corporate’s aggressive benefit. Robust efficiency has helped enable AB to publish a 5-year energetic AUM annualized natural progress price of two.1%. Comparably, primarily based on the identical metric, friends have posted a decline of two.4%.

AB Investor Presentation

4. Robust and quickly rising options enterprise

Various and multi-assets options account for $126 billion in AUM accounting for ~19% of the agency’s whole AUM. Complete personal markets AUM is $61 billion which represents ~9% of whole agency AUM. The corporate believes it may possibly develop its personal markets enterprise at a 10-12% CAGR by way of 2027 leading to $90-$100 billion in AUM.

As of FY 2022, personal markets income accounted for 9.2% of asset administration income. AB expects this quantity to extend to at the very least 20% by 2027. I imagine it could possibly be even larger if AB is ready to discover extra engaging M&A targets.

AB considerably expanded its options enterprise with the acquisition of CarVal Buyers in March 2022 which added $14.3 billion in options AUM. I imagine AB may proceed to accumulate smaller gamers and bulk up its options enterprise by way of strategic M&A. Specifically, it could make sense for AB to accumulate a midsized personal fairness agency to enrich its power in personal credit score. One of many key drivers of the CarVal acquisition was the concept AB’s robust distribution platform would enable CarVal to develop belongings extra quickly than would have been doable on a stand-alone foundation. The identical argument would apply to a possible personal fairness deal sooner or later. One latest instance of a standard asset administration agency shopping for its manner into the PE house is Franklin Sources, which acquired Lexington Companions in 2022.

5. Strategic partnership with Equitable Holdings offers key benefits

Equitable Holdings (EQH) is AB’s controlling shareholder with a 61% possession curiosity within the firm. EQH is a monetary providers firm that gives insurance coverage and different monetary providers.

Along with being AB’s majority buyers, EQH can also be the corporate’s largest shopper with $109 billion in everlasting capital. This accounts for ~16% of AB’s whole AUM. EQH additionally provides AB a $900 million lost-cost line of credit score and a further $300 million uncommitted facility.

EQH’s possession curiosity in AB represents a serious a part of its personal worth (~30% of EQH money stream) and thus EQH is extremely incentivized to assist AB develop. EQH has been a seed investor in lots of AB’s options methods and has dedicated greater than $6 billion to seed previous funds.

A latest instance of EQH offering seed capital to launch a brand new product might be seen within the launch of AB’s NAV Lending fund on December 5, 2023. EQH has offered the preliminary anchor funding.

I view AB’s relationship with EQH as a big optimistic as a big proportion of AB’s AUM is successfully captive. This is a bonus that almost all massive friends, apart from PIMCO which has the same relationship with its controlling shareholder Allianz, shouldn’t have. Whereas EQH may transfer its belongings elsewhere, it might have little incentive to take action given its controlling curiosity in AB. Furthermore, AB can also be poised to learn from future AUM progress associated to EQH’s rising funding portfolio going ahead.

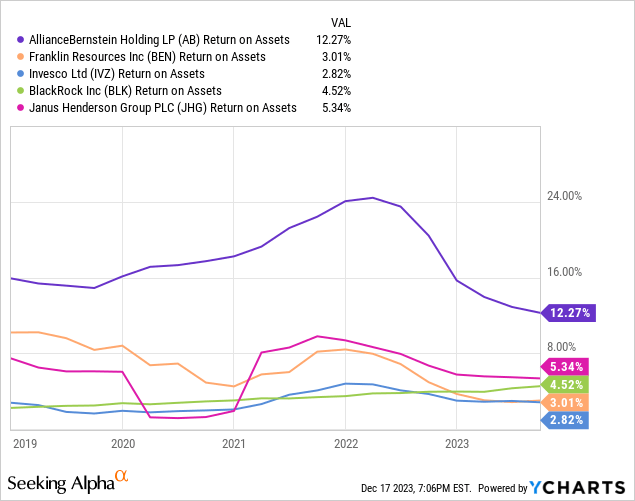

Having EQH as a key strategic accomplice and the related capital base permits AB to function with a decrease degree of belongings in comparison with most friends. Thus, AB is ready to generate the next return on belongings.

6. Enticing valuation

Given AB’s excessive degree of dividends and correlation with earnings progress, I imagine a dividend low cost mannequin represents an inexpensive valuation methodology.

Key assumptions in my evaluation embrace a levered beta of 1.05, an fairness danger premium of 5.5%, FY 2024 dividend of $2.79 per share (that is inline with consensus earnings estimates and AB usually pays out 100% of earnings as a dividend), and a dividend progress price of three.5% into perpetuity. Primarily based on these inputs, I discover that AB must be price $42.9 per share. Whereas AB’s dividend has been considerably risky traditionally as earnings might be risky on account of market strikes, the corporate has grown its dividend at a 5.1% CAGR over the previous 10 years.

Primarily based on the buying and selling degree of the corporate inventory of ~$32.4, the inventory is pricing in perpetual earnings progress of simply 1.4%. I view this as a lot too conservative as it’s nicely under AB’s historic progress price and nicely under annual nominal GDP growth which has averaged 6.2%.

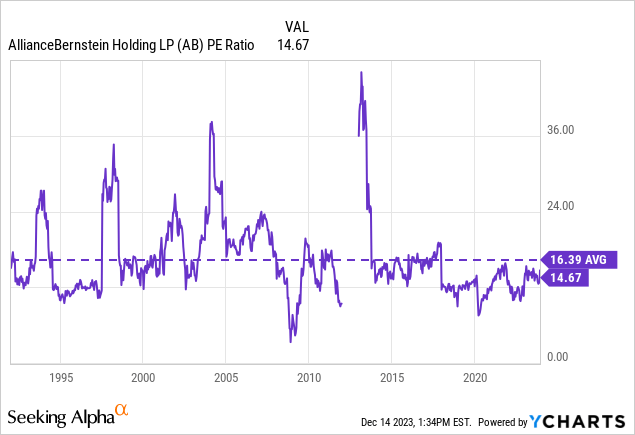

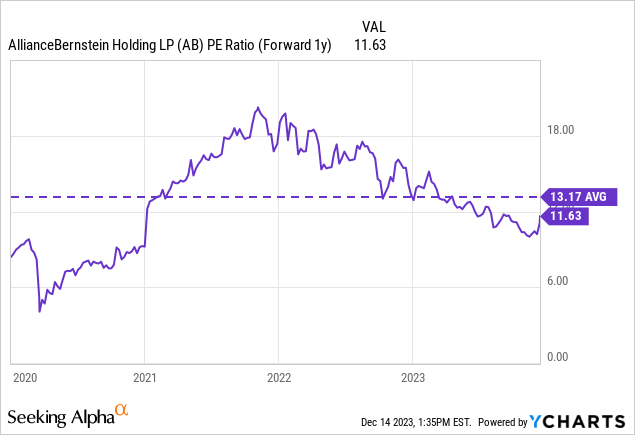

Along with being engaging primarily based on an intrinsic valuation, I additionally discover AB engaging relative to its historic valuation vary. AB trades at 11x consensus FY 2024 EPS. This compares to a historic common P/E ratio of 16.4x and a newer common ahead P/E ratio of 13.2x.

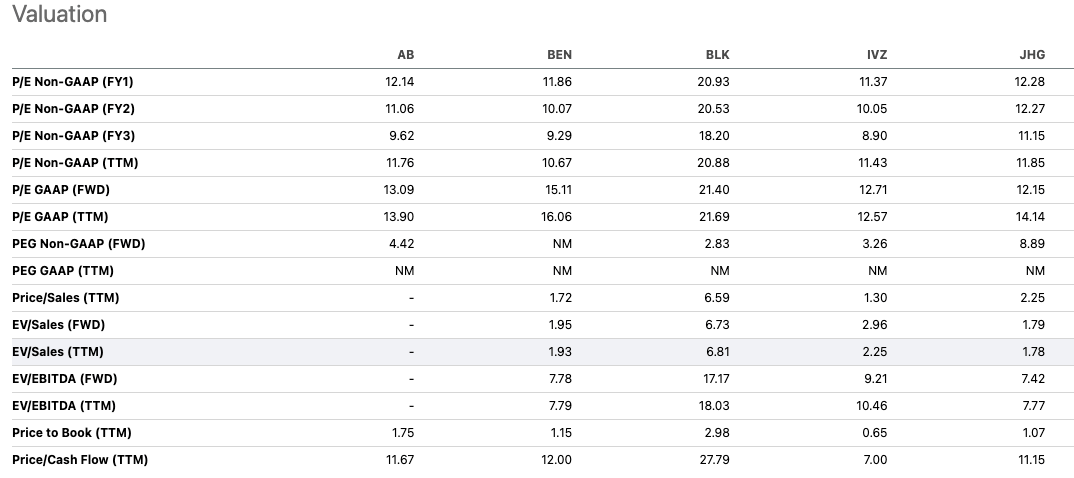

By way of peer valuation, AB trades inline with friends comparable to Franklin Sources, Invesco, Janus Henderson, and others. AB trades at a reduction to BlackRock, however I discover that low cost to be acceptable given BlackRock’s stronger place in passive.

In search of Alpha

Dangers To Contemplate

One key danger to contemplate with AB is the truth that the corporate has been late to embrace ETFs. The corporate has simply $1 billion in ETF belongings and solely launched its ETF platform a 12 months in the past. ETFs have grow to be common for quite a few causes, together with their tax benefits over mutual funds and typical decrease value construction. Early movers BlackRock, Vanguard, and State Avenue are market leaders and maintain a combined ~76% of whole U.S. ETF market share. The subsequent largest U.S. ETF platforms Invesco and Charles Schwab have an estimated 5.6% and 4% market share respectively. Thus, the highest 5 gamers have a complete market share of ~85.6%.

A part of the explanation for that is the advantages on account of scale have made it difficult for different gamers to achieve share. Bigger ETFs have a bigger asset base to unfold mounted prices towards and thus are in a position to keep profitability at very low price ranges. Comparably, smaller ETFs with much less belongings have a a lot smaller asset base to unfold mounted prices throughout. This dynamic makes it tough to new ETF issuers to interrupt into the market in a worthwhile manner until merchandise are extremely differentiated from present ETFs. At the moment, an estimated 33%-50% of ETFs are working at a loss for issuers.

As a late mover in what is a reasonably saturated ETF market, AB faces the danger {that a} secular shift away from mutual funds in direction of ETFs leads to market share losses as buyers go for decrease price ETFs supplied by present merchandise with massive AUM. For instance, think about the not too long ago launched AB US Low Volatility Fairness ETF (LOWV) which was launched in March 2023, fees an expense ratio of 0.48%, and has simply $16 million in belongings. Comparably, the iShares MSCI USA Min Vol Issue ETF (USMV) fees an expense ratio of 0.15% and has belongings of $27 billion. Given LOWV’s small measurement, it is vitally tough for this fund to compete with USMV on value and thus buyers are prone to favor USMV given the price benefit.

Whereas AB was sluggish to enter the ETF house it has grown quickly and is one in all simply 5 energetic ETF sponsors to succeed in $1 billion in belongings throughout the first 12 months of launch. This knowledge is encouraging and means that the agency is having traction with its choices and is providing merchandise which buyers view as differentiated. I count on AB to proceed rising its ETF enterprise however buyers ought to pay shut consideration to its success going ahead given the aggressive benefits loved by entrenched main ETF suppliers.

One other key danger to contemplate is that AB fails to ship higher than common fund efficiency vs friends and benchmarks. A sustained interval of below-average fund efficiency would ship a substantial blow to conventional energetic franchises and will result in outflows.

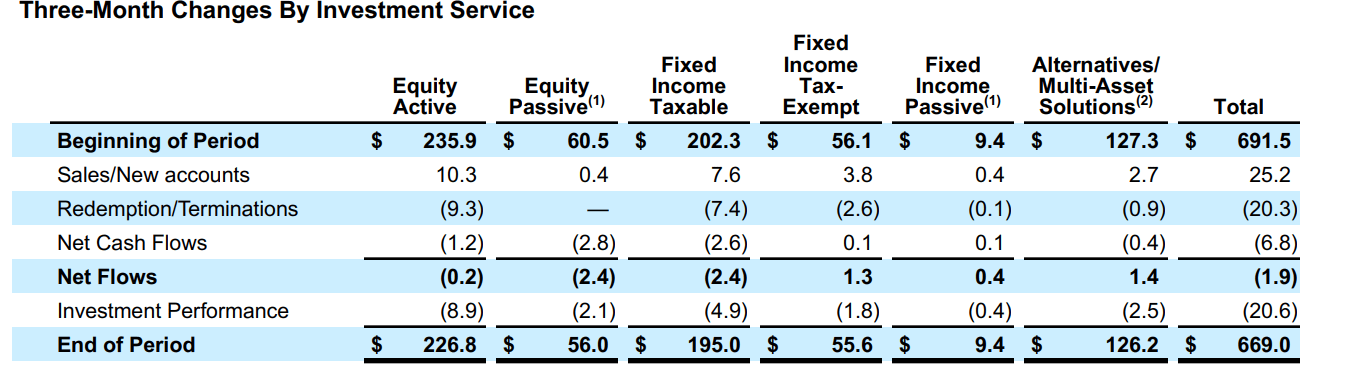

Whereas latest fairness product efficiency has been weaker than historic efficiency it has not considerably impacted fund flows as AB continues to be producing flows that are principally inline with friends. Throughout Q3 2023, AB posted internet outflows of $1.9 billion on an asset base of $691.5 billion. Comparably, Franklin Sources posted long-term internet outflows of $6.9 billion on an asset base of $1.4 trillion whereas BlackRock posted long-term internet out outflows of $13 billion on an asset base of ~$9.1 trillion.

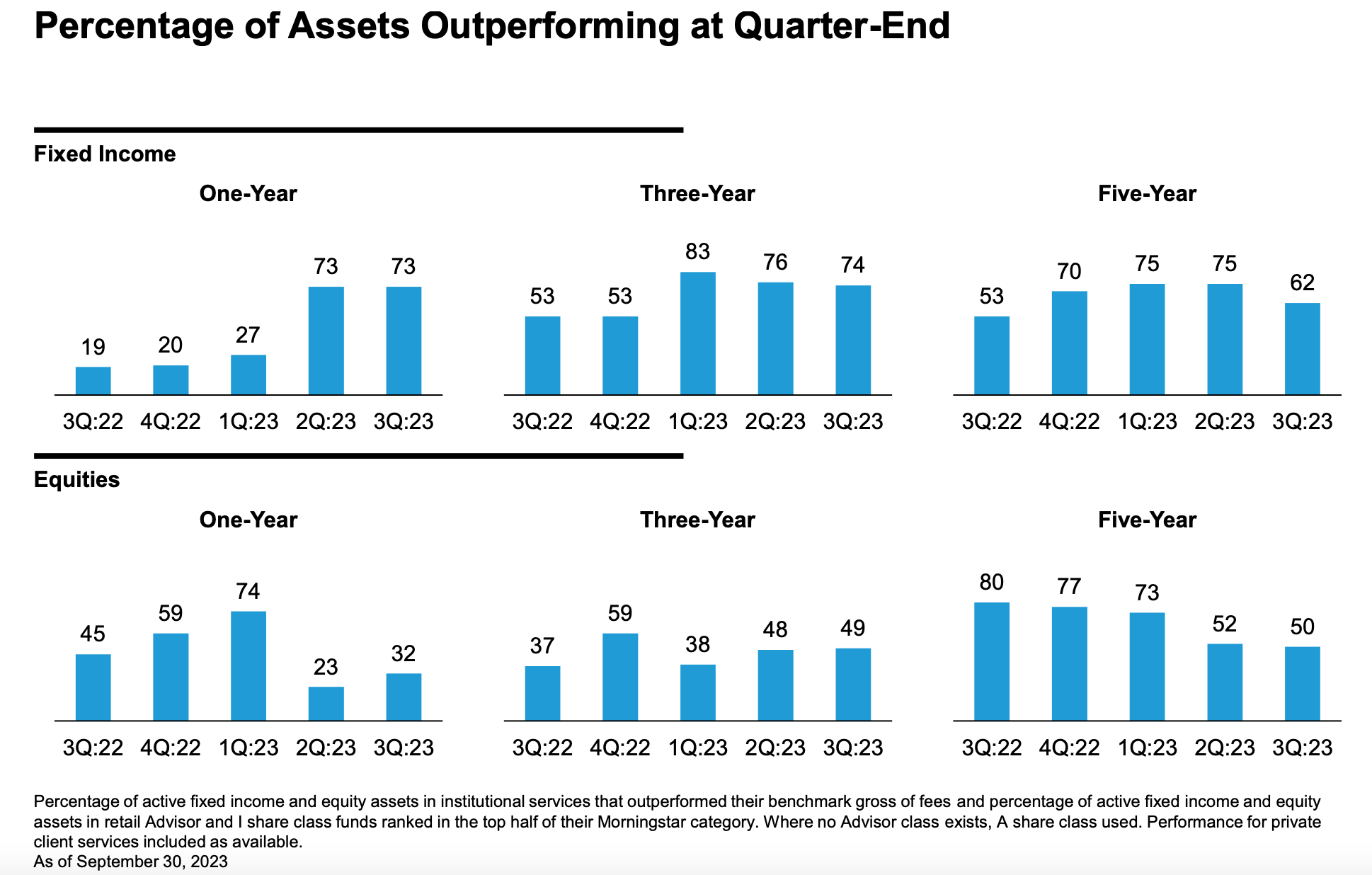

As of Q3 2023, simply 50% of AB’s fairness belongings had been outperforming over the previous 5-year interval. Comparably, this quantity was 80% only a 12 months in the past. One driver of this has been that benchmarks are typically tilted extra in direction of mega cap names whereas AB merchandise are typically extra diversified. For instance, AB Massive Cap Development Fund (APGAX) has ~26% invested in its high 5 holdings. Comparably, the Russell 1000 Development Index has ~35% exposure to its high 5 holdings. Time beyond regulation, I count on the market advance to broader out which ought to assist efficiency.

Latest mounted earnings efficiency has been higher with 62% of belongings outperforming over the previous 5 years in comparison with 52% throughout the identical interval a 12 months in the past. Thus, in combination, I imagine latest efficiency has been moderately robust, however buyers ought to proceed to observe efficiency for indicators of sustained weak spot relative to benchmarks.

AB Investor Presentation AB Q3 2023 Flows Information (AB Q3 Earnings Launch)

Conclusion

AB has a robust historical past of delivering stable outcomes for shareholders. One distinctive attribute of AB is its partnership construction. This construction permits the corporate to save lots of on taxes whereas permitting buyers to learn from tax deferrals.

In sure instances, people might be able to personal AB and pay little or no tax in the event that they by no means promote and the premise steps up upon switch.

AB stands out from friends on account of its robust historic efficiency monitor file, substantial personal wealth enterprise, and strategic partnership with EQH.

The corporate has a quickly rising options enterprise which represents a big progress alternative for the corporate.

I discover AB extremely engaging primarily based on an intrinsic valuation and relative to its personal historic norm.

I’m initiating AB with a purchase score and would think about downgrading the corporate if that valuation had been to grow to be much less engaging.