Cineberg

Following our evaluation on Zurich Insurance Group, we’re again to touch upon Allianz’s fairness story, growing our purchase ranking goal due to the extra upside to cost in (OTCPK:ALIZF, OTCPK:ALIZY). Our Allianz funding was backed by 1) an “attractive and predictable dividend” improvement, 2) a valuation supported by the PIMCO division (a world chief in Asset Administration), and three) a decrease bills ratio coupled with a better reinvestment yield due to rate of interest evolution. Right here on the Lab this yr, we now have already analyzed the corporate’s Q1 (Solid Start) and Q2 outcomes (Solid Numbers And Solvency Strengths). For that reason, we’ll briefly replace our readers on Q3, however extra importantly, we now have determined to replace you with a follow-up be aware with 4 extra help key takeaways.

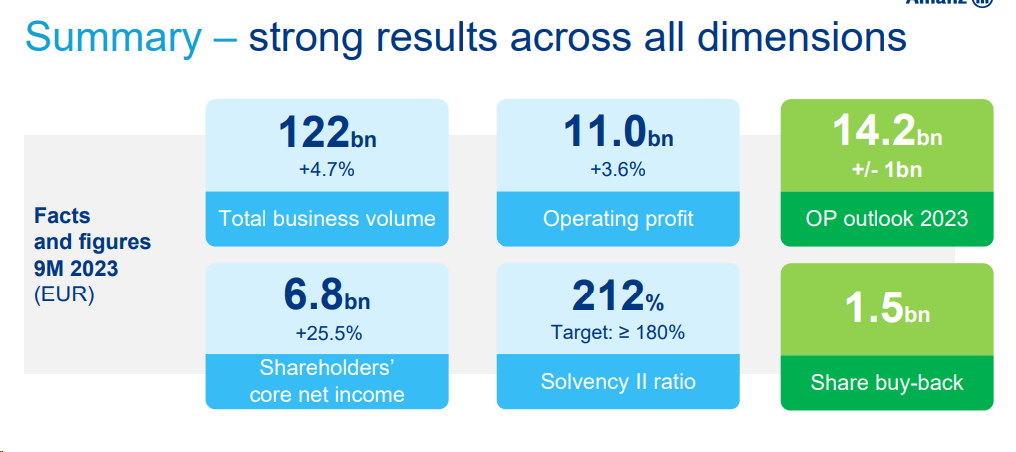

Noteworthy Areas. In Q3, the German insurance coverage participant reported a 29.5% decline in web revenue to €2.02 billion. This was primarily as a consequence of increased claims from pure catastrophes. Regardless of that, Allianz’s numbers beat analysts’ consensus web earnings forecast of €1.99 billion. Working revenue additionally contracted 14.6% to €3.47 billion, with €1.3 billion in reimbursements linked to pure disasters. Allianz described the extent of claims as “exceptionally excessive.” Sadly, Continental Europe has been hit by unprecedented floods and hailstorms over the summer season. P&C profitability declined with a mixed ratio to 96.2% within the quarter from 92.5% in Q3 2022. Regardless of that, Allianz maintained its 2023 goal. In line with our estimates, and contemplating nat cat loss, Allianz’s working revenue was 8% increased than anticipated. We’re impressed by the P&C income development of 11% and the Asset administration move, which reached €10 billion. The Solvency II ratio rose 212% from 208% in Q2 2023.

Allianz Q3 Financials in a Snap plus outlook

Supply: Allianz Q3 results presentation

Why are we supportive?

On the Inside Allianz Collection presentation, the corporate showcased three items with upside in every space. As well as, we additionally reported Allianz’s M&A optionality and our constructive view of the IFRS regulatory framework.

- (IFRS upside) Beginning with the latter, as we already reported in Zurich with an evaluation referred to as IFRS 17 Might Provide An Upside, we additionally consider that Allianz is ready to profit from the IFRS 17 low cost profit. As a reminder, IFRS 17 implies that the claims included within the mixed ratio calculation needs to be decreased accordingly. Intimately, claims’ current worth needs to be decrease than their final value. This increased uncertainty creates a reduction being deducted from the insurance coverage funding earnings. Right here on the Lab, we consider this new regulatory framework has been detrimental for non-life insurers’ valuation. Regardless of that, the mixed ratio can be reported after discounting future claims, and Allianz is growing its insurance coverage product portfolio pricing. For that reason, the corporate confirmed its 93% mixed ratio for 2023 and 92% as a mid-term outlook. The corporate lately offered an replace throughout the Inside Allianz Collection presentation and decreased its mixed ratio by 2.6 foundation factors regardless of a better low cost sooner or later (Fig 1). Nonetheless, this didn’t translate into working earnings falling. As a substitute, we would have an extra upside: if rates of interest begin to decelerate, the claims low cost needs to be decreased, offering a revenue uplift for Allianz;

- (Greater pricing actions) Publish Q3 and Allianz’s newest presentation, we estimate a mean enhance of 10% in insurance coverage pricing. That is additionally supported by the IFRS 17 view, the place pricing actions at the moment are accelerating to offset discounting dilution;

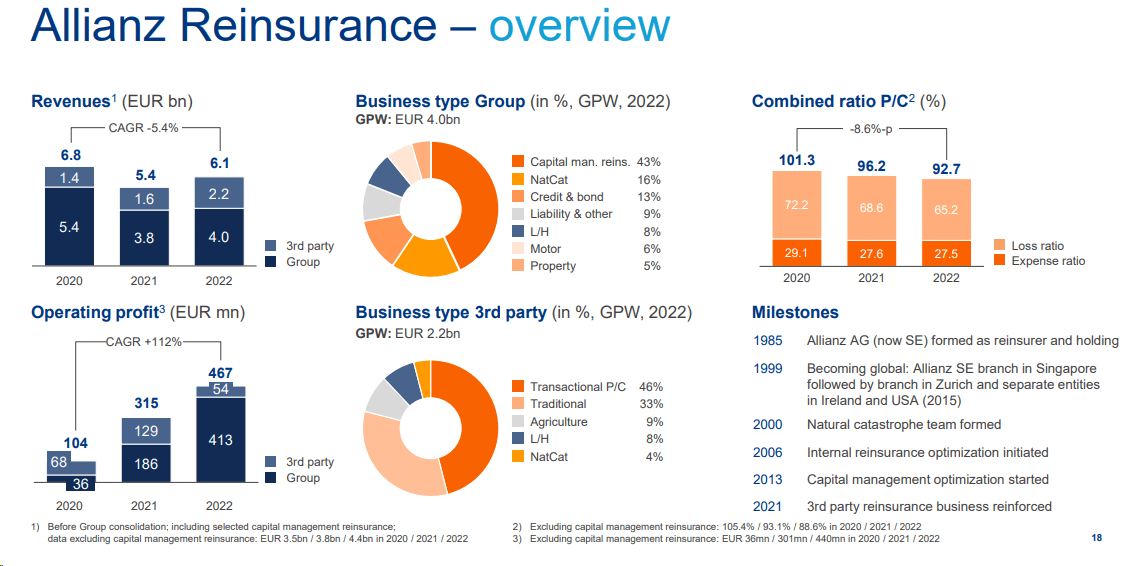

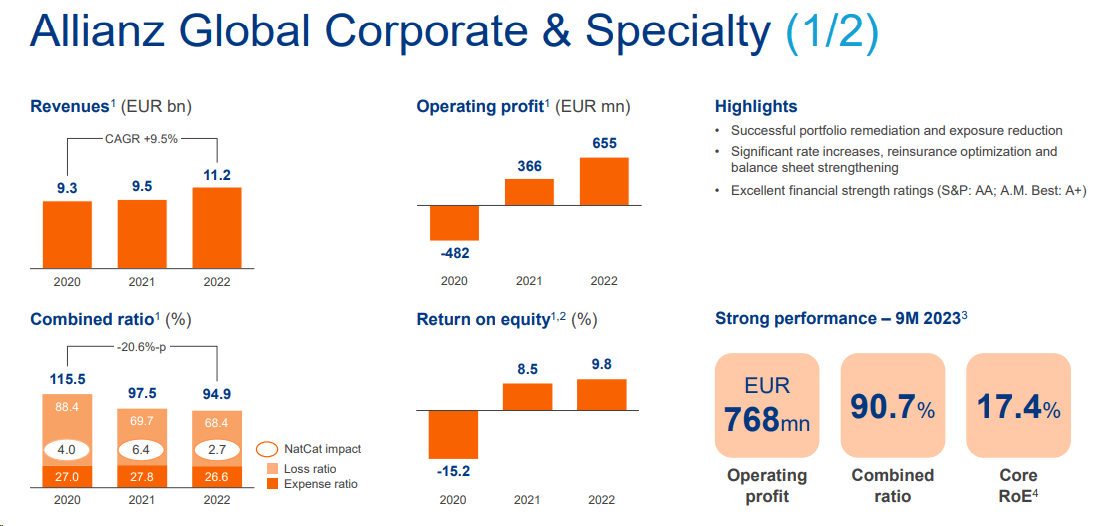

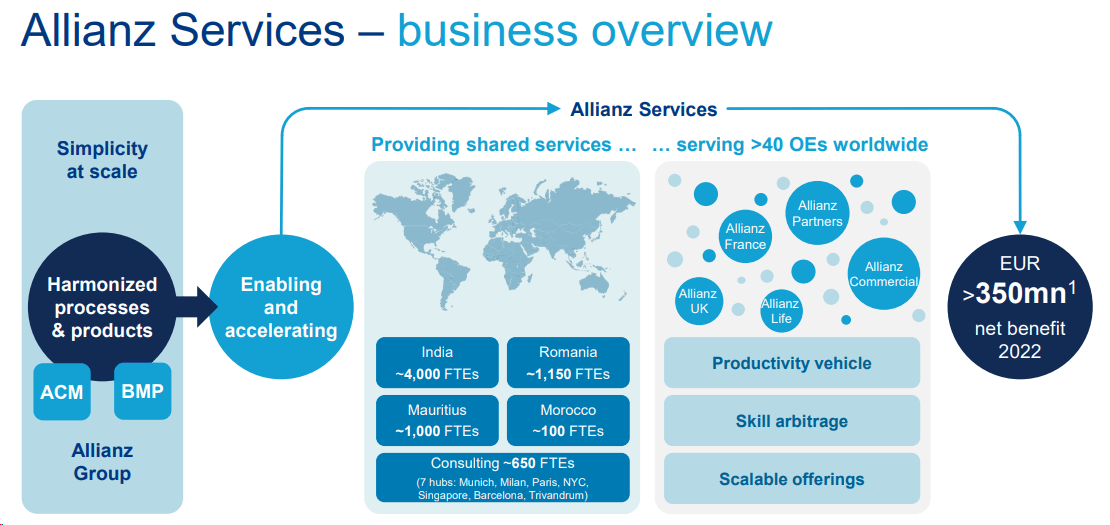

- (Greater financial savings and synergies) Trying on the three items with potential upside, we be aware 1) Allianz RE improvement (Fig 2), 2) the formation of Allianz Industrial referred to as AGCS (Fig 3), and three) Allianz Providers evolution (Fig 4). The previous division’s working revenue is ready to rise by 50%. The division goals to optimize Allianz’s capital allocation by inside reinsurance. Regardless of that, Allianz Re additionally used exterior third-party reinsurance, and the corporate is elevating its working revenue by €150 million. AGCS additionally goals to extend its core working revenue from €100 million due to increased volumes. The latter, the Allianz Providers phase, throughout the Allianz Collection presentation, raised its effectivity financial savings to over 350 million in 2025. In our estimates, we now forecast €150 million increased financial savings to achieve €500 million by 2025. Due to this fact, we elevated the phase working revenue accordingly;

- (M&A optionality) In This autumn, Allianz agreed to acquire Tua Assicurazioni from Assicurazioni Generali. This inorganic acquisition was carried out for a complete worth of €280 million. Tua Assicurazioni’s premium portfolio is 60% primarily based on automotive coverage and is distributed by a community of roughly 500 brokers. Topic to regulatory approvals anticipated in early 2024. Allianz’s market share within the P&C insurance coverage market is anticipated to develop by about 1% to 11%, consolidating its place because the third participant in Italy.

Allianz discounting upside

Supply: Allianz Inside Series presentation – Fig 1

Allianz RE third-party upside

Fig 2

AGCS replace

Fig 3

Allianz Service financial savings

Fig 4

Conclusion and Valuation

This yr, our core working revenue is ready at €14.6 billion, and we’re barely under the consensus expectation of €14.7 billion. Given the corporate’s supportive earnings uplift, we determined to extend our 2024 outlook with an working revenue of roughly €15.5 billion, and our 2024 EPS estimates reached €28.5. Allianz is buying and selling at 8.8x 2024 P/E (8.3x 2025 P/E) under its >10x five-year historic common. Due to this fact, primarily based on our unchanged 10x P/E a number of, we elevated our purchase ranking goal from €235 to €285 per share ($30.5 in ADR). Draw back dangers embody credit standing downgrade, costly M&A offers, resulting in elevated earnings volatility and better leverage, and decrease than anticipated Solvency II evolution. Extra dangers are included in our Q2 update.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please pay attention to the dangers related to these shares.