FG Commerce Latin/E+ through Getty Photographs

Elevator Pitch

Alternative Inns Worldwide, Inc. (NYSE:CHH) shares are assigned a Purchase funding ranking. Earlier, I wrote about CHH’s 2024 monetary outlook in my previous update printed on October 10, 2023.

This text highlights Alternative Inns’ latest optimistic developments that traders ought to take into account. Firstly, CHH is now not pursuing an acquisition of Wyndham Inns & Resorts (WH). Secondly, Alternative Inns has not too long ago introduced an enlargement of the corporate’s share buyback plan. Thirdly, the corporate is rising its midscale prolonged keep model Everhome Suites’ footprint in new markets.

I retain a Purchase ranking for Alternative Inns in view of those favorable developments.

Overhang Relating To Proposed M&A Deal Has Been Eliminated

CHH beforehand printed a press release on October 17, 2023 revealing that it has made “a proposal to acquire all the outstanding shares of Wyndham Hotels & Resorts.” Alternative Inns’ shares fell by -6.8% on the day of the M&A deal announcement and subsequently dropped to a 52-week trough of $108.91 throughout intra-day buying and selling on March 5, 2024. It’s worthy of word that Wyndham Inns’ board of administrators didn’t support the deal.

However Alternative Inns’ inventory worth finally rose by +4.7% on the finish of the March 5, 2024 buying and selling day. On that day, Searching for Alpha Information reported that CHH “will either decide to extend or terminate the merger offer” after contemplating “the level of participation in the tender offer” for WH’s shares.

A subsequent March 11, 2024 Searching for Alpha Information article highlighted that CHH had “ended its hostile attempt for an $8 billion takeover of Wyndham Hotels.” The promote facet analysts from Jefferies (JEF) and Baird raised their respective investment ratings for Alternative Inns on the identical day in response to the termination of the corporate’s deliberate acquisition. Notably, Alternative Inns’ share worth rose by +5.6% to shut at $127.77 on March 11, or +17.3% above its 52-week low.

Beforehand, the market was prone to have been involved that CHH might be embroiled in a long-drawn battle for the management of WH on the expense of different capital allocation alternate options and natural progress plans. This supplies an evidence for Alternative Inns’ prior share worth weak point which led the inventory to drop to a 52-week trough in early March.

As such, Alternative Inns’ determination to maneuver away from this deliberate takeover of WH is a optimistic growth.

Latest Buyback Plan Enlargement Announcement Is A Constructive

On March 11, 2024, Alternative Inns announced “an increase in the number of shares authorized under its share repurchase program” by “five million shares” to “6.8 million shares.”

Final 12 months, CHH spent $366 million shopping for again 2.9 million of the corporate’s shares, which left it with 1.8 million shares remaining from its share buyback authorization on the finish of 2023. Subsequently, it was extremely possible that Alternative Inns would have returned a lot much less capital to its shareholders through share repurchases this 12 months, assuming that it continued with the WH deal and put aside capital for this potential transaction.

Now, it’s clear that the corporate is focusing its consideration on different value-accretive capital allocation alternatives, because it strikes on from the potential Wyndham Inns M&A deal.

Alternative Inns has guided for a +5.6% progress in its normalized earnings per share or EPS from $6.11 for FY 2023 to $6.45 (mid-point of steering) in FY 2024. In its This fall 2023 earnings press release, CHH famous that its FY 2024 steering doesn’t incorporate the consequences of “additional repurchases of company stock” amongst different components. In different phrases, there’s potential upside pertaining to Alternative Inns’ precise backside line efficiency this 12 months, if it repurchases extra of its personal shares underneath the expanded share buyback plan.

Progress Potential Related With New Model Attracts Consideration

In early March this 12 months, Alternative Inns issued a media release disclosing “the opening of Everhome Suites in Newnan, Georgia, marking the midscale extended stay brand’s debut on the East Coast.”

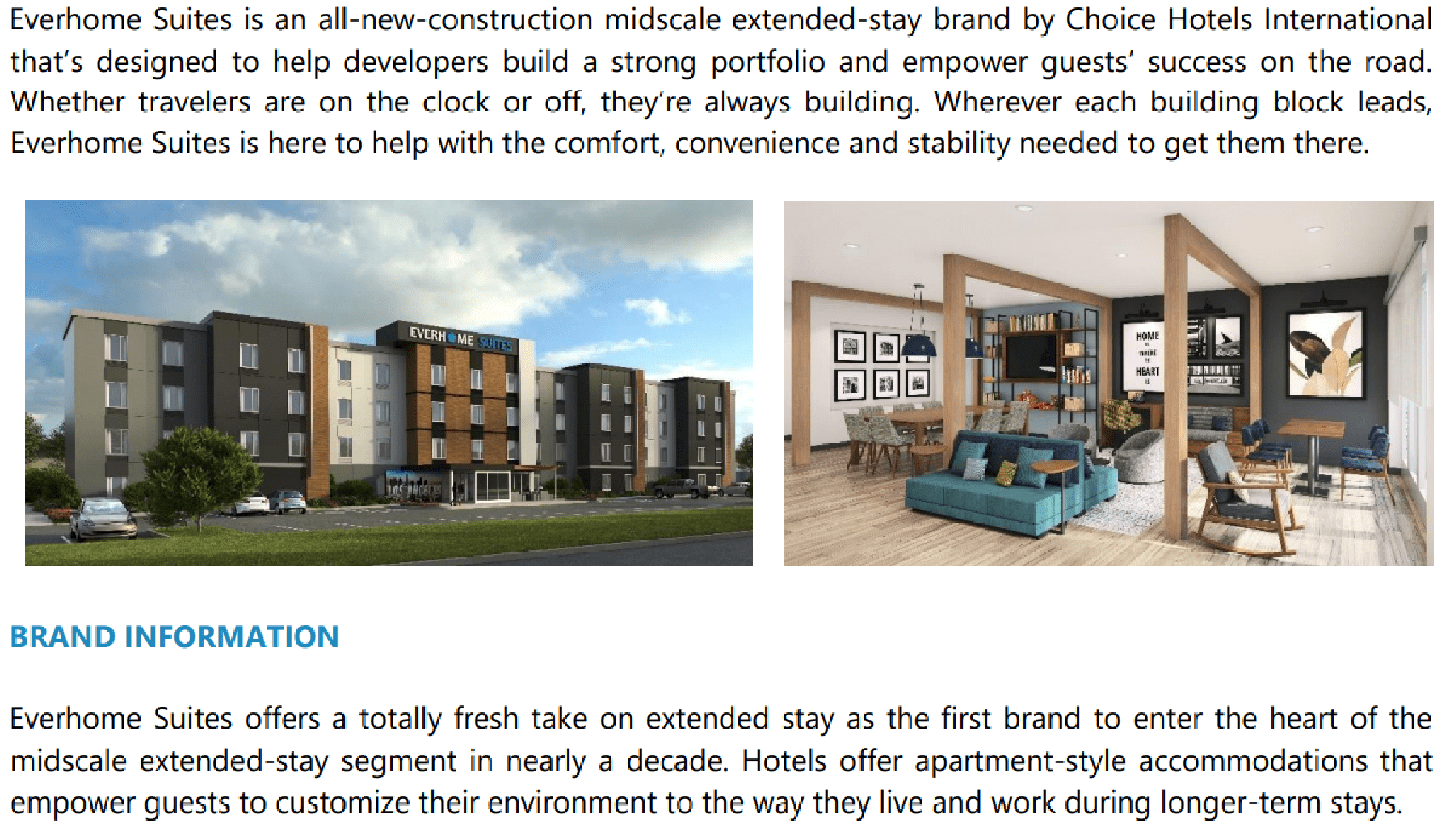

An Overview Of The Everhome Suites Model

Everhome Suites Model Factsheet

Everhome Suites is the most recent model that the corporate has added to its portfolio initially of 2022, and this model has big progress potential.

In 2023, the full variety of items in CHH’s portfolio elevated by +1.8%, whereas the prolonged keep phase’s variety of items grew by a a lot better +14.9% within the earlier 12 months. Shifting ahead, Alternative Inns anticipates that its prolonged keep phase can obtain a +15% unit CAGR for the FY 2024-2028 time-frame as per its administration commentary on the Q4 2023 earnings briefing.

Individually, hospitality firm Accor (OTCPK:ACRFF) (OTCPK:ACCYY) famous in its January 31, 2024 article posted on its web site that “as remote and hybrid work models come into their own, more and more professional travelers” are “looking to stay at their destination for longer.” On this end-January write-up, Accor additionally cited analysis agency Future Market Insights’ forecasts that the worldwide prolonged keep hospitality market phase can develop at a fairly sturdy CAGR on the teenagers proportion stage for the 2023-2033 time interval. This supplies help for CHH’s progress goal referring to its prolonged keep phase.

I’m of the opinion that Alternative Inns is prone to allocate extra capital to natural progress alternatives reminiscent of increasing the attain of its midscale prolonged keep model, Everhome Suites, in a bigger variety of markets going ahead. With the Wyndham Inns deal out of the best way, CHH can dedicate extra effort and time to realizing its full natural progress potential.

Last Ideas

CHH’s present consensus subsequent twelve months’ normalized EV/EBITDA a number of of 13.8 instances is 14% decrease than its historic imply EV/EBITDA ratio of 16.0 time (supply: S&P Capital IQ) for the previous decade. I believe that Alternative Inns can commerce at the next EV/EBITDA metric nearer to and even exceeding its historic common in time to come back, when the market pays extra consideration to its favorable developments.