bymuratdeniz/E+ through Getty Pictures

Pemvidutide’s Kilos and Issues: Altimmune’s Balancing Act

Since December, Altimmune’s (NASDAQ:ALT) inventory has practically tripled since revealing obesity data (MOMENTUM) in late November for his or her GLP-1/glucagon agonist, pemvidutide (subcutaneous weekly). Altimmune just isn’t the primary to review GLP-1/glucagon agonism. A number of medicine are at present in improvement, together with Merck’s (MRK) efinopegdutide, Eli Lilly’s (LLY) LY3437943, and Boehringer’s BI 456906, all of that are weekly subcutaneous injections in Section 2 improvement. Different GLP-1/glucagon agonists have been discontinued prior to now on account of gastrointestinal misery. The important thing seems to be an appropriate steadiness of GLP-1 and glucagon agonism. Needless to say GLP-1 alone creates gastrointestinal issues, and glucagon stimulation exacerbates the issue.

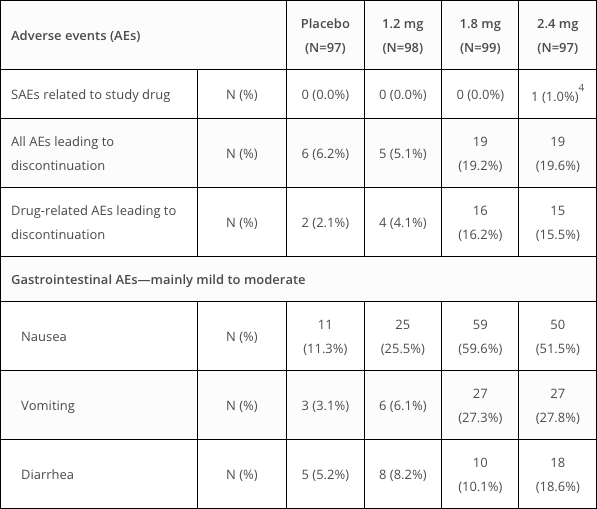

In Altimmune’s Section 2 examine, weight reduction was dose-dependent with pemvidutide, displaying -10.3%, -11.2%, and -15.6% reductions at 1.2 mg, 1.8 mg, and a pair of.4 mg doses, respectively, in comparison with -2.2% with placebo after 48 weeks. Over 80% of topics on the very best dose achieved greater than 5% weight reduction, and enhancements had been additionally seen in ldl cholesterol and triglyceride ranges. Nonetheless, adversarial occasions led to excessive discontinuation charges, particularly at larger doses (19.2% and 19.6% for 1.8 mg and a pair of.4 mg doses, respectively), with gastrointestinal points being the most typical. Drug-related AEs resulting in discontinuation had been notably larger within the therapy arms in comparison with placebo.

Altimmune

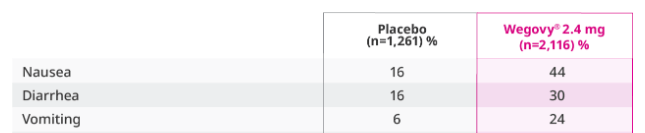

The variety of discontinuations is hanging when in comparison with Novo’s (NVO) GLP-1 agonist, Wegovy, which noticed a discontinuation rate (associated to an adversarial response) of 6.8%.

When adjusting for placebo, pemvidutide’s nausea (48.3% for 1.8 mg) and vomiting (24.7%) AEs are noticeably larger than Wegovy’s (28% and 18%, respectively).

Novo

This disparity seemingly explains the noticed distinction in discontinuation charges. I might not suppose that pemvidutide’s theoretically negligible weight discount benefits over medicine like Wegovy offset any tolerability difficulties.

Altimmune

The corporate is more likely to go ahead with the 1.8 mg dose as dose titration within the 2.4 mg cohort (described within the picture above) did not have a lot impression on adversarial occasions and discontinuations. I’ve seen some posters on social media cite the dearth of dose titration for the 1.8 mg dose as a possible differentiator relative to different weight problems medicine. I do not discover this to be a compelling differentiator contemplating the theoretical prices is a rise in unwanted side effects (which is the reasoning for titration to start with). Now, if the drug was exceptionally well-tolerated (e.g., low drop-out charges on account of adversarial occasions), the absence of titration could be a differentiator. Nonetheless, this doesn’t look like the case for now.

In evaluating Altimmune’s efficacy information to that of a peer, Boehringer’s BI 456906 information look superior at a look. Of the 2 teams, 67% of BI 456906 patients achieved body weight loss of 15% or more, whereas 51.8% of pemvidutide sufferers achieved the identical. Conversely, 24% of BI 456906 sufferers discontinued therapy due to an adversarial occasion; the corporate said that “most treatment discontinuations due to adverse events occurred during the rapid dose-escalation phase and may potentially be mitigated with more gradual dose escalation.”

Monetary Well being

Altimmune’s balance sheet showcases $140.8 million in belongings, with notable liabilities like Accounts Payable ($3 million) and Accrued Bills ($8.8 million), yielding a robust present ratio of 12.9. Regardless of a $59.3 million money burn over 9 months, their 21-month runway signifies manageable short-term liquidity. Nonetheless, with a reasonable threat of needing extra funds inside a yr, Altimmune’s speedy monetary well being is secure, however future sustainability hinges on decreasing bills or securing extra capital.

Market Sentiment

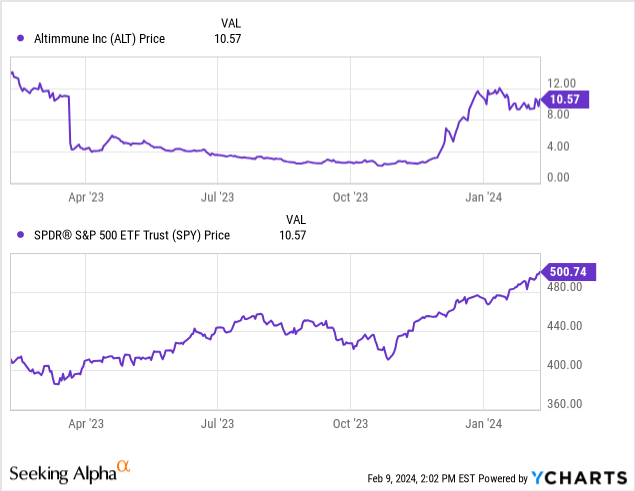

In line with In search of Alpha information, the corporate has a market capitalization of $520.63 million, suggesting a mid-cap entity with particular market area of interest volatility. Its inventory momentum has been distinctive, with a +258.89% improve over 3 months, considerably outperforming the SPY within the brief time period, regardless of a -30.04% decline over one yr.

Short curiosity stands at 21.14%, representing a excessive stage of market skepticism or speculative curiosity within the inventory’s future value actions. Institutional ownership exhibits combined sentiment, with 948,469 new positions and 1,787,438 sold-out positions. Notable holders embrace Blackrock, Nuveen Asset Administration, and Vanguard, indicating a stage of institutional confidence regardless of the general difficult outlook. Insider trades reveal internet promote exercise over the previous three months, with 22,133 shares bought, contrasting with a internet purchase of 12,209 shares over the previous twelve months. Contemplating these elements, the corporate’s market sentiment will be certified as “fragile.”

Is ALT Inventory a Purchase, Promote, or Maintain?

Key takeaways:

- A number of GLP-1/glucagon agonists are underneath improvement.

- It is going to be important for GLP-1/glucagon agonists to have some form of security, efficacy, or comfort benefit (with out a detrimental impact) over GLP-1s as a result of, if a number of of them are permitted, they should compete with GLP-1 drugs that may already be well-established amongst prescribers and payers. This benefit just isn’t but clear.

- Weight reduction medicine like semaglutide and tirzepatide are additionally permitted in diabetes on account of their capacity to decrease hemoglobin A1c. Weight problems and diabetes are sometimes linked collectively. This would cut back the weight problems market (by roughly 30%) for medicine like pemvidutide which have but to show efficacy in diabetes.

- Furthermore, GLP-1/glucagon agonists might also need to compete with different GLP-1/glucagon agonists.

- Altimmune’s GLP-1/glucagon agonist, pemvidutide, does not seem to have a differentiated profile relative to different GLP-1/glucagon agonists.

Contemplating Altimmune’s promising but precarious place with pemvidutide, the corporate confronts a posh path towards industrial success. Whereas the inventory’s substantial rally displays optimism, the underlying efficacy towards weight problems should be weighed towards important competitors and security considerations. Pemvidutide’s journey to turn out to be the main GLP-1/glucagon agonist amongst many contenders is fraught with challenges, not least of which embrace standing out in a crowded area the place it should not solely surpass its direct rivals but additionally show compelling benefits over the established and dominant GLP-1 agonists.

Given these dynamics, the advice to take care of a “hold” on Altimmune’s inventory is underscored by strategic warning. Though I’m pessimistic about Altimmune’s long-term medical and market prospects, it is troublesome to be too pessimistic with its market capitalization of simply $500 million. Given ALT’s erratic value conduct prior to now, it could not shock me to see the rally keep on.

Traders are suggested to undertake a vigilant strategy, mitigating dangers whereas intently monitoring the evolving panorama of medical outcomes and market shifts. This nuanced stance acknowledges the potential of Altimmune’s pipeline but additionally acknowledges the hurdles to attaining standout industrial success in a aggressive and rigorous market. Balancing optimism with prudence permits traders to navigate the uncertainties forward, leveraging alternatives whereas making ready for the complexities inherent within the biopharmaceutical sector’s development.