Boarding1Now

American Airways (NASDAQ:AAL) has been a trailblazer within the skies, however its new iteration presents a distinctly completely different really feel. Beforehand, airways aggressively battled for market share in what was usually a extremely aggressive trade. Profitability within the airline sector was seen as the results of a strategic monetary warfare involving among the largest names moderately than a given. Nonetheless, the pandemic essentially altered the panorama for airways. Up to now, buyers would eagerly purchase shares, attracted by progressive dividends and repurchase plans set forth by the management groups. Now, revered trade gamers like American Airways are adopting a extra balanced method, weighing shareholder rewards in opposition to the necessity to keep a powerful stability sheet and place the corporate for future success. As shareholders, we at all times concentrate on the return on funding over the deliberate period of our inventory possession. Strengthening an organization’s stability sheet and accountable management may not at all times be instantly rewarded by buyers, however at these ranges, there may be a lot to understand about American Airways.

The corporate reported an adjusted pre-tax revenue of $362 million, exceeding the higher restrict of its personal EPS steering vary.

This achievement isn’t solely a numerical victory but additionally a testomony to the group’s relentless pursuit of excellence. They’ve targeted on key areas similar to reliability, profitability, accountability, and strengthening the stability sheet.

Financially, the corporate is prospering. A report third-quarter income of $13.5 billion was pushed by robust demand and a profitable journey rewards program. The airline is seeing regular home demand and strong worldwide progress, particularly within the Atlantic, Caribbean, and Central American markets.

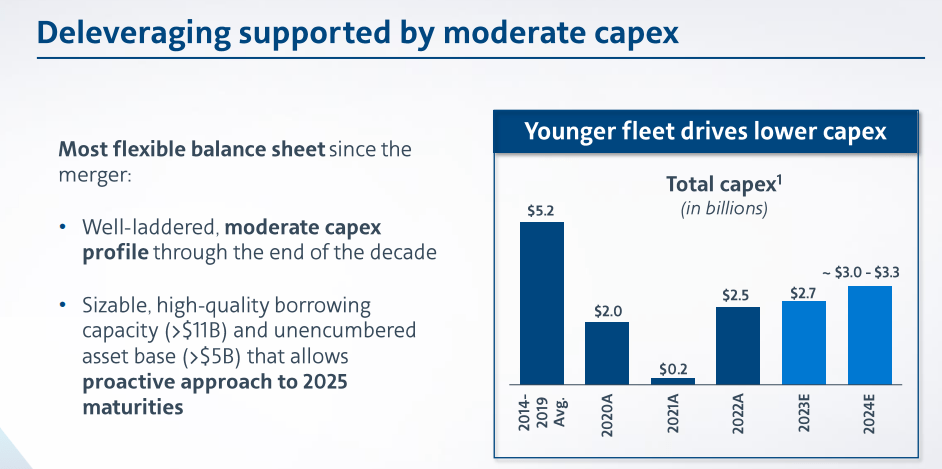

Financially, the airline navigated the trade’s challenges with strategic and targeted administration, reporting a third-quarter web revenue of $263 million. The corporate’s aggressive method to debt discount, which targets a discount of complete debt by $15 billion by the top of 2025, demonstrates a transparent dedication to monetary stability and long-term success.

The projected debt discount will largely be pushed by decrease anticipated CAPEX spending, owing to American Airways’ comparatively younger fleet.

American Airways

Just lately, it seems that the management group at American Airways has been diligently engaged on strengthening the corporate’s stability sheet. This effort is aimed toward making certain extra steady monetary outlays within the coming years. Traders may keep in mind how, through the 2020 pandemic, many main airways, together with American, have been unprepared for the disaster. They’d targeted closely on rewarding shareholders by way of inventory repurchases and dividends, leading to insufficient money reserves. Because the trade confronted sudden and important challenges, these airways lacked the mandatory stability sheet flexibility to face up to the shock, resulting in plummeting inventory values.

In a notable strategic shift, American Airways is now prioritizing the long-term well being of the corporate. This method contrasts with that of its opponents, who proceed to concentrate on aggressive growth and the promotion of premium providers and seats to drive worth. This distinction in technique may clarify why American Airways’ inventory has not lately proven robust efficiency. Nonetheless, it additionally means that the airline could be extra resilient within the face of potential downturns, similar to a recession. This built-in resilience positions American Airways probably forward of its friends by way of preparedness for each a downturn and the following restoration.

Whereas this technique could lack the quick enchantment of short-term sensational beneficial properties that buyers usually search in cyclical and client discretionary sectors, it shouldn’t be underestimated. Compared to industries like bitcoin mining or massive tech, which may supply speedy returns, American Airways’ method could seem much less thrilling. Nonetheless, this resilience may very well be a vital issue within the firm’s long-term capital beneficial properties potential.

As buyers concentrate on capital beneficial properties, it is vital to think about whether or not American Airways, with its present technique, will finally ship these beneficial properties. This consideration raises the query: are there higher alternatives on the market, particularly when contemplating sectors recognized for fast returns? Whereas American Airways’ technique could lack the quick pleasure of speedy progress sectors, its method to resilience and long-term stability may show advantageous within the broader funding panorama.

Pilot Replace and Latest Occasions

The airline’s enhancements transcend the stability sheet, as seen in its finalized contract with the Allied Pilots Affiliation, which improves compensation and high quality of life for its pilots. This transfer underscores American’s precedence – its individuals.

Operationally, American Airways is in prime gear, striving in the direction of new agreements for flight attendants and brokers. The corporate’s operational effectivity, buyer focus, and free money circulation era are all a part of a rigorously crafted technique to make sure stability and progress.

Wanting Ahead

The outlook for the fourth quarter stays constructive, with regular enhancements in enterprise journey and robust worldwide demand. The airline’s capability and income administration methods are set to adapt to the altering market dynamics, making certain continued progress and profitability.

The Journey Rewards program has been a game-changer for American Airways, with important progress in co-brand bank card acquisitions and enrollments within the Benefit program. Roughly 80% of bookings now come instantly by way of the airline’s channels, up 11 factors from the earlier yr, indicating a profitable shift to extra environment friendly distribution channels.

American Airways stays targeted on leveraging its Community and Journey Rewards program. The corporate’s fleet, the youngest and most effective amongst U.S. Community carriers, is a strategic asset. Their initiatives to drive incremental worth, coupled with restricted close to and medium-term capital expenditure necessities, are anticipated to keep up a wholesome money circulation for reinvestment within the enterprise.

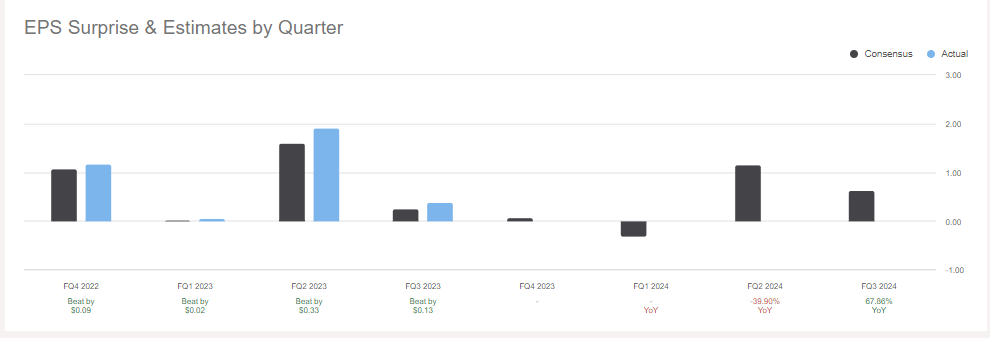

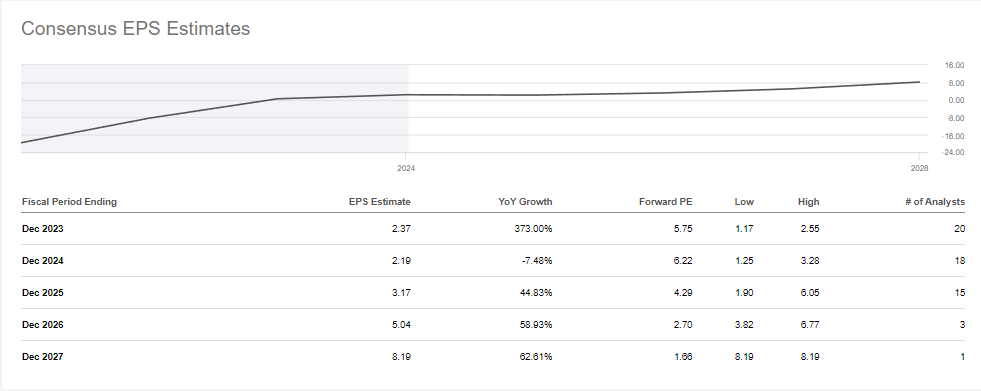

The corporate has been doing a fantastic job at assembly or beating EPS estimates, however as instructed with the debt discount technique talked about earlier, EPS estimates going ahead are removed from thrilling.

Searching for Alpha

In truth, it’s going to seemingly be a while earlier than buyers can anticipate important progress, which is probably going why the inventory has stalled a bit. We will see from the analyst estimates beneath that significant progress will seemingly return through the calendar yr 2025, which means that if issues go nicely, calendar yr 2024 could become an incredible shopping for alternative for a long-term maintain.

Searching for Alpha

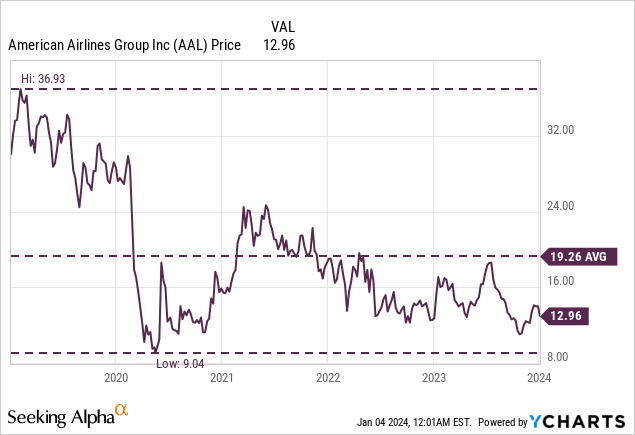

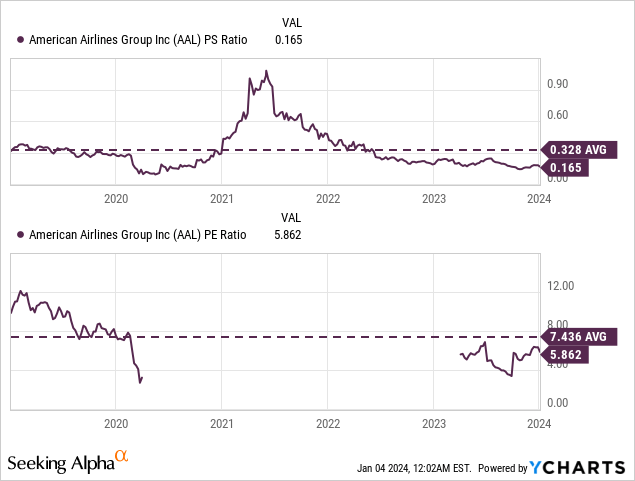

With respect to valuation, we’re actually at enticing ranges, and once more, there are good causes for that.

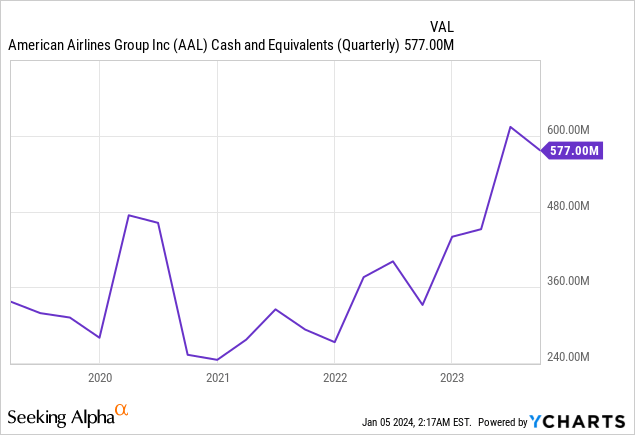

The worrying a part of that is that we’ve got been at enticing valuations for a while now, and the inventory appears to be getting cheaper. However we’re additionally seeing the consequences of the accountable administration practices by the management group. The money balances have been bettering, and as proven above, so too have debt ranges. Although the bettering money stability is probably going no less than partially attributable to the notes offered final November.

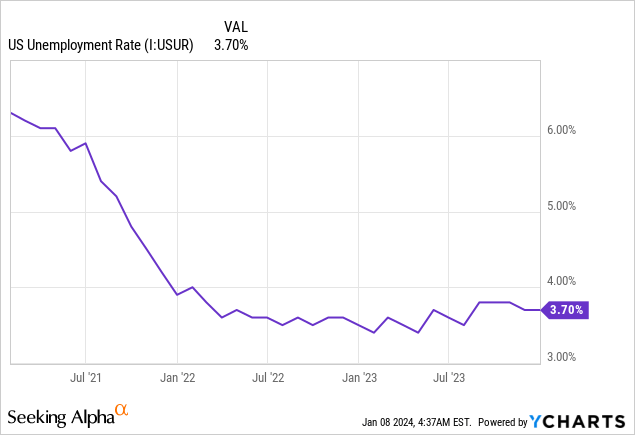

Navigating the debt overhang will seemingly take a while. I might say the top of the calendar yr 2025 can be a very good time for buyers to focus on noticeable appreciation. Within the meantime, this firm is bettering, however the inventory will seemingly take some lumps. I am engaged on constructing with the place of those ranges, however it’s not my highest precedence. That is due to the recession threat. Thus far, there have been only a few indicators that the US will likely be going into a significant recession. Enterprise journey has been robust, and to be trustworthy, the financial state of affairs appears considerably good, with low unemployment and the shortage of any actual monetary disaster.

Nobody is aware of for certain if or when issues may shift, however there’s a feeling of uncertainty available in the market, and because of this, I am shopping for up shares slowly moderately than unexpectedly and preserving an affordable allocation as I redirect funds briefly from know-how.

The Takeaway

American Airways has launched into a transformative journey that goes past mere monetary restructuring. Its latest settlement with the Allied Pilots Affiliation, bettering pilot compensation and high quality of life, displays a deep-seated dedication to its workforce. Furthermore, the airline’s operational enhancements and negotiations with flight attendants and brokers illustrate a holistic method to organizational excellence. American Airways isn’t just recalibrating its stability sheet; it’s reshaping its company tradition to prioritize individuals, operational effectivity, and buyer satisfaction. This method bodes nicely for the airline’s long-term resilience and progress prospects.

Wanting forward, American Airways appears well-positioned to navigate the evolving dynamics of the airline trade. The corporate’s constructive outlook for the fourth quarter, buoyed by strong enterprise journey and worldwide demand, signifies a gentle trajectory towards progress and profitability. The success of its Journey Rewards program and its strategic concentrate on leveraging its community and fleet efficiencies additional reinforce this optimism. Nonetheless, the trail to important progress may take time, with the calendar yr 2025 earmarked as a possible turning level. Till then, buyers may witness a interval of consolidation, with the inventory value reflecting the cautious however strategic steps taken by the corporate. In essence, American Airways presents an image of an organization steadily fortifying itself for the long run, making it an intriguing consideration for long-term buyers who worth stability and incremental progress over speedy however probably unstable beneficial properties. As a long-term-oriented investor, I’m tremendous with this, and I’m constructing a place that I plan to carry for a while. I charge American Airways as a purchase.