sorn340/iStock through Getty Photos

Americold Realty Belief, Inc. (NYSE:COLD) is a distinguished world participant within the chilly storage business, offering temperature-controlled storage and value-added providers. This REIT primarily acquires, develops, and leases temperature-controlled warehouses which are designed for the storage of temperature-sensitive gadgets, together with prescription drugs and meals merchandise.

Although I’m intrigued by the prospects right here, because the title says, COLD shares are pretty valued. As I’m reluctant to spend money on a REIT that’s not undervalued, I imagine that buyers ought to wait in the event that they discover consolation in a margin of security as I do. On high of that, the dividend yield is just too low for me and I think that it might be not excessive sufficient for a lot of buyers within the present setting. Regardless, I needed to dive into the elements that make Americold’s enterprise promising in case a reduction is ever provided by the market. I will additionally get into the specifics of valuation that can assist you perceive the place I am coming from. Let’s take issues from the beginning.

Portfolio

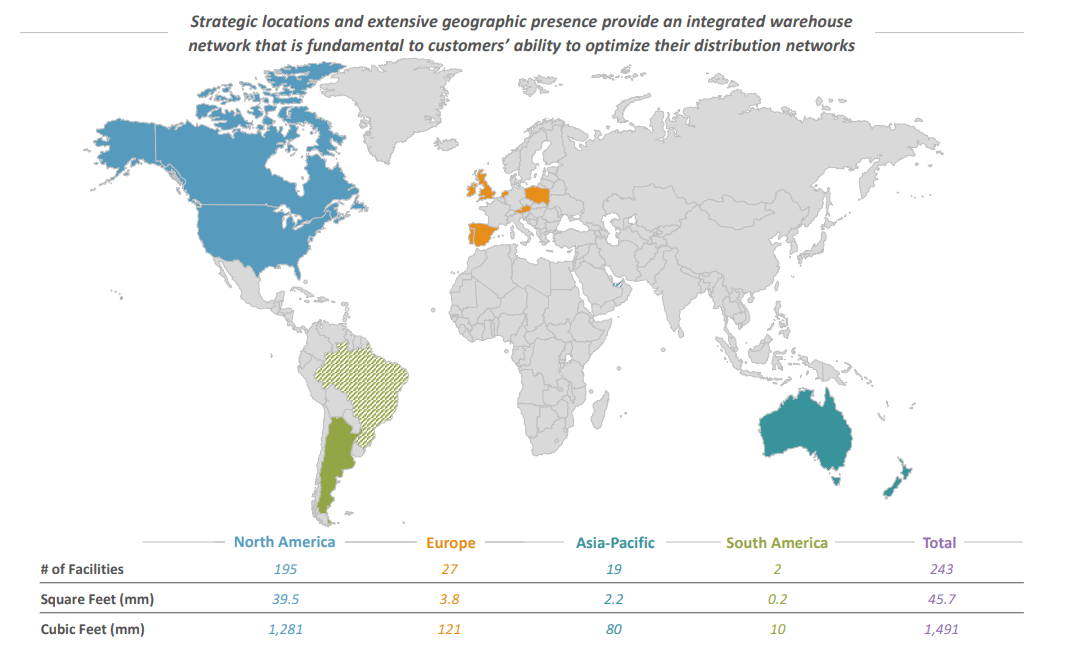

This self-managed REIT manages a worldwide portfolio of 243 warehouses, totaling a quantity of roughly 1.5 billion cubic toes. The portfolio consists of 195 warehouses in North America, 27 in Europe, 19 in Asia-Pacific, and a pair of in South America.

Clearly, if one have been to hunt publicity to a chilly storage supplier, Americold’s portfolio appears exceptionally diversified from a geographical standpoint:

Investor Presentation

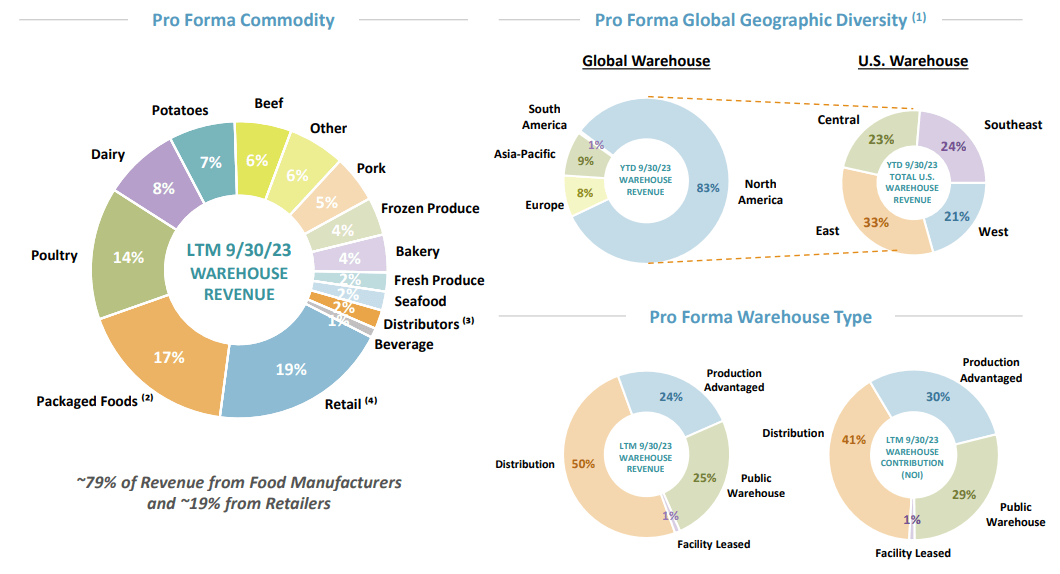

However diversification can also be current in the kind of purchasers the REIT serves; round 80% of its income comes from meals producers and nearly 20% comes from retailers. On the identical time, it is additional diversified in the case of the warehouse kind:

Investor Presentation

Whereas I discover that its 25 largest clients accounting for 48% of its buyer base can appear dangerous, they’ve been with the corporate for a mean of about 36 years. Furthermore, 15 of them are funding grade.

Efficiency

To start with, Americold’s financial occupancy for its same-property portfolio reached 84% in the course of the three months ended on September 30, 2023, marking a development of 345 foundation factors in comparison with the corresponding interval within the earlier 12 months. Additionally, its common bodily occupancy stood at 75.8%. For a similar-store property, these are very low charges so there’s undoubtedly a big margin for enchancment right here.

In relation to working efficiency, the REIT has skilled respectable income development in a comparatively quick time period, however its working earnings and FFO efficiency did not comply with:

Nevertheless, more moderen outcomes are excellent when in comparison with the latest previous. Under, you’re looking on the change between the newest figures annualized and their corresponding common annual ones as reported within the REIT’s final 3 fiscal years:

| Rental Income Progress | 21.79% |

| Similar-Property Money NOI Progress | 24.17% |

| AFFO Progress | 21.93% |

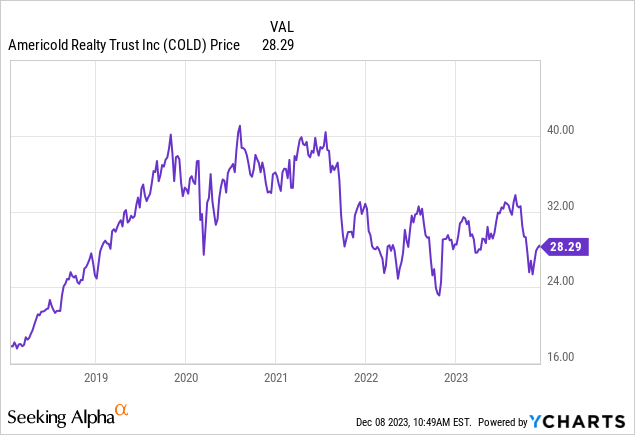

Nevertheless, the elemental development hasn’t but been mirrored within the value efficiency, with COLD’s value nonetheless oscillating up and down after realizing a assured enhance up till 2020:

Leverage

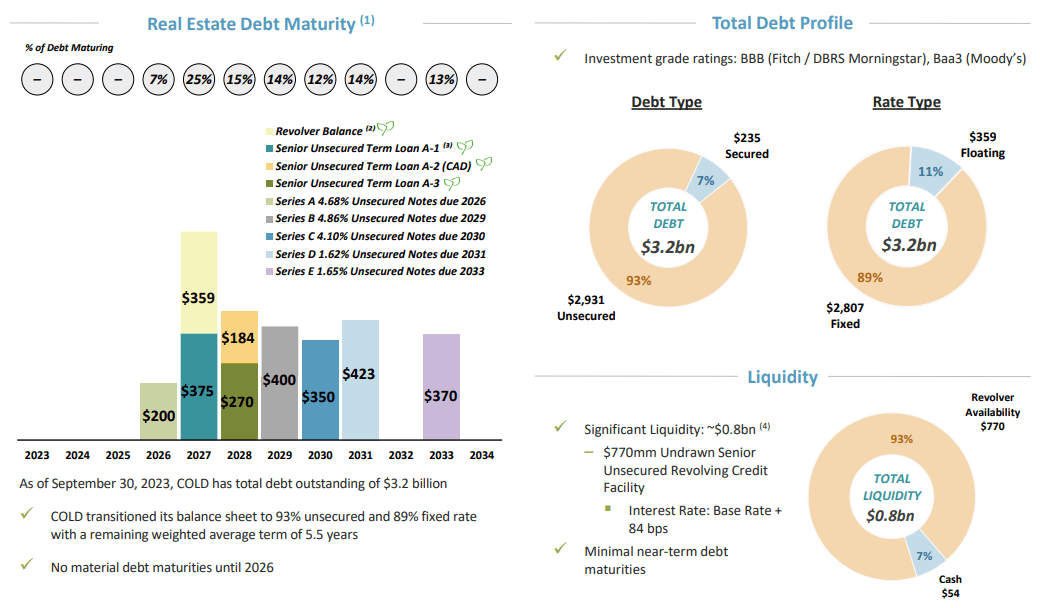

As for the usage of leverage, Americold has decreased it from round 50% in 2019 to 36.44% as we speak. Its debt-to-EBITDA ratio sits at 8.27 instances, which I see as acceptable. Nevertheless, its TTM curiosity protection at 0.22x is regarding and one thing to keep watch over:

Fortuitously, its revolving credit score facility, unsecured notes, and time period loans value a weighted common rate of interest of 4.02%.

On high of that, there are not any vital maturities till 2026, solely 11% of its debt has floating charges, and simply 7% of it’s secured, offering loads of flexibility.

Investor Presentation

Prospects

It is good to know that the market Americold is in has vital development potential. The chilly chain logistics market was valued at $280.23 billion in 2022 and is anticipated to develop at a CAGR of 15.5% till 2031 when it is anticipated to succeed in ~$1 trillion.

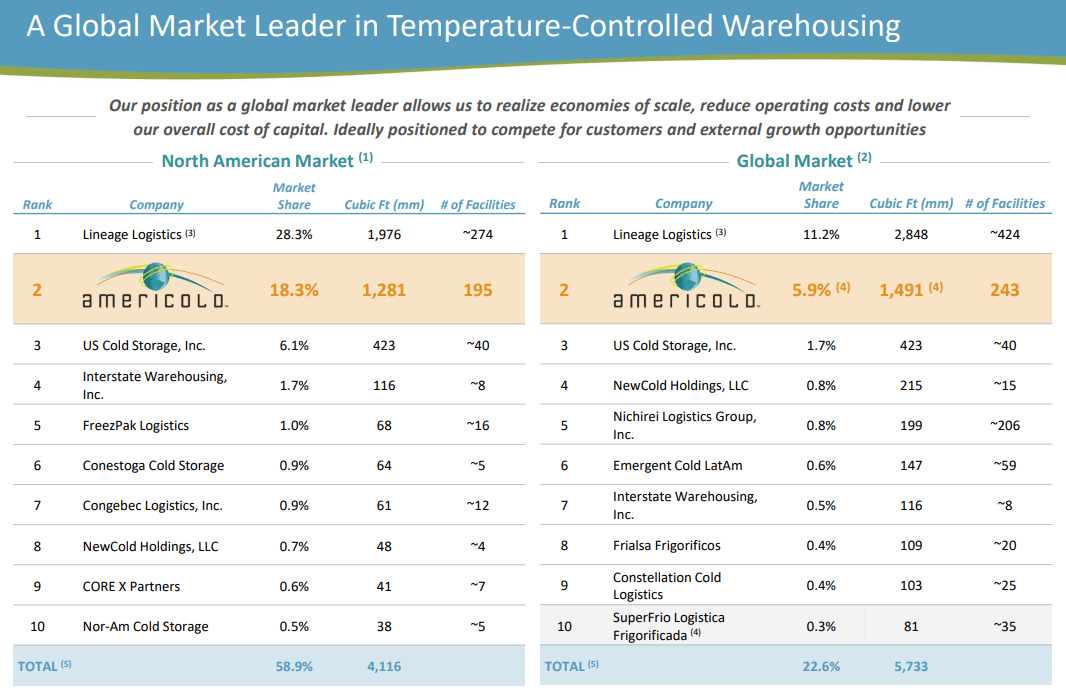

COLD looks as if the suitable automobile to place oneself for such development since, based mostly on market share, it is ranked second place in each the North American market and globally in the case of temperature-controlled warehousing:

Investor Presentation

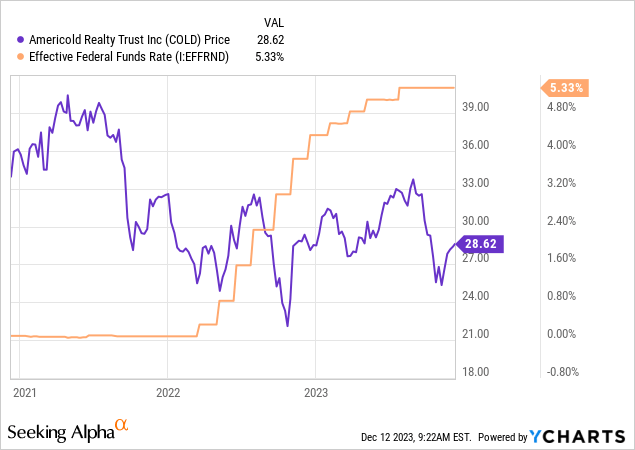

That is the long run although. Within the close to time period, I imagine that any alleged value stress that will have been utilized by the aggressive Fed hikes within the latest previous on COLD may very well be alleviated. We now have already seen the probably response by the market when the speed was held regular just lately:

And it is very likely that charges will stay unchanged within the subsequent assembly on December 13, doubtlessly offering additional assist for the latest COLD shares’ repricing.

Administration

Earlier than we go into valuation, I would wish to briefly notice some issues you need to be conscious of associated to administration:

-

Americold’s CEO, George F. Chappelle Jr. was paid $7,689,546 in 2022 (additionally accounting for inventory awards); the very best compensation throughout the firm

-

As of the tip of the fiscal 12 months 2022, 0.24% of COLD inventory was held by executives

-

There have been no latest COLD share acquisitions by insiders; simply gross sales and inventory awards

In my opinion, a compensation scheme that permits for such doubtlessly excessive figures, very low insider fairness, and simply share tendencies most definitely enabled by inventory awards, are usually not apparent crimson flags. However they fail to color an important image of administration high quality.

Many extra elements must be thought of when assessing that high quality, however I feel that shortly observing some key shareholder-interest alignment indicators just like the above may give an investor the power to see in the event that they want to be “in business” with an organization. You be the decide.

Dividend & Valuation

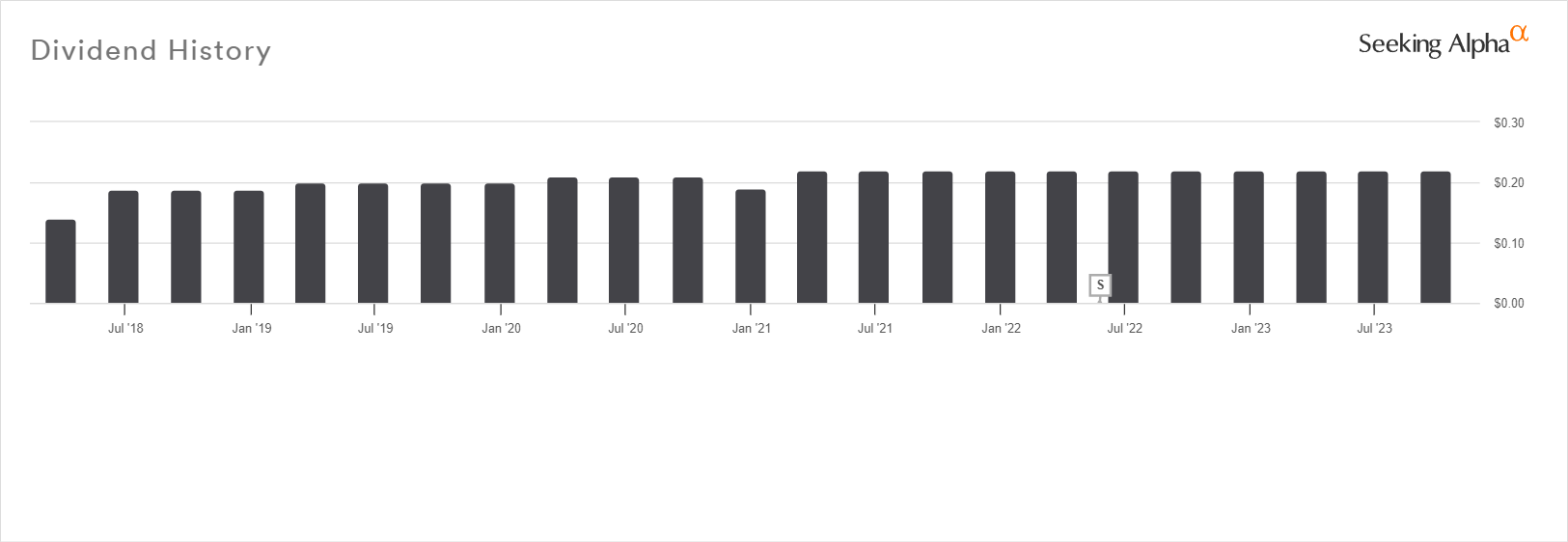

The REIT pays a quarterly dividend of $0.22 per share, which ends up in a ahead yield of three.07%. For what’s price, the dividend is comparatively secure. Though we do not have a protracted observe document of funds or a particular development pattern, the payout ratio based mostly on the final AFFO determine annualized is 70.75%.

In search of Alpha

Clearly, when different much less dangerous choices provide a considerably increased yield just like the 1-Yr Treasury Invoice bond, one wants to contemplate what else COLD could have to supply right here.

If it is a additional enhance within the value of COLD you search, I imagine that there are higher alternatives elsewhere. The shares are at the moment buying and selling at an implied cap price of 6.17%, which suggests a roughly honest valuation.

Even when we assume that potential consumers of cold-storage warehouses at the moment do not demand a cap price premium regarding the broader industrial actual property market averages, we’d nonetheless want to make use of a ~6% cap price as the suitable one right here; keep in mind that debt financing remains to be costly so something under 6% can be unreasonable.

Dangers

In consequence, the potential slender margin of security at finest and its non-existence at worst right here could notice a chance value. Keep in mind that the dividend yield is just too low to offset a possible missed alternative.

Talking of dividends, the distribution document would not make a dividend lower unlikely as I might personally have it in the case of investing in REITs. On the one hand, I can recognize a prudent allocation of capital, however the reluctance to extend the dividend would not exhibit confidence.

Verdict

For these causes, I assign a HOLD ranking and would rethink COLD if it reaches wherever near $20 per share. Such a value level would nonetheless indicate a low yield, however a virtually 20% low cost to NAV based mostly on a conservative assumption of a 7% cap price as the suitable one.

What are your ideas? Do you personal COLD or intend to? Be at liberty to let me know under within the feedback. Thanks for studying.