Bloomberg/Bloomberg by way of Getty Pictures

Following Anglo American (OTCQX:NGLOY) (OTCQX:AAUKF) reset expectations in early December 2023, the corporate’s This autumn 2023 realized commodity costs and working performances align with beforehand communicated steerage. We will conclude that “No information is nice information.” That stated, Anglo is among the largest diversified mining corporations worldwide. It’s headquartered in London and listed in ISE in addition to within the FTSE. Anglo American’s main commodities are iron ore and copper. Our workforce believes the corporate’s danger/reward is extraordinarily enticing.

Certainly, Anglo considerably underperformed during the last two years (-38.86% in inventory worth decline in 2023 and -12% YTD), and we forecast a significant upside danger to the evolution of copper costs as a result of EV transition. As well as, on a draw back state of affairs, Anglo affords a minimal dividend coverage of 40% of earnings, and on the upside, it has two world-class tasks. Right here on the Lab, we carried out two particular analysis research on these new developments: 1) the Quellaveco copper mine in Peru (which is already delivering optimistic outcomes) and a pair of) the Woodsmith polyhalite project in the UK.

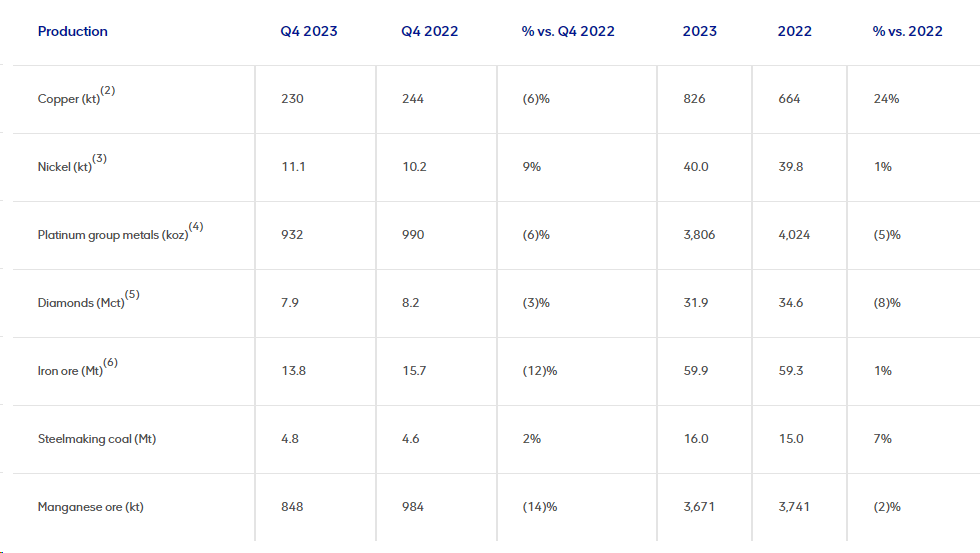

This autumn Manufacturing Evaluation

Earlier than transferring on with our replace, reporting the newest CEO’s phrases is essential. Duncan Wanblad sees “significant value upside from operational resilience, reducing complexity, and growth opportunities.” Publish This autumn launch, we confirmed our 2024 EBITDA forecast at $10.6 billion (7% down versus our earlier estimate).

Anglo This autumn key takeaways that help our numbers are the next (Fig 1):

- Beginning with Copper manufacturing, the corporate lifted output by 20kt in This autumn. That is backed by Quellaveco Mine attaining a quarterly file. That stated, the corporate flags non permanent decrease grades in H1 offset by Quellaveco growth in H2. Subsequently, we utilized no modifications in our estimates;

- Wanting on the Iron Ore, Minas-Rio additionally delivered its highest-ever quarterly quantity of 6.6 million tonnes. Regardless of that, the corporate curtailed manufacturing by 2.5Mt for rail capability upkeep to alleviate mine stockpile constraints. As well as, cross-checking the This autumn efficiency, the realized worth of iron ore was $117 (15% above the benchmark). As reported in our BHP Group’s newest steerage, and regardless of iron ore slides to the bottom since November 2023 due to China demand, our longer-term assumption on iron ore prices is ready at $85/t;

- On the Diamonds division, it’s essential to report that the DeBeers lifted stock by roughly 5Mcts in This autumn. We consider destocking actions will transfer on in 2024. The corporate barely decreased the manufacturing steerage, and This autumn gross sales had been decremental given a decrease realization worth ($83/ct). Our workforce believes that the diamond market is stabilizing after H2 2023. That stated, we already reported our pessimistic view on the Q3 evaluation report, and the newest rumors on potential writedown on the De Beers diamond unit confirmed our detrimental sentiment. Our workforce sees the potential for the corporate to impair Diamond’s belongings. The Diamond division guide worth is at $8.4 billion, and in our estimates, it’s now at $6 billion. That stated, this doesn’t create any change within the firm’s working money move;

- On a optimistic observe, met-coal manufacturing was lifted by 9% to 4.8Mt in This autumn. This was as a result of stable efficiency of Aquilla & Grosvenor, which offset Moranbah geology challenges. Realized worth was robust as a result of combine, and the output is anticipated to be secure in 2024;

- Platinum Group Metals manufacturing fell by 9% quarterly because of Kroondal’s disposal and deliberate upkeep of the Amandelbult web site. On a optimistic observe, refined manufacturing elevated by 31% following smelter upkeep in Eskom.

- As reported by the corporate: “All 2024 outlook is unchanged from the December investor update“.

Anglo American This autumn 2024 Manufacturing Report

Supply: Anglo American Q4 2024 Production Report – Fig 1

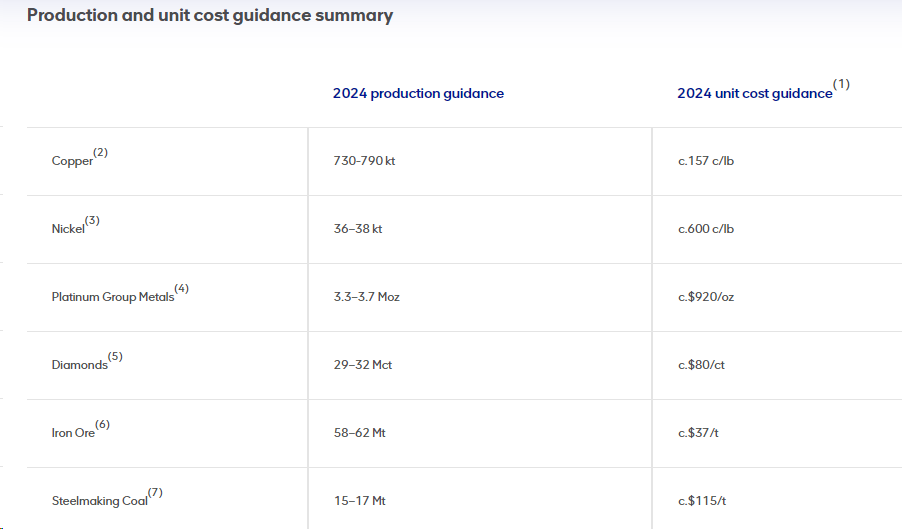

Anglo American 2024 unit value steerage

Fig 2

Conclusion and Valuation

We consider {that a} draw back state of affairs is already priced in. We anticipate an EBITDA of $10 billion in 2023 with a internet debt of $11 billion. Our estimates, aligned with the corporate’s payout, present a dividend per share set at $0.95 for 2024. Along with a possible write-off of the diamond division, we would anticipate administration to replace Wall Avenue on value financial savings initiatives to stabilize operational efficiency. With the confirmed unit value steerage and manufacturing estimate (Fig 2), we see an Anglo 2024 EBITDA of $10.6 billion achievable, with operational efficiency upside due to financial savings and complexity discount. As well as, we consider there’s flexibility in CAPEX.

From a valuation standpoint, Anglo American is presently buying and selling at <4x EV/EBITDA within the subsequent 12 months, in comparison with a historic five-year common of 4.6x. In December, we reset our expectations, reducing our goal worth to £28 per share however sustaining a purchase score standing. In the present day, we confirmed the obese, based mostly on an EV/EBITDA of 4.5 a number of.

As traditional, we level out to potential and present buyers the dangers inherent within the mining sector. This consists of the unstable nature of FX and commodity costs. As well as, the corporate is uncovered to political and operational dangers. These dangers have the potential to influence firm efficiency considerably. Most Anglo belongings are in South Africa, Chile/Peru, Brazil, and Botswana/Namibia.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please concentrate on the dangers related to these shares.