TU IS

During the last month, ANSYS (NASDAQ:ANSS) inventory noticed an enormous leap of round 25% after The Wall Avenue Journal reported that Synopsys (SNPS) is in talks to merge with the corporate. Since then, Synopsys inventory dropped by over 10%. Cadence Design Techniques (CDNS) was additionally cited as a possible suitor for the corporate. Sources stated, “the affords ANSYS attracted worth it well over $400 per share”. ANSYS is at the moment buying and selling at about $350 a share. The query is, is the market overreacting to this potential merger, or is it nonetheless a great time to enter?

A Little Concerning the Business

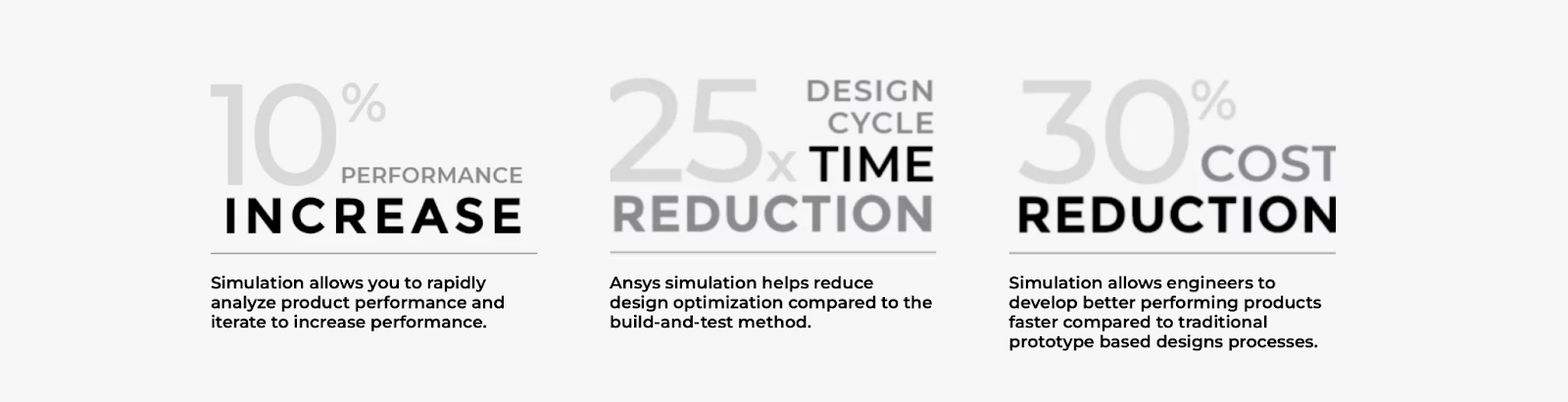

ANSYS focuses on growing engineering simulation software program that’s extensively used around the globe. Its simulation is utilized in a wide range of industries from aerospace to healthcare to 5G to chip design. These simulations are beneficial to engineers for rising efficiency, decreasing design cycle time, and decreasing R&D prices.

ANSYS

The simulation software program market dimension is predicted to extend at a quick tempo of 13.1% CAGR from 2023-2028. Simulation is a wanted characteristic in lots of industries, actually, the report finds that one of many greatest constraints to the expansion of market dimension is the variety of consultants conversant in the software program available. Most significantly, ANSYS works with a subscription mannequin, which is able to generate quite a lot of income simply from the recurring clients.

Then again, Synopsys is an business chief in digital design for the semiconductor and electronics business. It focuses on offering semiconductor design options and IP integration, which principally means to combine pre-designed modules onto a SoC (System on a chip).

Cadence additionally very a lot competes in the identical market as Synopsys, specializing in PCB designs. Its market capitalization on this business is barely second to Synopsys, with a price of $70 billion, in comparison with Synopsys’ $75 billion.

The EDA (Digital Design Automation) market is predicted to climb at a CAGR of 9.1% from 2023 to 2030. A key issue to observe is the mixing of AI and ML into the design software program, as it will possibly massively enhance the effectivity of the designing course of.

ANSYS Monetary Well being and Analysis

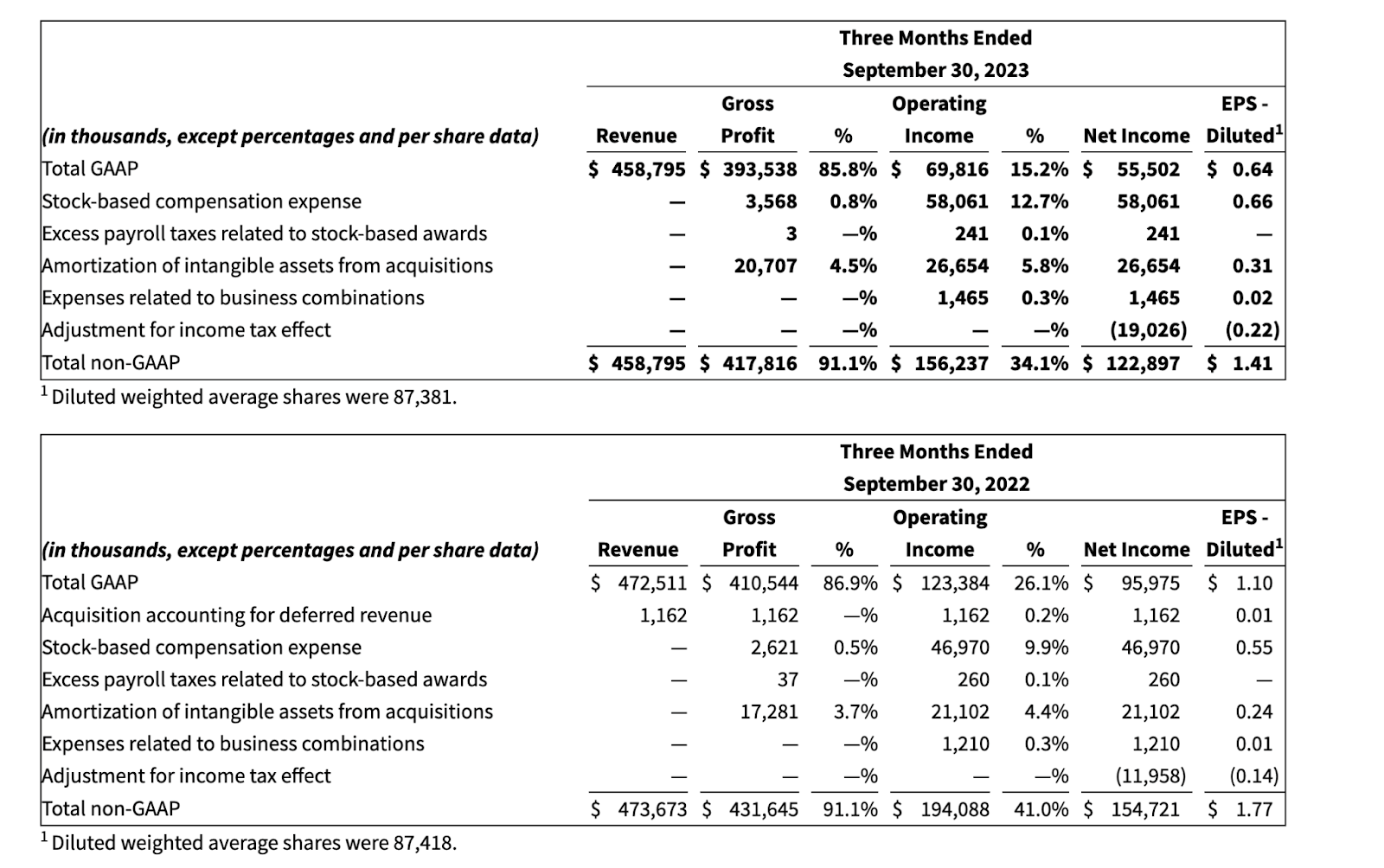

Now, let’s ignore the merger speak and search a good valuation for ANSYS. Over a yr in the past, I evaluated ANSYS at $255, however the market and the economic system have modified since then. In the newest Q3 2023 earnings report, ANSYS’ GAAP and non-GAAP income for Q3 2023 was $458.8 million, which is a 3% lower in reported foreign money or a 4% lower in fixed foreign money in comparison with Q3 2022. ANSYS’ GAAP and non-GAAP diluted earnings per share for Q3 2023 had been $0.64 and $1.41, respectively, in comparison with $1.10 and $1.77 for Q3 2022. Nevertheless, ANSYS’ annual contract worth (ACV) for Q3 2023 noticed a progress of 12% in reported foreign money. ANSYS’ Q3 2023 outcomes had been negatively impacted by incremental approval processes and export restrictions, together with extra restrictions on gross sales to sure Chinese language entities, which created a $20 million headwind to ACV and income that was not contemplated within the third quarter steering offered in August. For its steadiness sheet, the corporate’s money and short-term funding noticed a rise YoY from $614.5 million to $639.5 million. On the similar time, its long-term debt noticed a minor enhance from $753.5 million to $753.8 million YoY.

ANSYS

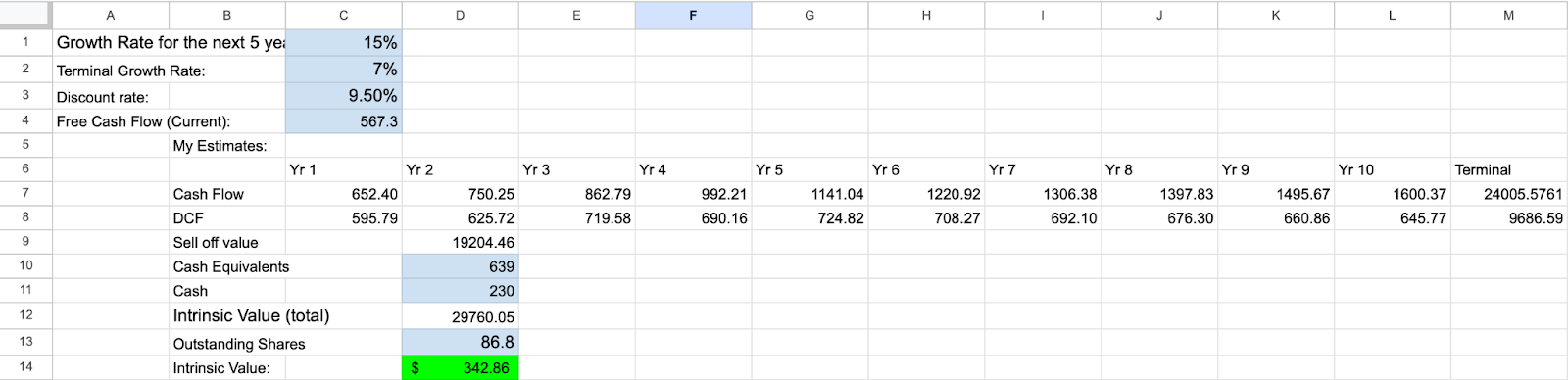

This was fairly excellent news for the corporate, as its income and earnings stayed comparatively secure even amidst a tough political local weather. In reality, its earnings nonetheless beat Wall Avenue estimates by 11%. The sturdy progress in ACV demonstrates that the corporate has a robust and constant buyer base, and might significantly assist enhance profitability and cut back buyer acquisition prices. The corporate is clearly on target and its money circulation displays it. Evaluating Q3 for 2023 and 2022, ANSYS noticed an working money circulation enhance from $127.2 million to $160.8 million. The corporate’s money circulation is rising at a quicker tempo than I used for my earlier DCF analysis, so my new analysis goes to take this new information under consideration.

Creator’s personal Calculations (Sheets)

As soon as once more, when utilizing an assumed 12x terminal worth like I did final time, I additionally elevated the expansion fee to be barely increased than the anticipated CAGR for the market. And an attention-grabbing conclusion is reached – the corporate has grown into its intrinsic worth. Fairly curiously, I consider ANSYS is now correctly valued.

Plausibility of a merger and why I feel it will not occur

So an ANSYS merger is within the speak, who will come on prime? I feel nobody. Initially, between Cadence Design Techniques and Synopsys, it’s Synopsys who’s more likely to merge with ANSYS. Along with its better market capitalization, ANSYS and Synopsys have already been collaborating for years up so far. Whereas the 2 corporations do not immediately compete in the identical market, I consider a lot of ANSYS’ simulations and physics can significantly improve the calculations utilized in Synopsys’s software program. On the similar time, Cadence is a direct competitor to Synopsys, so there may be little likelihood it would merge with ANSYS.

For Synopsys, merging with ANSYS would imply not solely enhancing its simulation proficiency, but additionally reaching into fully new markets that ANSYS is part of.

Whereas this all sounds nice, ANSYS at the moment already has a market cap of $30 billion, so the value of the merger might presumably go as much as $40 billion. Synopsys is barely value $70 billion. So utilizing the stock-for-stock merger methodology, I consider the corporate inventory could possibly be anticipated to fall loads. When a merger occurs, the market cap simply would not merely add collectively. It could not be shocking if the market cap barely modified and the one factor that modified was the variety of excellent shares. Issuing and distributing over half the variety of its current shares is simply not a sensible transfer for any firm and could be actually dangerous for its traders for my part. We’re speaking about potential monetary troubles for the corporate which will take over a decade to get better. As well as, this deal wouldn’t simply be achieved as 2 competing corporations are within the potential merger speak. Even when one firm will get the merger deal, the opposite firm would doubtless not let it come out unscathed for my part. In the long run, I feel each events will notice a merger wouldn’t make a lot monetary sense.

Conclusion

For my part, whereas the general public is overreacting to the merger rumors, ANSYS inventory has really grown to its intrinsic worth. I don’t suppose both Cadence or Synopsys will merge with ANSYS. Thus, ANSYS inventory, on the present second, is a maintain.