akiyoko/iStock through Getty Pictures

Simply over 2 years in the past, Stone Fox Capital warned buyers that Apple (NASDAQ:AAPL) was dead money for up to 4 years. The inventory of the tech large was set to wrestle with the robust new product improvement wanted to warrant the present worth on the time, a lot much less larger costs through the years. My investment thesis stays extremely Bearish on the inventory with the valuation nonetheless disconnected from the dearth of development.

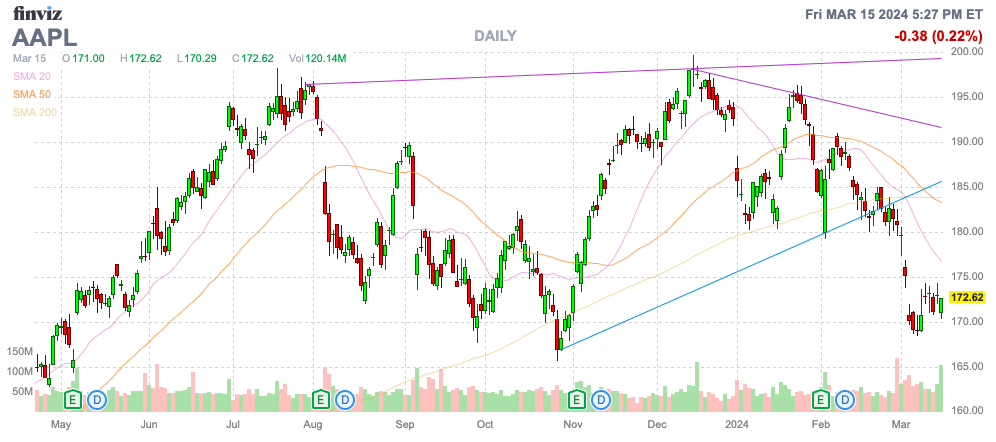

Supply: Finviz

Product Improvement Hiccups

Again in March 2022, analysts have been forecasting Apple to generate minimal development over the following 4 years whereas the inventory had already priced in huge development. The key query was whether or not the tech large may even hit these development charges.

Apple actually wanted new merchandise like AR/VR units and autonomous EVs as a way to hit the expansion charges wanted to warrant a inventory buying and selling up at $166. On this entrance, the Imaginative and prescient Professional was lately launched with minimal income forecasts attributable to manufacturing limits and the lengthy vaunted Apple Automotive plans have been terminated.

The corporate enters the mid-point of FY24 with neither merchandise anticipated to supply materials revenues to Apple over the following few years when these merchandise have been the long run development drivers of the FY22 funding thesis. The Imaginative and prescient Professional undoubtedly has some constructive suggestions when launched, however the $3,500 worth level and complexity in making the AR/VR system has restricted each provide and demand. To not point out, Apple hasn’t introduced any street map for the AR/VR system phase, just like how the iPhone has new product releases on an annual foundation.

Prime analysts like Dan Ives of Wedbush Securities and Wamsi Mohan of BofA Securities forecast Imaginative and prescient Professional gross sales within the 400K to 600K range. At $3,500 a unit, revenues will solely hit $1.4 to $2.1 billion for 2024, which might presumably embody the December quarter that counts in direction of FY25 gross sales.

Influential Apple analyst Ming-Chi Kuo has even advised gross sales have slowed down significantly following the early adopter rush resulting in issues concerning the depth of demand. The analyst suggests the MR system product roadmap has restricted visibility with an anticipated cheaper model in Q1’26 adopted by a brand new mannequin with superior expertise not till 2027.

Mohan gives a 4 million unit estimate for the lower-end mannequin in FY26. At a value of $2,000, the Imaginative and prescient Professional line would generate solely $8 billion in gross sales and this quantity seems aggressive contemplating the demand equation as slowed dramatically for the preliminary system and $2K for an AR/VR system remains to be extraordinarily costly for client adoption.

On the similar time, Apple faces an existential menace in China with iPhone gross sales plunging. Counterpoint Analysis documented a 24% dip in iPhone sales in China for the primary 6 weeks of 2024 after Huawei shocked the market with a aggressive smartphone regardless of U.S. chip restrictions.

Supply: Counterpoint Analysis

Huawei noticed gross sales surge 64% YoY to begin 2024 whereas different smartphone producers noticed gross sales droop. Total items offered in China have been down 7% YoY contributing to substantial weak spot for Apple with market share down 3 proportion factors to 16% on high of the weaker gross sales ranges.

China is a giant drawback for Apple with FY23 gross sales representing 19% of whole revenues. The nation produced $73 billion in annual gross sales and was the second largest area for the tech large, barely behind the entire Europe at $94 billion.

Supply: Enterprise of Apps

In actuality, Apple does not have a shiny spot within the product improvement street map until the iPhone 16 sees additional demand from an AI focus. The iPhone 15 confronted issues from the beginning with no important upgrades resulting in apathy in upgrading a cellphone costing upwards of $1,000.

The iPhone now generates $200 billion in annual gross sales and the weak spot in China is a significant concern. Even with the 5G iPhone and Covid pull forwards, iPhone gross sales are nonetheless solely barely above the FY18 stage of $166 billion, chatting with demand points. Apple remains to be solely promoting roughly the identical iPhones as FY15 when items offered first topped 230 million leaving the entire income good points attributable to larger ASPs.

Inventory Weak spot Ought to Persist

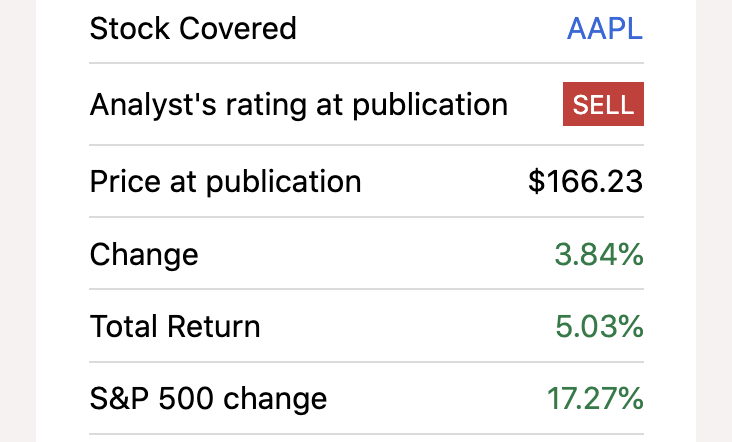

The unique useless cash thesis was written again in March 2022 and Apple has solely risen 4% in the course of the interval with the S&P 500 index up over 17%. The inventory rose to a excessive of almost $200 throughout this era and buyers have been warned that an irrational rally would possibly happen, even to as excessive as $250.

Supply: Looking for Alpha

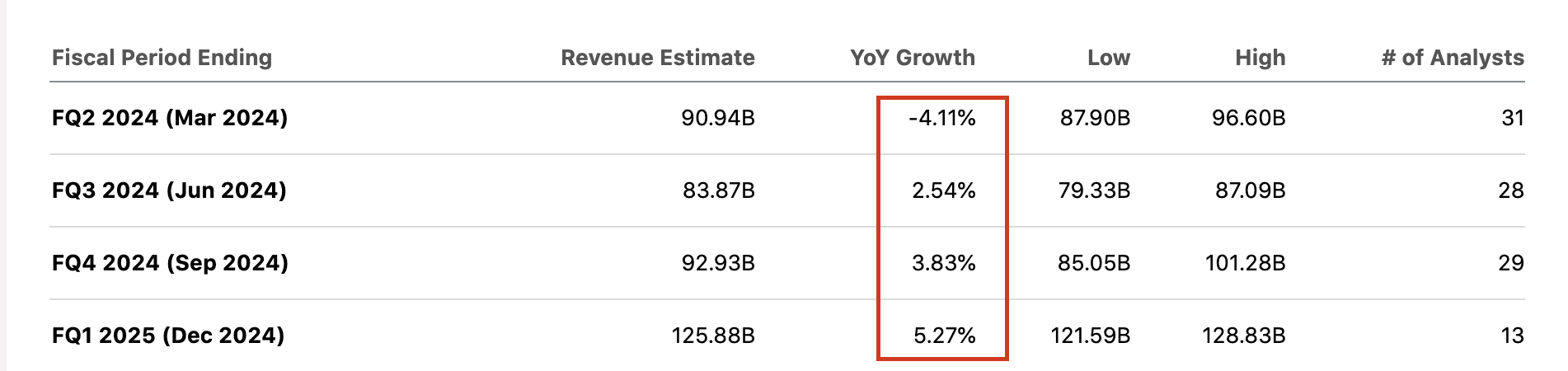

The important thing right here is that Apple has now reported 5 consecutive quarters of minimal or detrimental development charges and the forecasts forward aren’t significantly spectacular. The corporate guided to FQ1’24 gross sales dipping $5 billion from the gross sales ranges of FQ2’23 resulting in a 4% decline. The analyst forecasts for development the next 3 quarters seem significantly aggressive contemplating the iPhone gross sales points in China and the dearth of latest product innovation offering a lift to revenues.

Supply: Looking for Alpha

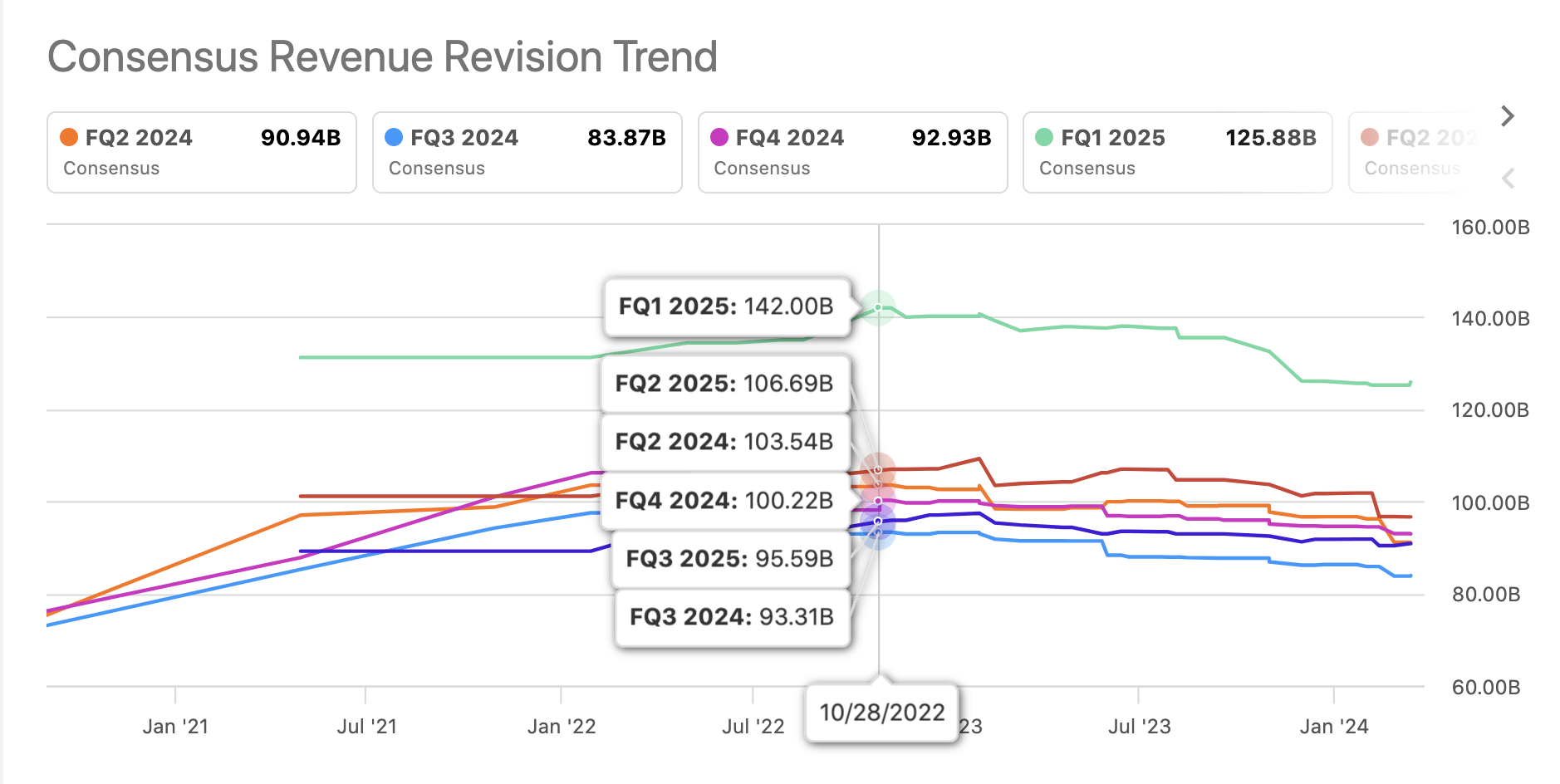

A major instance of how analyst estimates have been overly aggressive for some time now are the FQ1’25 revenues targets. The consensus targets again in October 2022 have been $142 billion and the quantity has now fallen under $126 billion for less than 5% development YoY.

Supply: Looking for Alpha

As highlighted in our analysis during the last 2 years, Apple has a historical past of usually matching analyst targets for the quarters forward. The tech large will beat estimates by a minor quantity with restricted development. Solely in the course of the Covid interval did gross sales development ramp up and the corporate begin smashing analyst estimates, however that interval of extreme development is probably going contributing to a few of the weak spot now.

The unique useless cash article even predicted what the FY25 EPS estimates would appear like, if Apple truly beat analyst estimates by 5% yearly. The EPS goal was nonetheless solely $8.82 below a bullish money situation and now the consensus analyst EPS estimate is simply $7.16.

Even below one of the best case situation the place Apple was producing the annual 6% development charges and beating analyst EPS targets, the inventory nonetheless did not justify a worth of $166. Now, Apple nonetheless trades at 26x these lowered EPS targets and the worth is clearly not justified.

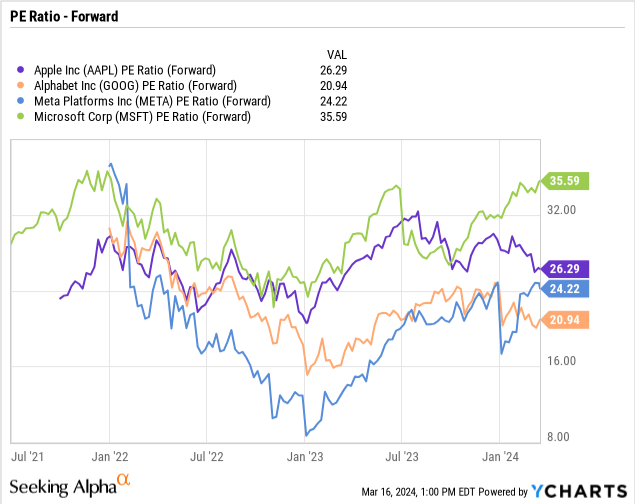

The inventory nonetheless trades at larger multiples than Meta Platforms (META) and Google (GOOG) regardless of these firms being closely concerned in AI and already reporting robust development. Microsoft (MSFT) trades in a unique environment at almost 36x ahead EPS targets.

Regardless of the market loving these Magnificent 7 shares during the last 2 years, a number of shares have significantly lagged the market throughout a tricky interval. One has to actually query why Apple has a good valuation when even a 20x PE a number of solely produces a $143 inventory worth.

Once more, the market might be aggressive assigning 7% to 10% EPS development charges for Apple over the following 3 years. Even when the corporate makes these targets, Apple ought to be fortunate to garner a 15x a number of with none clear new product providing a path for materials development off a income base approaching $400 billion.

The Imaginative and prescient Professional is the one product garnering client intrigue, however the common consensus is for gross sales of just a few billion within the subsequent few years and the product will shortly age heading into FY26. Apple hasn’t proven any signal of an up to date product thus far.

Takeaway

The important thing investor takeaway is that warning buyers that Apple ought to be useless cash for 4 years was truly over constructive on the result. The inventory ought to see appreciable draw back based mostly on the weak outcomes and ongoing product improvement failures. CEO Tim Cook dinner turns 64 this yr and stress may begin mounting for his retirement after one other yr missing development and weak product improvement resulting in a weak inventory worth.

Buyers ought to contemplate the inventory nonetheless buying and selling above $170 as a present. In a traditional market, Apple can be fortunate to commerce at 15x EPS targets resulting in a inventory worth of solely $107. The inventory may simply face greater than 2 years of ongoing useless cash with the true threat that buyers face detrimental returns over this era whereas watching years of good points disappear.