Bloomberg/Bloomberg by way of Getty Photographs

After a yr of income declines, evidently Apple (NASDAQ:AAPL) has lastly discovered its footing. The newest first rate earnings report for Q1 together with the profitable launch of Imaginative and prescient Professional headset point out that the Cupertino large is lastly on the trail to restoration after a yr stuffed with disappointments. Nonetheless, the corporate nonetheless faces a number of main inner and exterior challenges, together with China-related dangers, which could undermine Apple’s momentum within the following months. As such, the corporate’s shares will probably proceed to really feel the promoting strain regardless of the current appreciation because the draw back won’t be totally priced at this stage.

Apple Is Lastly Rising Once more

In my newest article on Apple that was printed final yr, I’ve been highlighting two main points that the corporate has been dealing with, that are the dearth of development and the rise of China-related dangers. If we look at Apple’s efficiency in FY23, we’ll see that its revenues had been declining Y/Y throughout every consecutive quarter of the final yr on account of the dearth of development catalysts. The excellent news although is that evidently the expansion difficulty has lastly been fastened and one other quarter of income declines has been averted.

Earlier this month, Apple released its Q1 earnings report, which confirmed that the corporate’s revenues in the course of the interval elevated by 2.1% Y/Y to $119.6 billion and had been above expectations by $1.34 billion. The corporate has additionally reported a stable bottom-line efficiency, as its GAAP EPS of $2.18 had been above the estimates by $0.07.

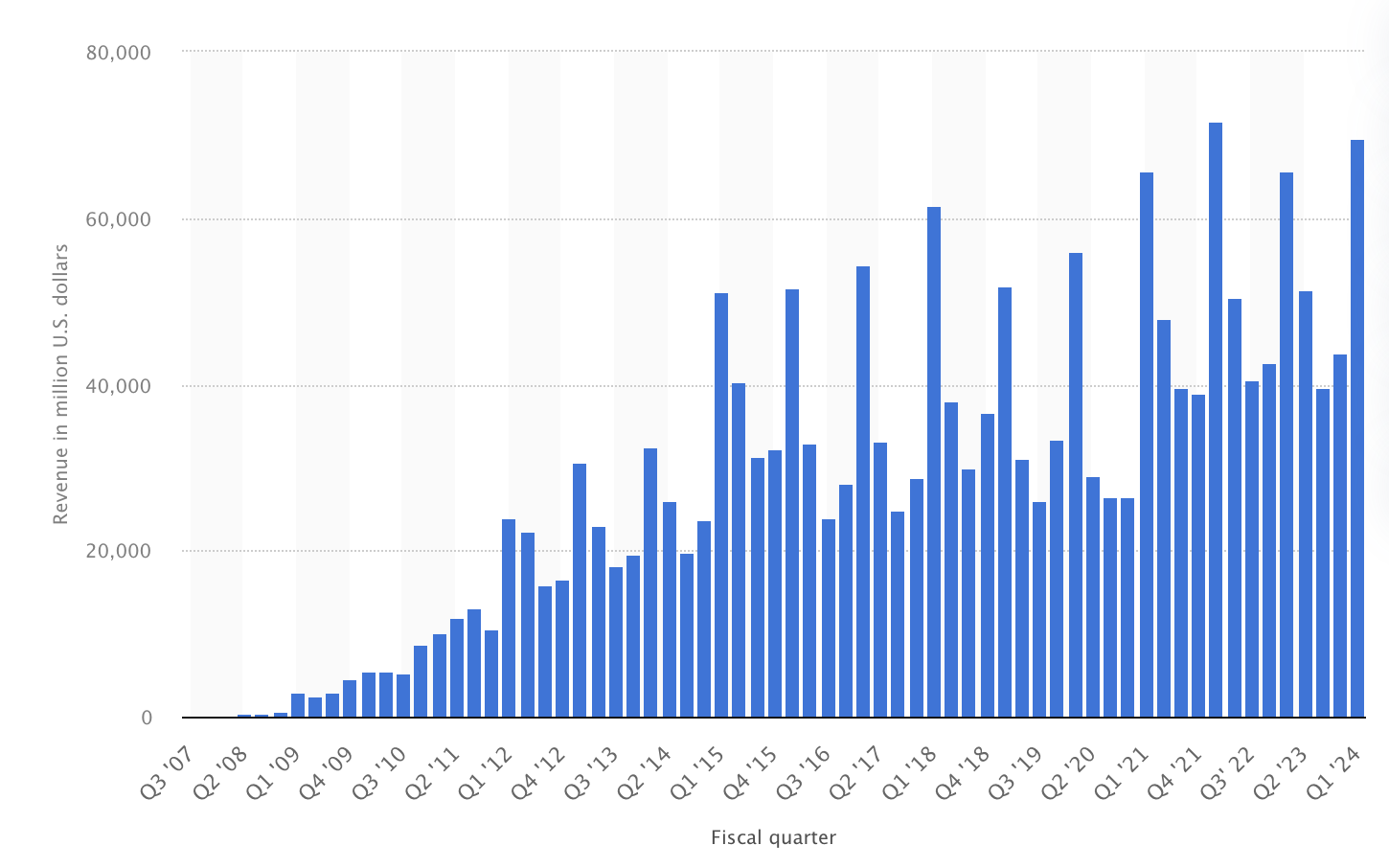

It could be secure to say that such a efficiency didn’t come as a shock, regardless of the disappointing efficiency in current quarters. In any case, we shouldn’t neglect that Apple launched its newest iPhones final September and managed to retain the gross sales momentum in current months. That’s one of many essential the reason why the revenues generated by the iPhone enterprise elevated by 6% Y/Y in Q1 to $69.7 billion. On the identical time, the corporate managed to set a brand new gross sales report in a number of areas, and grew its iPhone person base to a brand new all-time excessive, whereas Q1 became the second-best quarter when it comes to iPhone gross sales in Apple’s historical past.

Apple’s iPhone Income Chart (Statista)

It’s additionally essential to notice that though the corporate’s total revenues had been on a decline final yr, its companies enterprise has been exceeding expectations for some time and that was additionally the case in Q1. The newest earnings report confirmed that the revenues of Apple’s companies enterprise elevated by 11.4% Y/Y to $23.12 billion and set a brand new report for the corporate. Such a efficiency was achieved primarily because of the rise of the put in base, as Apple now has over 1 billion paid subscriptions throughout its ecosystem. What’s extra is that even when the iPhone gross sales lose their momentum within the following months, the companies enterprise is predicted to proceed to develop at a double-digit fee sooner or later and mitigate a number of the downsides that is likely to be attributable to the weaker efficiency of different segments.

As for Apple’s different segments, there are causes to be optimistic about their future as effectively. Within the following months, we’re probably going to see a release of recent iPads and MacBooks to spice up gross sales, whereas the current launch of Imaginative and prescient Professional headset has the potential to revive development of the corporate’s wearable section that recorded a income decline of 11.4% Y/Y to $11.95 billion in Q1. Final yr I noted how regardless of its excessive price ticket of $3500, Imaginative and prescient Professional might develop into a serious catalyst of development for Apple as a result of distinctive launch technique that goals to reduce the mission’s prices and scale the person base on the identical time. It’s secure to say that this technique has been profitable up to now because the firm could sell as many as 600,000 headsets this yr alone, above the earlier expectations of 460,000 units, which might increase the wearables section income by an extra ~$2 billion in FY24.

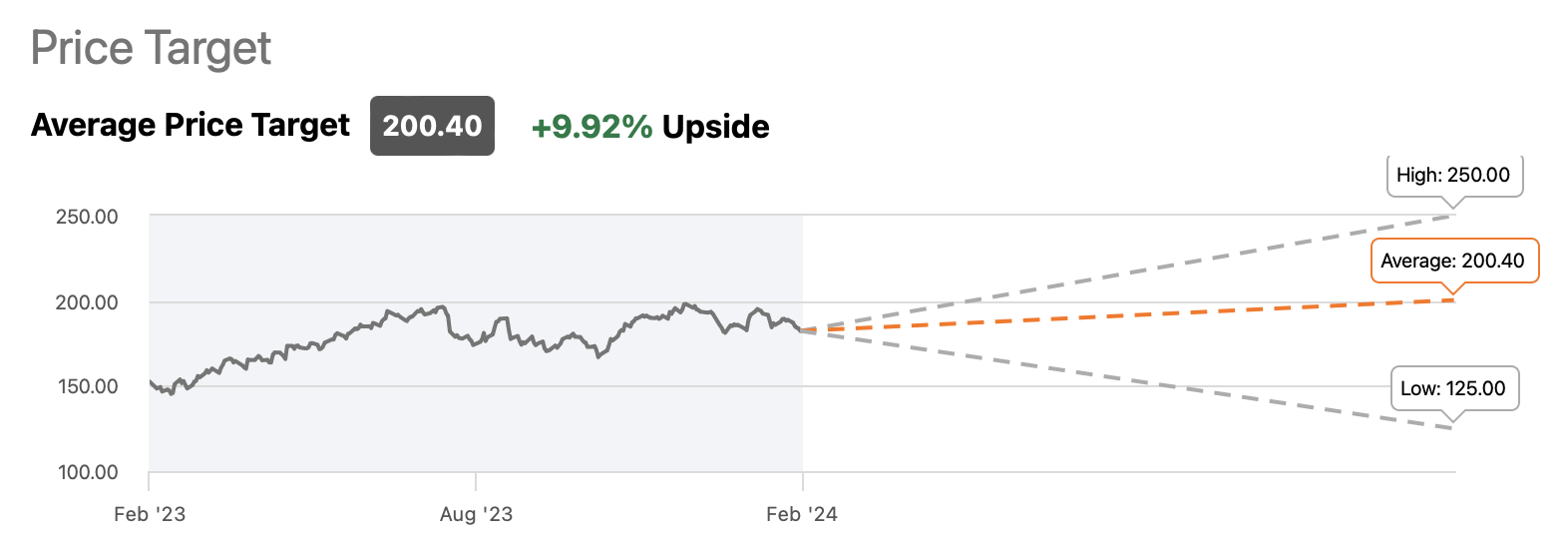

One other optimistic factor about Apple is that it seems that its inventory presently trades at a reduction and represents ~10% upside based on the road consensus. With a ahead P/E of ~28x, the shares are additionally trading near the S&P 500 common P/E of ~27x. This may recommend that if the market continues to develop on optimistic macro knowledge, then Apple’s shares might additional admire and even outperform the remainder of the pack given the quantity of development catalysts that the corporate has.

What’s extra, is that the continuation of the buyback program might guarantee an extra appreciation of the share worth within the following months. In Q1 alone, Apple repurchased 112 million of its shares at a complete worth of $20.5 billion, and an identical factor might occur within the following quarters as effectively. Add to all of this the truth that there’s an indication that Apple is prone to return to development and as soon as once more improve its revenues Y/Y this yr and past, it is sensible to consider that the bullish thesis will not be totally lifeless at this stage.

Apple’s Consensus Worth Goal (In search of Alpha)

Is The Momentum Going To Be Brief-Lived?

The most important difficulty with Apple is that though its shares have an upside on the present worth and will additional admire within the close to time period on optimistic macro knowledge, the corporate faces a number of main challenges that might undermine its development potential in the long term. Let’s not neglect that whereas the road expects Apple to develop Y/Y in FY24 partially because of the first rate ends in the earlier quarter, the corporate’s steerage was not as stable as the road anticipated. This is because of the truth that Apple is very reliant on China each from the availability and demand facet, which has develop into one of many firm’s greatest weaknesses lately.

On the one hand, Apple is struggling to compete with native Chinese language opponents, which have been aggressively rising their market share on the mainland lately. In Q1, Apple’s revenues within the Higher China area decreased to $20.8 billion, down from $23.9 billion a yr in the past and beneath the road expectations of $23.5 billion. On high of that, Chinese language manufacturers like Xiaomi and Huawei are about to release their latest smartphones in China within the foreseeable future, which might make it even tougher for Apple to generate aggressive returns there sooner or later. Whereas the Cupertino large lately decided to supply extra reductions to Chinese language customers, it’s questionable whether or not such a tactic would work given the rising competitors that provides smartphones at extra reasonably priced costs and the potential deflation in China that might undermine the corporate’s gross sales efforts on the mainland. The road already made dozens of income downside revisions in current months and expects the corporate’s gross sales to lower Y/Y in Q2 as China’s client sentiment stays muted.

Then again, Apple continues to be tremendously uncovered to geopolitical dangers as a result of majority of its provide chain remaining in China. There’s an indication that near 80% of the corporate’s manufacturing companions have a footprint in China, whereas Apple itself lately deepened its cooperation with Chinese language companies. Given the rise of tensions within the Taiwan Strait, the worsening of Sino-American relations, and the potential implementation of new trade restrictions, it turns into apparent that having nice publicity to China is not thought of a bonus as was the case even a decade in the past.

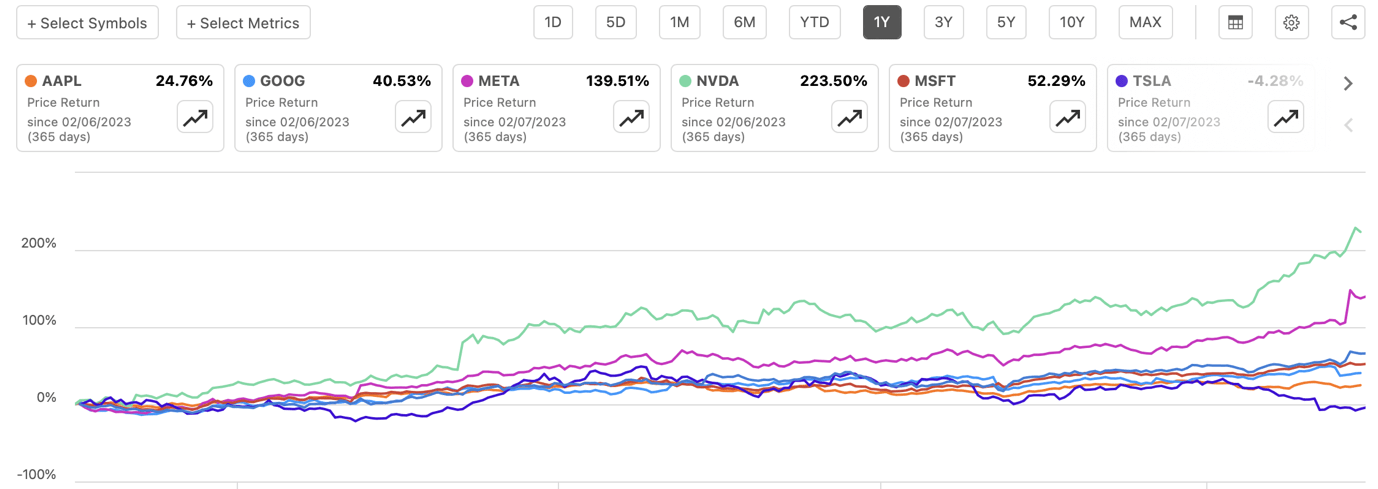

On account of all of this, Apple’s inventory could possibly be ‘dead money’ within the foreseeable future as the corporate is in a worse place compared to its Huge Tech friends that aren’t that uncovered to China, particularly from the availability facet. If we examine the efficiency of Apple’s inventory to its Magnificent 7 friends, we’ll see that the corporate has tremendously underperformed towards most of them aside from Tesla (TSLA), which additionally has great exposure to China. Contemplating this, it’s secure to imagine that Apple might proceed to underperform towards the opposite massive names that don’t immediately face the identical ‘China problem.’

Apple’s Worth Return Comparability Towards Its Friends (In search of Alpha)

The Backside Line

Apple is in a troublesome spot presently. On the one hand, it’s nice to see that its enterprise is lastly rising once more after a disappointing efficiency in FY23. Then again, there’s a danger that its momentum goes to be short-lived as a result of varied inner and exterior challenges, together with China-related dangers, that the corporate faces. As such, I’m sticking with my HOLD ranking for now contemplating that whereas Apple’s inventory has some extra room for development because of the most recent developments, its upside seems to be restricted on the present worth since many of the draw back is probably going not totally priced in at this stage.