ozgurdonmaz

Whereas Apple (NASDAQ:AAPL) was one of the crucial vital holdings in my portfolio a number of years in the past, I’ve been neutral or negative on the stock extra not too long ago. And I have been proper. Whereas many high-quality tech shares have surged to new all-time highs on this AI-driven bull market, Apple’s inventory has been basically useless cash for years.

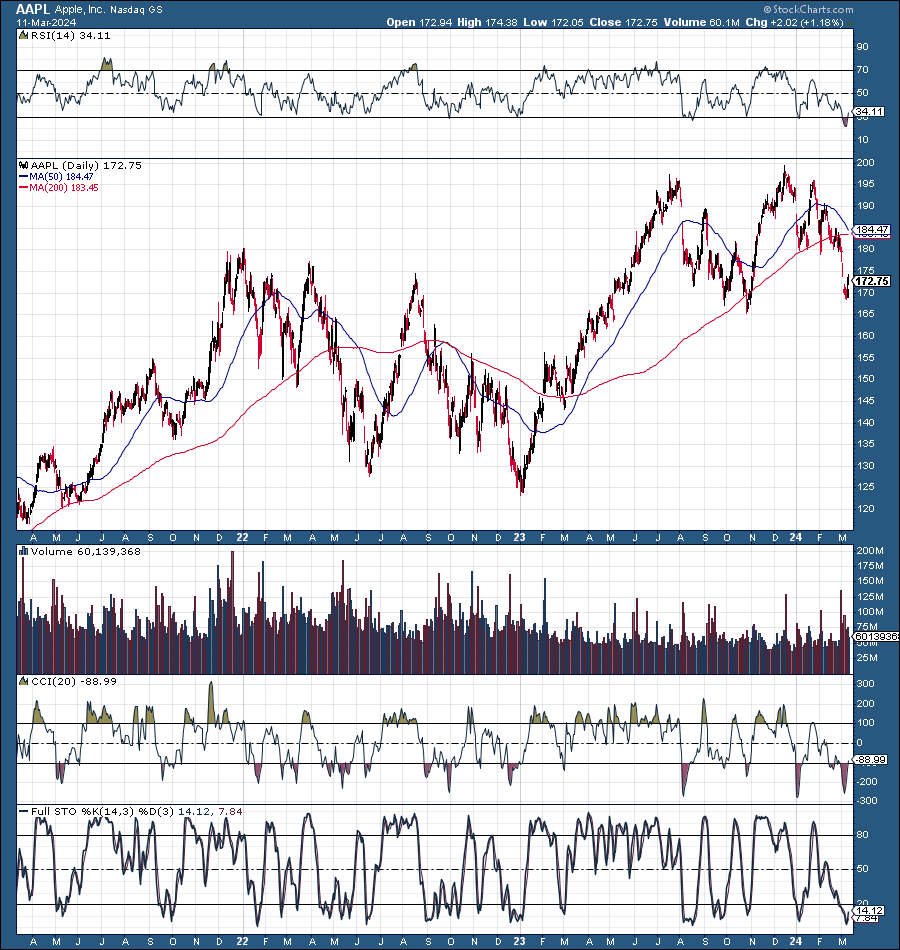

Apple 3-Yr Chart

AAPL (stockcharts.com)

Apple’s inventory has solely elevated by about 35% within the final three years and is now under its peak in 2021. Moreover, Apple is down by round 15% from its latest double-top, and there’s no proof that its share worth will make a significant restoration any time quickly.

Apart from Apple’s deteriorating technical picture, its valuation stays excessive, and the corporate has minimal development potential within the close to time period. Apple’s China sales are plunging, and Huawei and different Chinese language smartphone makers appear intent on protecting their lead.

Apple is a worth inventory, buying and selling at a development inventory’s valuation (27 forward P/E ratio). Moreover, Apple lacks clear catalysts that may allow appreciable development to return quickly. Moreover, Apple may face margin compression as a result of faltering iPhone, Mac, and different gross sales. Due to this fact, we may proceed seeing a number of compressions and a decrease inventory worth for Apple as the corporate churns via one other stagnant part.

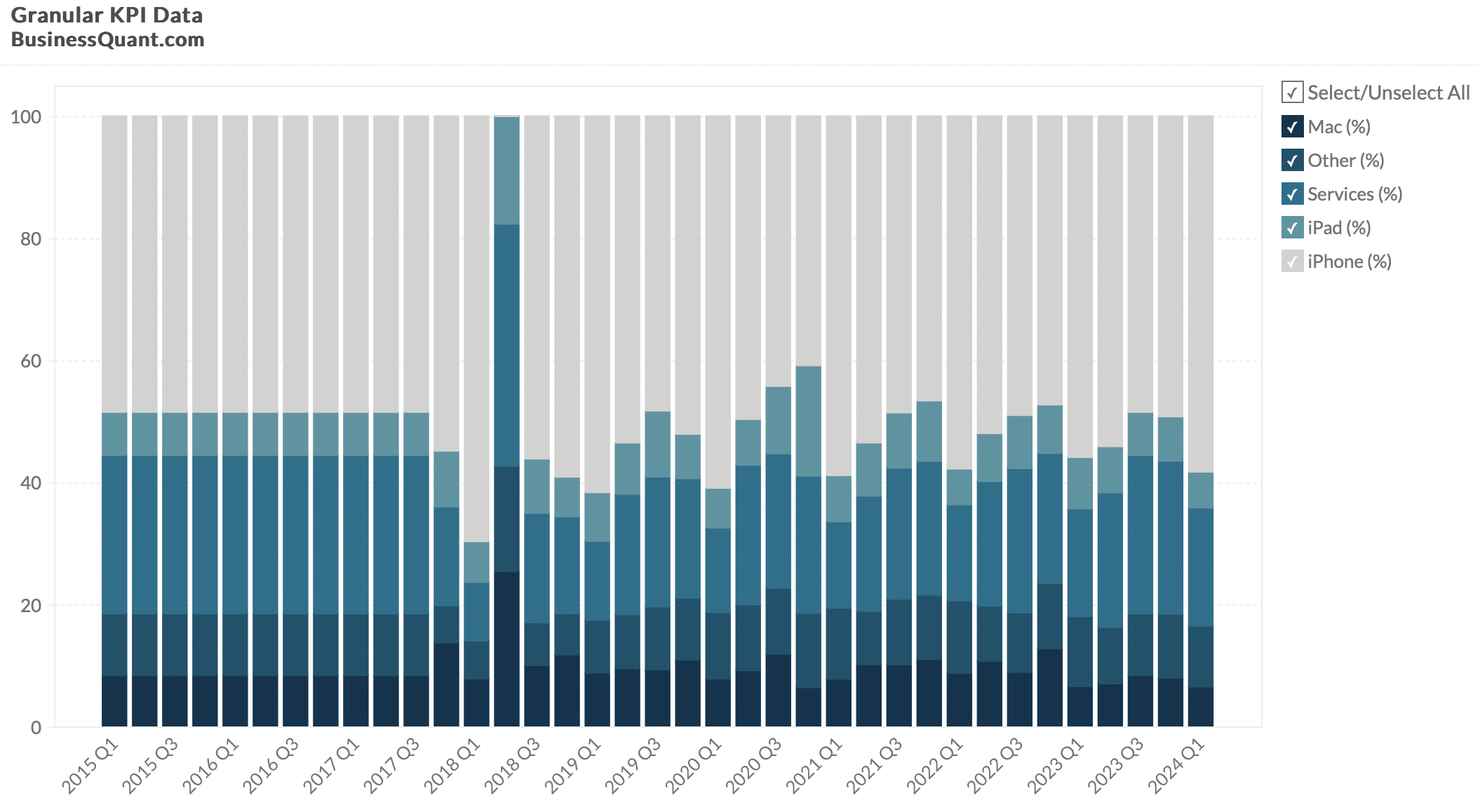

iPhone Gross sales Are A Drawback

The issue with Apple is that the lion’s share of its revenues nonetheless comes from iPhone gross sales. In truth, final quarter, iPhone gross sales accounted for over 58% of Apple’s whole revenues.

Apple Gross sales By Phase

Gross sales by section (businessquant.com)

This determine represented the best proportion of whole gross sales since Q1 2021, three years in the past. One other vital drawback for Apple is that iPhone gross sales have peaked and at the moment are declining.

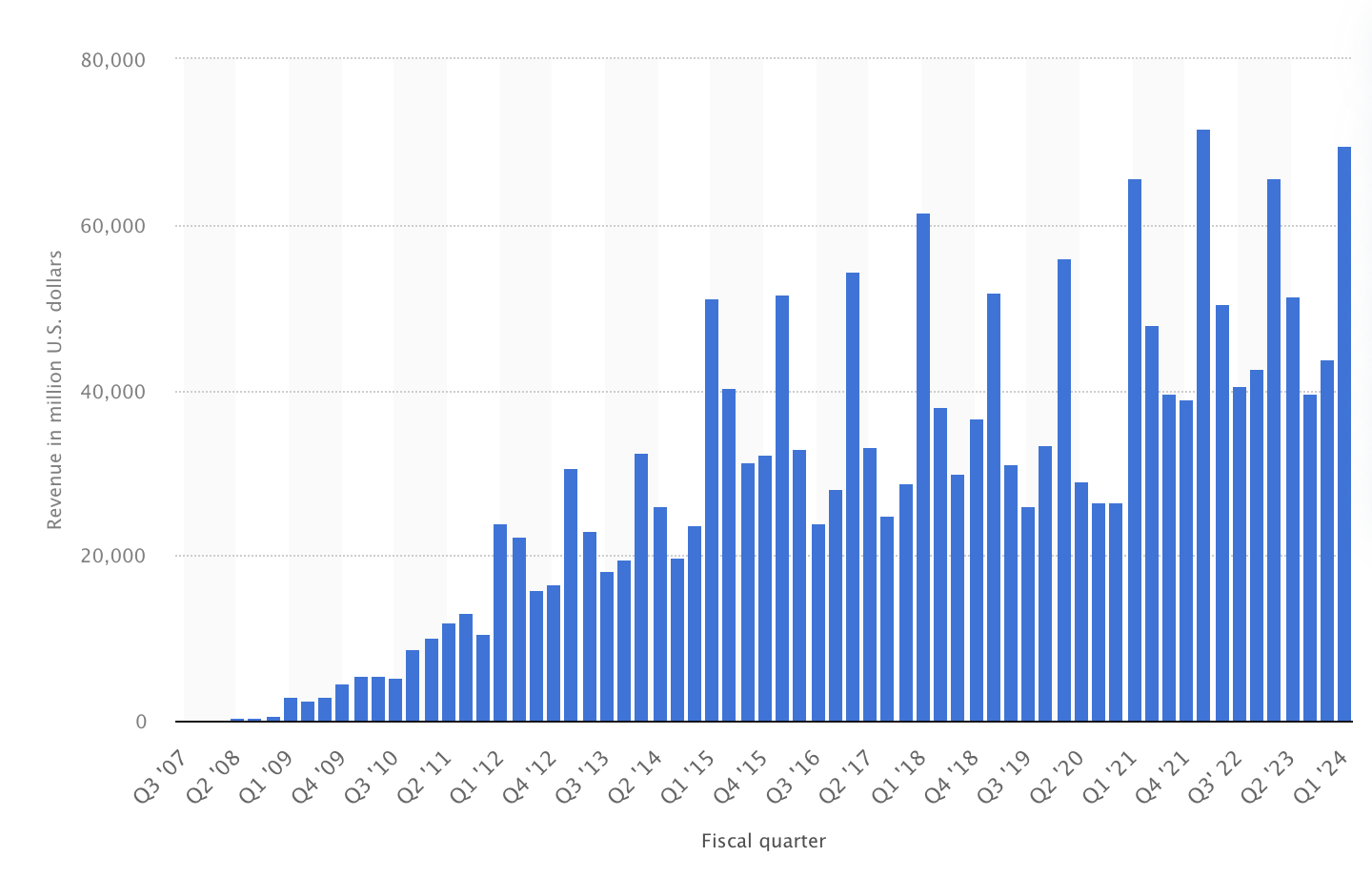

iPhone Gross sales By Quarter

iPhone gross sales (statista.com)

In Q1 2022, iPhone gross sales have been round $71.63 billion (registration required). In Q1 2024, iPhone gross sales have been $69.7 billion, practically 3% decrease than two years in the past. One main difficulty is that the iPhone has turn into stale, with its newest fashions nonetheless sporting the same look because the iPhone 12. Why would I improve for incremental enhancements I can not distinguish from older fashions if I personal the iPhone 12?

Do I have to get a barely totally different black shade variation? I do not see a motive to improve. So, I’m nonetheless utilizing my iPhone 12 Professional Max. Seemingly, I’m not alone, and extra folks could also be utilizing their iPhones for longer, three or possibly even 4 years, as a substitute of the standard cycle of two years or much less.

China Is A Huge Problem

China is an enormous marketplace for Apple, with roughly 17.5% of its whole gross sales coming from this one nation alone. Nevertheless, gross sales in China dropped by 13% YoY final quarter, and issues may worsen. As a result of reputation of Huawei and different extremely succesful home smartphones, Apple’s gross sales crashed by 24% within the first six weeks of the brand new yr. The weak demand has prompted Apple to cut prices, a dynamic that may most likely eat into its margins, negatively affecting Apple’s backside line. Furthermore, there isn’t any clear catalyst for the pattern to alter, as Apple’s Chinese language rivals proceed innovating and seem like profitable the smartphone conflict in China.

Mac And iPad Gross sales Proceed Slipping

Regardless of Apple’s progress with new in-house processors and new iPad/Mac fashions, the segments usually are not doing nicely (growth-wise).

Gross sales by section (investor.apple.com)

The Mac area was basically flat YoY, and iPad revenues crashed by over 25% YoY. Mixed, the revenues of the 2 segments declined by 14% from final yr. Apple’s wearables, house, and equipment section, a shaped vibrant spot, can also be declining, with gross sales dropping by 11% from final yr. Apple’s lonely development engine, its providers section, which was placing up stable double-digit development in recent times, additionally illustrates indicators of a substantial slowdown, offering simply 11% development YoY.

The Imaginative and prescient Professional Could Not Be A Blockbuster Product

There are “rumors” that Apple has bought round 200,000 units of its Imaginative and prescient Professional Headsets. Nevertheless, at a nostril bleeding $3,500 per unit, the topset may stay a comparatively area of interest product as a substitute of going mainstream (just like the iPhone). Some analysts predict Apple will promote round 400,000 units this yr and round a million Imaginative and prescient Professional Headsets in 2025. Nevertheless, 400,000 models symbolize about $1.4 billion in gross sales, and a million models is simply round $3.5 billion, which is minuscule relative to Apple’s $383 billion in revenues final yr, and is hardly able to delivering vital development, in my opinion.

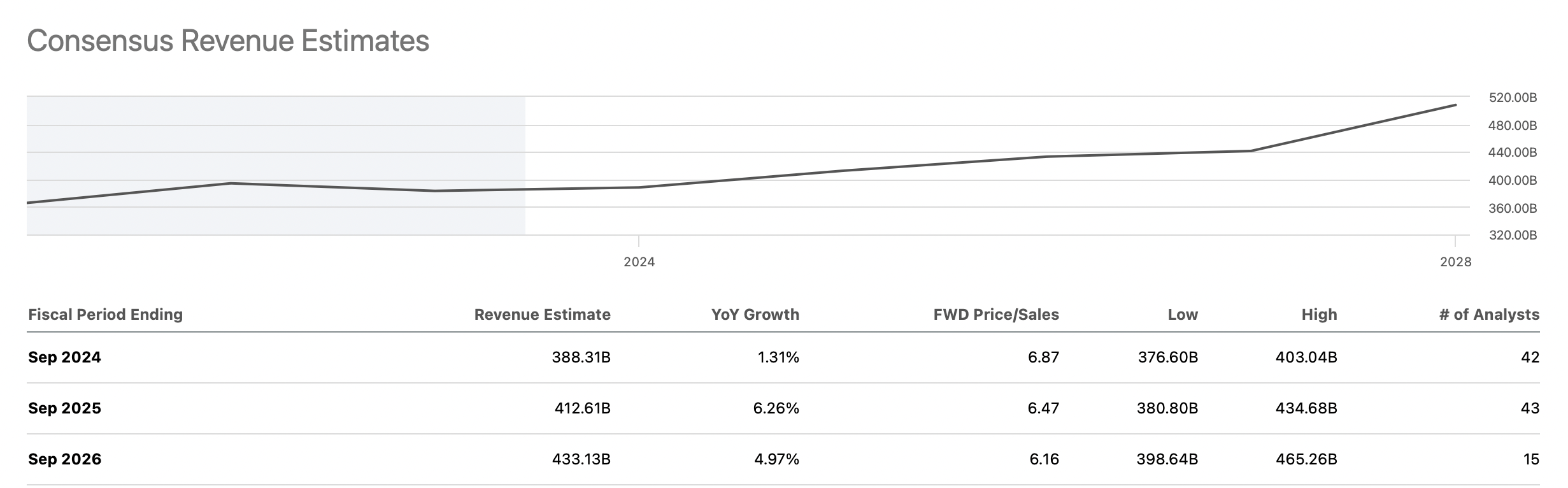

Apple Is Not A Development Inventory Anymore

When Apple launched the iPhone and introduced different extremely revolutionary merchandise to the market, it was a development inventory. Nevertheless, the market has turn into extremely saturated with Apple merchandise, and Apple is just not a development inventory anymore.

Gross sales development (seekingalpha.com )

In truth, Apple’s future development seems exaggerated, as there aren’t any clear catalysts to spark appreciable development. Quite the opposite, Apple’s gross sales declined by about 3% final yr, and income development projections for this yr are underneath 2%. Due to this fact, Apple’s 2024 gross sales will probably be under 2022 ranges, illustrating that Apple’s development is stagnating with out a complete catalyst to enhance.

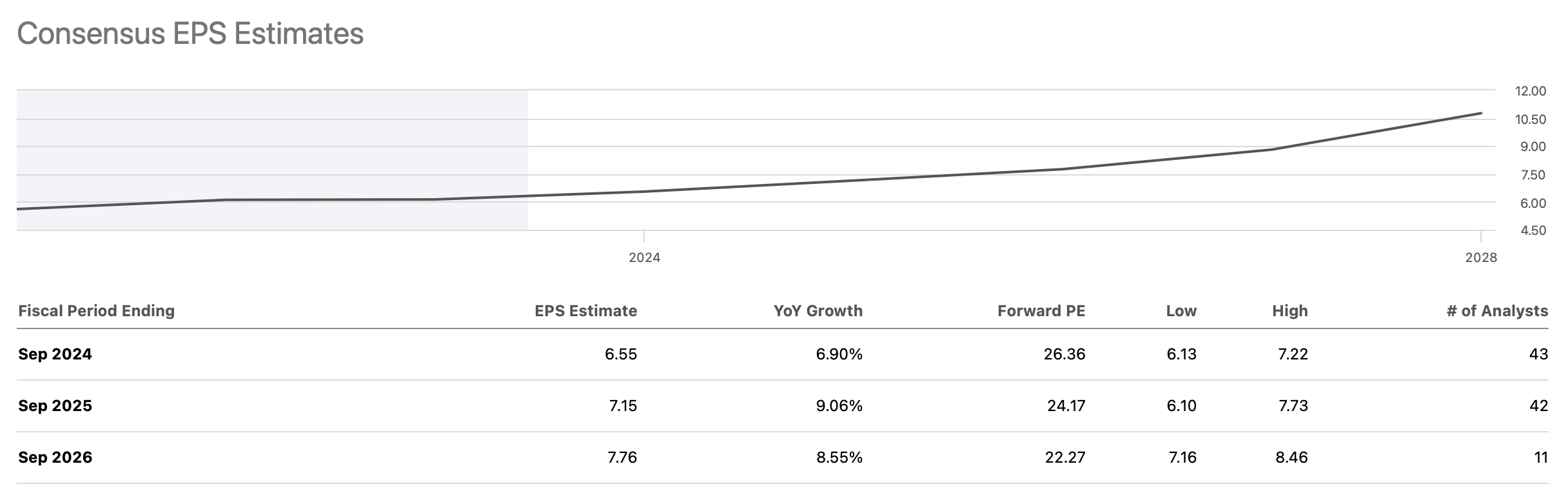

EPS May Stagnate Or Decline

EPS projections (seekingalpha.com)

Apple’s EPS elevated by simply two cents yr over yr final yr. Due to this fact, I’m not positive the place the projected 7-10% EPS development will come from in future years. Quite the opposite, Apple faces margin compression points as a result of elevated competitors in China and different areas. Due to this fact, we may even see stagnant or declining EPS as a substitute of the anticipated development.

Apple may earn round $6 per share, towards the decrease finish of analysts’ EPS estimates this yr and in 2025. This dynamic implies that Apple’s EPS may stagnate for 3-4 years, which does not warrant a comparatively excessive a number of of 25-30 occasions projected EPS.

Nonetheless, Apple continues to have a excessive valuation, which can proceed to say no as a number of compressions happen. $6 in EPS implies that Apple trades round 29 occasions the ahead P/E a number of, a really excessive valuation for an organization in Apple’s place.

Due to this fact, we may even see additional a number of compression and a decrease inventory worth for Apple within the close to time period, and the market might revalue Apple as a “standard” worth inventory as we advance. With EPS of round $6-7 and a P/E a number of of 18-20, Apple’s “fair value” could also be round $110-$140. Thus, Apple stays a maintain for me, with an preliminary buy-in goal under $150.