Magdalena Wygralak

Lately, I had success investing in Carrols Restaurant Group, Inc. (NASDAQ:TAST), a number one franchisee of Burger King and Popeye’s eating places. In my October article, I famous TAST was attractively valued at simply $1.4 million per restaurant s. substitute price of $1.8 million.

Not lengthy after my article, Carrols introduced it was being acquired by Restaurant Manufacturers Worldwide (QSR), the mother or father firm of Burger King. The transaction worth was $1 billion in enterprise worth, or $1.7 million / restaurant, a good value in my view.

Recent off my TAST-y success, I actively sought out different restaurant firms that could be equally undervalued and got here throughout Arcos Dorados Holdings Inc. (NYSE:ARCO).

Arcos Dorados is the biggest franchisee within the McDonald’s system working and sub-franchising over 2,300 eating places. Its capability to sub-franchise eating places to unbiased entrepreneurs have allowed the corporate to generate superior revenue margins in comparison with Carrols.

Nevertheless, valuing the corporate utilizing a sum-of-the-parts evaluation, I consider ARCO is correctly valued by the market at $3.9 billion enterprise worth. I price ARCO a maintain pending a drop in its valuation or an acceleration of its sub-franchising efforts.

Firm Overview

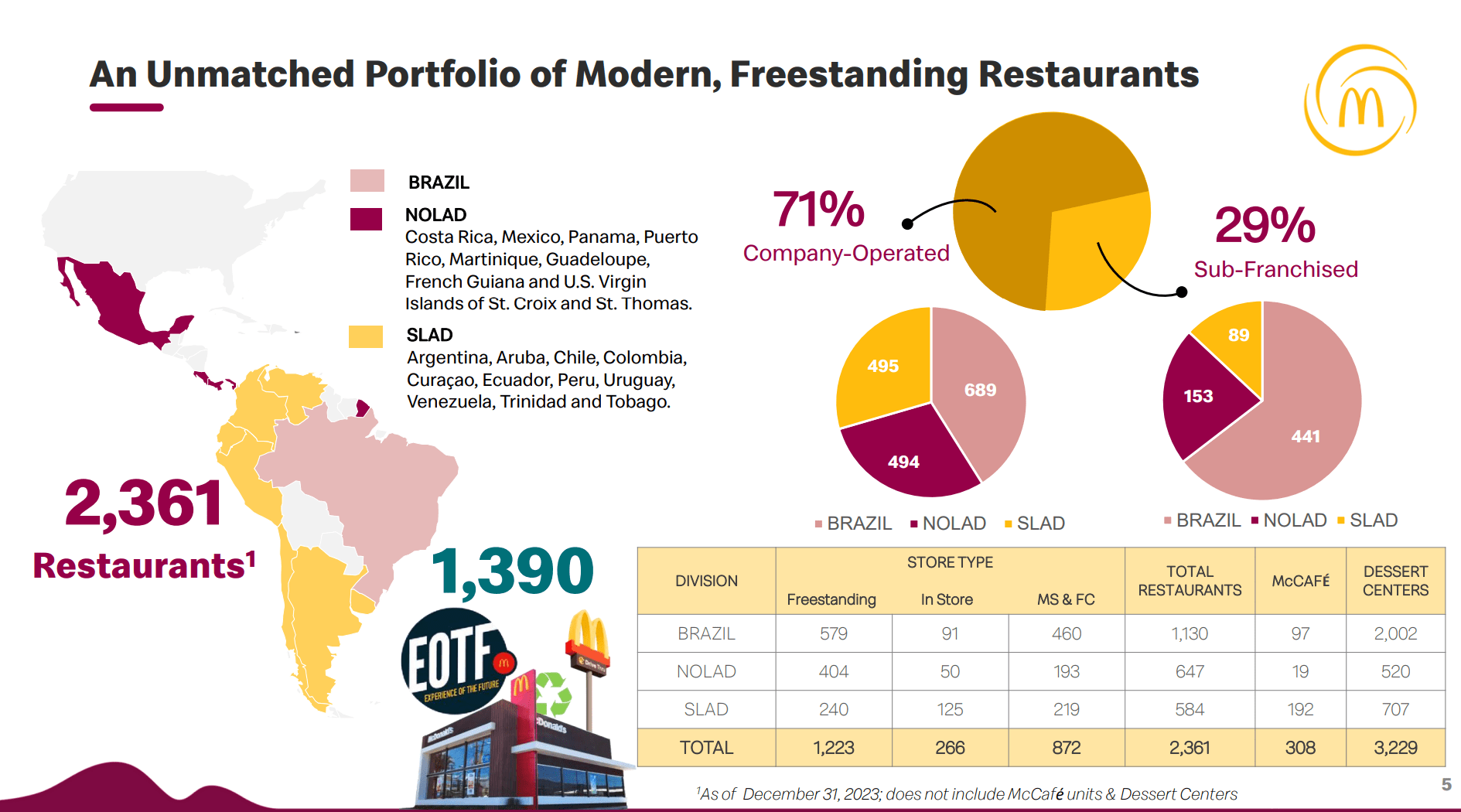

Arcos Dorados Holdings Inc. is the biggest fast service restaurant (“QSR”) operator in Latin America and the Caribbean and is the biggest unbiased franchisee within the McDonald’s restaurant system, producing over 4% of McDonald’s world gross sales. ARCO operates over 2,300 eating places immediately or by means of sub-franchise agreements in Brazil, Costa Rica, Mexico, and different South American nations (Determine 1).

Determine 1 – ARCO overview (ARCO investor presentation)

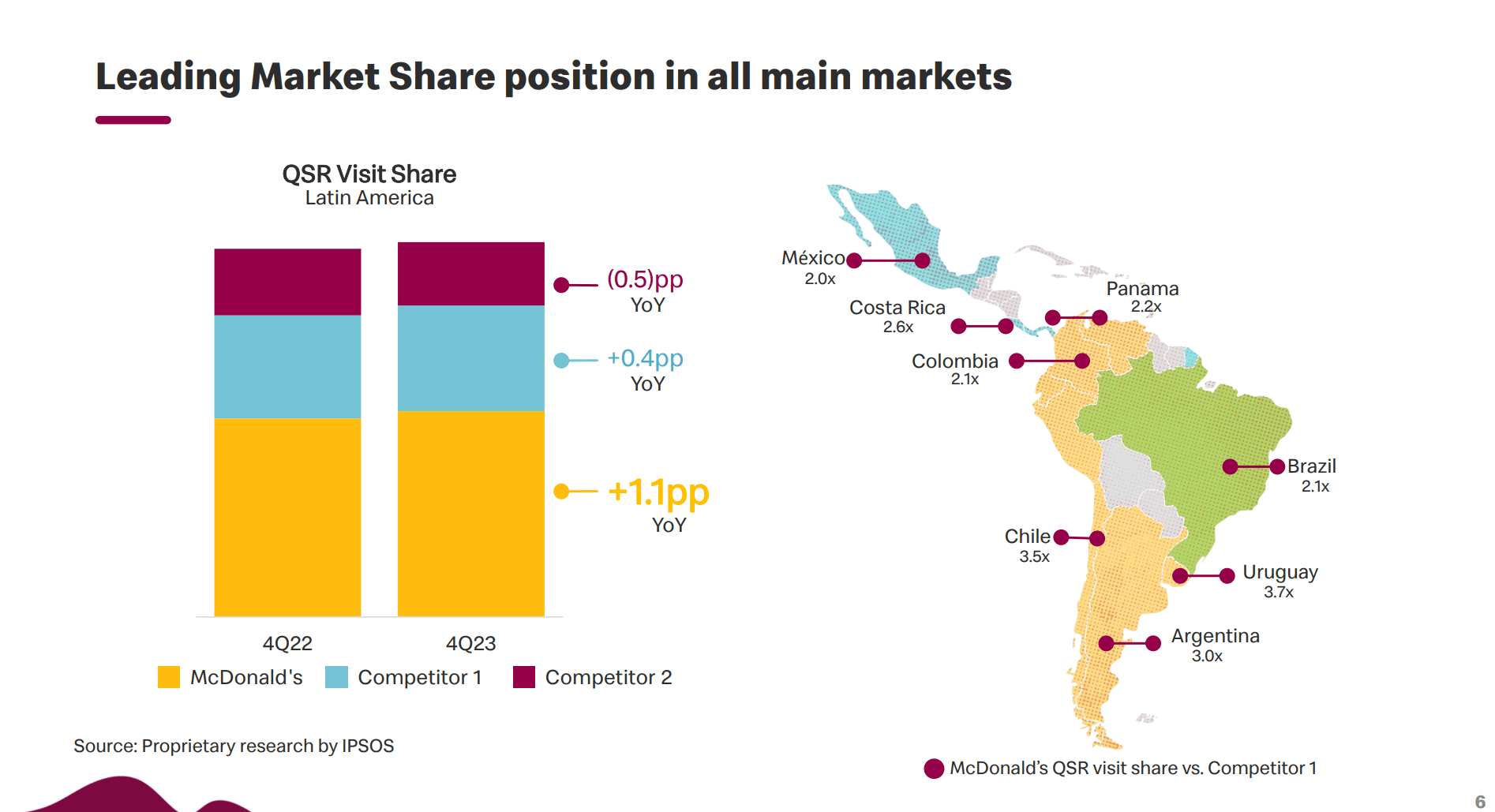

McDonald’s (MCD) is a number one world QSR restaurant model and instructions a number one market share place inside all of ARCO’s principal markets (Determine 2).

Determine 2 – McDonald’s is a number one QSR model (ARCO investor presentation)

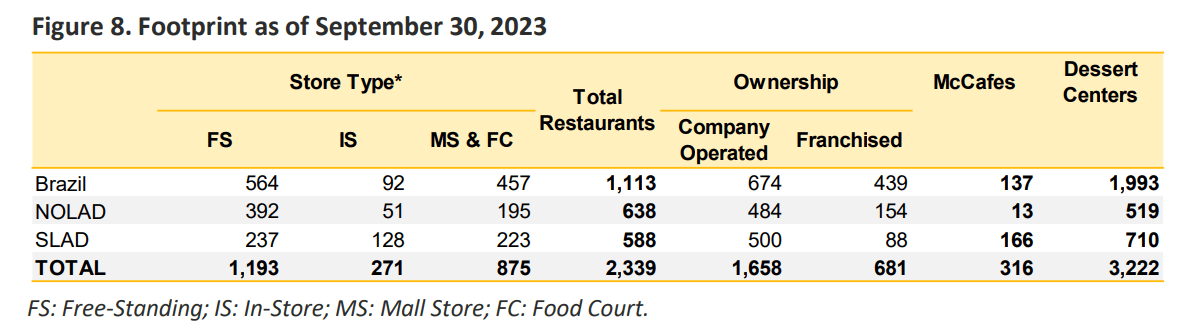

In whole, ARCO’s operated 1,658 eating places throughout Latin America and sub-franchised 681 eating places as of September 30, 2023. It additionally derived revenues from 316 McCafes and over 3,000 dessert facilities (Determine 3).

Determine 3 – ARCO restaurant depend (ARCO monetary studies)

ARCO Is Extra Worthwhile Than TAST

Traditionally, proudly owning a franchise restaurant has been a well-trodden path to wealth for the middle-class. Within the U.S., in keeping with the Franchise Business Review, the typical restaurant franchisee makes income of $120,000 per yr for companies which were open for greater than 2 years.

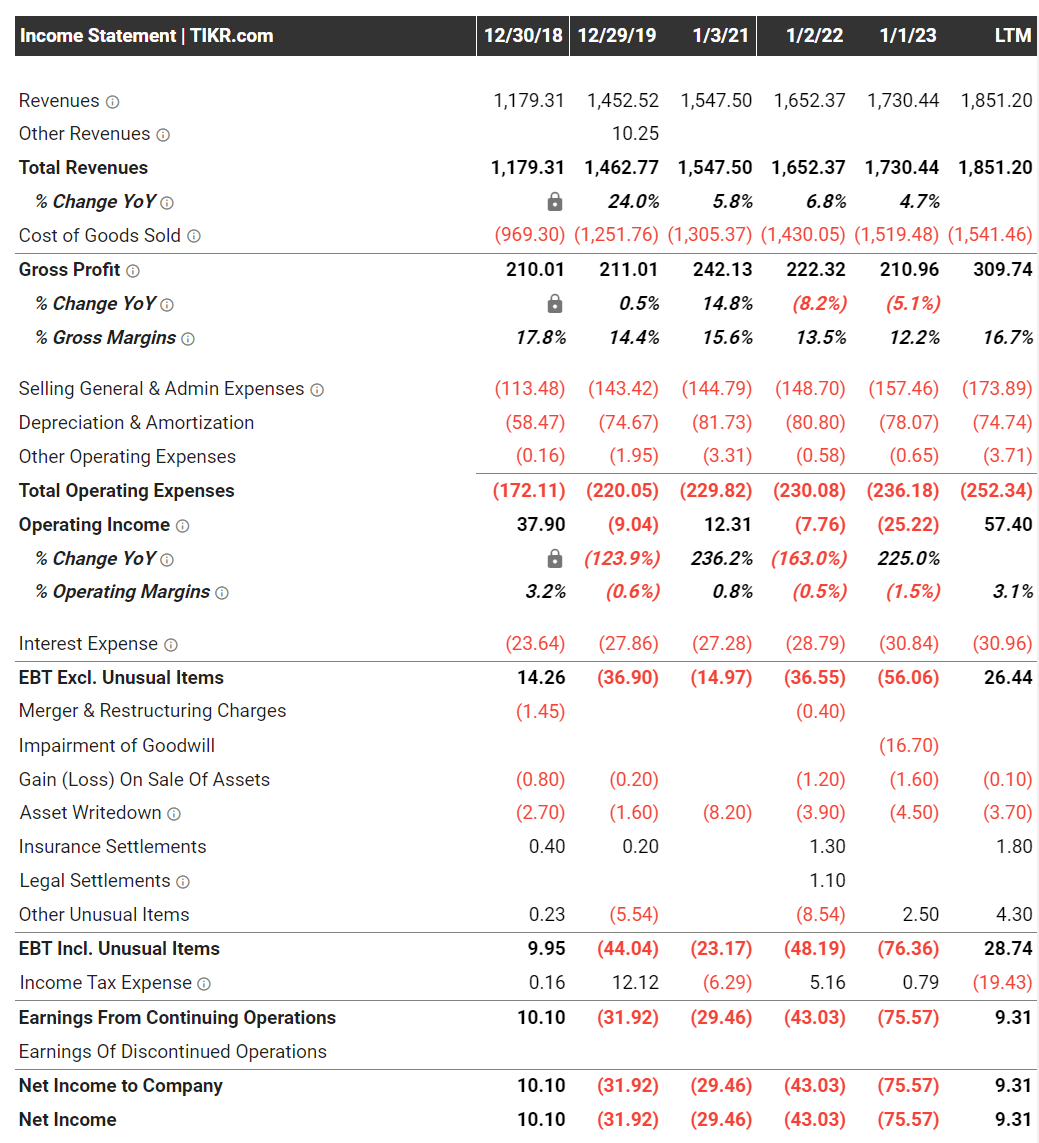

Nevertheless, whereas particular person franchisees could make very important income, outcomes from publicly traded franchisees of QSR manufacturers like Carrols Restaurant Group have typically been disappointing, as there are important dis-economies of scale. For instance, TAST has reported years of low or detrimental earnings regardless of proudly owning over 1,000 Burger King and Popeye’s eating places (Determine 4).

Determine 4 – TAST monetary abstract (tikr.com)

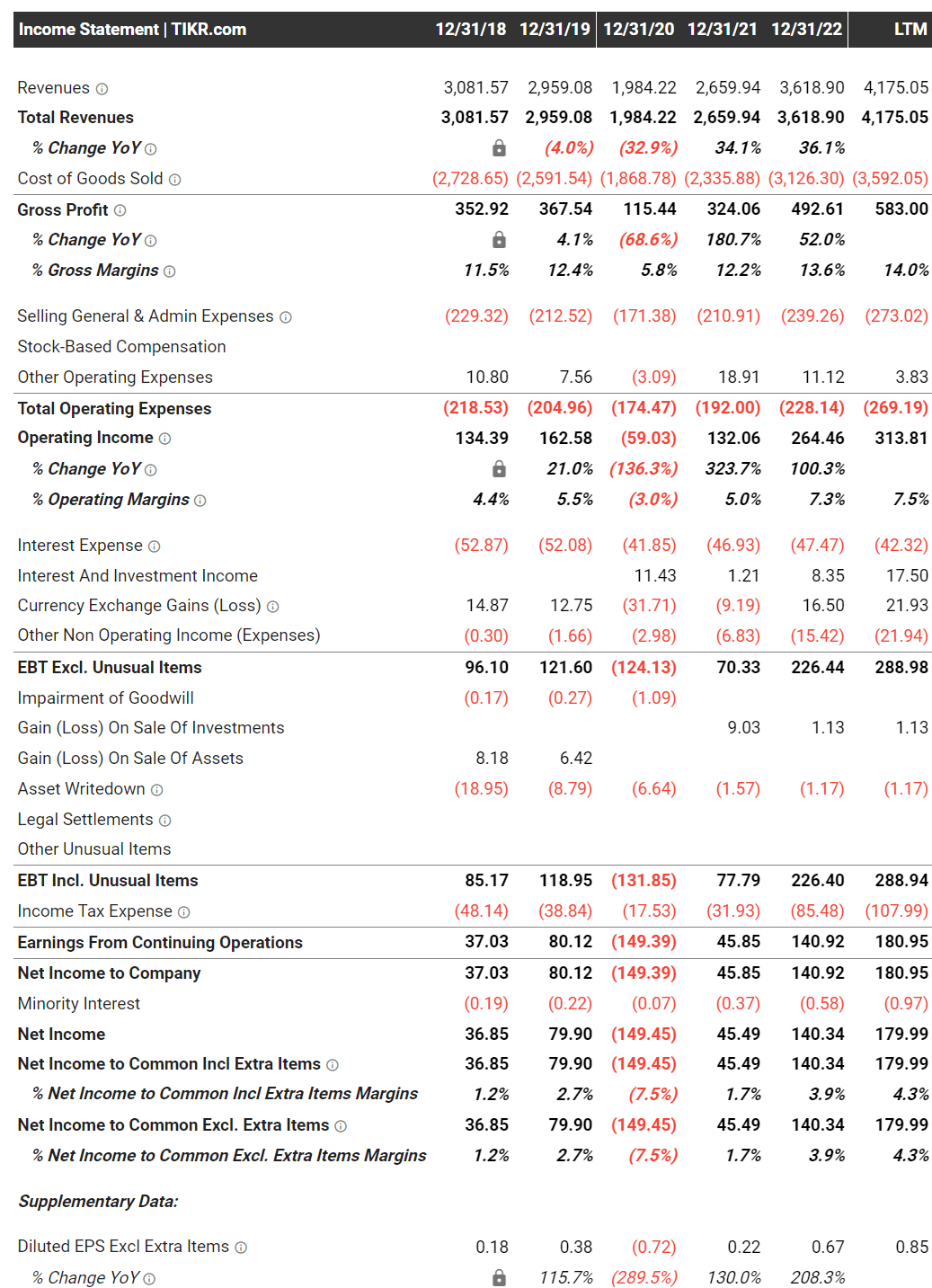

Fortuitously, ARCO isn’t any TAST, as the corporate has been producing sturdy income yearly, apart from 2020, when the COVID pandemic negatively impacted outcomes (Determine 5).

Determine 5 – ARCO monetary abstract (tikr.com)

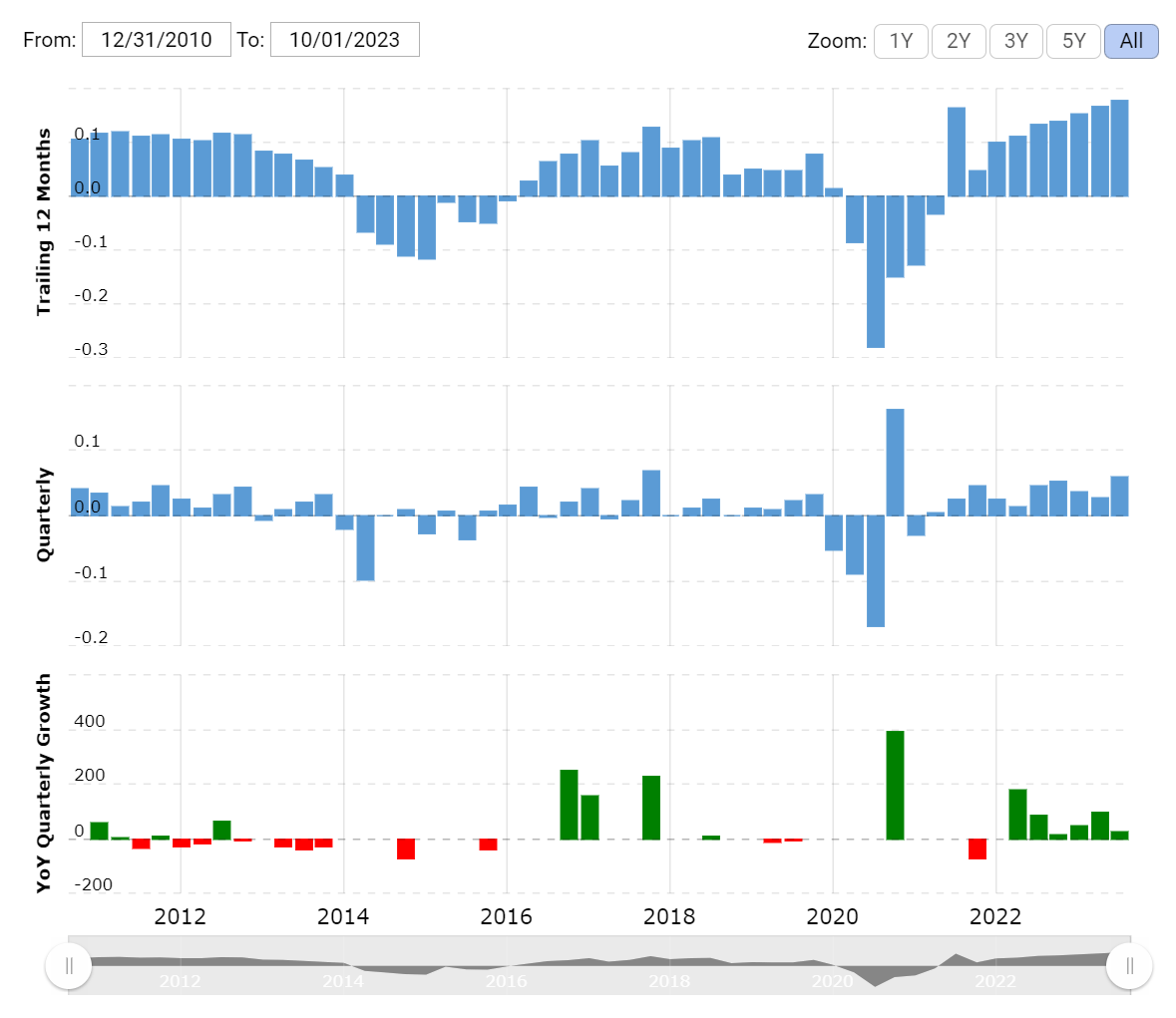

The truth is, ARCO has been persistently worthwhile and the corporate’s LTM internet income of $180 million is the very best in its historical past (Determine 6).

Determine 6 – ARCO generated $180 million in LTM internet income (macrotrends.internet)

Sub-Franchising Is the Key Differentiator

What’s the key differentiator permitting Arcos Dorados to generate $180 million in trailing 12 month internet income in comparison with nearly nothing for Carrols?

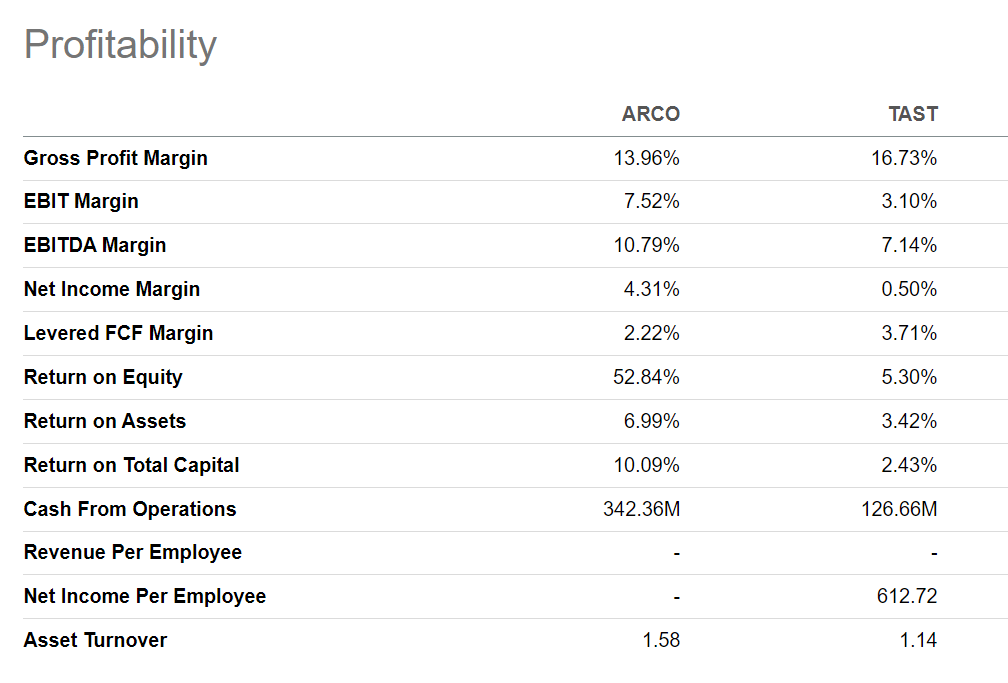

Evaluating ARCO and TAST’s profitability, we will see that ARCO truly has a decrease gross margin of 14.0% in comparison with 16.7% for TAST (Determine 7). So ARCO’s working atmosphere is definitely harder than TAST’s.

Determine 7 – ARCO vs. TAST profitability (In search of Alpha)

Nevertheless, once we transfer all the way down to the EBIT and EBITDA margin line, we see that ARCO’s outcomes are considerably higher than TAST.

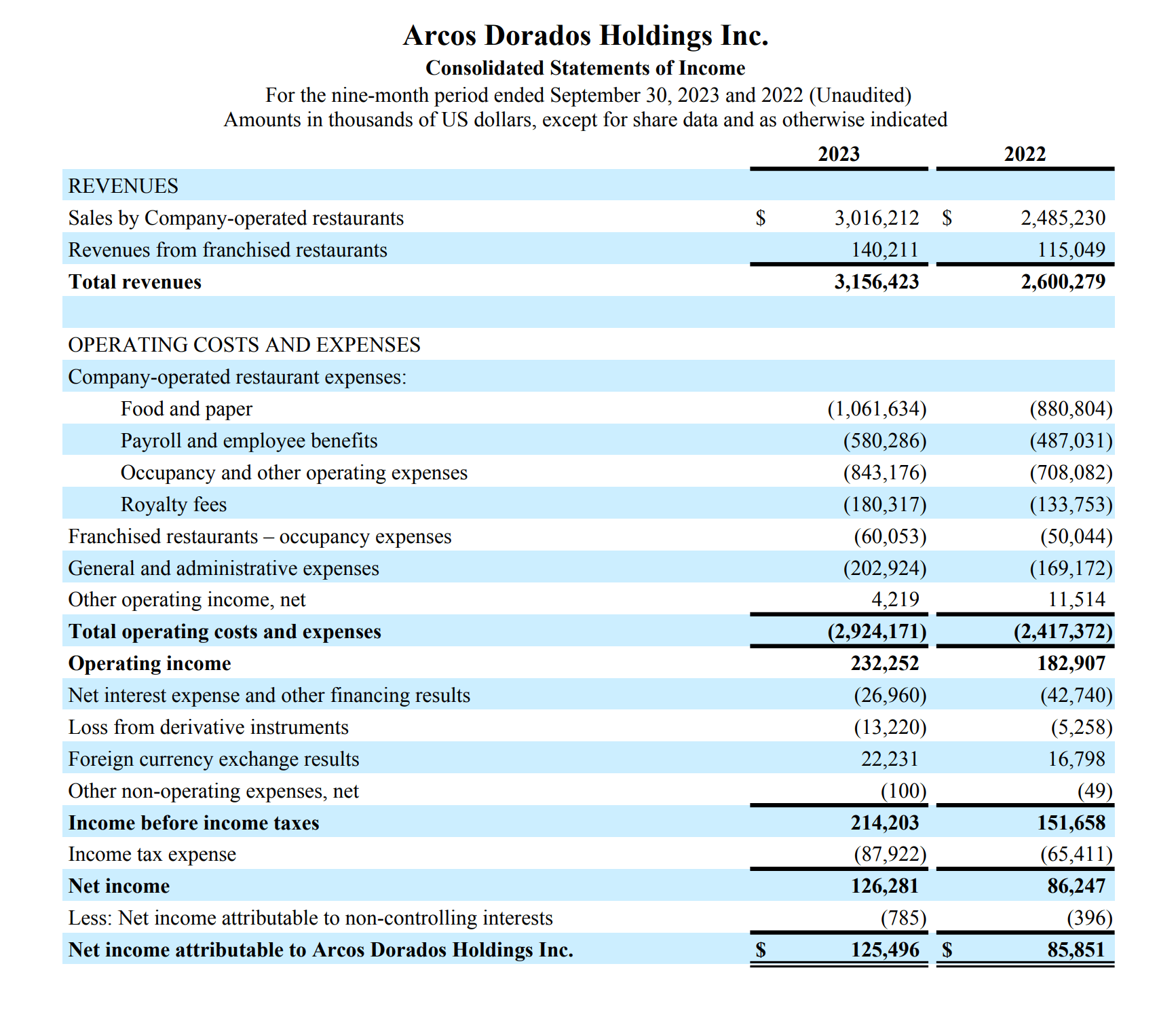

In my view, the important thing distinction between ARCO and TAST is ARCO’s capability to sub-franchise shops to unbiased entrepreneurs. For instance, taking a look at ARCO’s monetary statements for the 9 months to September 30, 2023, we will see that ARCO generated $140.2 million in franchised revenues whereas paying $60.1 million in franchised restaurant hire bills (Determine 8). This interprets into $80.1 million in internet franchise revenues or 34% of the corporate’s working revenue.

Determine 8 – ARCO monetary statements, YTD September 2023 (ARCO monetary studies)

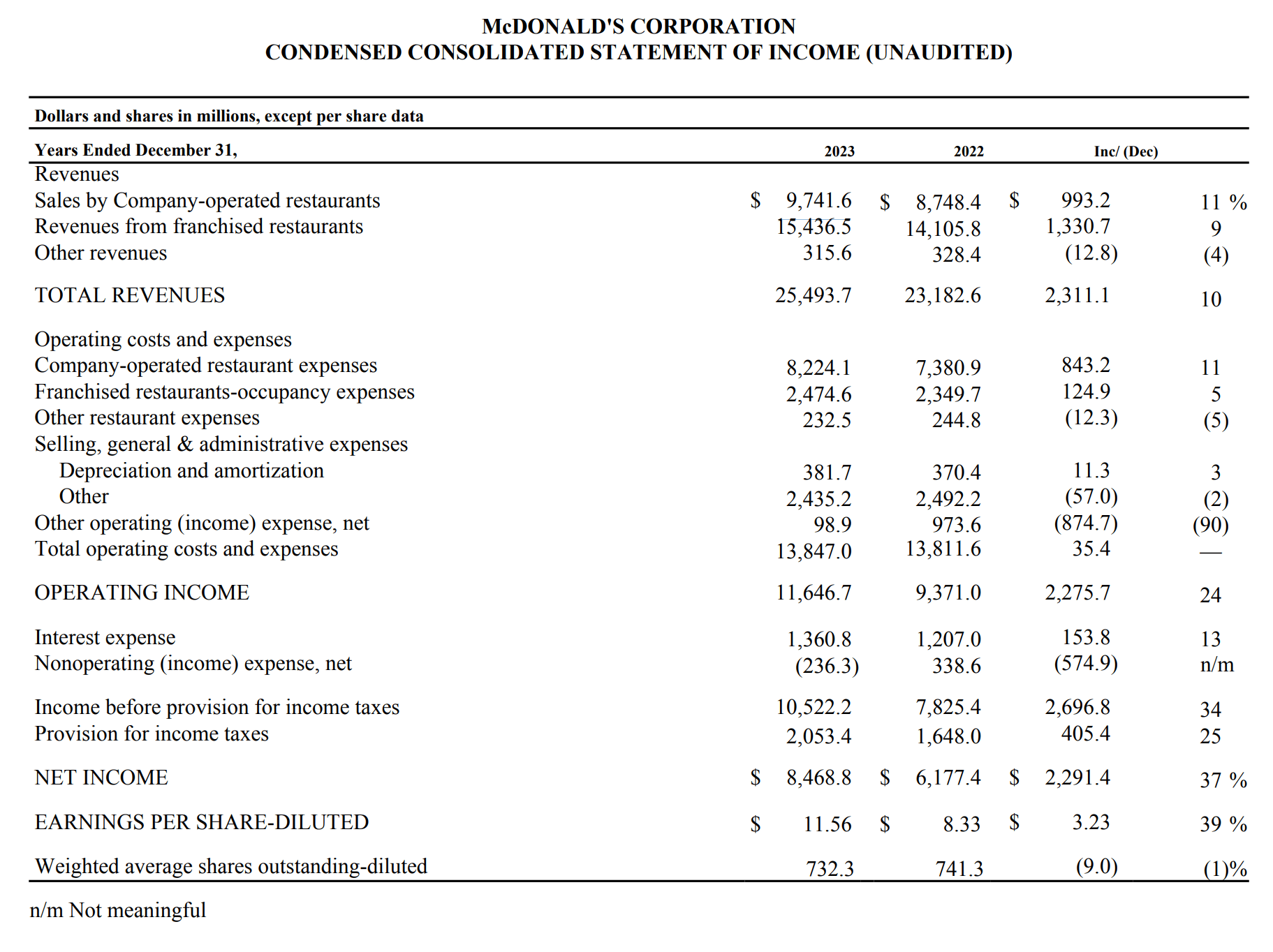

That is taking a web page out of McDonald’s playbook, because the overwhelming majority of McDonald’s working income are additionally generated from internet franchise revenues (Determine 9). “According to industry analysts, McDonald’s keeps about 82% of the profit generated by franchisees, compared with only about 16% from its company-operated locations, further trimmed by the costs incurred in operating these units”.

Determine 9 – MCD monetary statements, 2023 (MCD monetary studies)

Valuing ARCO As Sum-Of-The-Elements

So a technique to consider ARCO is as a mini-McDonald’s. McDonald’s generated $13.0 billion in internet franchise revenues in 2023, or $340k per franchisee (McDonald’s has over 40,000 eating places in its community on the finish of 2022 and 95% are franchised).

As compared, ARCO has 681 franchised eating places producing $108 million in LTM internet franchise revenues to September 30, 2023 or ~$160k per sub-franchisee.

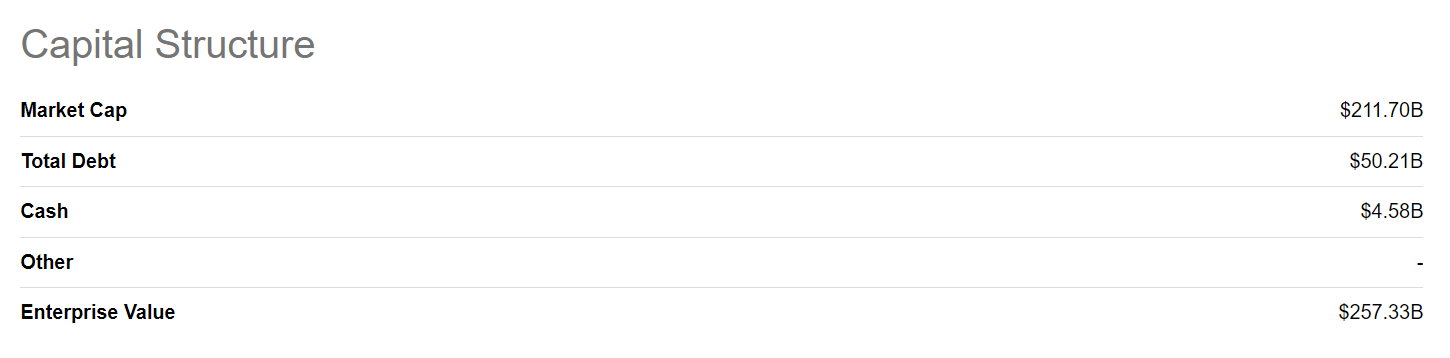

If we settle for the premise that a lot of MCD’s enterprise worth is derived from the corporate’s franchising mannequin and never working eating places, MCD has $257 billion in enterprise worth for ~38,000 franchised eating places or roughly $6.7 million per franchised restaurant (Determine 10). That is roughly a 20x a number of on the web franchise charge of $340k per restaurant.

Determine 10 – MCD enterprise worth (In search of Alpha)

Utilizing an analogous metric, we will worth ARCO’s sub-franchise worth as 20x its internet franchise charges or $2.2 billion ($160k per restaurant x 20 x 681 eating places).

ARCO’s operated eating places are additionally extremely worthwhile and deserve worth. Within the trailing twelve months, ARCO’s operated eating places generated $205 million in working income or $121 million after tax (ARCO has an efficient tax price of ~41%). Since working eating places is extra risky and decrease margin, this money movement stream ought to be valued at a decrease a number of in comparison with franchise charges.

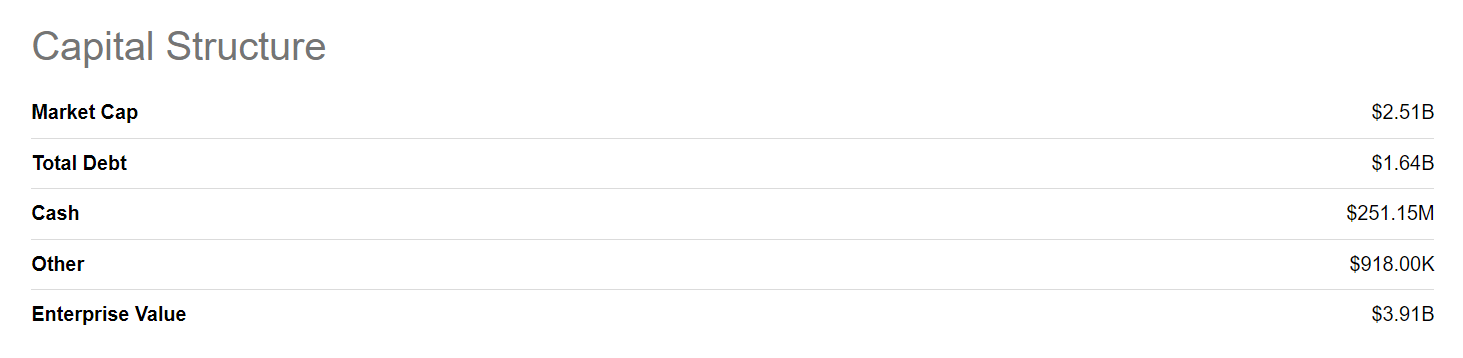

If we assign a 15x a number of to this earnings stream, ARCO’s operated eating places are price $1.8 billion. So your complete firm is price $4.0 billion utilizing a sum-of-the-parts valuation. This compares to ARCO’s present enterprise worth of $3.9 billion (Determine 11).

Determine 11 – ARCO enterprise worth (In search of Alpha)

Primarily based on this sum-of-the elements evaluation, ARCO appears pretty valued in the meanwhile.

Dangers To ARCO

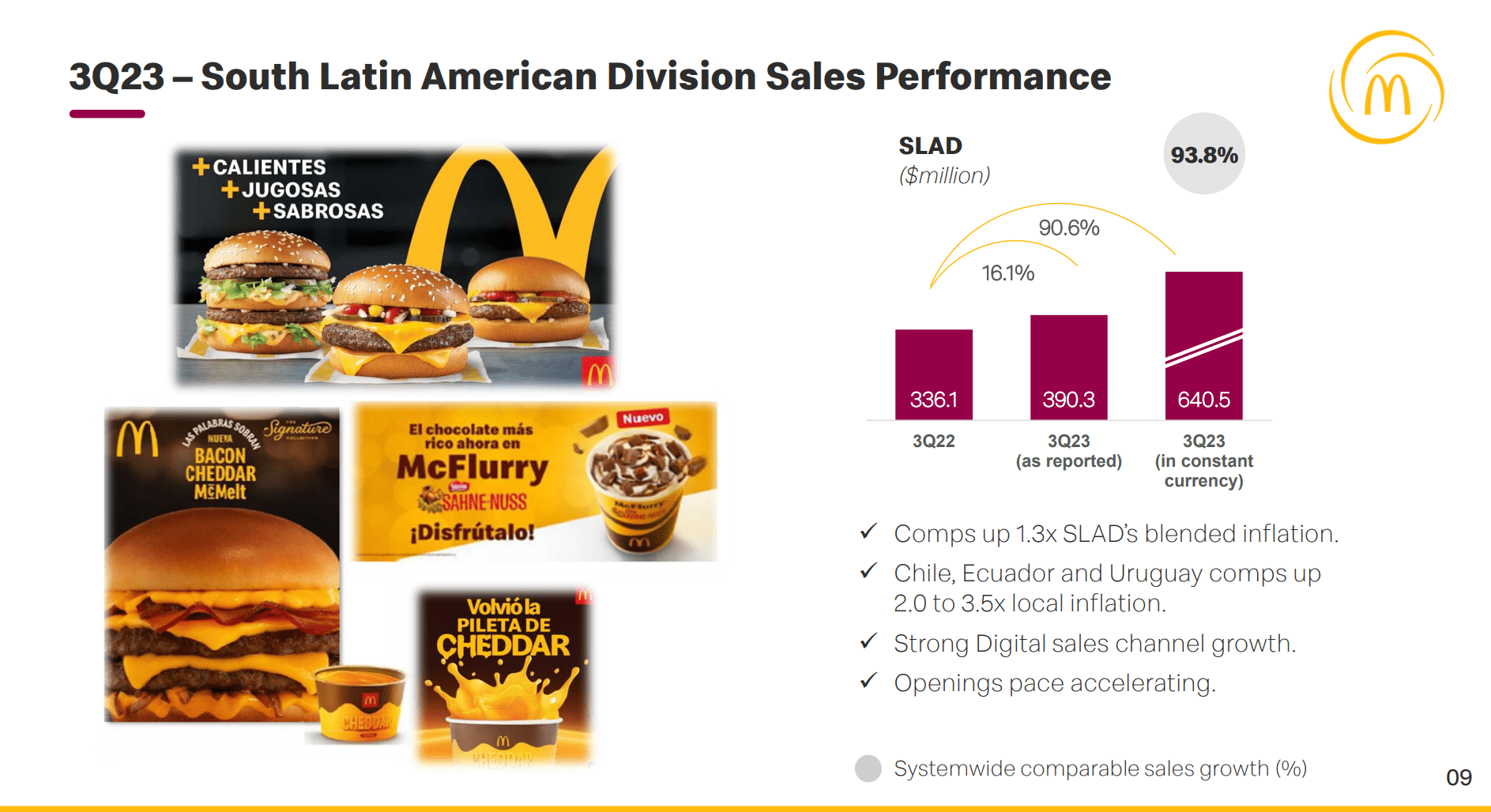

On the upside, ARCO has seen distinctive comparable gross sales development, particularly in its South Latin American Division (“SLAD”) the place comp gross sales had been up 93.8% YoY in Q3/23 (Determine 12). This distinctive efficiency was attributable to sturdy digital gross sales development along with restaurant openings and value will increase.

Determine 12 – SLAD has been star performer for ARCO (ARCO investor presentation)

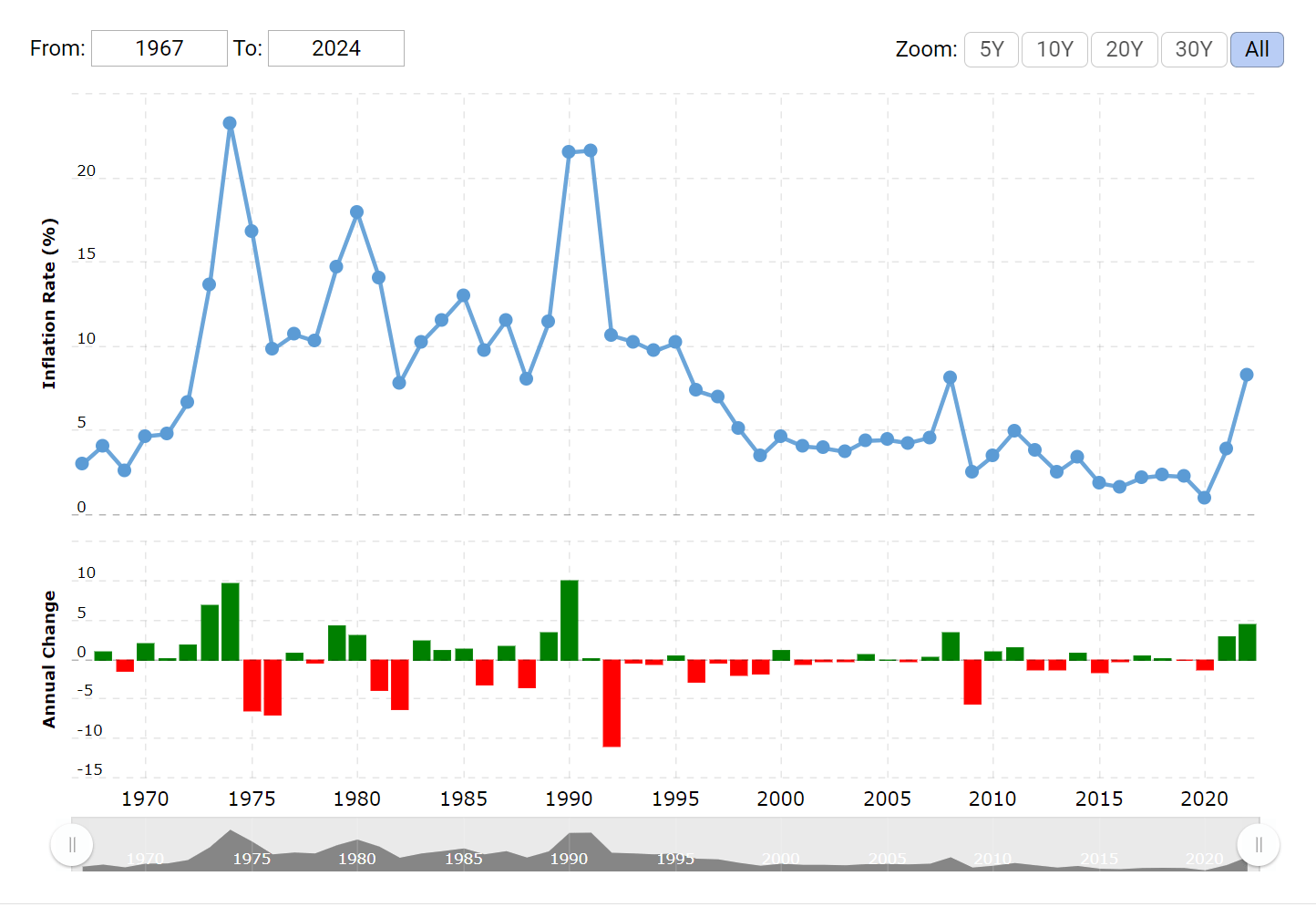

Usually, Latin American nations have traditionally confronted greater inflation charges (Determine 13), so shoppers there might not be as delicate as American shoppers, who’ve been revolting towards value will increase at McDonald’s.

Determine 13 – Latin American inflation has traditionally been excessive (macrotrends.internet)

So whereas gross sales development could decelerate for North American restaurant chains as they can’t take as a lot value will increase, Latin American eating places like ARCO could proceed to profit from value will increase.

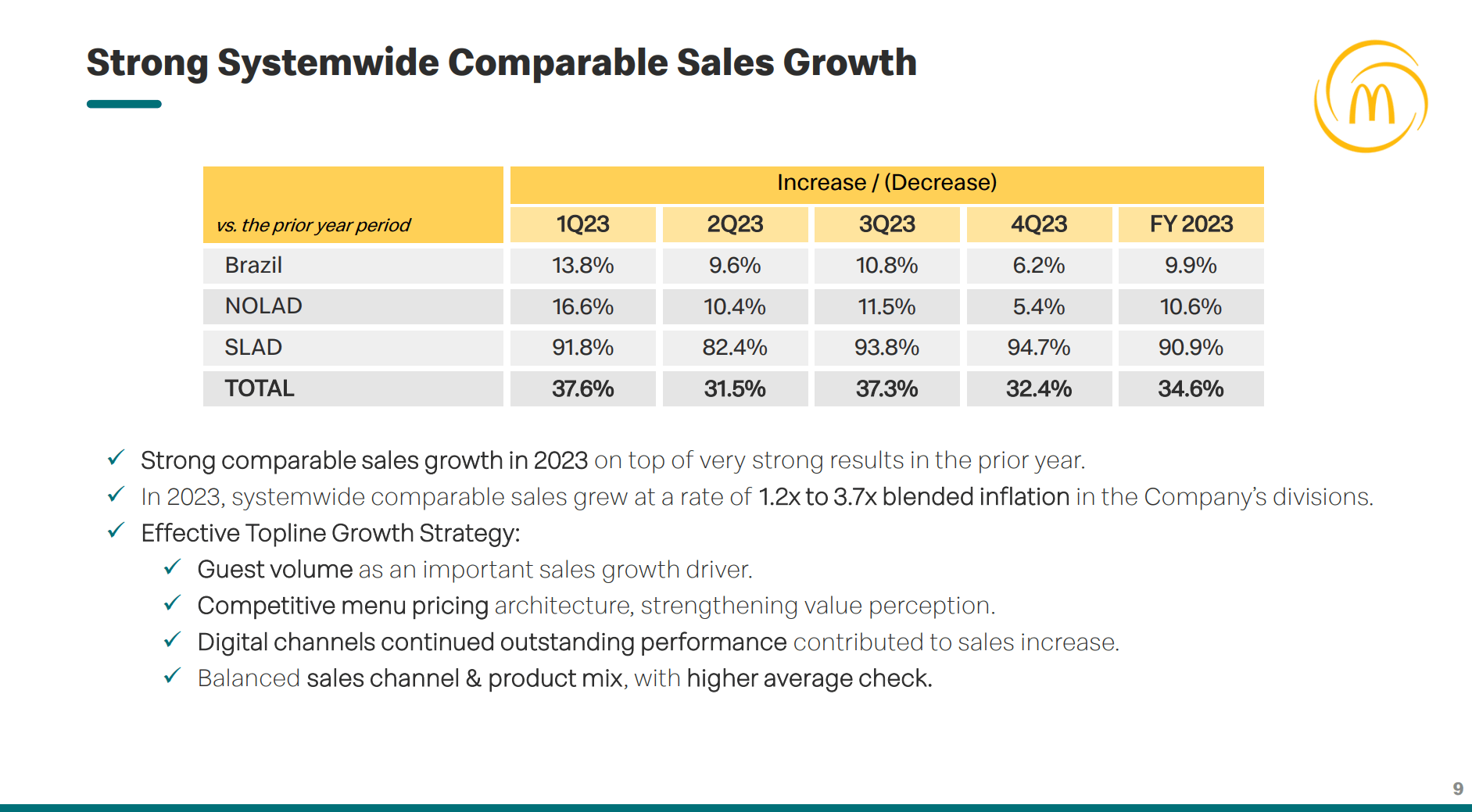

On the flipside, shoppers are usually poorer in Latin American nations, so if Arcos Dorados maintain growing its menu costs, the corporate could threat alienating clients and negatively impacting gross sales. Moreover, many elements of the world have been slipping into recession. If recession strike Latin American nations, Arcos Dorados may see its gross sales endure. Up to now, comp gross sales have been sturdy, however buyers ought to intently monitor quarterly outcomes to positive this doesn’t grow to be a difficulty (Determine 14).

Determine 14 – ARCO comp gross sales have been sturdy (ARCO investor presentation)

Conclusion

Arcos Dorados is a number one Latin American franchisee of McDonald’s eating places. It operates and sub-franchises over 2,300 eating places, contributing over 4% to McDonald’s worldwide gross sales.

Taking a look at ARCO’s monetary efficiency, I consider the important thing differentiator between ARCO and different franchisee firms like Carrols is ARCO’s capability to sub-franchise eating places in its geographical areas. This has allowed ARCO to earn engaging net-franchise charges, similar to McDonald’s.

Valuing ARCO’s enterprise utilizing a sum-of-the-parts evaluation between franchised and operated eating places, I consider ARCO’s share are at present pretty valued. I price the corporate a maintain for now.