Chip Somodevilla

Ares Capital is a BDC Market Chief

Ares Capital (NASDAQ:ARCC) is without doubt one of the market’s main enterprise growth firms or BDC. It has a well-diversified portfolio in direct lending and a comparatively small publicity in fairness investments. Ares Capital’s portfolio contains principally floating-rate securities, accounting for 69% of its portfolio truthful worth. Therefore, the BDC has capitalized on the fast rate of interest hikes to drive its core EPS.

As well as, Ares Capital’s higher “defensive” publicity in software program and healthcare helps the corporate keep away from the cyclical uncertainties linked to industries reminiscent of oil and gasoline, accommodations, and gaming. In consequence, Ares Capital believes that the portfolio development helps the BDC to “mitigate risks associated with economic downturns.”

Moreover, its affiliation with main various asset supervisor Ares Administration Company (ARES) offers a wealth of sourcing and funding experience, sharpening its aggressive edge towards its smaller friends. With a market cap of $12.13B, Ares Capital has vital scale and advantages from the “incumbency” benefit with its portfolio firms. In consequence, the corporate highlighted that about “50% of new commitments are directed towards the existing portfolio.”

Regardless of that, ARCC has underperformed the S&P 500 (SP500) since I downgraded ARCC to a Maintain in early January 2024. I argued that buyers should brace for affect as Ares Capital’s core earnings have possible peaked. With the Fed more and more prone to execute three fee cuts in 2024, I imagine the extra cautious shopping for sentiment resulting in ARCC’s latest underperformance is justified.

Ares Capital administration articulated in a latest convention that originations in 2024 haven’t met its preliminary expectations. The direct lending house can be more and more aggressive as banks discover one other progress vector as they emerge from their hammering in 2023. Regardless of that, Ares Capital’s market-leading positions and strong incumbency ought to place the BDC effectively, as charges are nonetheless anticipated to remain higher for longer.

In consequence, even with expectations of decrease rates of interest in 2024, Ares Capital has confidence that deal exercise ought to speed up later this yr as improved fee stability returns to the market. Bolstered by the necessity for private equity to return/recycle capital for his or her LPs, a probably improved M&A traction ought to assist propel a extra strong deal-making stream, lifting Ares Capital’s direct-lending prospects.

ARCC’s Valuation Dislocation Has Normalized

However the optimism surrounding Ares Capital’s market-leading capabilities, it is important to not throw warning to the wind. With ARCC valued at a ahead dividend yield of 9.7%, its valuation dislocation has largely normalized to its 10Y common of 9.6%. There are additionally issues about poorer recovery prospects from defaulted loans in non-public credit score, additional hampered by decrease ranges of transparency in comparison with syndicated loans.

In consequence, I imagine the market will proceed to low cost the valuations of BDCs like ARCC to account for such execution dangers. Regardless of my warning, ARCC stays solidly positioned in a medium-term uptrend, suggesting the market is not unduly frightened about such dangers impacting its deal stream and core earnings potential.

Is ARCC Inventory A Purchase, Promote, Or Maintain?

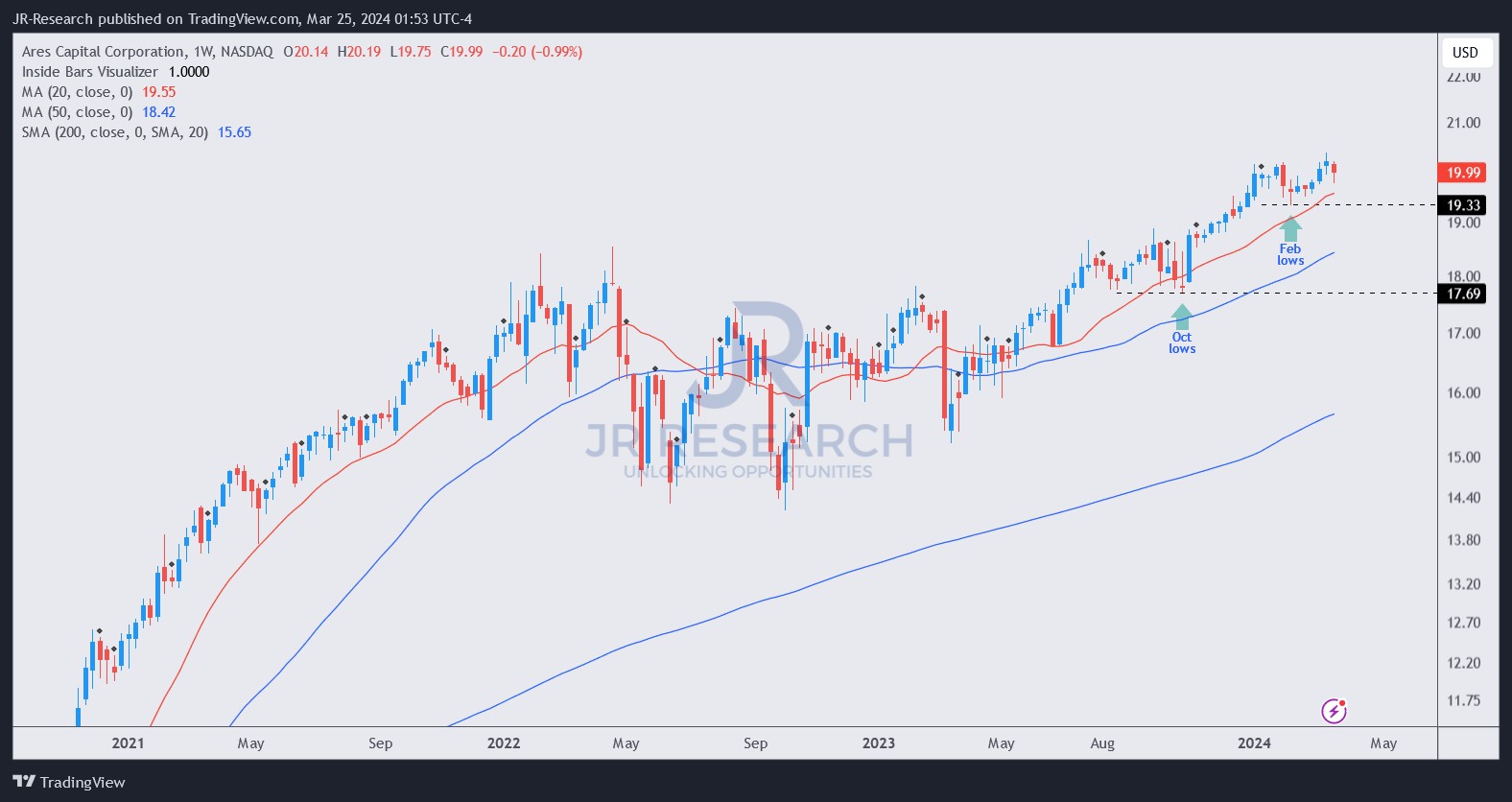

ARCC value chart (weekly, medium-term, adjusted for dividends) (TradingView)

As seen above, ARCC’s uptrend bias stays extremely strong. In consequence, previous pullbacks over the previous yr attracted dip-buyers so as to add publicity, leveraging ARCC’s enticing dividend yields.

ARCC’s “A” valuation and profitability grade ought to bolster the market’s confidence in its enterprise mannequin and market management within the BDC sphere. In consequence, I’ve not assessed causes to be frightened about ARCC’s value motion, suggesting it could be well timed for buyers to reload publicity following its latest pullback and underperformance.

Score: Improve to Purchase.

Vital word: Buyers are reminded to do their due diligence and never depend on the knowledge offered as monetary recommendation. Please at all times apply impartial pondering. Observe that the score will not be supposed to time a selected entry/exit on the level of writing except in any other case specified.

I Need To Hear From You

Have constructive commentary to enhance our thesis? Noticed a important hole in our view? Noticed one thing vital that we did not? Agree or disagree? Remark beneath with the goal of serving to everybody in the neighborhood to be taught higher!