PM Pictures

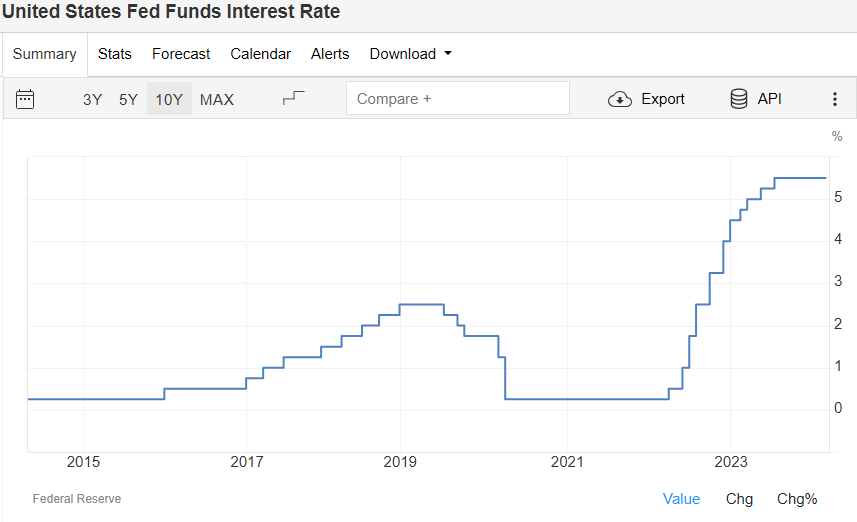

One of many large questions is what is going to occur to enterprise improvement firms (BDC) when the Fed begins its rate-cutting cycle. BDCs have turn into more and more common in the course of the rate-hiking cycle as they generate bigger returns for his or her shareholders and better yields from their distributed earnings in comparison with risk-free property. I feel lots of the common BDCs will do effectively in a lower-rate atmosphere, particularly Ares Capital (NASDAQ:ARCC), usually referred to as the gold normal within the BDC realm. Rates stay at multi-decade highs, and the reducing cycle is not anticipated to achieve 3% till after 2026 is completed. I do not assume now could be the time to desert high quality BDCs, particularly ARCC. Traditionally, ARCC has maintained a big dividend all through completely different charge environments, and I consider {that a} charge atmosphere that slowly declines could possibly be helpful for ARCC as the price of capital decreases and the chance to develop turns into extra engaging for decrease and center market corporations. I feel top-tier BDCs will stay sturdy earnings investments and will see an inflow of traders as capital flows again into the markets from the sidelines. ARCC might not be nearly as good of a purchase right this moment because it was final yr, however I’m nonetheless bullish on ARCC as an earnings funding and sit up for reinvesting the dividends and rising my place in 2024.

In search of Alpha

Following up on my earlier article about ARCC

I’ve been bullish on ARCC for a while and gave ARCC a really bullish ranking in my final article, which was revealed on 10/22/23 (can be read here). Since then, shares of ARCC have appreciated by 7.01%, and when the dividend is factored in, the whole return is 12.21%. ARCC has trailed the S&P 500 returns of 24.32%, nevertheless it’s not in competitors with the market. In that article, I mentioned why I used to be a purchaser going into Q3 earnings and why I believed ARCC may proceed to profit from the present state of rates of interest. I’m following up on this funding thought as a major quantity of macroeconomic information has been launched, and now we have a clearer image of the place charges can be going sooner or later. I’ll have a look at how ARCC completed the 2023 fiscal yr and provides my opinion on why I’m bullish on ARCC getting into right into a declining charge atmosphere.

In search of Alpha

Dangers to my funding thesis on ARCC

ARCC will both stay a powerful funding or deteriorate based mostly on its underwriting skill. The largest danger to the funding thesis with ARCC is not when charges will decline or how rapidly they’ll fall, it is whether or not their investments maintain up. As a BDC, ARCC takes an fairness stake in corporations or lends capital to corporations within the decrease and center markets within the type of several types of debt. If the businesses ARCC underwrites loans to or takes an fairness stake endure sudden losses or a shift within the enterprise atmosphere happens, inflicting them to not carry out as anticipated, ARCC could possibly be severely impacted. The flexibility to make curiosity funds and pay again their loans comes into query, and the fairness turns into much less priceless than what they’ve acquired. ARCC is simply as sturdy as the businesses it is doing enterprise with and the way effectively its underwriting crew can mannequin the long run panorama. If we head right into a recession that finally ends up being prolonged for a time frame, the businesses that ARCC is doing enterprise with are extra in danger than massive caps, and this might affect ARCC’s returns. Investing in ARCC may generate capital appreciation and huge dividend yields, however there are vital dangers as a result of the general financial system is unpredictable, and a number of belief is being positioned on ARCC’s crew to enter into sturdy offers that may mitigate downturns in the event that they happen.

ARCC completed 2024 sturdy and I consider it might proceed its monetary power in a declining charge atmosphere

2023 ended up being ARCC’s strongest yr over the previous decade. ARCC generated $2.61 billion in income and after its working bills have been factored in, its working revenue was $1.87 billion. The underside-line revenue for ARCC after curiosity bills and taxes amounted to $1.52 billion in internet earnings. ARCC operated at a 71.46% working margin and a 58.23% revenue margin for his or her 2023 fiscal yr. ARCC grew its income by 24.71% YoY, whereas its working earnings grew by 16.6% YoY. 2024 marked the threerd consecutive yr of top-line development because it continued to drive its metrics increased. On a per-share foundation, ARCC delivered $0.72 per share of GAAP internet earnings in This autumn of 2023. Its core EPS grew to $0.63 per share from $0.59 per share in Q3 2023. On an annualized foundation, ARCC generated $2.37 in core EPS for the 2023 fiscal yr, which was a rise of $0.35 (17.33%) YoY, whereas its internet asset worth (NAV) elevated from $18.40 to $19.24.

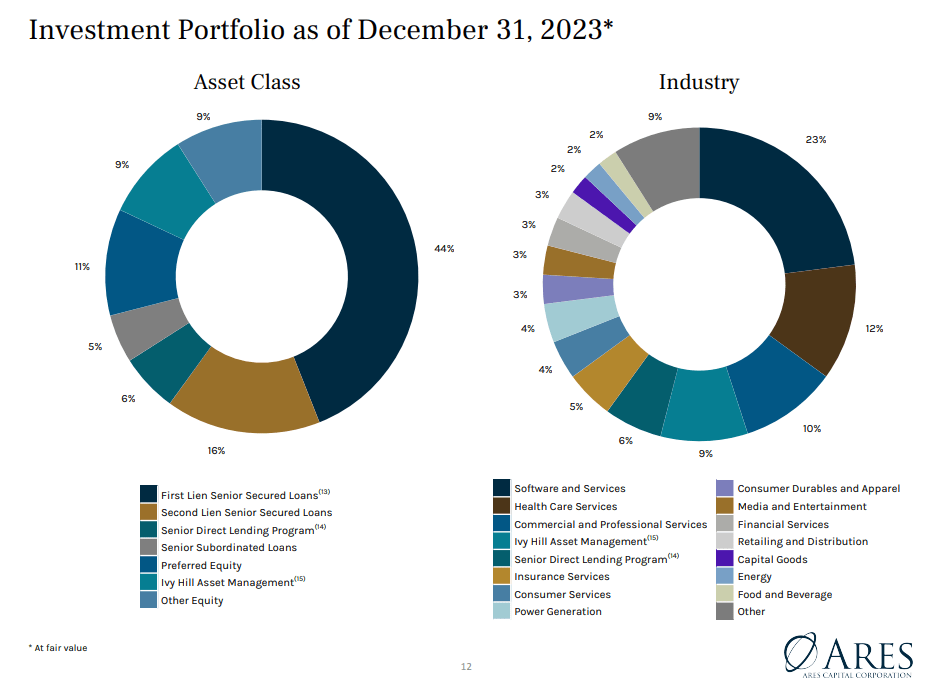

In 2023, ARCC’s portfolio grew to 505 debtors, which is a rise of 8% YoY and 47% over the previous 5 years. Solely 2 of their investments exceed 2% of the portfolio, and the highest 10 investments signify 12% of ARCC’s portfolio at honest worth. All through 2023, ARCC derived roughly $6 billion in new funding commitments throughout 200 transactions. In This autumn, ARCC secured $2.4 billion in funding commitments from 74 debtors, which indicated that the origination market wherein they function continues to be wholesome. ARCC collected 99% of its contractual curiosity from its underlying investments all through 2024, which is a testomony to its underwriting crew. This allowed ARCC to generate $1.27 billion in internet funding earnings (NII), and when the web realized and unrealized good points have been factored in, its internet earnings was $1.52 billion.

Ares Capital

The Fed did not begin elevating charges till Q1 of 2022, and there was virtually a 2-year interval wherein charges have been 25 bps. The Fed took charges from 25 bps to 550 bps over a yr and a half. In 2021, ARCC generated $1.82 billion in income and $1.14 billion in working earnings, coming off charges that have been principally non-existent for greater than half of 2020 and all of 2021. ARCC has 69% of its curiosity earnings tied to floating-rate debt and 12% tied to fixed-rate debt. The common yield on its debt and different income-producing securities is 12.5%. The Fed is projecting that charges will decline to roughly 460 bps in 2024, 360 bps in 2025, and 310 bps in 2026. There’s a lengthy runway for ARCC’s investments to generate massive quantities of funding earnings, and so they have been capable of challenge fixed-rate debt on the highest ranges in many years. Charges should not anticipated to fall beneath 300 bps till at the very least 2027, and ARCC will proceed to originate loans at these ranges. Sooner or later, I consider that ARCC may really do higher than their 2023 outcomes as a result of it would turn into a quantity recreation. Companies can be extra more likely to develop as the price of capital declines, and ARCC may see an inflow of originations, which may drive increased ranges of NII. The businesses that ARCC has fairness investments in might also do higher, inflicting the honest worth of ARCC’s fairness investments to extend. The Fed is not anticipated to chop charges as rapidly as they improve them, and I do not consider a charge atmosphere that’s slowly declining will negatively affect ARCC.

Buying and selling Economics

ARCC can proceed to be an earnings champion for traders

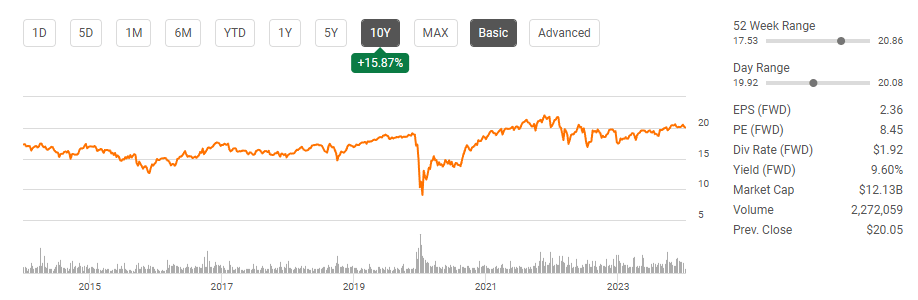

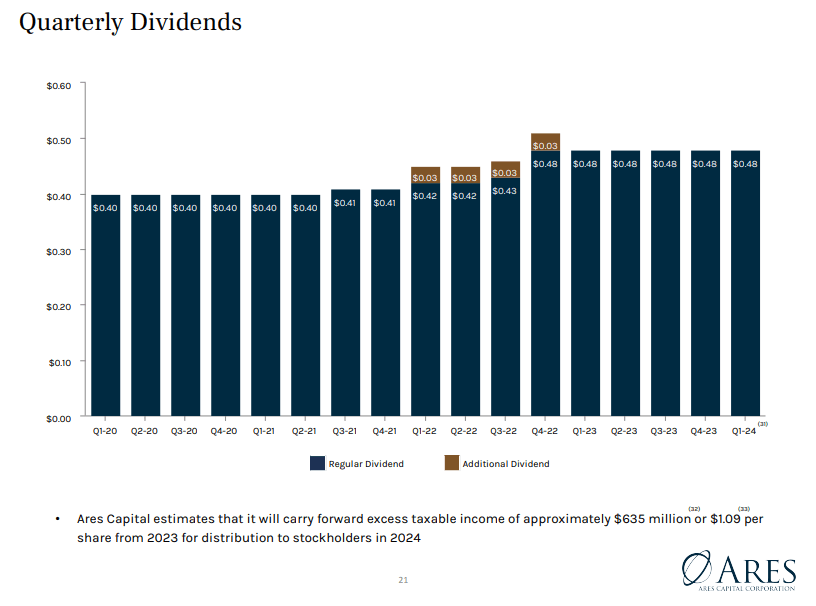

Throughout a charge atmosphere that was principally non-existent, ARCC did not slash its dividend, in reality, it elevated it. In 2021, the quarterly dividend elevated from $0.40 to $0.41, and in 2022, ARCC bumped the quarterly dividend all the way in which as much as $0.48 whereas paying particular dividends every quarter. At this time, shares of ARCC commerce for $19.99, and the annual dividend of $1.92 has a yield of 9.6%. ARCC’s dividend earnings was capable of be relied on in the course of the pandemic and all through a low-rate atmosphere. I anticipate that ARCC will proceed to be a excessive dividend payer particularly since BDCs can keep away from paying company taxes if they’re distributing at the very least 90% of their taxable earnings via their dividend program. The $0.48 quarterly dividend is presently supported by $0.60 of NII per share and $0.63 of core EPS. There’s greater than sufficient room for ARCC to proceed paying out the present dividend.

There’s presently $6.36 trillion sitting on the sidelines in cash market accounts with out making an allowance for capital tied to CDs and T-bills that can be maturing over the following yr. Because the risk-free charge of return begins to say no, I feel BDCs will turn into extra common as a substitute for the T-bill and chill methodology for producing earnings. ARCC is taken into account the gold normal as a result of it has the most important internet property and generates the most important quantity of NII within the BDC sector. As charges begin to fall, I feel a good quantity of capital will discover its means again into the fairness markets, and we are going to see earnings traders seeking to recreate their yields via a mix of investments, which can embody BDCs. I consider ARCC can be on the high of the checklist as its dividend monitor document resembles stability, and when traders look into the underlying financials, it appears as if ARCC is in a great place to take care of the dividend at its present degree.

Ares Capital

Evaluating ARCC to its friends

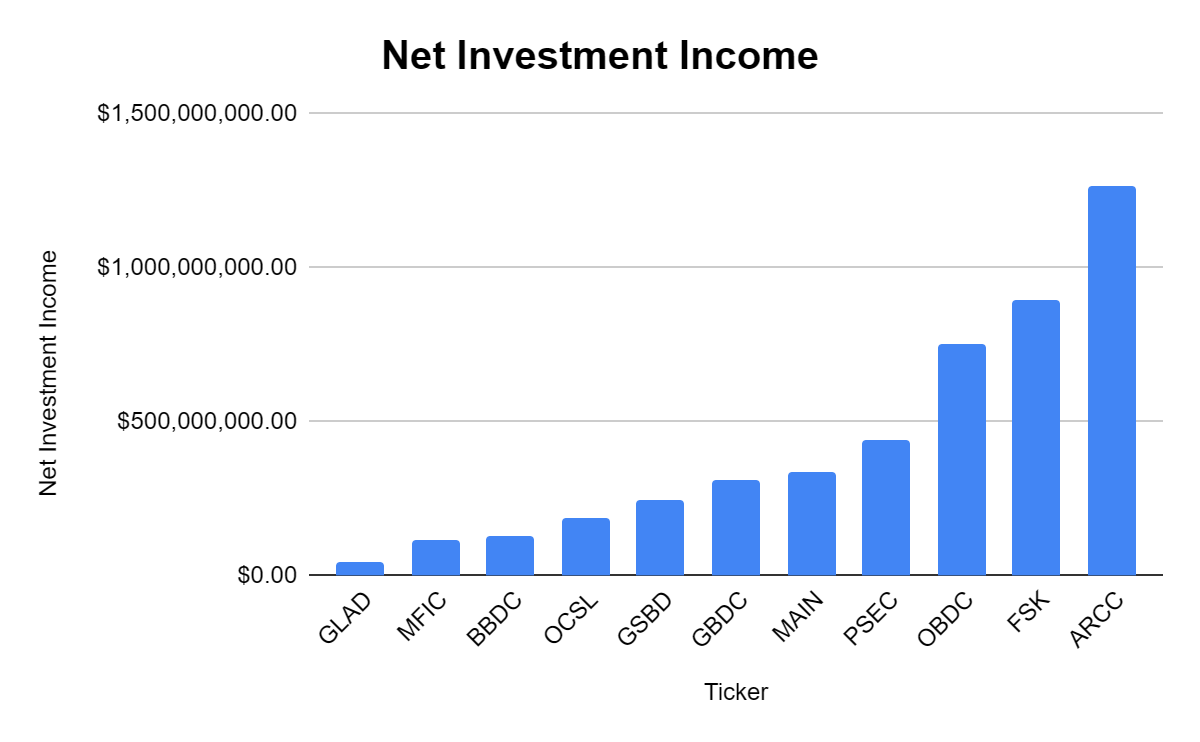

I monitor 12 BDCs so I can evaluate how the peer group is buying and selling and the way any particular person BDC is being valued. The peer group that I’ll evaluate ARCC to consists of the next BDCs:

- Major Road Capital (MAIN)

- Prospect Capital Corp. (PSEC)

- Barings BDC (BBDC)

- Blue Owl Capital Company (OBDC)

- MidCap Monetary Funding Company (MFIC)

- Goldman Sachs BDC (GSBD)

- Oaktree Specialty Lending Company (OCSL)

- Golub Capital BDC (GBDC)

- FS KKR Capital Corp (FSK)

- Gladstone Capital (GLAD)

- Sixth Road Specialty Lending (TSLX)

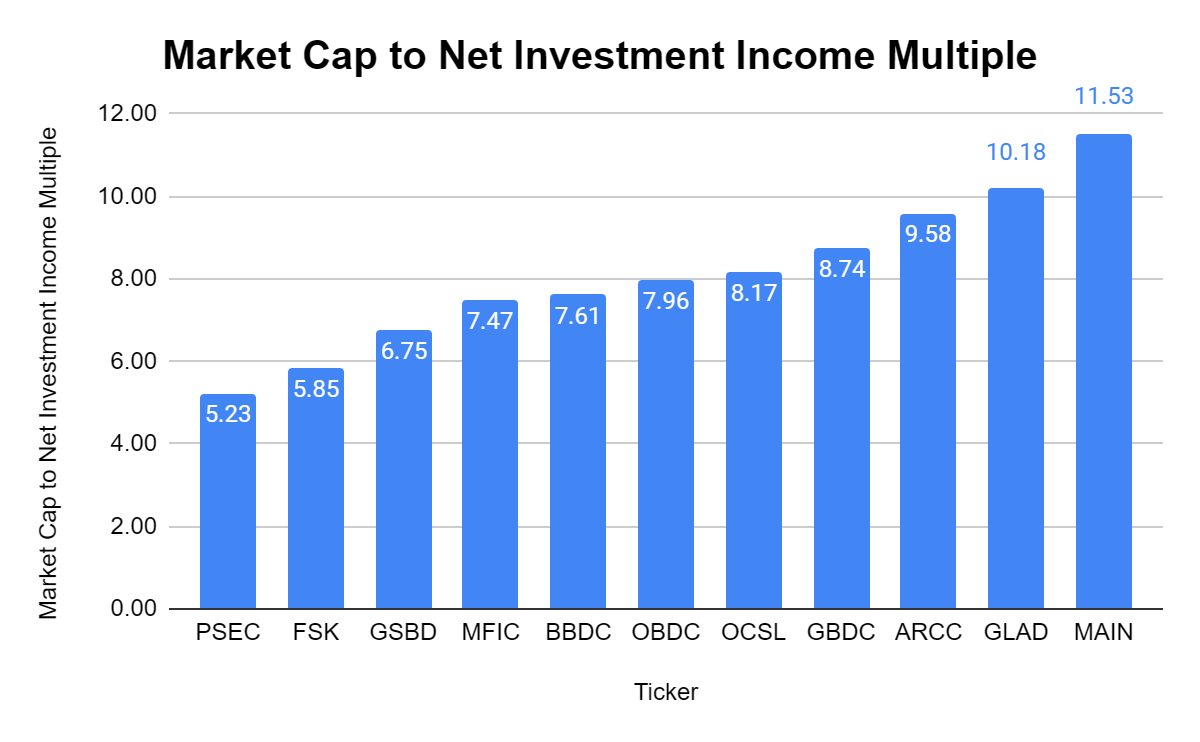

ARCC is the most important BDC by NAV, and by the quantity of NII it produces. I at all times need to pay an ideal value for a BDC’s NII, however I do consider a premium needs to be positioned on nice corporations. At this time, ARCC is producing $1.27 billion in NII and trades at a market cap to NII a number of of 9.58x. This can be a premium on the peer group common of 8.1x. Of the 12 BDCs I monitor, solely 3 of them generate over $500 million in NII, so paying barely increased than the peer group common for ARCC is justified, in my view. I’m snug with the place ARCC is buying and selling and really feel it deserves a bit increased premium because of its high quality.

Steven Fiorillo, In search of Alpha Steven Fiorillo, In search of Alpha

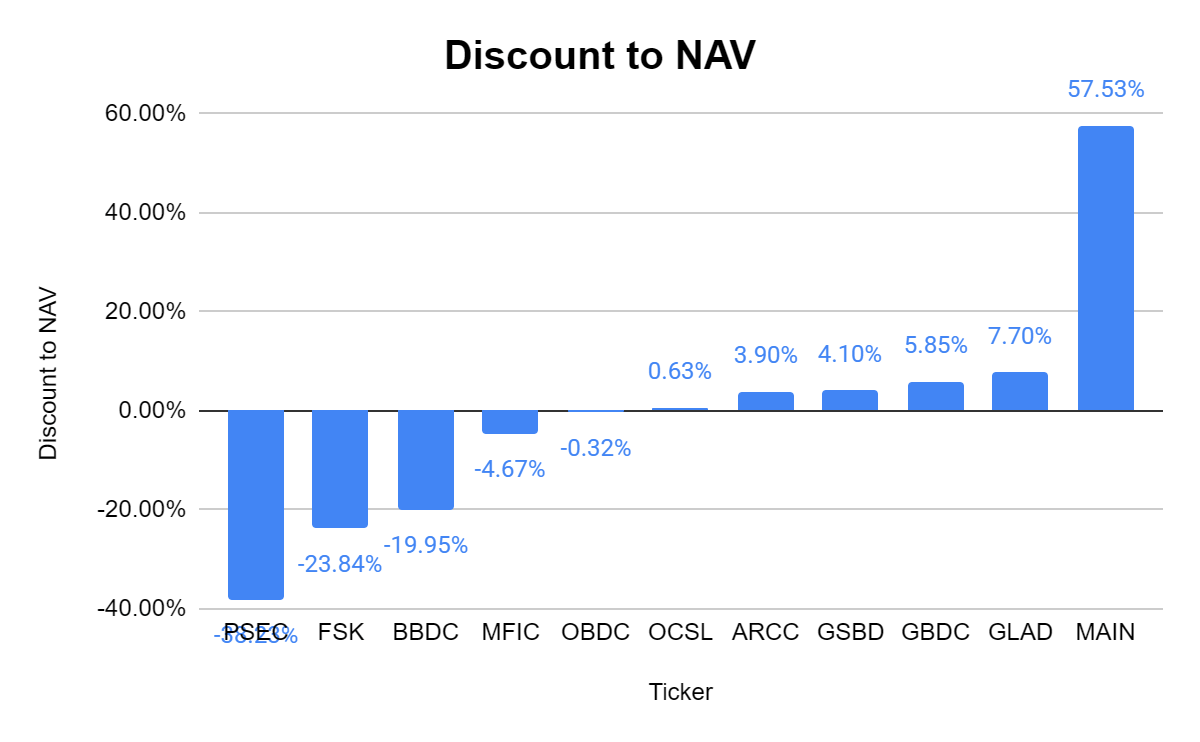

Along with the market cap to NII a number of, I at all times look to see how a lot of a reduction or premium a BDC is buying and selling at in comparison with its NAV. ARCC trades at a 3.9% premium to its NAV in comparison with a peer group common of a -0.66% low cost. Once I see that BDCs akin to MAIN proceed to commerce at greater than a 50% premium to its NAV it makes me be ok with ARCC’s premium. I feel a 3.9% premium is justified, and I would not be stunned if it traded between a 5-10% premium sooner or later.

Steven Fiorillo, In search of Alpha

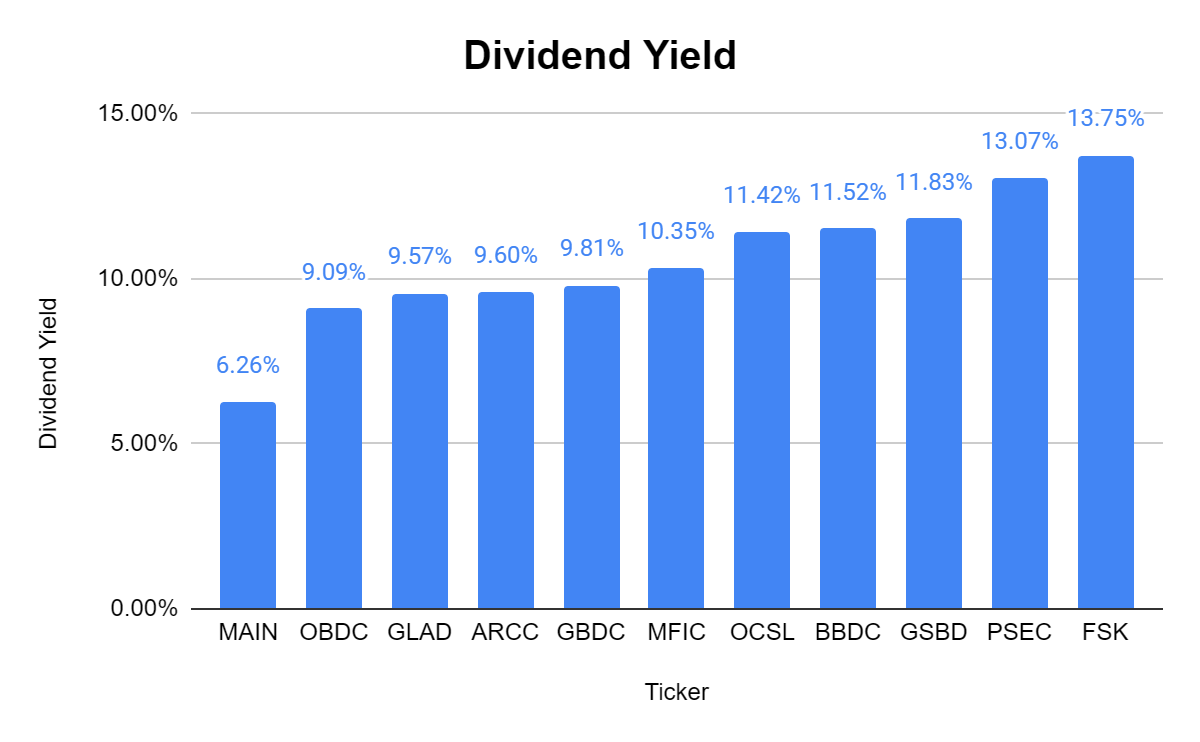

BDCs are recognized for producing massive dividend yields, and ARCC presently has a dividend yield of 9.6%. Whereas that is beneath the peer group common of 10.57%, I haven’t got any complaints about an funding coming with a 9.6% yield. I feel a few of the BDCs with double-digit yields are undervalued, and that contributes to ARCC being beneath the peer group common.

Steven Fiorillo, In search of Alpha

Conclusion

Regardless of ARCC being up 15.58% previously yr, I feel shares are nonetheless a purchase for income-focused traders. The likelihood of ARCC outperforming the market is slim, however its skill to proceed producing $1.92 per share in dividend earnings appears to be like protected in comparison with its core EPS and NII. I feel shares of ARCC will pattern increased over the following yr, and going right into a declining charge atmosphere will not be detrimental to the funding thesis. At this time, traders can lock in a 9.6% dividend yield on price whereas shares commerce at a slim premium to NAV. As we enter right into a rate-declining atmosphere, I feel the top-tier BDCs will turn into magnets for capital seeking to recreate earnings from the T-bill and chill motion. I’m lengthy ARCC and nonetheless really feel it is a chance to generate larger-than-average yields and capital appreciation.