MicroStockHub

Markets Evaluation

(All MSCI index returns are proven web and in U.S. {dollars} until in any other case famous.)

|

Sources: CAPS CompositeHubTM, Bloomberg Previous efficiency just isn’t indicative of future outcomes. Aristotle Worldwide Fairness Composite returns are offered gross and web of funding advisory charges and embrace the reinvestment of all earnings. Gross returns shall be diminished by charges and different bills which may be incurred within the administration of the account. Internet returns are offered web of precise funding advisory charges and after the deduction of all buying and selling bills. Aristotle Capital Composite returns are preliminary pending closing account reconciliation. Please see vital disclosures on the finish of this doc. |

International fairness markets rallied within the fourth quarter. General, the MSCI ACWI Index rose 11.03% in the course of the interval. Concurrently, the Bloomberg International Mixture Bond Index elevated 8.10%. By way of fashion, worth shares underperformed their development counterparts in the course of the quarter, with the MSCI ACWI Worth Index trailing the MSCI ACWI Development Index by 3.57%.

The MSCI EAFE Index climbed 10.42% in the course of the fourth quarter, whereas the MSCI ACWI ex USA Index elevated 9.75%. Inside the MSCI EAFE Index, Europe & Center East and Asia had been the strongest performers, whereas the U.Ok., although posting robust absolute outcomes, gained the least. On a sector foundation, all eleven sectors throughout the MSCI EAFE Index posted optimistic returns, with Data Expertise, Supplies and Actual Property producing the biggest features. Conversely, Vitality, Well being Care and Shopper Staples gained the least.

Regardless of posting total features, international fairness markets had been shocked with one other warfare and humanitarian disaster as tensions between Israel and Hamas reached a watershed in the course of the quarter. In response to the lethal terrorist assault on civilians by Hamas, Israel commenced a army marketing campaign within the Gaza Strip. Whereas issues that the warfare would possibly unfold all through the whole Center East abated in the course of the interval, the advanced non secular, ethnic and political make-up of the area might complicate diplomatic relationships sooner or later.

In the meantime, in Europe, Ukraine’s 2023 counteroffensive towards Russia was confirmed as a failure, and Western assist for the beleaguered nation appears to be waning. President Putin has said that Russia’s warfare targets haven’t modified, however experiences point out that he could also be open to a cease-fire. In Asia, President Xi Jinping claimed that reunification is inevitable, including to the mounting Chinese language stress on Taiwan forward of Taiwan’s 2024 election.

On the financial entrance, international labor markets remained tight, and most nations and areas continued to make inroads within the battle towards inflation, because the U.S., U.Ok., eurozone and Japan all reported slowing annual inflation in November; 3.1%, 3.9%, 2.4% and a couple of.8%, respectively. In response to the bettering situations, each main western and japanese nations largely stored rate of interest coverage regular in the course of the quarter. Nonetheless, future coverage path appears to be divided heading into the brand new yr, because the U.S. signaled potential price cuts, the U.Ok. and eurozone rebuffed untimely discussions of cuts, and Japan appears to finish its coverage of damaging charges in 2024. However, the Worldwide Financial Fund expects international inflation to proceed to steadily decline attributable to total tighter financial coverage and decrease commodity costs, which have been additional suppressed by the bursting of China’s property bubble.

Annual Markets Evaluation

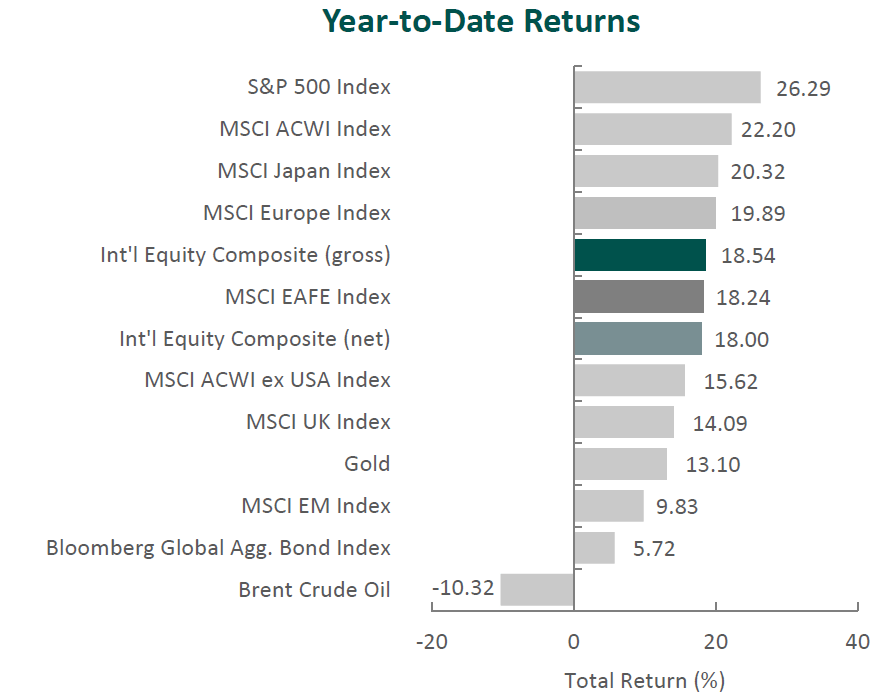

After a tumultuous yr in 2022, international fairness markets rebounded in 2023, because the MSCI ACWI posted a full-year return of twenty-two.20%. Moreover, after underperforming worth in 2022 by the biggest quantity since 2000, development recovered, because the MSCI ACWI Development Index outperformed the MSCI ACWI Worth Index by 21.41% in 2023. In the meantime, mounted earnings markets additionally rose, because the Bloomberg International Mixture Bond Index elevated 5.72%.

Although markets trended in a optimistic path, 2023 nonetheless had its share of twists and turns within the type of a banking disaster and geopolitical conflicts in Europe, the Center East and Asia. Moreover, inflation, corresponding central financial institution insurance policies, and financial restoration in areas like Europe and Asia generated important headlines and proved to be key macroeconomic elements.

Given the multitude of headlines in a yr and their fickle nature, short-term returns are sometimes unstable and inconsistent. Due to this fact, we as a substitute select to concentrate on enterprise fundamentals over the long run. By discovering nice companies which might be undervalued with actionable catalysts inside our funding time horizon, we imagine we will present constant and lasting worth to our shoppers.

Efficiency and Attribution Abstract

For the fourth quarter of 2023, Aristotle Capital’s Worldwide Fairness Composite posted a complete return of 10.41% gross of charges (10.31% web of charges), underperforming the MSCI EAFE Index, which returned 10.42%, and outperforming the MSCI ACWI ex USA Index, which returned 9.75%. Please seek advice from the desk beneath for detailed efficiency.

| Efficiency (%) | 4Q23 | 1 Yr | 3 Years | 5 Years | 10 Years | Since Inception* |

|---|---|---|---|---|---|---|

| Worldwide Fairness Composite (gross) | 10.41 | 18.54 | 3.32 | 8.81 | 5.17 | 5.63 |

| Worldwide Fairness Composite (‘web’) | 10.31 | 18.00 | 2.84 | 8.30 | 4.66 | 5.13 |

| MSCI EAFE Index (‘web’) | 10.42 | 18.24 | 4.02 | 8.16 | 4.28 | 2.76 |

| MSCI ACWI ex USA Index (‘web’) | 9.75 | 15.62 | 1.55 | 7.08 | 3.83 | 2.35 |

| *The inception date for the Worldwide Fairness Composite is January 1, 2008. Previous efficiency just isn’t indicative of future outcomes. Aristotle Worldwide Fairness Composite returns are offered gross and web of funding advisory charges and embrace the reinvestment of all earnings. Gross returns shall be diminished by charges and different bills which may be incurred within the administration of the account. Internet returns are offered web of precise funding advisory charges and after the deduction of all buying and selling bills. Aristotle Capital Composite returns are preliminary pending closing account reconciliation. Please see vital disclosures on the finish of this doc. |

|

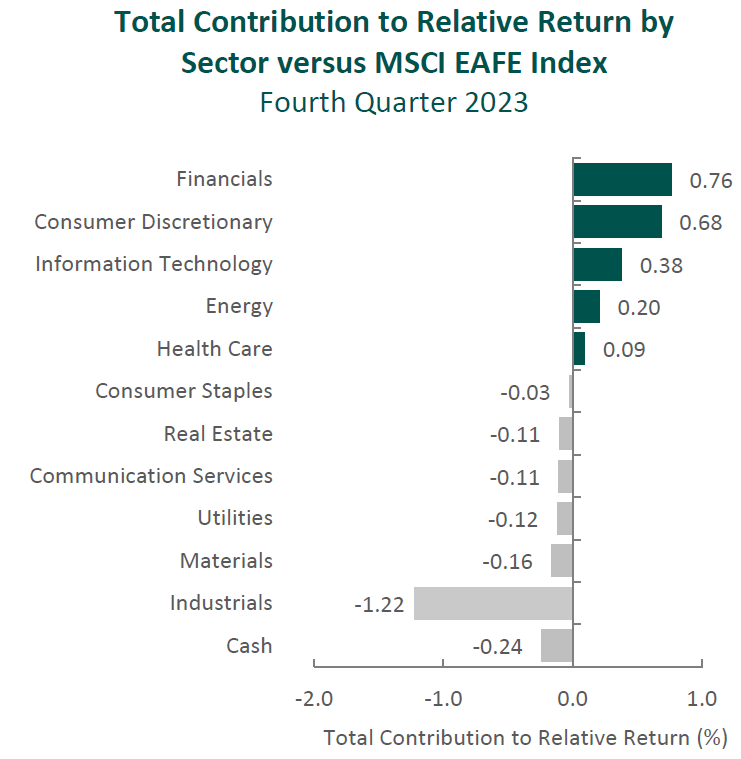

Supply: FactSet Previous efficiency just isn’t indicative of future outcomes. Attribution outcomes are based mostly on sector returns that are gross of funding advisory charges. Attribution is predicated on efficiency that’s gross of funding advisory charges and contains the reinvestment of earnings. |

From a sector perspective within the fourth quarter, the portfolio’s modest underperformance relative to the MSCI EAFE Index could be attributed to allocation results, whereas safety choice had a optimistic impression. Safety choice in Industrials and Well being Care, in addition to an obese in Vitality, detracted probably the most from the portfolio’s relative efficiency. Conversely, safety choice in Financials, Shopper Discretionary and Vitality contributed to relative return.

Regionally, safety choice was answerable for the portfolio’s underperformance, whereas allocation results had a optimistic impression. Safety choice within the U.Ok. and Asia detracted from relative efficiency, whereas publicity to Canada and safety choice in Europe & Center East contributed.

Contributors and Detractors for 4Q 2023

Rentokil Preliminary, the U.Ok.-based pest management and hygiene providers firm, was the biggest detractor for the quarter. The corporate’s pest management section (which accounts for 94% of whole working revenue) reported a slowdown in natural income development from 5.6% within the first half of 2023 to 2.3% within the third quarter. As these outcomes are quick time period in nature, we are going to proceed to carefully monitor the corporate’s progress on each integration of Terminix and additional enchancment of its advertising and marketing technique. This contains the current appointment of Brad Paulsen as CEO of the North America Area and his impression on the corporate’s most vital geography (accounting for ~75% of pest management gross sales). Over the long run, we stay assured that the Terminix acquisition will create scale efficiencies and in-market densification (with a focused $200 million in value synergies by 2025), in addition to speed up the consolidation of the U.S. pest management market. Brief-term impacts on the corporate’s inventory worth, in our opinion, are overdone given these basic enhancements coupled with the resilient nature of the pest management enterprise.

Japan-based Nidec, the worldwide provider of brushless motors, was one of many largest detractors for the quarter. The corporate’s electrical automobile (‘EV’) traction motor enterprise has disenchanted, with cargo assumptions dropping to 350,000 from 949,000 in the beginning of the fiscal yr. Administration additionally withdrew its bold goal for the EV enterprise to show worthwhile this fiscal yr, now projecting an working lack of ¥15 billion, because it famous all motor suppliers to Chinese language EV producers are at present experiencing losses attributable to intensifying worth competitors. In response, Nidec has introduced a shift in its technique to each improve R&D spending to speed up product improvement and shore up profitability with extra selective order placement. Whereas we proceed to imagine Nidec’s experience in energy effectivity gives it with a singular benefit to produce industrial motors throughout markets (not just for EVs, but additionally robots, home equipment and industrial purposes), we’re fastidiously reviewing whether or not current setbacks are cyclical points or extra everlasting in nature, and we additionally proceed to observe modifications in management, together with these set to happen in April 2024.

Nemetschek, a venture administration software program options supplier for the structure, engineering and building business, was the biggest contributor for the quarter. Over the previous couple of years, the corporate has made important efforts to transition the enterprise from a license to a subscription SaaS (software program as a service) mannequin, which we anticipated would drive increased and extra steady revenues per consumer whereas creating extra long-term worth for patrons. Consistent with this technique, the corporate reported that ~75% of its revenues at the moment are recurring, up from ~65% final yr. Moreover, with the backdrop of steady demand and robust operational execution, administration reported EBITDA margins on the excessive finish of steering and raised its income projections for the yr. We imagine the optimization of Nemetschek’s enterprise mannequin, continued enchancment in operational effectivity by efforts like internalization, and product innovation, such because the open and cloud-based dTwin platform, will result in long-term enhancements in profitability and place the corporate for market share features as constructing complexity continues to extend.

Experian, one of many largest credit score bureau firms on the planet, was a major contributor in the course of the quarter. Amid tighter lending situations, the corporate continues to point out its power. This contains current product launches and innovation throughout the firm’s Ascend platform, which leverages deeper analytics in order that lenders can automate processes and goal audiences extra successfully. The credit score bureau additionally expanded its place in employer providers and verifications and has seen additional digital penetration in areas like Auto and Well being. Throughout our effectively over a decade-long possession of Experian, the corporate has more and more discovered methods to monetize current knowledge units and serve new sorts of clients. We imagine Experian’s distinctive business construction and large knowledge library (with knowledge on ~1.5 billion customers and ~200 million companies) not solely creates an exceptionally scalable enterprise with excessive obstacles to entry, but additionally makes it uniquely positioned to learn from the elevated want for large knowledge throughout many industries.

Latest Portfolio Exercise

Through the quarter, we bought our positions in Dassault Systèmes and Sandoz and invested in a brand new place in Daikin Industries.

We first invested in Dassault within the first quarter of 2015. Throughout our greater than eight-year holding interval, the corporate executed on a lot of catalysts, together with a worthwhile transition to a brand new software program platform (i.e., 3DExperience) and profitable entry into new verticals corresponding to life sciences by way of the 2019 acquisition of Medidata. Whereas we proceed to view Dassault as a high-quality firm, we determined to exit our funding in favor of what we view as a extra optimum alternative in Daikin Industries, which is mentioned intimately beneath.

Now we have been Novartis shareholders for over a decade. In October of 2023, the corporate accomplished the spinoff of Sandoz, its generics and biosimilars enterprise. This divestiture furthers Novartis’s ongoing transition to a concentrate on branded pharmaceuticals, having over the past a number of years additionally exited its eye care, vaccine, animal well being and client healthcare companies. Upon additional evaluation, we determined to promote the shares obtained within the Sandoz spinoff and use the proceeds for what we take into account to be a extra optimum funding.

Daikin Industries, Ltd.

Based in 1924 and headquartered in Japan, Daikin Industries is the world’s largest business and residential air conditioner firm. Daikin primarily manufactures and sells air con techniques, warmth pumps, air purifiers and refrigeration tools (which accounts for over 90% of income). Daikin has lengthy been an business chief in creating energy-efficient merchandise, which was molded by its roots in Japan, a area with restricted pure sources and excessive vitality prices. The corporate’s R&D consists of a worldwide Expertise Innovation Heart and 39 different regional improvement services answerable for tailoring choices to their native markets. As we speak Daikin’s merchandise are bought in over 170 nations, and the corporate boasts main market positions in Japan and China, in addition to within the U.S. residential market.

Distribution is especially vital since air con techniques are tough to put in. Daikin’s 2012 acquisition of Goodman within the U.S. added a whole bunch of distribution factors throughout the nation, offering Daikin with a number one nationwide market place and platform from which to broaden. In China, specialty retail shops (ProShops) promote on to owners, specializing in high-end, multi-unit merchandise at a lot increased margins than in the event that they had been promoting to a developer or contractor.

Excessive-High quality Enterprise

Among the high quality traits now we have recognized for Daikin embrace:

- Robust model recognition and a big international distribution community are, in our opinion, robust aggressive benefits and function excessive obstacles to entry;

- Historical past of technological innovation, notably in energy-saving inverters and variable refrigerant stream techniques; and

- Capacity to tailor merchandise to totally different native preferences throughout geographies and different ranges of HVAC rules, due to Daikin’s community of worldwide manufacturing bases and improvement services.

Enticing Valuation

Primarily based on our estimates, shares of the corporate are attractively valued. We imagine higher international adoption of air con, in addition to increased priced and extra worthwhile applied sciences (i.e., warmth pumps and inverters), will result in increased normalized FREE money stream than at present appreciated by the market.

Compelling Catalysts

Catalysts now we have recognized for Daikin, which we imagine will trigger its inventory worth to understand over our three- to five-year funding horizon, embrace:

- As the biggest international provider and a pacesetter in vitality effectivity, Daikin is uniquely positioned to learn from the rise in worldwide air con adoption charges (projected to triple by 2050) whereas leveraging its mental property in inverters and warmth pumps;

- Market share features within the U.S. as Daikin additional leverages its expertise in premium residential air con supported by Goodman’s distribution community; and

- Execution of its Fusion 25 strategic plan that features making enhancements in technological improvement, strengthening gross sales and repair networks, selling digital transformation, and extra.

Conclusion

With unstable financial knowledge factors, altering central financial institution insurance policies, shocks to the banking system and varied geopolitical conflicts, 2023 was filled with headline-worthy information. Nonetheless, because the market’s consideration shortly shifted from one macro occasion to the following, we remained true to our backside up, basic funding philosophy.

As such, as a substitute of chasing the following headline or “placing bets” on short-term predictions, our focus stays on enterprise fundamentals and what’s analyzable in the long term. For over the previous quarter century, now we have devoted ourselves to a “bottom-up” strategy of figuring out high-quality companies buying and selling at significant reductions to intrinsic worth, that possess catalysts that are underway and inside administration’s management. By doing so, we imagine we will discover long-term success whatever the macroeconomic surroundings or information of the day.

|

Disclosures The opinions expressed herein are these of Aristotle Capital Administration, LLC (Aristotle Capital) and are topic to vary with out discover. Previous efficiency just isn’t a assure or indicator of future outcomes. This materials just isn’t monetary recommendation or a suggestion to purchase or promote any product. You shouldn’t assume that any of the securities transactions, sectors or holdings mentioned on this report had been or shall be worthwhile, or that suggestions Aristotle Capital makes sooner or later shall be worthwhile or equal the efficiency of the securities listed on this report. The portfolio traits proven relate to the Aristotle Worldwide Fairness technique. Not each shopper’s account could have these traits. Aristotle Capital reserves the best to change its present funding methods and methods based mostly on altering market dynamics or shopper wants. There isn’t a assurance that any securities mentioned herein will stay in an account’s portfolio on the time you obtain this report or that securities bought haven’t been repurchased. The securities mentioned could not signify an account’s total portfolio and, within the combination, could signify solely a small share of an account’s portfolio holdings. The efficiency attribution offered is of a consultant account from Aristotle Capital’s Worldwide Fairness Composite. The consultant account is a discretionary shopper account which was chosen to most carefully mirror the funding fashion of the technique. The standards used for consultant account choice is predicated on the account’s time period below administration and its similarity of holdings in relation to the technique. Suggestions made within the final 12 months can be found upon request. Returns are offered gross and web of funding advisory charges and embrace the reinvestment of all earnings. Gross returns shall be diminished by charges and different bills which may be incurred within the administration of the account. Internet returns are offered web of precise funding advisory charges and after the deduction of all buying and selling bills. All investments carry a sure diploma of danger, together with the potential lack of principal. Investments are additionally topic to political, market, foreign money and regulatory dangers or financial developments. Worldwide investments contain particular dangers that will specifically trigger a loss in principal, together with foreign money fluctuation, decrease liquidity, totally different accounting strategies and financial and political techniques, and better transaction prices. These dangers sometimes are higher in rising markets. Securities of small‐ and medium‐sized firms are inclined to have a shorter historical past of operations, be extra unstable and fewer liquid. Worth shares can carry out in another way from the market as an entire and different sorts of shares. The fabric is supplied for informational and/or academic functions solely and isn’t supposed to be and shouldn’t be construed as funding, authorized or tax recommendation and/or a authorized opinion. Buyers ought to seek the advice of their monetary and tax adviser earlier than making investments. The opinions referenced are as of the date of publication, could also be modified attributable to modifications out there or financial situations, and will not essentially come to move. Data and knowledge offered has been developed internally and/or obtained from sources believed to be dependable. Aristotle Capital doesn’t assure the accuracy, adequacy or completeness of such data. Aristotle Capital Administration, LLC is an impartial registered funding adviser below the Advisers Act of 1940, as amended. Registration doesn’t indicate a sure stage of ability or coaching. Extra details about Aristotle Capital, together with our funding methods, charges and targets, could be present in our Kind ADV Half 2, which is out there upon request. ACM-2401-45 Efficiency Disclosures  Sources: CAPS CompositeHubTM, MSCI  Composite returns for all intervals ended December 31, 2023 are preliminary pending closing account reconciliation. Previous efficiency just isn’t indicative of future outcomes. The data supplied shouldn’t be thought of monetary recommendation or a suggestion to buy or promote any explicit safety or product. Efficiency outcomes for intervals higher than one yr have been annualized. Returns are offered gross and web of funding advisory charges and embrace the reinvestment of all earnings. Gross returns shall be diminished by charges and different bills which may be incurred within the administration of the account. Internet returns are offered web of precise funding advisory charges and after the deduction of all buying and selling bills. Index Disclosures The MSCI EAFE Index (Europe, Australasia, Far East) is a free float-adjusted market capitalization-weighted index that’s designed to measure the fairness market efficiency of developed markets, excluding the USA and Canada. The MSCI EAFE Index consists of the next 21 developed market nation indexes: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Eire, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the UK. The MSCI ACWI captures giant and mid-cap illustration throughout 23 developed market nations and 24 rising markets nations. With roughly 3,000 constituents, the Index covers roughly 85% of the worldwide investable fairness alternative set. The MSCI ACWI Development Index captures giant and mid-cap securities exhibiting total development fashion traits throughout 23 developed markets nations and 24 rising markets nations. The MSCI ACWI Worth Index captures giant and mid-cap securities exhibiting total worth fashion traits throughout 23 developed markets nations and 24 rising markets nations. The MSCI ACWI ex USA Index captures giant and mid-cap illustration throughout 22 of 23 developed markets nations (excluding the USA) and 24 rising markets nations. With roughly 2,300 constituents, the Index covers roughly 85% of the worldwide fairness alternative set exterior the USA. The MSCI Rising Markets Index is a free float-adjusted market capitalization-weighted index that’s designed to measure the fairness market efficiency of rising markets. The MSCI Rising Markets Index consists of the next 24 rising market nation indexes: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Kuwait, Malaysia, Mexico, Peru, Philippines, Poland, Qatar, Saudi Arabia, South Africa, Taiwan, Thailand, Turkey and United Arab Emirates. The S&P 500® Index is the Normal & Poor’s Composite Index of 500 shares and is a well known, unmanaged index of widespread inventory costs. The Brent Crude Oil Index is a serious buying and selling classification of candy gentle crude oil that serves as a serious benchmark worth for purchases of oil worldwide. The MSCI Japan Index is designed to measure the efficiency of the big and mid-cap segments of the Japanese market. With roughly 250 constituents, the Index covers roughly 85% of the free float-adjusted market capitalization in Japan. The Bloomberg International Mixture Bond Index is a flagship measure of worldwide funding grade debt from 28 native foreign money markets. This multi-currency benchmark contains treasury, government-related, company and securitized fixed-rate bonds from each developed and rising markets issuers. The MSCI United Kingdom Index is designed to measure the efficiency of the big and mid-cap segments of the U.Ok. market. With practically 100 constituents, the Index covers roughly 85% of the free float-adjusted market capitalization in the UK. The MSCI Europe Index captures giant and mid-cap illustration throughout 15 developed markets nations in Europe. With roughly 430 constituents, the Index covers roughly 85% of the free float-adjusted market capitalization throughout the European developed markets fairness universe. These indexes have been chosen because the benchmarks and are used for comparability functions solely. The volatility (beta) of the Composite could also be higher or lower than the respective benchmarks. It isn’t potential to take a position straight in these indexes. |

Editor’s Observe: The abstract bullets for this text had been chosen by Looking for Alpha editors.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please concentrate on the dangers related to these shares.