Ignatiev

Prelude

I covered Arm Holdings (NASDAQ:ARM) pre-IPO, stating that I believed the valuation was a bit too rich. I rated ARM a Hold at the time, a rating I maintain in this coverage. Admittedly, this was a bad call. The fact is, ARM is a foundational piece of the semiconductor ecosystem, and we are amidst a drastic upswing in hype and stock valuations in the sector. It was a poorly timed call based only on valuation and not on general market sentiment. Those that ignored my call and bought the IPO have done quite well. Despite this, the story is fundamentally unchanged, and the recent stock run has resulted in a ridiculously stretched valuation. Despite the fundamental quality of ARM’s business, there is no reason to pay such a price for any business.

Let’s discuss.

Business Overview

The ARM ISA is the standard in mobile devices today, in large part because of the energy efficiency offered by a RISC (reduced instruction set computer) compared to a CISC (complex instruction set computer) chip. The x86, the prolific CISC architecture, is losing share in data center to ARM because of the increasing floor space dedicated to AI accelerators. The problem rapidly arising with AI is the vast power it requires to run and cool these accelerators, so all chip designers have an incentive to build atop the most efficient architecture possible.

This is clear in ARM’s design wins in data center accelerators: Nvidia’s (NVDA) Grace CPU, Google (GOOG) Axion, and Microsoft (MSFT) Cobalt, to name a few. There are very positive growth prospects looking forward in data center as AI continues to accelerate hyperscaler capex and as accelerators continue increasing CPUs per chip.

ARM’s revenue model is straightforward: the company earns money by licensing its IP and by earning a royalty on unit shipments. The transition to the current generation of the ARM ISA, Armv9, is accelerating royalty growth as it earns a higher royalty rate. Meanwhile, licensing revenue grew 60% YoY due largely to the aforementioned design wins with hyperscalers.

Q4 FYE 2024 Investor Presentation

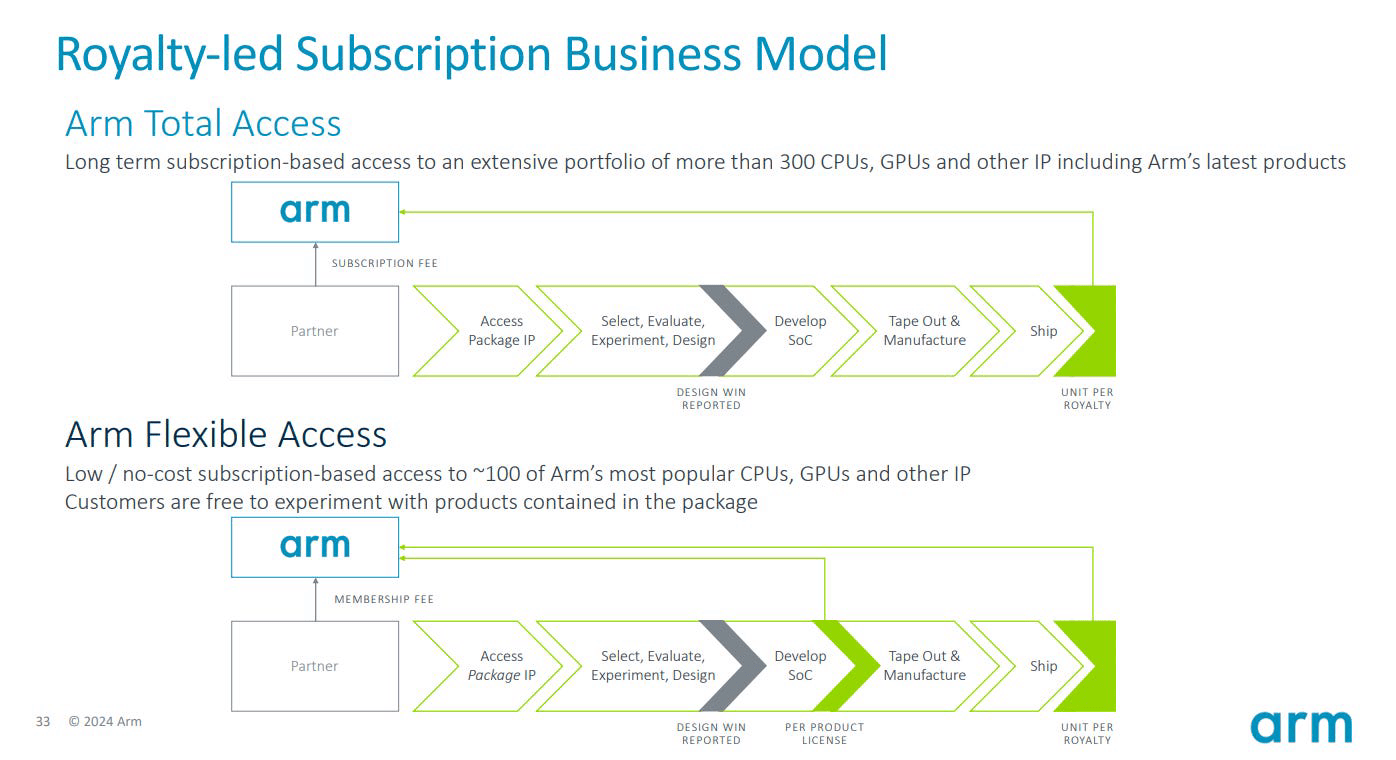

ARM offers two primary licensing levels: ARM Flexible Access (“AFA”) and ARM Total Access (“ATA”). It also offers a newer product called CSS, Compute Subsystem, which offers entire CPU cores with customizable memory, I/O and networking. The most common CSS is the Neoverse CPU line (used in Nvidia Grace CPUs). Compute Subsystems are offered in the most expensive ‘C’ tier of ATA licenses. CSS designs are specialized by use case, Neoverse is the data center CSS, with others targeting different markets like autonomous vehicles and IoT, for example. ARM Flexible Access also offers $0 access to ARM IP for startups.

www.arm.com

ACV, Annualized Contract Value, is the best gauge of licensing revenue durability. ATA licenses are very accretive to ACV. ARM currently has 31 ATA customers; many of whom are experiencing booming sales growth.

While ARM’s business model looks impeccable at first glance, there are two notable risks. As noted above, customers pay ARM twice – once for the license and then royalties for each chip sold. As customers grow and have more cash to fund internal R&D, they could seek to move down the ARM value chain by designing their own cores. This risk could become especially prevalent if ARM becomes less customer friendly or tries to exert pricing power on royalty rates. The company is in an ongoing legal battle with Qualcomm over a licensing dispute, for example. This could be a one-off or the first of a string of costly and time-consuming lawsuits. Regardless, this is a headwind to future earnings growth.

Next, RISC-V remains a considerable risk to ARM. RISC-V is an open-source and royalty-free platform offering RISC chip architecture designs. It’s unlikely a meaningful risk in the short run, but is definitely a long-term threat considering the amount of custom silicon projects ongoing in the industry. ARM has an engineering lead and deep industry ties, but RISC-V is testing how defensible the ARM moat is.

Investment Case

The company is undoubtedly well positioned to benefit from the AI cycle that is reshaping the global economy. The revenue model is simple, straightforward, and effective. Yet, I am rating ARM a Hold. Why? It’s equally simple: the company has an abysmal net margin and obscene valuation. This is priced beyond perfection. It’s priced at complete FOMO levels.

Momentum traders could still see opportunity here – Nvidia Blackwell shipments will boost revenue for ARM, hyperscalers are increasingly shifting to custom silicon, and iPhone shipments are recovering after a few tough quarters. It does not seem that the AI hype cycle has topped out yet (although Nvidia’s earnings on May 22nd could change this). This stock could certainly run higher. But long-term investors ought to beware: this stock is massively overvalued and will face a correction in due time. When a correction brings ARM’s price in closer alignment with fundamentals, I will be buying hand over fist. This company is a quality investor’s dream, but the price is just too high right now.

Earnings Discussion

With that, let’s discuss the earnings report, call, and some positive and negative takeaways.

The Report

Considering ARM’s valuation, this report was mixed. ARM is trading at 128x forward earnings and 28x forward sales. While the 47% YoY growth in Q4 sales was strong, it wasn’t 28x P/S strong. The full year 2024 sales growth of 21% was even less so.

Q4 FYE 2024

-

Revenue of $928m, up 47% YoY

-

Royalty revenue of $514m, up 37% YoY

-

License revenue of $414m, up 60% YoY

-

-

Operating profit of $391m & 42% non-GAAP operating margin

Full Year 2024

-

Revenue of $3.23b, up 21% YoY

-

Royalty revenue of $1.86b, up 8% YoY

-

License revenue of $1.43b, up 43% YoY

-

-

Non-GAAP operating profit of $1.4b, up 80% YoY & 43.6% margin

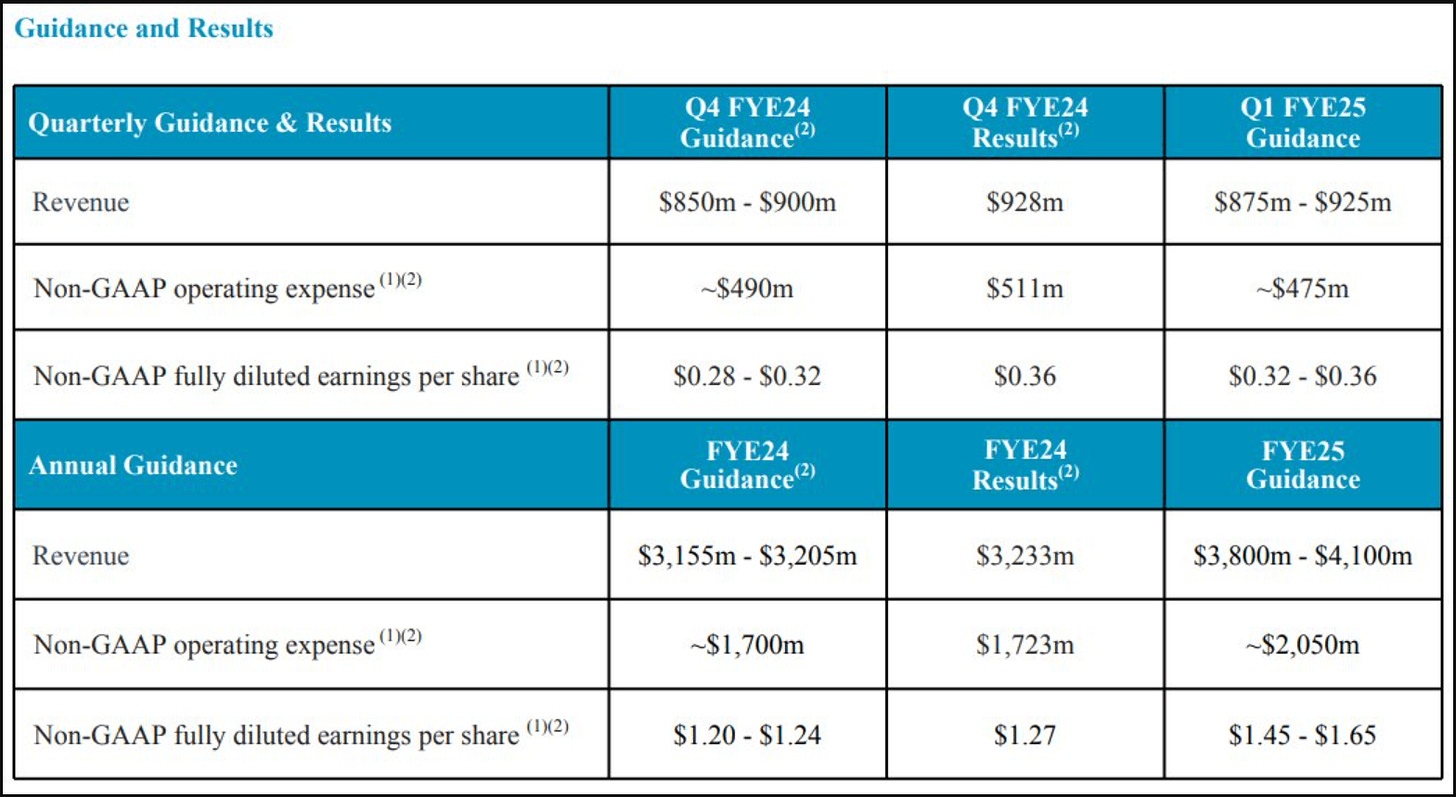

Guidance

ARM Q4 2024 Earnings Report

The results for the year and quarter were strong and followed up with strong guidance. ARM exceeds the top end of previous guidance and guided for continued strong growth. Meanwhile, ARM had a 96% gross margin on the year, illustrating the incredible competitive advantage and cost efficiency of the business. RPOs (remaining performance obligations) were up 45% to $2.48b and ACV was up 15% YoY to $1.18b. Total chips shipped was down 10% YoY to 7b from 7.8b, which confirms the broader rhetoric of a general slowdown in semis despite AI hype in 2023. ARM’s top line is impeccable, with strong growth and a very lucrative gross margin profile. The durability of revenue growth is strong as well – royalty revenues will grow in line with the semiconductor industry at a minimum. The adoption of Armv9 will accelerate royalty growth as well. Licensing revenue is benefitting from ARM’s strategic shift to specialized CSS offerings:

ARM Q4 2024 Investor Report

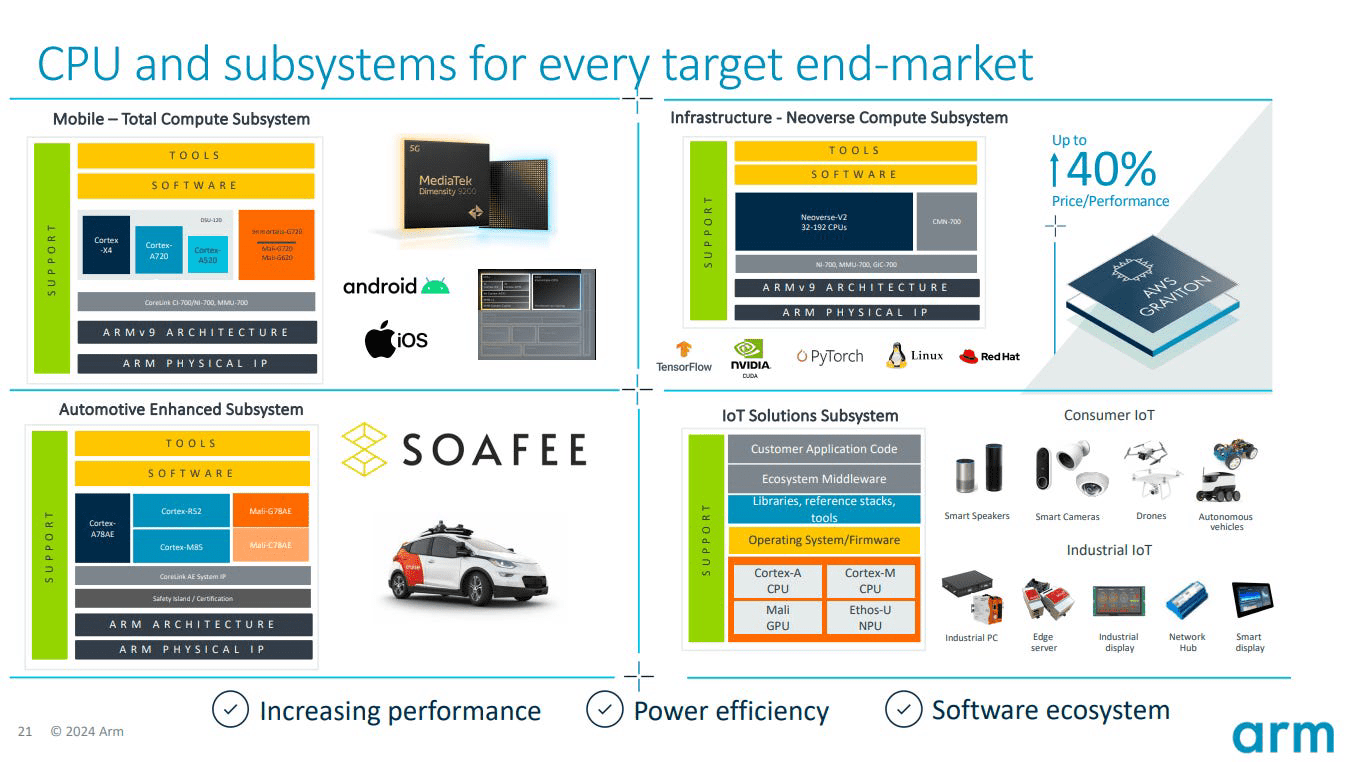

There is a lot to love in ARM’s revenue profile. However, there is a lot to dislike about the rest of ARM’s income statement. OpEx was $865m in Q4, while R&D was $584m. While the 96% gross margin illustrates the competitive advantage, R&D expense gobbled up 63% of revenues! ARM is investing heavily in engineering (83% of employees are engineers) to aggressively defend or earn share in four main end markets: mobile (defend 99% market share), data center (infrastructure; ARM is currently winning share from x86), Automotive and IoT, which are both compelling opportunities. It’s not a bad strategy, but considering ARM’s multiple, using 63% of revenues on R&D is unsustainable. Worse yet, another 30% of revenues went to SG&A expense, so 93% of revenues were lost in SG&A plus R&D. This valuation is entirely divorced from reality.

That said, there is still a lot to love about this company. I will be an investor in ARM at one point, but I can’t justify buying even the best of companies at this valuation. ARM is aggressively pursuing four core markets and has an opportunity to greatly expand royalty rates. The Armv9 adoption ramp is accelerating this, while ACV is expected to double next year.

Investor Takeaway

ARM is a wonderful business. There is no doubting that. Yet, investment is about more than just finding a wonderful business, it’s also about buying that business at the right price. Despite the solid results and overall quality of ARM’s business model, I do not see any reason to invest in ARM at current valuations. I recommend waiting for a sizable multiple contraction.

ARM’s business model is similar to high gross margin software businesses. I’d compare it to Adobe (ADBE), Salesforce (CRM), Palantir (PLTR), and Shopify (SHOP). Alternatively, we could compare to some fabless semiconductor stocks like Nvidia, Advanced Micro Devices (AMD), Broadcom (AVGO) or Qualcomm (QCOM). ARM is overvalued relative to these companies:

| Stock | FWD P/S | FWD Sales Growth Estimate |

|---|---|---|

| ARM | 28 | 26.88% |

| ADBE | 10 | 10.80% |

| CRM | 7 | 10.19% |

| PLTR | 17 | 19.37% |

| SHOP | 9 | 22.29% |

| NVDA | 20 | 74.26% |

| AMD | 10 | 11.42% |

| AVGO | 13 | 19.93% |

| QCOM | 6 | -1.45% |

While ARM does have very solid growth expectations relative to this group, the multiple is clearly misaligned. We need not look further than Nvidia and Shopify, the two companies I’d say present the best P/S multiple relative to growth expectations.

ARM is due for a contraction at some point. I would be more comfortable with a forward P/S of 10-15, which would be around $40b-$60b right now. That would leave the stock price around $40-$60. I would begin to make minor purchases at that P/S level and continue to add more as the price fell.