Yana Boiko/iStock through Getty Pictures

Intro

We wrote about Armanino Meals of Distinction, Inc. (OTCPK:AMNF) again in February 2020 once we delved by means of a number of the key monetary developments that make up the corporate’s dividend. Shares had been buying and selling at $3.20 per share on the time. Though we noticed no points with the US frozen meals producer on the time with developments in e-book worth and EBIT being notably sturdy, on condition that shares had topped out in September’2019 and had been present process a sustained development of decrease lows on the time, we rated the inventory a ‘Maintain’ till we had affirmation that monetary markets had bottomed out.

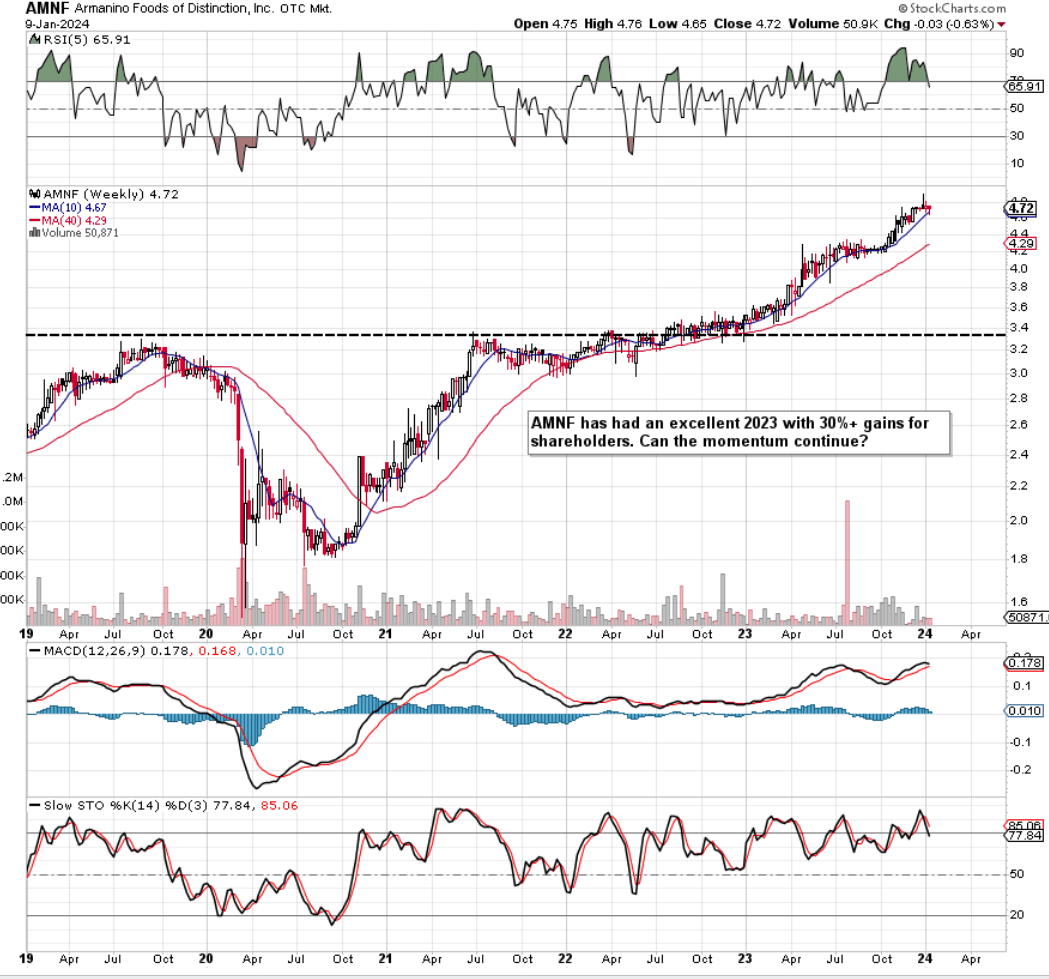

The ‘Maintain’ ranking on the time was the fitting name as shares traded under $2 a share within the throes of the pandemic earlier than lastly bottoming out. As we see from the technical chart under, publish the inventory’s rally out of the pandemic 2020 lows, shares did consolidate (restricted share-price beneficial properties) between mid-2021 & late 2022. Nevertheless, Armanino’s fundamentals appeared to obtain a big enhance as soon as calendar 2023 began as since then, shares have by no means regarded again. Shareholders (minus dividend distributions) have seen a 30% acquire over the previous 12+ months which demonstrates that the ramifications of the pandemic might have been a blessing in disguise.

AMNF Technical Chart (Stockcharts.com)

Progress Triggers In A number of Areas

We state this as a result of Armanino is a a lot completely different firm now than it was in 2020 in that the downturn compelled administration to get its prices below management, enhance inner efficiencies & advertising and marketing efforts, and above all, double down on progress drivers to realize market share. After reviewing Armanino’s most recent earnings report (sixteenth of October 2023) & investor presentation, administration appears adamant that vital potential stays in its meals service core enterprise, retail in addition to its new product platform.

In meals service, restaurant penetration stands at solely 30% demonstrating the lengthy runway for progress Armanino has for the multitude of its frozen recent choices illustrated under. On the retail entrance, the success of the Armanino model within the likes of Safeway in sure jurisdictions demonstrates that the corporate has a superb product the place the worth case amongst clients is recognized. Once more, within the retail phase, there’s a lengthy runway for progress right here given Armanino’s restricted presence within the South West, Texas & the East of the US. The ‘Prepared Meal’ development is one other progress space the place Armanino can reap the benefits of the current relationships it has with its retailers. The goal market Armanino desires to hit right here is the health-minded deli buyer who desires wholesome meals out of a restaurant setting.

Armanino High-Promoting Foodservice Objects (Firm Web site)

Monetary Tendencies

Proof of Armanino’s transformation may be seen in its latest quarterly numbers (ending September 2023) & corresponding 9-month (year-to-date) developments. Gross sales grew by 4% over the identical interval of 12 months prior and by 7.5% over the primary three quarters of 2022. What was notably noteworthy (alluded to earlier) is how the corporate continues to get its prices so as and thus enhance its margins. Web revenue of $2,263,972 within the September quarter was a 46% acquire over the identical interval of 12 months prior whereas the primary 9 months of 2023 ($6,188,927) got here in 20% larger in comparison with the identical 9-month interval of 2022.

Suffice it to say, probably the most evident development within the firm’s near-term financials is the tempo at which bottom-line progress has been outpacing top-line progress. Though shares are for probably the most half priced on Wall Avenue on their earnings progress, sturdy gross sales progress additionally needs to be within the image to make sure sustained EPS progress can certainly proceed. In saying this, administration stays assured that vital prices (regarding commodity pricing & capital enhancements on its manufacturing facility) will proceed to be seen over time within the firm’s financials. Whereas this can be so, traders would like to see a extra diversified buyer base which consequently would convey much less threat to the corporate’s top-line gross sales numbers. We state this as a result of Armanino’s principal buyer continues to contribute properly over 50% of the corporate’s top-line gross sales at current.

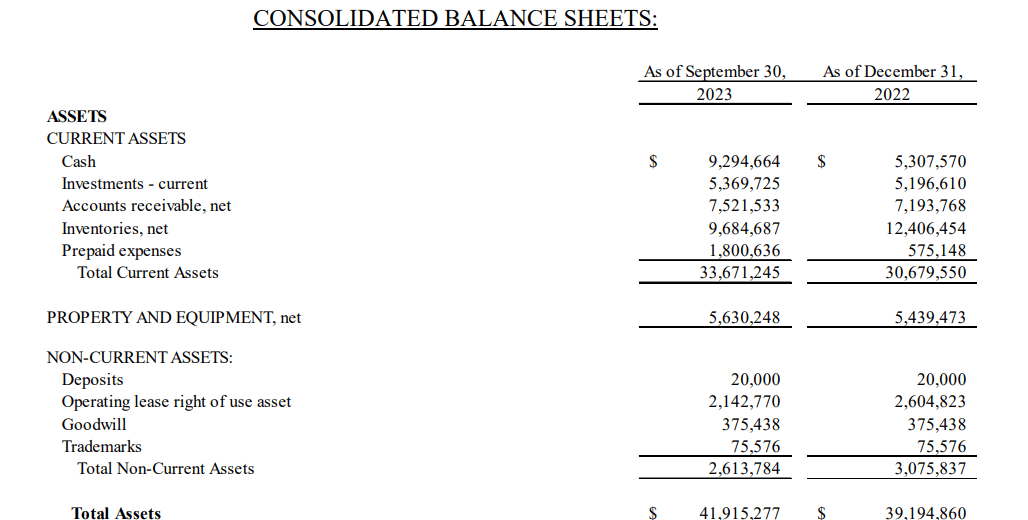

Regarding the stability sheet, contemplating the corporate’s sturdy liquidity (present ratio of three.04 within the newest quarter) & absence of interest-bearing debt (sturdy solvency), it’s not stunning to see sturdy developments in its property as we see under. A giant motive nevertheless for the numerous soar within the firm’s money stability over the previous three quarters was the $2.7+ million drop in stock over this era. A decrease stock rely on larger gross sales is superb for cash-flow technology so it will likely be attention-grabbing to see if this development can proceed over time. Accounts receivables have remained in test at simply over $7.5 million.

Armanino Stability Sheet (Property) (www.otcmarkets.com/otcapi/firm/financial-report/386290/content material)

Ahead-Wanting Expectations

Due to this fact, with a debt-free balance sheet and earnings progress most definitely happening in 2023, the query is whether or not Armanino is reasonable sufficient to warrant lengthy publicity at current. In impact, the worth of Armanino as an funding is predicated on its future earnings however since forward-looking progress charges are unattainable to foretell, we’ll go to the corporate’s conventional valuation multiples to see how they stack up towards the sector basically.

To get a way of the expansion path Armanino is at the moment endeavor, we’ll annualize the year-to-date 2023 numbers to get a learn on how low-cost the corporate’s gross sales, earnings & money movement are from a forward-looking foundation. After we annualize fiscal-2023 year-to-date top-line gross sales, internet earnings & working money movement, we get adjusted annual gross sales of $63.29 million, adjusted internet revenue of $8.25 million & adjusted annual working money movement of $10.55 million. Utilizing the current market cap of $152.24 million, we get the next adjusted multiples

| Valuation A number of | Adjusted 12-Month | Sector Median |

| Value To Gross sales | 2.4 | 1.15 |

| Value To Earnings | 18.45 | 21.26 |

| Value To Money/Move | 14.43 | 12.25 |

Though Armanino’s gross sales are costlier than the patron staples median, its earnings are at the moment trailing the typical. Nevertheless, once we have a look at the corporate’s stability sheet ($28.994 million reported on the finish of Q3), we see that Armarino’s property are overextended as the corporate’s trailing e-book a number of is available in at 5.25 versus a sector common of two.4.

What can we study from the above-adjusted multiples? Properly, property & gross sales are the important thing metrics that drive an organization’s earnings & gross sales over time. Due to this fact, for the value-minded long-term investor, it is smart to purchase an organization’s property & gross sales as cheaply as potential as valuation multiples many occasions revert to their long-term imply. Though short-term upside appears on the playing cards right here as a result of power of the inventory’s technicals, the corporate’s property look a tad dear which is why we reaffirm our ‘Maintain’ ranking on this play.

From a elementary standpoint, Armanino stays a powerful buyout goal as a result of progress triggers talked about above and powerful financials. If certainly a much bigger participant had been to return onto the scene, you then would really feel that the corporate would have the ability to obtain significantly better economies of scale and improve the corporate’s addressable market extra rapidly. If a buyout had been to not happen. What we see taking part in out is that if sturdy gross sales progress stays absent in upcoming quarters, we’ll see the inventory consolidate till its key valuation multiples catch up or ‘revert’ over time.

Conclusion

Due to this fact, to sum up, regardless of Armanino’s sound profitability, well-covered dividend & a number of progress triggers, the corporate’s property & gross sales look a tad overpriced at this level. Moreover, one would consider that larger ranges of income progress will probably be wanted over time to maintain these sturdy double-digit bottom-line progress charges intact. The inventory stays a ‘Maintain’ for us at current. We look ahead to continued protection.

Editor’s Word: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please pay attention to the dangers related to these shares.