Darren415

I wrote about Ascend Wellness (OTCQX:AAWH) in early November, saying it was no longer the cheapest MSO. The inventory was buying and selling at simply $1.00 then, and it now trades a lot increased. I prefer it, although! To be truthful, I appreciated it then too, however I used to be involved that it wasn’t as low cost to its friends because it had been.

On this follow-up, I evaluate the This autumn and 2023 monetary outcomes, talk about the outlook and the way it has modified, check out the chart and assess the valuation. Hopefully, the evaluation that I’m sharing will clarify why AAWH is presently 19% of my Beat the American Hashish Operator Index mannequin portfolio and now 6% of my Beat the World Hashish Inventory Index mannequin portfolio. I added it final week, together with a purchase order on Friday at $1.30.

Ascend Wellness Improved in 2023

Ascend Wellness grew web income by 28% in 2023 to $518.6 million. The gross margin fell from 33.1% to 29.9%. Fortuitously, its working bills expanded solely 12%, aided by the dearth of a settlement expense. Eradicating the $5 million cost from the 2022 outcomes, working bills expanded by 16%. Adjusted EBITDA for the yr expanded by 14% to $106.5 million. One of many greatest enhancements was in money stream from operations, which expanded to $75.3 million from -$38.4 million in 2022. Capital spending was$24.2 million, which means that the corporate generated free money stream. For 2024, the 10-Ok of the corporate included a forecast of capital spending of $35-40 million.

I like that Ascend Wellness is not in as many states as most of the different MSOs, because it offers them an opportunity to broaden or to be doubtlessly acquired by a bigger MSO. Many traders fail to understand that a number of states restrict the operators. Some prohibit the variety of dispensaries, and a few put a cap on the scale of the cultivation services.

Ascend, primarily based in NYC, operates in Illinois, Maryland (no cultivation), Massachusetts, Michigan, New Jersey, Ohio and Pennsylvania. It’s on the restrict of 10 dispensaries in Illinois, and it endured some challenges in 2023 as a result of Missouri legalization for adult-use. Two of its shops have been close to the Missouri border and benefitted from vacationer purchases.

Serving to Ascend in 2023 was the New Jersey legalization for adult-use, which was carried out in April of 2022. It expanded by acquisition in Maryland, which prolonged from medical to adult-use. Ohio is about to legalize for adult-use, and Pennsylvania might achieve this as properly.

One factor that I do not like about Ascend and plenty of of its friends is that they’ve substantial debt however unfavorable tangible guide worth. I believe that the debt might be tough to refinance. Ascend ended 2023 with web debt of $236 million. Its tangible fairness was -$126.1 million.

The Ascend Wellness Outlook Has Brightened

Forward of the This autumn report, analysts, in keeping with Sentieo, have been anticipating 2024 income to be $576 million. They have been forecasting adjusted EBITDA of $121 million. Now, the analysts predict income to develop 11% to $576 million nonetheless, however they challenge adjusted EBITDA will develop 17% to $124 million. The expansion projected this yr is increased for Ascend Wellness than its friends, as the common income progress for the Tier 1 and Tier 2 names is simply 4.5%, and Ascend has the best projected progress of those firms. Ascend has the second-highest projected adjusted EBITDA progress, and it’s properly above the common of 10%.

Two of the 9 analysts have been projecting 2025 income of $589 million with adjusted EBITDA of $139 million. Now 5 analysts count on income to develop 7% to $617 million.

Ascend Wellness Has an Enticing Chart

AAWH is up 29.5% to date in 2024. It is a bit forward of the New Hashish Ventures World Hashish Inventory Index, which has gained 26.0% up to now. AAWH was not a part of that index throughout Q1, nevertheless it has joined for Q2 on account of increased buying and selling quantity.

In comparison with MSOs, Ascend is trailing. The NCV American Hashish Operator Index, which incorporates it and a dozen different MSOs, is up 34.9% in 2024 via Q1.

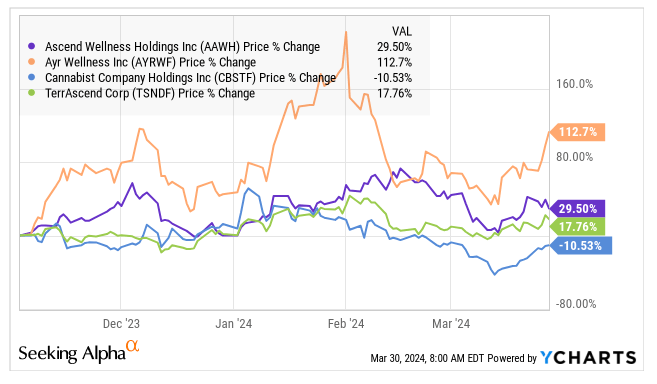

Wanting on the efficiency of Ascend relative to the three different Tier 2 MSO names since early November, it has trailed AYR Wellness (OTCQX:AYRWF) considerably. It has outpaced the opposite two:

YCharts

I like Cannabist (OTCQX:CBSTF), which bought a convertible observe not too long ago that weighed on the inventory. I wrote positively about TerrAscend (OTCQX:TSNDF), however I now not embody it in both of my mannequin portfolios.

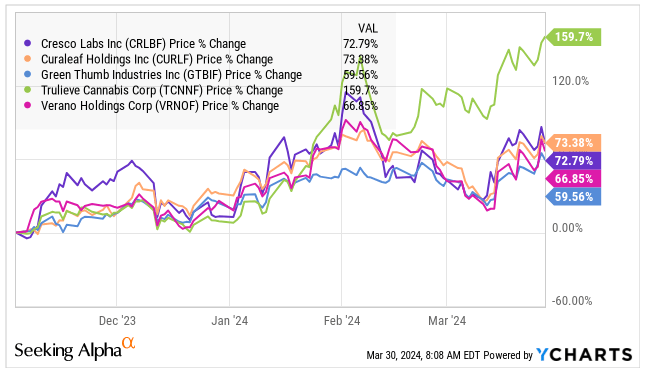

Wanting on the bigger friends, the 5 Tier 1 names have all carried out significantly better than AAWH since 11/3. The very worst title has returned greater than twice as a lot as Ascend Wellness:

YCharts

AdvisorShares Pure US Hashish ETF (MSOS) has rallied 70.2% since 11/3. Then, the ETF owned no AAWH. Now, it owns 1.9 million shares, which is simply 0.2% of the whole fund. It first purchased over 1 million shares in early February, when the inventory was a lot increased than it’s now.

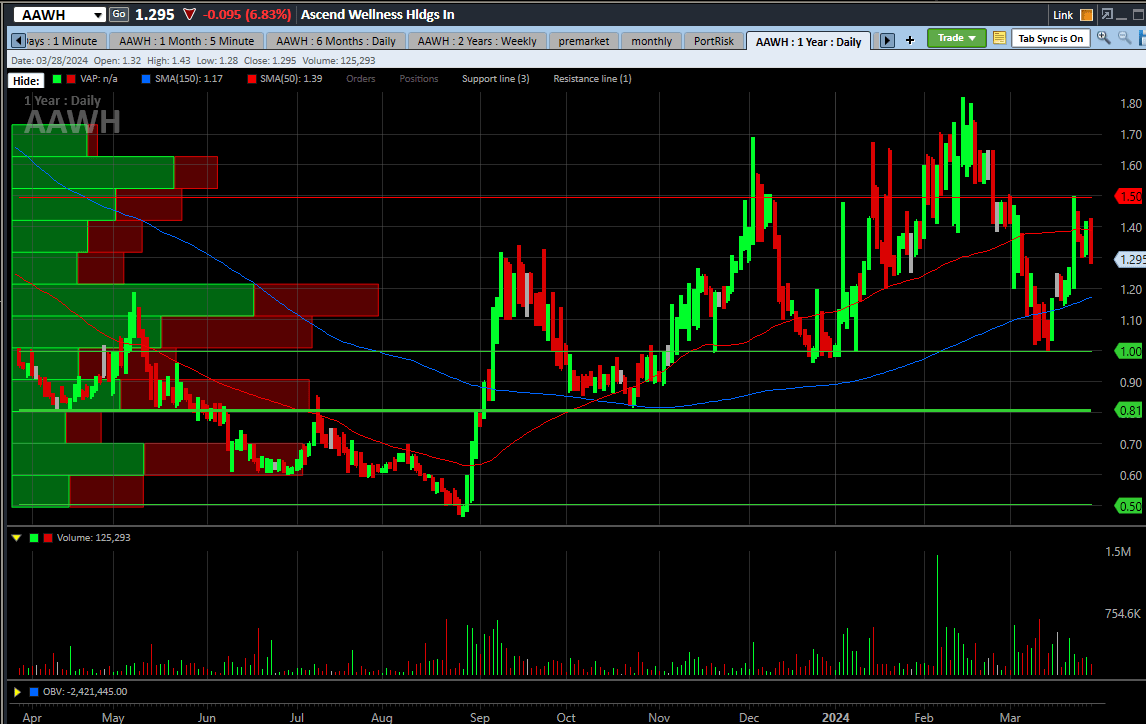

I believe the chart of Ascend is enticing, because it reveals increased lows and better highs, with very excessive quantity not too long ago:

Schwab

The large spike in quantity in early February is probably going associated to the acquisition by MSOS, however the quantity has remained comparatively elevated.

The inventory posted an all-time low in late August simply forward of the potential rescheduling information. It peaked in February and pulled again to $1.00, which appears to be like like strong assist for now. For now, I see $1.50 as potential near-term resistance.

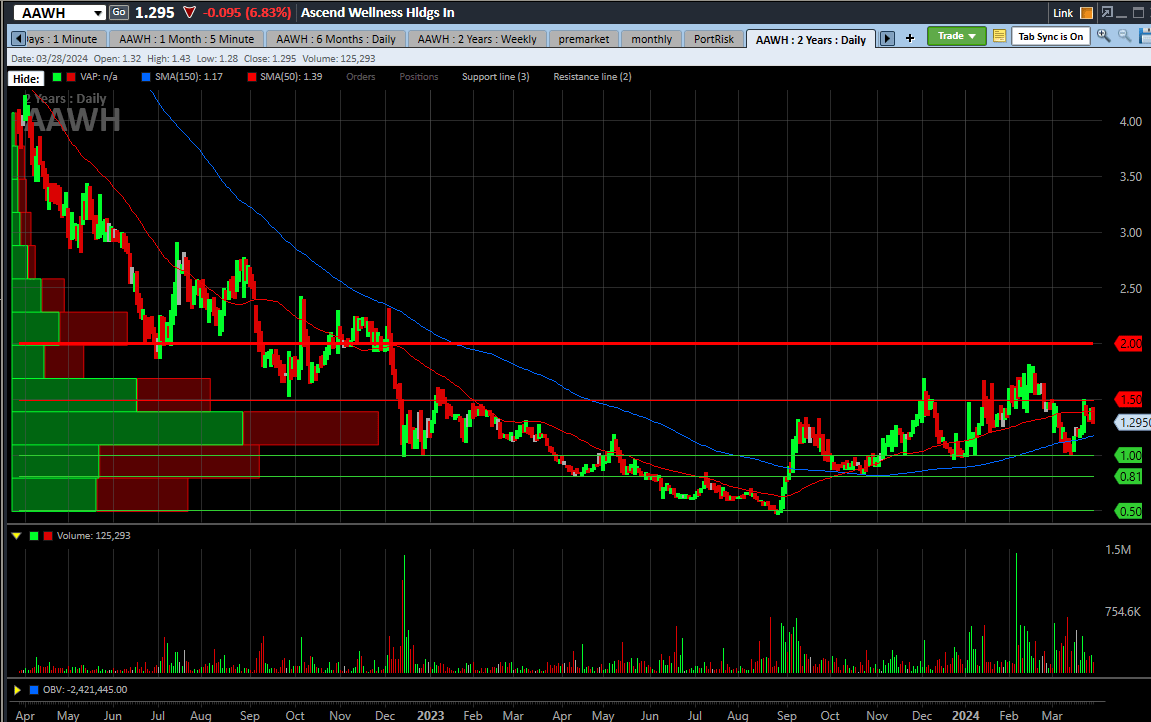

Having a look on the previous two years, the inventory continues to be down considerably:

Schwab

Because the finish of 2022, the inventory has rallied solely 12.6%, considerably lower than the 45.3% achieve within the American Hashish Operator Index.

Ascend Wellness Is Low-cost to MSO Friends Once more

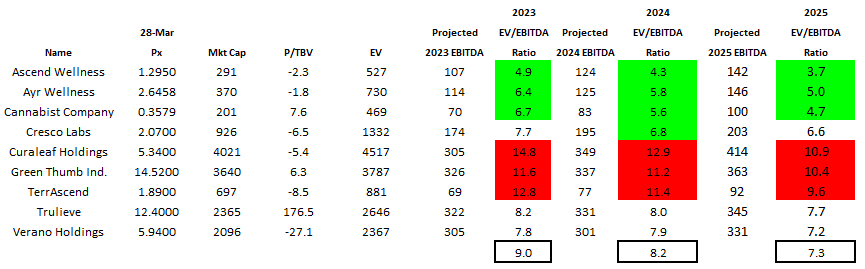

In November, I identified that Ascend, whereas low cost, now not stood out prefer it had previously. It had an enterprise worth to projected adjusted EBITDA for 2024 ratio of three.7X, the second-lowest of the 9 Tier 1 and Tier 2 firms. The common for the group at the moment was 5.5X.

Right here is the up to date information for each 2024 and in addition 2025:

Alan Brochstein, utilizing Sentieo

For 2024 estimates, Ascend is now the most affordable at 4.3X. The common is now a lot increased than earlier than at 8.2X. The AAWH estimates have elevated, although lower than its value. Its friends, although, have seen decreases of their adjusted EBITDA estimates and far increased costs.

For 2025, Ascend can also be the most affordable at simply 3.7X. The common is 7.3X, If hashish is rescheduled to Schedule 3, then the 280E tax shall be eradicated. This may be an excellent factor for the MSOs, and it might enable valuations to broaden.

Forward of the This autumn report, I shared a set of year-end 2024 targets with members of my investing group. My optimistic goal, assuming 280E goes away, was $3.89, and my pessimistic goal was $0.78. Updating these targets utilizing the identical metrics, I now get an optimistic goal, primarily based on an enterprise worth of 8X projected 2025 adjusted EBITDA, of $4.00. This may be a rally of 209%. My pessimistic goal, primarily based on a decline to 3X, could be $0.84, representing a possible decline of 35%. It is a lot higher than its friends.

Conclusion

Ascend has rallied rather a lot since early November, nevertheless it has rallied lower than its MSO friends. The inventory appears to be like comparatively low cost to them. How rescheduling performs out will extremely influence its return, however I prefer it sufficient to incorporate it in my mannequin portfolios.

I’ve mentioned the enticing chart and a budget valuation relative to friends. It’s now within the World Hashish Inventory Index that I’m attempting to beat in my mannequin portfolio, and I’m a bit chubby relative to that index.

The most important threat to AAWH and its friends is that if 280E doesn’t go away. AAWH has a unfavorable tangible guide worth and substantial debt, as I’ve mentioned, and these would strain the inventory. One other threat is that Pennsylvania, anticipated by many to maneuver past medical hashish to adult-use, doesn’t achieve this.

Two weeks after I wrote the piece on Ascend, I reiterated my bullishness on Trulieve (OTCQX:TCNNF), which was then $5.61, up from the $4.775 value once I assessed Ascend. It has greater than doubled! I not too long ago downgraded TCNNF to a “Sell”. I believe AAWH is a superb substitute for TCNNF, which has less upside and more downside than Ascend Wellness.

So, whereas I’m not a lot of a fan presently of the MSOs on account of my worry that traders have gotten overly enthusiastic about one thing that will not occur, I charge this MSO as a Purchase.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please pay attention to the dangers related to these shares.