SweetBunFactory

Ashland (NYSE:ASH) affords specialty components and components worldwide. ASH not too long ago introduced This fall FY23 and FY23 outcomes. They struggled in FY23 resulting from a destocking concern, which is predicted to have an effect on them in FY24. So, the outlook for FY24 isn’t that constructive, and its valuation appears excessive. So, I believe ASH could be unable to supply their buyers any worth. So, contemplating the chance, I assign a promote ranking on ASH.

Monetary Evaluation

ASH not too long ago posted This fall FY23 and FY23 results. The gross sales for This fall FY23 had been $518 million, a decline of 18% in comparison with This fall FY22. The gross sales from its life sciences, specialty components, private care, and intermediates segments noticed a decline, which led to the poor efficiency of the corporate by way of gross sales. The gross sales from the life sciences, specialty components, private care, and intermediates segments declined by 5%, 23%, 22%, and 42% in This fall FY23 in comparison with This fall FY22. All of the segments had been affected by buyer stock destocking, which led to a decline in gross sales. The gross margin additionally declined, and the decline was as a result of stock actions taken by the corporate resulting from low demand. The online loss for This fall FY23 was $4 million in comparison with a internet revenue of $57 million in This fall FY22.

The annual numbers had been additionally weak. The FY23 gross sales had been down 8% in comparison with FY22, and the revenue from continued operations additionally declined 7.1%. The quarterly and annual outcomes had been disappointing, and the destocking concern affected them extra within the second half. The destocking concern didn’t have an effect on them a lot within the first half, but it surely was aggravated within the second half. The corporate is experiencing softness in demand, particularly in Europe and China. The corporate expects the destocking concern to final till Q2 FY24, however that may be the best-case situation. It could actually additionally prolong additional than that. One factor that considerably offset the destocking concern was the excessive pricing. The corporate loved excessive pricing in This fall FY23, which I imagine generally is a matter of concern for FY24. Presently, the demand throughout markets is low, and nobody can assure that the corporate will proceed to get pleasure from excessive pricing. So, if they don’t seem to be in a position to get pleasure from excessive pricing, then it may be worse for them. So, the way forward for ASH in FY24 appears unsure.

Technical Evaluation

Buying and selling View

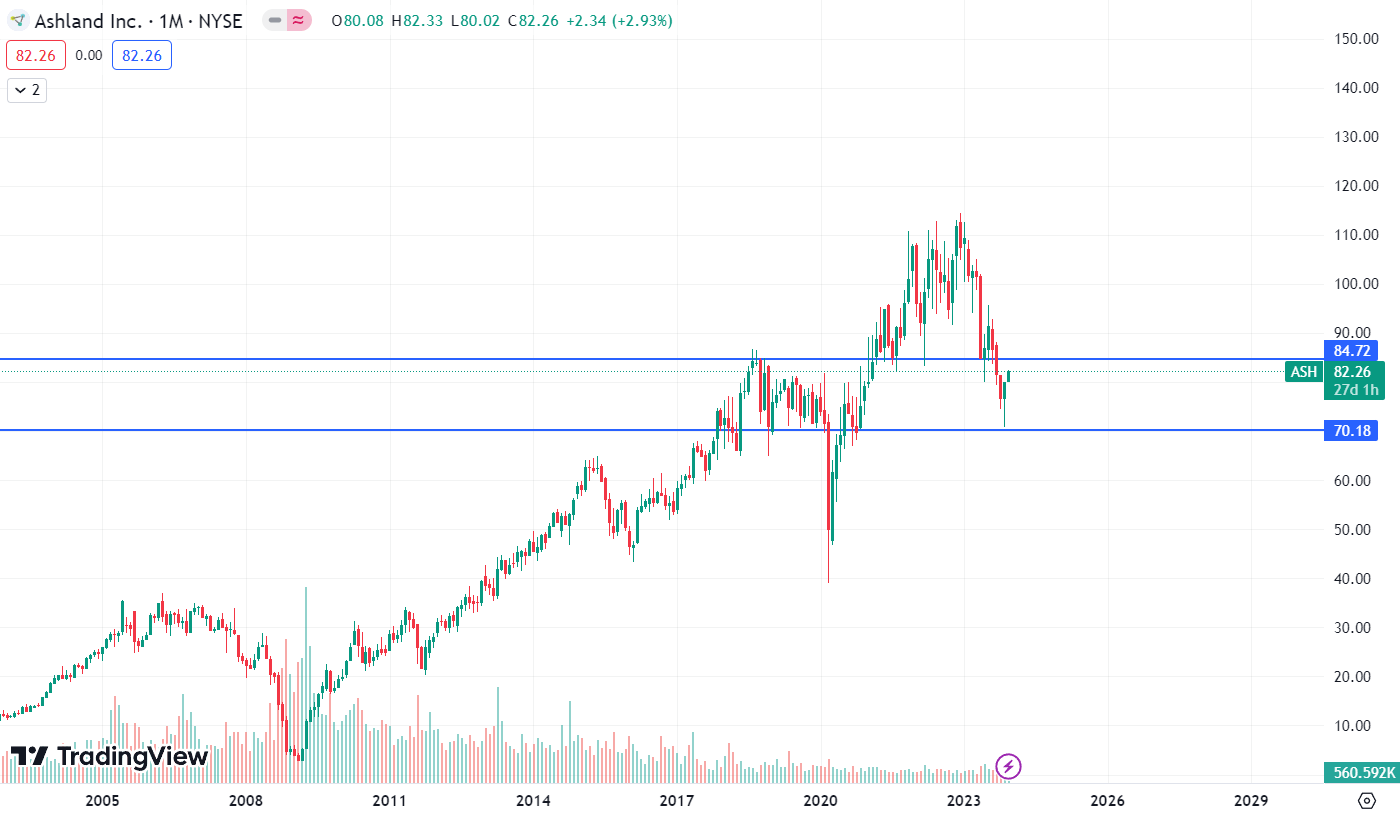

ASH is buying and selling at $82.2. ASH’s worth chart would not look good. In September, the worth broke down under the $85 stage, which was an necessary help zone for the inventory. After giving the breakdown, the inventory is returning to retest the $85 stage. So, the setup made right here is bearish, and after the retest is finished, there’s a excessive probability that the inventory would possibly proceed its downward trajectory. The following help zone for the inventory is at $70. So there’s a excessive probability that it’d attain $70 within the coming occasions. Therefore, contemplating the bearish worth motion, I’d advise to keep away from investing in ASH.

Ought to One Make investments In ASH?

After three years of constructive gross sales progress, they struggled to develop their gross sales in FY23, and with the steering supplied by the administration and looking out on the headwinds, I believe they could proceed to wrestle in FY24 by way of progress. The anticipated gross sales for Q1 FY24 are round $480 million, which is 8.5% decrease than Q1 FY23. So, the anticipated weak spot in FY24 can adversely have an effect on ASH’s share worth. Moreover, the present valuation of ASH appears costly. ASH is buying and selling at a P/E [FWD] ratio of 26.86x in comparison with the sector median of 16.87x, and contemplating its efficiency, I believe ASH is overvalued. Its EPS [FWD] is $3.83, and contemplating its outlook for FY24, I believe it might commerce round a P/E of 19x. So, it offers us a worth goal of $72.7, which is round 11% decrease than the present share worth. So, contemplating the poor outcomes, overvaluation, and not-so-positive outlook for FY24, I assigned a promote ranking on ASH.

Danger

Rising and unstable costs for uncooked supplies, significantly for wooden pulp, cotton linters, and hydrocarbon derivatives, might hurt Ashland’s working bills, operational efficiency, and stock valuation. Equally, power bills play an enormous position in a number of of Ashland’s product prices. Ashland’s capability to move on the prices of worth rises is reliant on market circumstances, and it isn’t all the time in a position to increase costs in response to such rising prices. Equally, decreases in Ashland’s stock valuation introduced on by market volatility may not be made up for and would possibly even trigger losses.

Ashland purchases particular items and uncooked supplies from distributors, incessantly in accordance with formal provide agreements. Ashland could be unable to make alternate provide preparations if these suppliers determine to cancel or fail to meet contractual obligations or if they can’t fulfill Ashland’s orders in a well timed method. Moreover, Ashland might discover it troublesome to accumulate some uncooked supplies on commercially acceptable circumstances resulting from nationwide and worldwide authorities guidelines pertaining to the manufacturing, delivery, or import of explicit uncooked supplies. Clary sage, aloe, guar, and cotton linters are agricultural merchandise which might be very important to a number of Ashland industries. Crop yields, meteorological circumstances, and different components can considerably affect the supply of those assets.

Backside Line

ASH posted poor This fall FY23 and FY23 outcomes. The gross sales had been down considerably, and the outlook for FY24 is weak. It would wrestle financially in FY24, and its valuation appears costly. Contemplating these components, I believe ASH may not be capable of present any worth to its buyers within the coming quarters. So I assign a promote ranking on ASH.