Pixelimage

We beforehand coated ASML Holding N.V. (NASDAQ:NASDAQ:ASML) (OTCPK:ASMLF) in January 2024, discussing why we consider that its 2024 commentary had been on the cautious facet, with a number of Huge Tech corporations and information heart REITs nonetheless reporting rising urge for food for cloud computing/ generative AI providers and infrastructure associated spending.

Nevertheless, with the inventory already recording huge recoveries because the current October 2023 backside, we had additionally really useful traders to attend for a extra enticing entry level for an improved upside potential.

Since then, ASML has charted one other +39.8% rally, properly outperforming the broader market at +9.1%. Regardless of so, we will focus on why it stays a long-term winner as we enter the subsequent cloud tremendous cycle, due to the insatiable demand for generative AI SaaS and Nvidia’s (NVDA) double digit progress.

Regardless of its rising bookings and multi-year backlog, readers might need to look forward to a reasonable retracement for an improved margin of security, since many of the exuberance has additionally been embedded right here.

The ASML Lengthy-Time period Funding Thesis Stays Promising, Albeit Inflated At Present Ranges

With ASML set to report the FQ1’24 earnings on April 17, 2024, all eyes will probably be on the administration, on whether or not it is going to be in a position to proceed the consecutive earnings beat since 2010, apart from the one-time top-line miss in 2021.

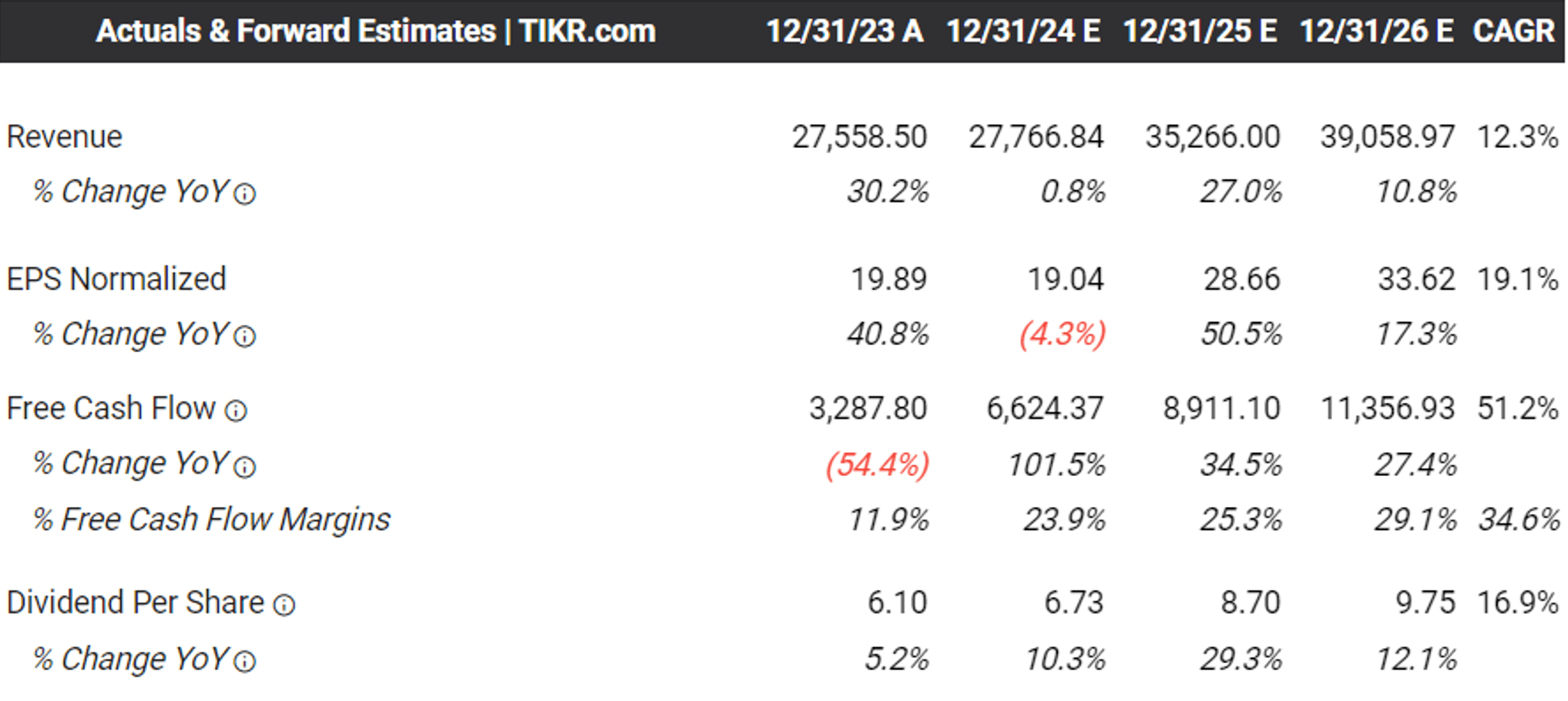

For context, the lithography firm reported a stellar FY2023 sales of €27.55B (+30.1% YoY) and adj EPS of €19.91 (+40.8% YoY), with spectacular internet bookings of €20.04B (-34.6% YoY) and multi-year backlog of €39B (-3.4% YoY).

These numbers indicate the sturdy demand for ASML’s market-leading choices, regardless of the supposed competition from Canon (OTCPK:CAJPY) (OTCPK:CAJFF).

The latter has reported stagnant Industrial sales of 314.7B Yen (-4.4% YoY) in FY2023, with the unit gross sales progress for semiconductor lithography tools negated by the weak demand for FPD lithography tools.

If something, the US authorities has just lately confirmed $39B in CHIPs Act Subsidies, with:

- Intel (INTC) set to obtain $8.5B in subsidies/ $11B in loans,

- Taiwan Semiconductor Manufacturing (TSM) $6.6B in subsidies/ $5B in loans,

- Samsung Electronics (OTCPK:SSNLF) (probably) $6B in subsidies, and

- Micron (MU) (probably) $5B in subsidies, amongst others.

With the final word goal of boosting home manufacturing of semiconductors, it goes with out saying that ASML would be the primary beneficiary of those grants, since most (if not all) foundries should order lithography tools to help their new manufacturing crops.

This additionally explains why ASML has reported accelerating progress in net bookings to €9.18B by FQ4’23 (+253% QoQ/ +45.7% YoY), comprising €5.6B of EUV bookings (+1020% QoQ/ +64.7% YoY) and €3.6B of non-EUV bookings (+71.4% QoQ/ +24.1% YoY).

Regardless of the lack of profitability at the moment reported by INTC’s foundry section or TSM’s ability to “enable almost all AI processing at the data center and the edge,” it’s simple that their capex will probably be elevated over the subsequent few years, with a part of it attributed to ASML’s lithography tools.

Most notably, the Reminiscence section has additionally reported growing reserving share at 47% (+27 factors QoQ/ +13 YoY), in comparison with Logic at 53% (-27 factors QoQ/ -13 YoY) in FQ4’23.

These numbers are attention-grabbing certainly, since it’s obvious that the reminiscence market is recovering by leaps and bounds, as equally reported by MU within the current earnings name.

That is attributed to the insatiable demand for generative AI SaaS, which requires immense “storage solutions that may deal with huge volumes of knowledge, ship excessive throughput, provide low-latency entry, and retailer information securely.”

On account of the renewed progress alternatives submit hyper-pandemic interval, we consider that ASML might very properly report accelerating internet bookings and backlogs within the upcoming FQ1’24 earnings name, with gross sales more likely to be gated by supply timing and capability.

That is attributed to the administration’s comparatively smooth FQ1’24 internet gross sales steerage of €5.25B (-27% QoQ/ -21.6% YoY) and gross margins of 48.5% (-2.9 factors QoQ/ -2.1 YoY) on the midpoint, with “flattish sales growth in 2024.”

In an effort to meet its rising backlog, readers should additionally be aware that the corporate is anticipating to incur vital capex in 2024 to ramp up its manufacturing capability to 90 EUVs and 600 DPVs.

As we enter the subsequent cloud tremendous cycle, we consider that these investments will finally be accretive to ASML’s high/ backside traces, whereas widening the hole in its 20Y lithography moat.

The Consensus Ahead Estimates (€)

Tikr Terminal

The identical has been projected by the consensus, with ASML anticipated to generate an accelerated high/ backside line progress at a CAGR of +12.3%/ +19.1% by FY2026.

That is in comparison with the earlier estimates of +8.4%/ +16.6%, whereas constructing upon the historic enlargement at +22.1%/ +28.5% between FY2016 and FY2023, respectively.

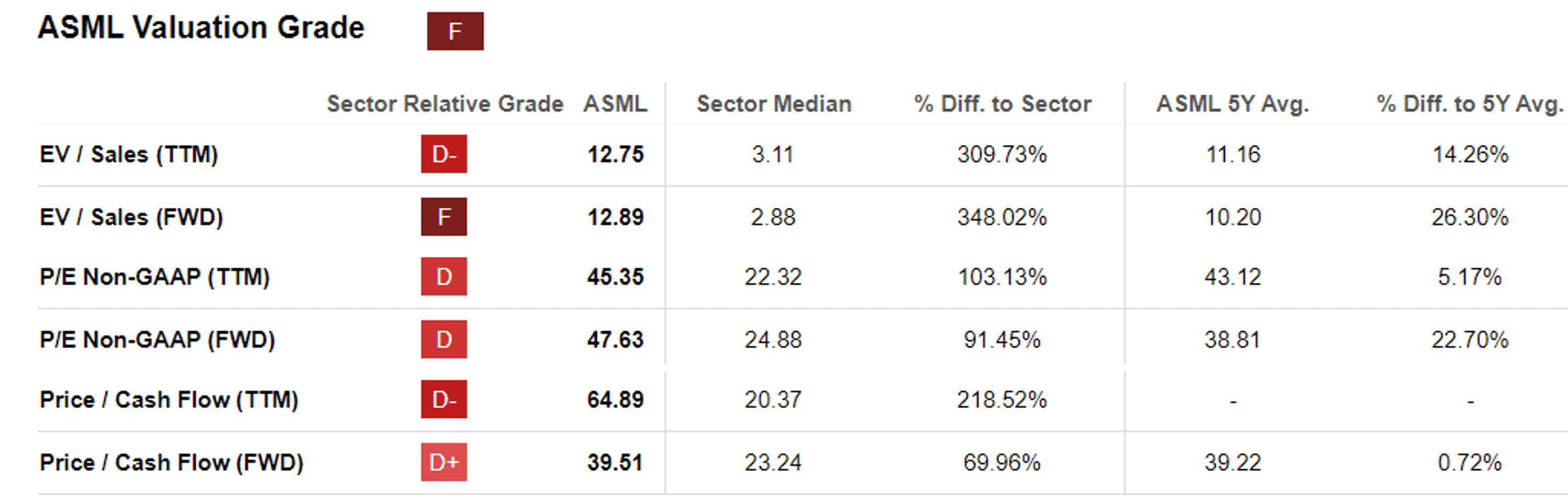

ASML Valuations

In search of Alpha

On account of the long-term tailwinds, it’s obvious that the market has opted to improve ASML’s FWD P/E valuations to 47.63x and FWD Value/ Money Circulate valuations to 39.51x, with it being second to none within the “very high-end semiconductor lithography equipment market.”

Nonetheless, we aren’t sure whether it is sensible to award this overexuberance within the inventory, in distinction to its 1Y imply of 35.55x/ 36.90x and 3Y pre-pandemic imply of 26.50x/ 29.30x, respectively.

Even when in comparison with its peer, Canon at 15.68x/ 9.06x, it’s obvious that ASML could also be somewhat costly right here, particularly because the latter is already buying and selling close to its hyper-pandemic peak valuations of 52.30x/ 56.87x, respectively.

So, Is ASML Inventory A Purchase, Promote, or Maintain?

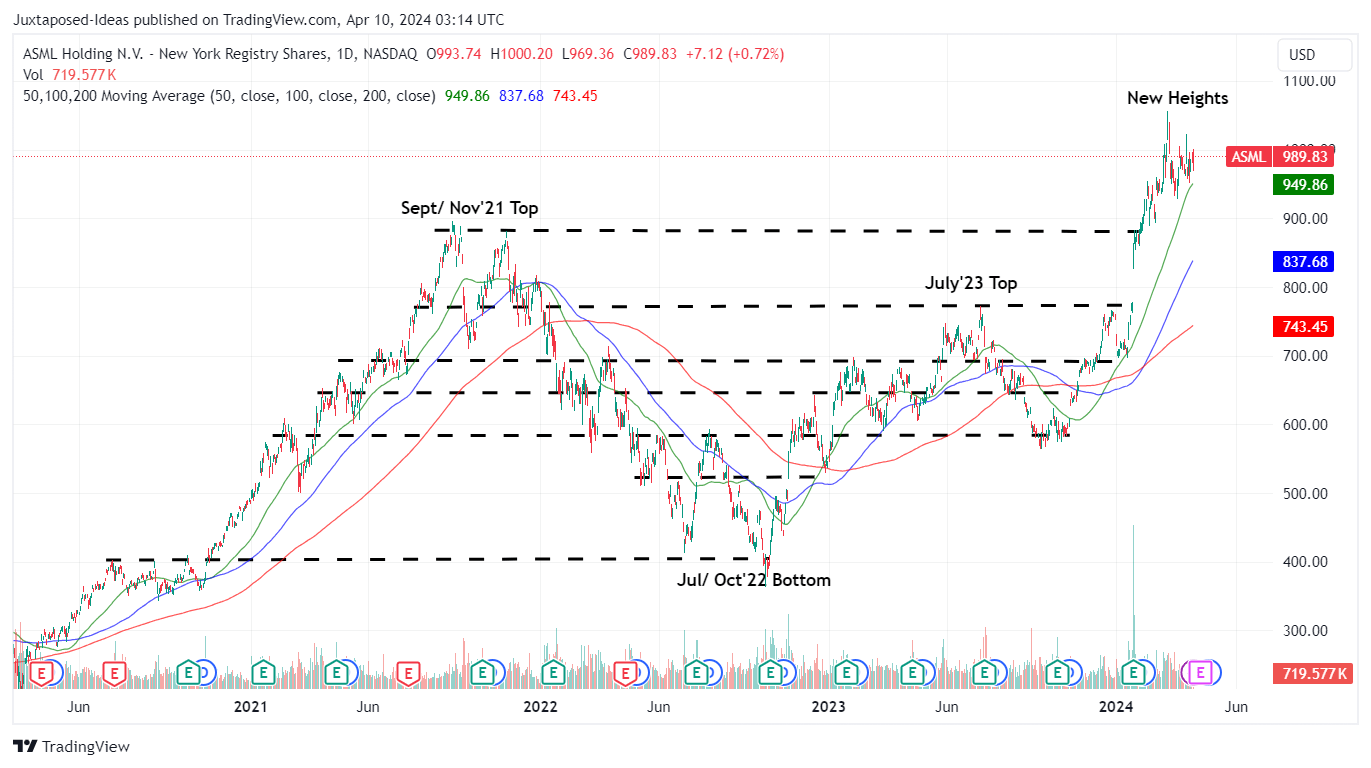

ASML 5Y Inventory Value

Buying and selling View

The identical over optimism can also be noticed in ASML’s inventory costs, with it at the moment charting new heights whereas working away from its 50/ 100/ 200 day transferring averages.

Based mostly on its 1Y P/E imply of 35.55x and the FY2023 adj EPS of $21.65, it’s obvious that the inventory is buying and selling manner above our truthful worth estimates of $769.60.

Whereas there stays a wonderful upside potential of +30.3% to our long-term value goal of $1.29K, primarily based on the consensus FY2026 adj EPS estimates of $36.50, we consider that there’s a minimal margin of security right here.

Whereas we might proceed ranking ASML as a Purchase, attributed to its brilliant long-term prospects, readers might need to time their entry factors, ideally after a reasonable retracement to its earlier buying and selling vary of between $770s and $880s.

We consider that these ranges might materialize ahead of anticipated, with the broader market already buying and selling sideways over the previous three weeks as we enter the Q1’24 earnings season.

Relying on how the tech and semiconductor shares carry out, there could also be reasonable volatility forward, particularly since ASML has recorded a YTD rally of +30.7% in comparison with the wider-market at +9.2%. Persistence for now.