Pituk Loonhong/iStock through Getty Pictures

Please word all $ figures in $CAD, not $USD, until in any other case acknowledged.

Introduction

I lately covered Hydro One (H:CA) and instructed that the corporate was seemingly the worst regulated utility in Canada having greater leverage, a poor dividend yield, and an costly valuation. At this time, I will be protecting one other utility, ATCO Ltd. (OTCPK:ACLTF) (OTCPK:ACLLF) (ACO.X:CA), and I am going to clarify why I consider it to be far superior and among the best energy and utility firms in Canada.

Firm Overview

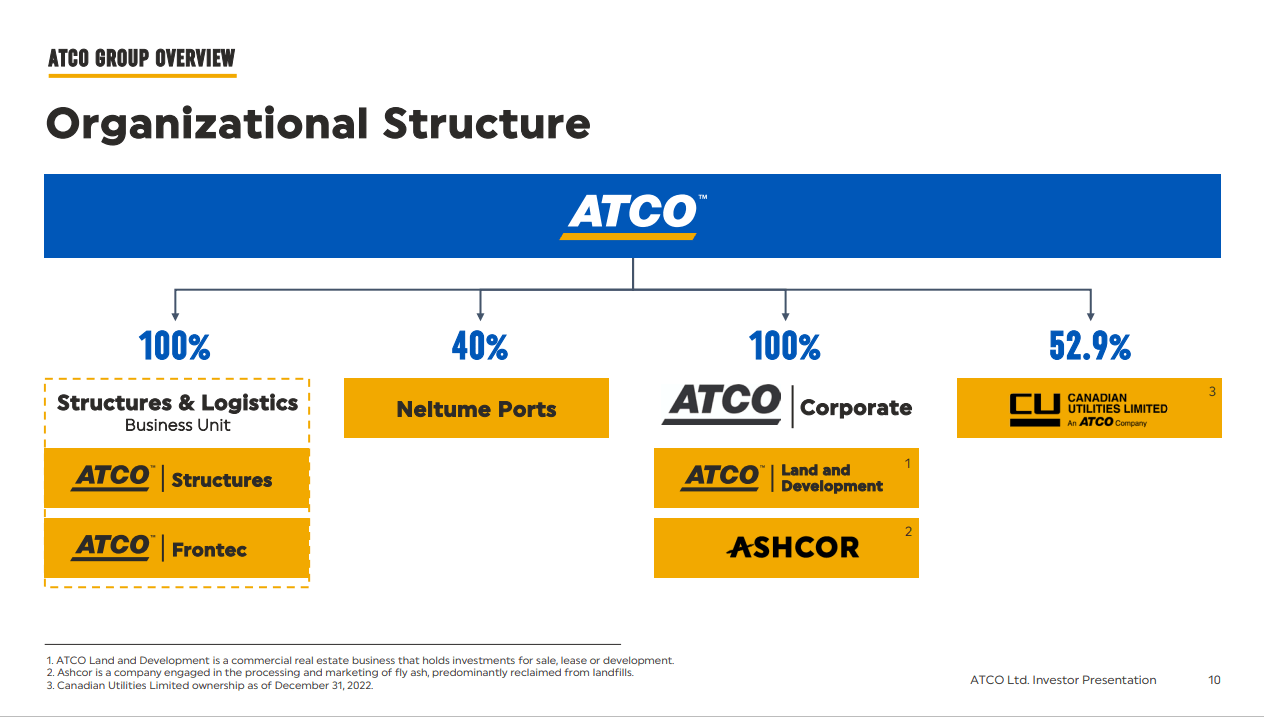

ATCO is a diversified Canadian firm that is not only a utility. Based mostly out of Alberta, it owns a stake in Canadian Utilities (CU:CA), which is concerned within the era of electrical energy by way of hydro, photo voltaic, wind, and pure fuel. By its 52.9% stake in Canadian Utilities, it additionally does transmission, distribution, and storage for pure fuel as properly as related providers for water.

ATCO additionally has a Buildings and Logistics enterprise that does workforce housing, house leases, everlasting modular building, manufacturing options, and operational assist providers. It additionally owns a 40% curiosity in Neltume Ports, which is a port operator that does bulk and container cargo in South America.

Lastly, by way of its company section, it owns ATCO Land and Improvement which has actual property pursuits in 11 industrial actual property properties, 20,000 sq. ft of commercial property, and 315 acres of land. Additionally in its company section is Ashcor which does repurposing of ash (each reside ash and ash reclaimed from landfills) that is used for prepared blended concrete, oil properly servicing, soil stabilization, and curler compacted concrete.

ATCO Organizational Construction (Investor Presentation)

As you may see, ATCO is a really diversified firm with many various companies. Breaking the enterprise segments down to provide a relative measurement of every, the Canadian Utilities stake accounts for 82.3% of adjusted earnings, the constructions and logistics enterprise accounts for 14.4%, and Neltume Ports accounts for simply 3.3% of adjusted earnings. As an organization, whereas ATCO has a dominant presence in Canada (84% of its revenues), the corporate additionally has worldwide publicity, primarily in Australia by way of its Buildings and Logistics enterprise, but in addition in South America by way of Neltume Ports.

Funding Thesis

ATCO hasn’t’ launched full fiscal 2023 outcomes (we should always anticipate to see This fall outcomes someday in February) however let’s check out the newest quarterly outcomes for Q3 to get a greater sense of the latest enterprise efficiency.

In its Q3 outcomes, whereas ATCO missed on its income goal by about $100 million (quarterly revenues got here in at $1.06 billion), ATCO reported a beat in EPS of $0.71, above consensus estimates of $0.63. The quarterly revenue determine was down about 8% 12 months over 12 months with EPS down about 7% 12 months over 12 months.

As you would possibly anticipate with a really massive stake in Canadian Utilities making up the majority of the earnings energy of ATCO, a lot of reason for the decline was attributable to softer numbers out of Canadian Utilities, however we did see very sturdy development within the Buildings and Logistics section.

For Canadian Utilities, the weak point might be attributed to the Alberta rebasing which put strain of earnings along with the Australian pure fuel distribution enterprise experiencing some destructive impacts on account of moderating inflation contrasted to greater charges seen in 2022. General although, with a Web Debt to EBITDA ratio of 4.7x and spitting off a 6.1% dividend yield on an 80% payout ratio, Canadian Utilities stays a free money circulation machine with minimal disruption danger.

A part of the explanation I like ATCO over Canadian Utilities is as a result of its extra diversified and also you get the advantages of getting extra diversification and higher development in its different working companies.

Within the Buildings and Logistics enterprise for instance, we noticed adjusted earnings of $28 million, which was a rise of about 56% in comparison with Q3 2022. As you would possibly anticipate, income and earnings might be fairly lumpy as a result of cyclicality of the enterprise however over time has been rising sooner than Canadian Utilities.

Smoothing out the earnings, it may be useful to have a look at the economics of the enterprise to get a way of how the Construction’s enterprise is performing. When analyzing the house leases and workforce housing companies, ATCO noticed a rise of 9% and 15% of their house leases fleet measurement and common rental charge, respectively. What this reveals in my opinion is these elements have been what been resulting in ATCO doubling the Buildings and Logistics section of the enterprise to virtually a billion in revenues over the past 5 years. Rising at a 14% CAGR, I would not anticipate this development charge to proceed however I do not see why a excessive single digit development charge in income plus a number of hundred foundation factors of margin growth as the corporate turns into extra environment friendly cannot be achieved.

Along with the Buildings and Logistics enterprise, I feel there’s additionally purpose to be excited in regards to the development alternatives at Neltume Ports as properly. For instance, throughout the quarter, the section grew by $3 million to $7 million for the quarter in comparison with final 12 months. Whereas a good chunk of the earnings development might be attributed to favorable alternate charges (recall that Neltume Ports operates in South America), the elevated possession at two of its privately owned terminals helped contribute to greater earnings. One catalyst for Neltume Ports that I look ahead to seeing is a three way partnership with Solvay (a significant participant within the within the soda ash house) which is basically a JV that may see the 2 firms work to construct a terminal that may have capability to export greater than 2.5 million tonnes of soda ash per 12 months.

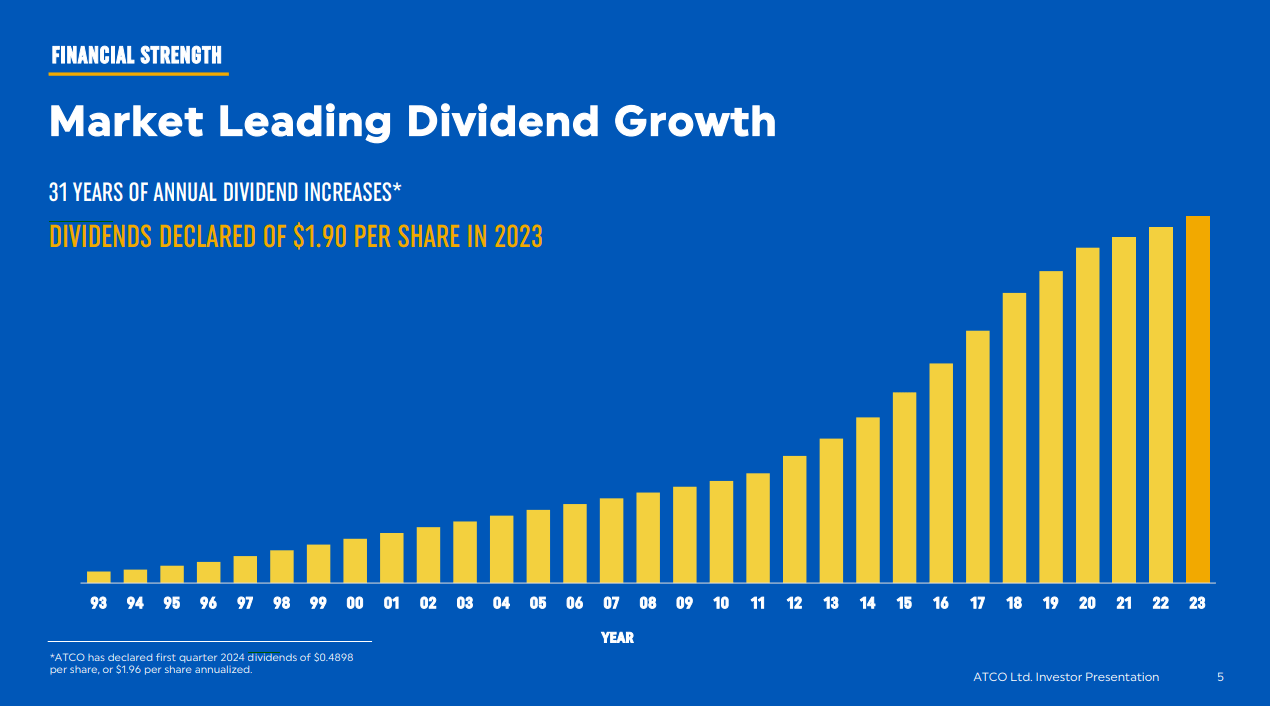

Earlier this month, ATCO additionally announced a dividend enhance of about 3% to $0.4898 per share, up from the earlier $0.4756 per share earlier than. This dividend demonstrates the corporate’s dedication to common dividend will increase and returning extra money to shareholders.

In truth, with the dividend enhance, this now marks over 30 years of constant yearly will increase within the annual dividend. There’s not many Canadian firms who’ve been in a position to obtain that, making ATCO a really enticing dividend inventory for revenue traders and retirees. At current, the present dividend represents a few 5.1% yield. Add one other 2-4% annual development in long-term capital appreciation and I feel you’ve got bought a comparatively protected dividend grower that might be a strong addition to a well-diversified portfolio.

Dividend Progress Historical past (Investor Presentation)

A 5% yield plus 2-4% of yearly capital appreciation may not sound like a lot, however close to time period I consider the valuation appears very enticing. Very like Financials and Actual Property, Utilities as a sector have been out of favor lately on account of rate of interest pressures and total sector rotation (know-how and excessive beta shares bought crushed in 2022 adopted by a robust rebound in 2023).

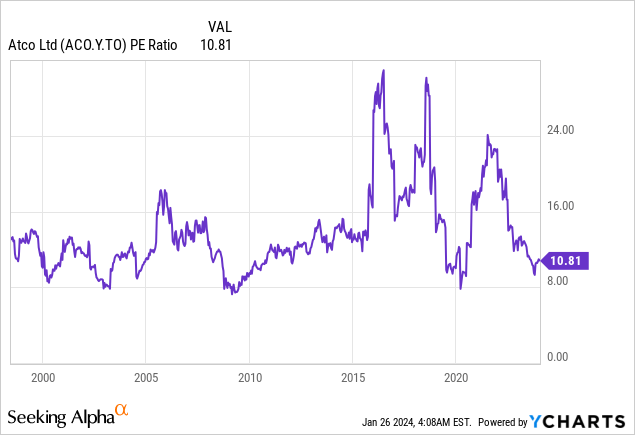

After we have a look at ATCO’s valuation, we will see that the corporate is buying and selling on the low-end of its historic EV/EBITDA vary at about 10.8x Value to Earnings (or about 10.1x adjusted). Wanting on the ahead P/E, the corporate appears extra enticing at 9.3x 2024 earnings and 9.0x 2025 earnings (suggesting future earnings development). So on the present valuation, I feel you may make the case that with utilities out of favor, you’ve got bought a fairly good margin of security at this a number of.

When the remainder of the peer group, we will see that ATCO has among the best valuations round; the bottom of the Canadian peer group. With a greater AFFO yield than Canadian Utilities, the market is at the moment suggesting that it expects the remainder of ATCO’s non-utility property to develop slower, however that is merely been unfaithful and is prone to proceed rising given latest developments. Furthermore, with a Web Debt to EBITDA ratio 4.7x, there’s much less danger in comparison with the peer group contemplating that ATCO carries much less debt in its capitalization construction with a Web debt to complete capitalization ratio of 54%. So total, with a greater valuation, greater dividend yield, and decrease leverage on the stability sheet, ATCO appears much more enticing in comparison with its friends within the energy and utility house.

Creator, based mostly on TD estimates

Based mostly on the six sellside analysts who cowl ATCO’s inventory, there are 3 purchase and three maintain scores on the inventory. The typical value goal $45.17, with a excessive estimate of $49.00 and a low estimate of $38.00. From the present value to the typical value goal one 12 months out, this suggests potential upside of twenty-two.2%, not together with the present dividend yield of 5.1%. So this means that analysts are fairly bullish on ATCO’s inventory.

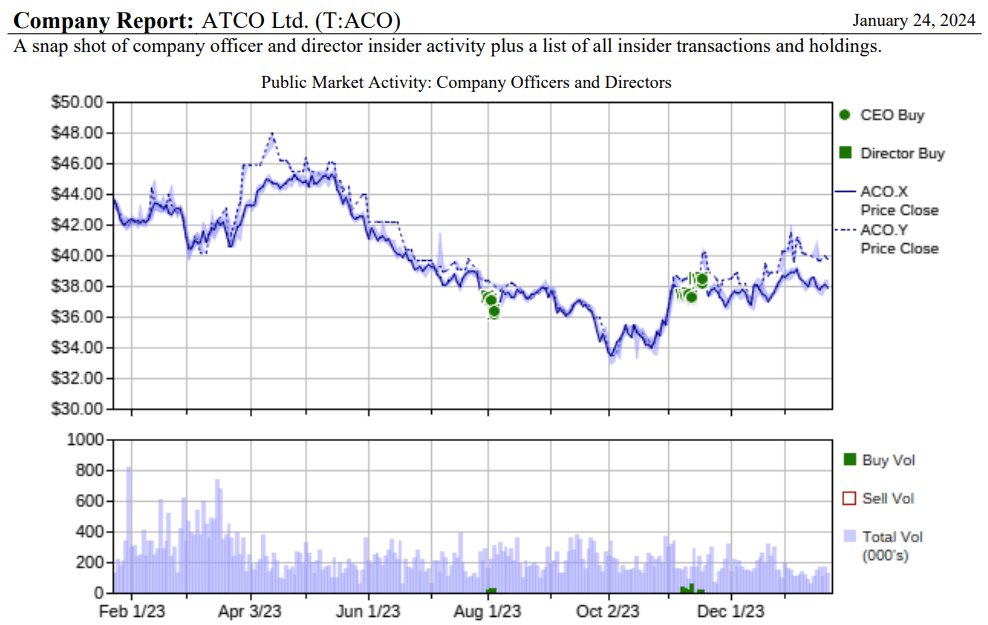

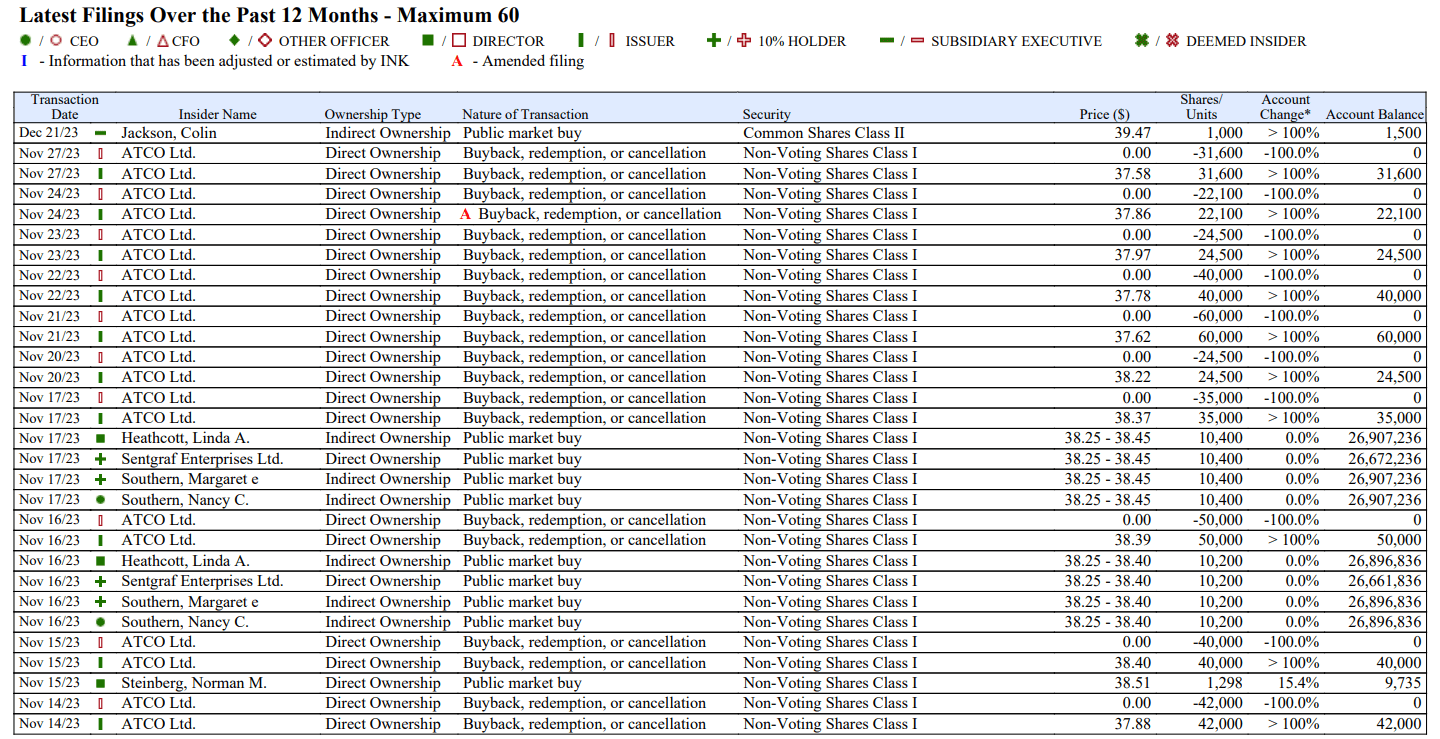

It will additionally appear that administration can also be bullish on the corporate’s long-term future outlook. With the CEO shopping for shares within the open market on the sub-$40 degree, it could appear administration is placing its cash the place its mouth is and shopping for shares themselves. Because the saying goes, administration can promote for a lot of causes however there’s solely purpose they purchase.

Public Market Buys (INK Analysis) Administration Shopping for Inventory (INK Analysis)

When it comes to the dangers for investing in ATCO’s inventory, one wants to think about the focus of the Canadian Utilities stake as a p.c of its complete adjusted earnings. When you’re bullish on ATCO, you’ll be de facto bullish on Canadian Utilities, so an investor also needs to take into account the potential of proudly owning Canadian Utilities over ATCO. For me although, I like ATCO given the diversification, greater development, and higher valuation, however the trade-off is perhaps the upper yield of Canadian Utilities.

Conclusion

In abstract, ATCO stays my prime choose within the Canadian energy and utilities house. You get the advantages of getting a 53% stake in Canadian Utilities in your fundamental publicity on the inventory, but in addition the industrials enterprise that manufactures modular buildings and gives website assist providers, and an curiosity in a ports enterprise. I like this diversification as a result of it gives you a bit bit extra development whereas sustaining stability by way of the constant efficiency of Canadian Utilities. ATCO’s Buildings and Logistics section, with its notable development in adjusted earnings, highlights this properly as ATCO has potential to broaden past simply conventional utilities. The latest dividend enhance underscores ATCO’s dedication to shareholders, making it a compelling selection for revenue traders and retirees. Moreover, with the inventory’s present valuation buying and selling on the decrease certain of its historic vary, I view this to be a superb shopping for alternative supported by insider shopping for, respectable development potential, total sector rotation, and long-term dividend will increase. So in my opinion, ATCO appears like among the best names within the Canadian energy and utilities house.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please concentrate on the dangers related to these shares.