3D Graphic Design/iStock through Getty Photographs

Introduction

I am positive I communicate for everybody after I say all of us love sale. Particularly when a few of your favourite shares are promoting at a reduction. With rates of interest remaining excessive for the foreseeable future, it isn’t simple discovering high quality enterprise growth corporations buying and selling at enticing valuations. As an avid BDC investor I’ve not added to any of my holdings since rates of interest have grow to be elevated over the previous 24 months or so.

However although some are buying and selling at giant premiums to their NAV costs at the moment, there’s one specifically that also trades at a reduction on the time of writing. On this article I focus on what makes Bain Capital Specialty Finance (NYSE:BCSF) enticing and why earnings traders might take into account including this to their portfolio.

Why The Low cost?

With many high quality BDCs buying and selling considerably above their NAVs at the moment, one has to marvel why Bain Capital Specialty Finance is the exception. One purpose would be the inventory’s observe report. The BDC, in comparison with friends like Capital Southwest (CSWC) and Ares Capital (ARCC), hasn’t been round as lengthy.

The BDC IPO’d on the finish of 2018, so that they have solely been public just a little over 5 years. I am not saying that is the rationale for the low cost, nevertheless it very nicely may have one thing to do with it. Most traders choose an extended observe report when seeking to put money into an organization.

How did they do over the past financial downturn? How lengthy have they paid a dividend? Did they reduce the dividend over the past recession?

These are all legitimate factors when trying into an organization, particularly one which pays out a big chunk of their earnings within the type of dividends like BDCs or REITs sometimes do.

However then once more there are some corporations with shorter observe data that commerce at premiums as nicely. Take one other favourite within the sector and holding of mine, Blackstone Secured Lending (BXSL). Their exterior supervisor Blackstone (BX), who is without doubt one of the most well-known corporations on the earth, may additionally have one thing to do with that although in my view. Both means BCSF appears to be doing all the suitable issues and will very nicely grow to be the subsequent famous person throughout the sector.

Improved Dividend Protection

In all probability essentially the most enticing factor about Bain Specialty is their dividend protection. Another excuse for the low cost might be the dividend reduce the corporate did again in 2020 once they slashed the dividend roughly 17% from $0.41 to $0.34. However as most might know, the pandemic was a tricky time for a lot of companies and compelled a number of corporations to default on loans.

However since then, the corporate has shortly gotten again to development, elevating the dividend from $0.34 to the present $0.42 a share. They usually’ve been out-earning their dividend by a large margin. The BDC reported Q3 earnings again in November, bringing in internet funding earnings of $0.55, beating estimates by $0.01. This was down from $0.60 in Q2 however seeing by the present dividend, they comfortably out-earned their dividend with protection nicely above 100%.

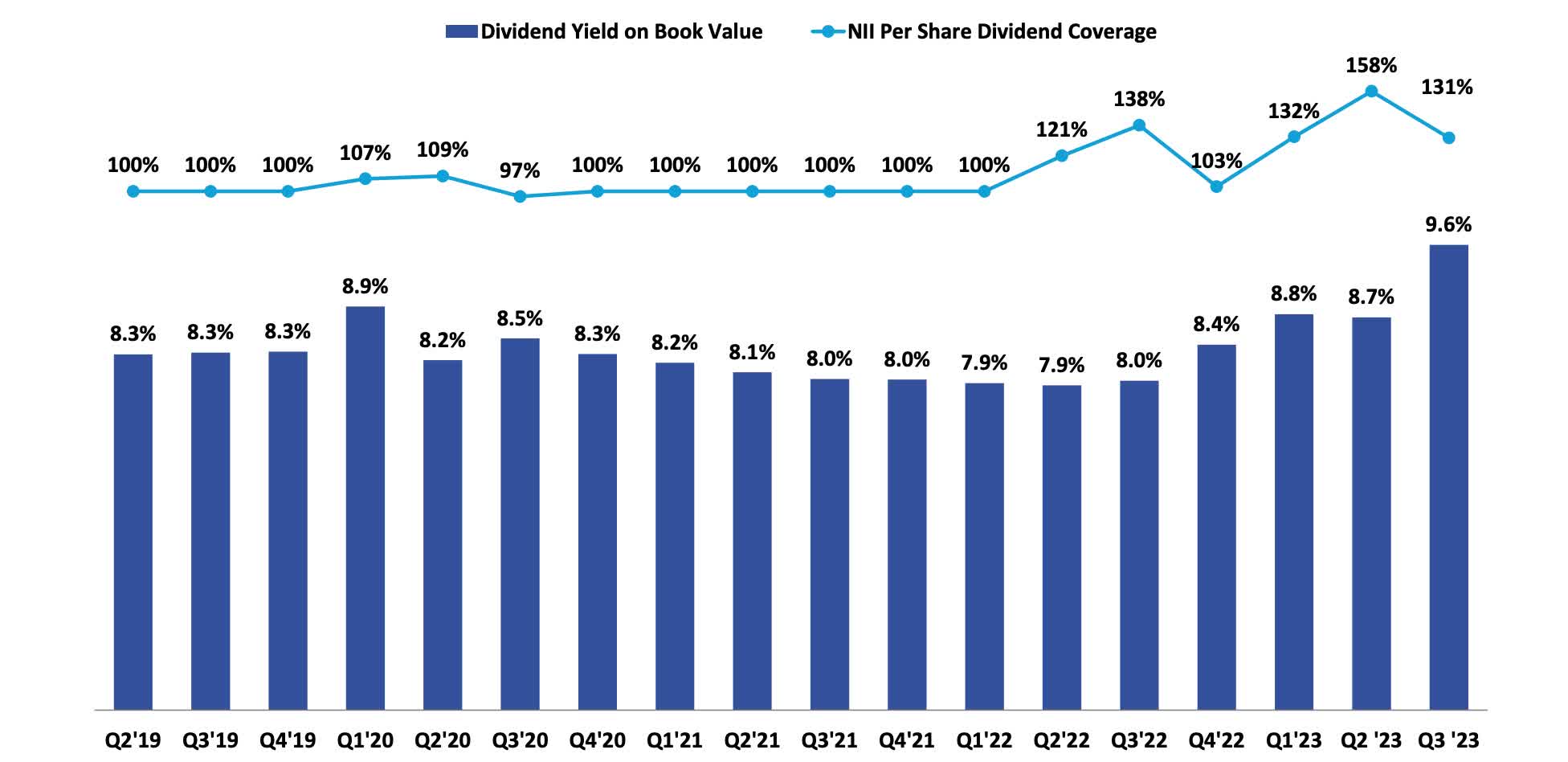

Within the chart under, you’ll be able to see for the reason that begin of fee hikes BCSF has comfortably lined their dividend. The BDC has not rewarded traders with a particular or supplemental like a few of its different friends, however the protection has remained sturdy with room to award shareholders sooner or later in the event that they see match.

BCSF investor presentation

However I believe it is good to not as they’ve been centered on rising their portfolio not too long ago. On the finish of Q3, they’d a complete of 143 portfolio corporations valued at $2.4 billion throughout 30 industries. This grew from 130 corporations and a complete portfolio truthful worth of $2.29 billion year-over-year.

Aerospace & Protection is their largest sector and through their newest quarter they continued with new investments in corporations who present mission-critical software program & surveillance options to the protection business and medical corporations that gives on-site providers to sufferers at expert nursing amenities. Over the 12 months they’ve invested a complete of $616 million with 84% in first-lien loans.

Their first-lien share at the moment stands at 64%, down from 66% in Q1. Administration attributed the drop in first-lien loans to development in new investments. Though they don’t seem to be as defensively positioned as Capital Southwest whose first-lien loans at the moment stand at 84%, they’re considerably larger than their largest peer Ares Capital’s 43.1%.

However seeing by the smaller market cap of the corporate, I count on this to rise over time as they proceed to make new investments to develop their portfolio.

Robust Stability Sheet

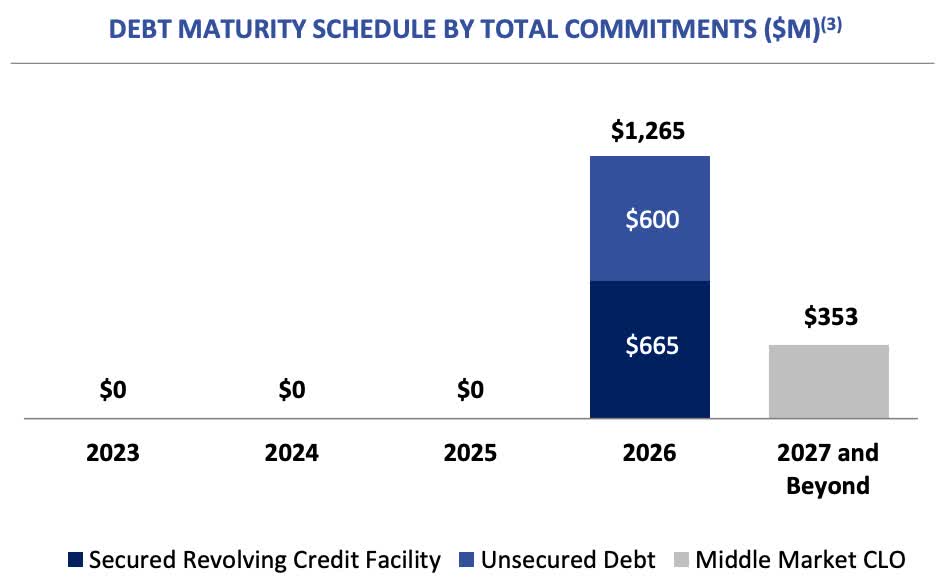

Though not as defensively positioned as some friends, the BDC does have a robust stability sheet with no debt maturities to fret about till 2026. So, if the economic system does expertise a recession or charges stay larger, the corporate is in a robust monetary place to navigate. Moreover, they’ve elevated their money stability from $29.6 million in Q1 to $79.5 million in Q3.

BCSF investor presentation

In addition they boast investment-grade credit score scores from all three main score businesses. Moreover, they’ve managed to lower their debt-to-equity ratio to 1.12x, down from 1.13x in Q2. That is compared to peer, ARCC’s 1.03x. One factor I like about BCSF is they seem extra fiscally conservative like ARCC, a desire of mine.

Rewarding shareholders within the type of specials & supplementals is nice and all, however paying out all of your earnings within the type of dividends and never retaining any money might be detrimental if the economic system experiences an surprising downturn. Or if one in all their portfolio corporations experiences monetary hardship. The corporate’s spillover earnings elevated from $0.44 to $0.79, or 1.9x in Q3. And I count on the corporate to proceed carrying over spillover earnings, just like peer ARCC.

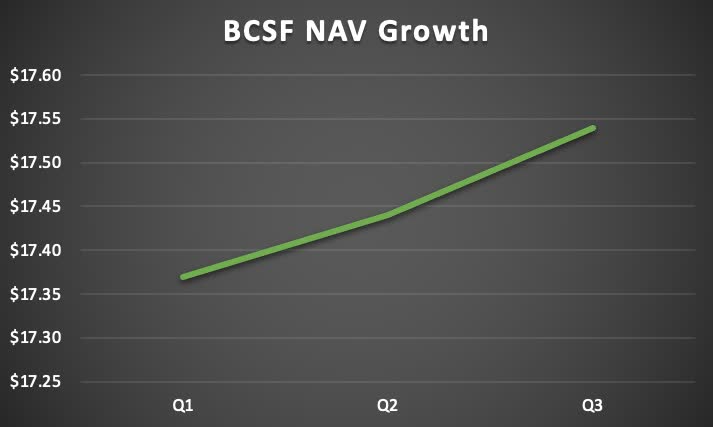

NAV Progress

With the corporate comfortably out-earning its dividend, the NAV worth has elevated steadily quarter-over-quarter from $17.37 in Q1 to $17.54 within the newest quarter. This was additionally up from $17.29 on the finish of 2022. A part of this may be attributed to their elevated dividend development and dividend protection well-above 100% over the previous 12 months. At a worth of lower than $15 on the time of writing, the inventory is enticing, providing a double-digit low cost of 17%.

Writer creation

Dangers To Thesis

Some traders could also be skeptical about investing in BCSF due to the dividend reduce in 2020 and/or their comparatively brief observe report. However the firm has been conservative for the reason that begin of fee hikes, strengthening their monetary place previously 12 months. With the FED electing to carry charges not too long ago making fee cuts seemingly out for subsequent month, the BDC will take pleasure in additional earnings for some time longer, primarily as a consequence of its predominantly floating fee debt portfolio.

At 94% and never being as defensively positioned in first-lien loans like some friends, this might trigger tighter dividend protection when charges are reduce. Which many predict someday this 12 months. And though they lined the dividend previous to the beginning of fee hikes, this protection was lower than a few of their bigger, and extra common friends within the sector. Moreover, if dividend protection turns into considerably tighter, their share worth can even seemingly endure within the course of. So, traders at the moment holding or seeking to doubtlessly purchase BCSF, that is one thing to regulate going ahead.

Backside Line

Bain Capital Specialty Finance is a reasonably newcomer to the BDC house and regardless of their monetary troubles throughout the pandemic that noticed them reduce the dividend, they’ve been rising their portfolio impressively since then. They’ve additionally elected to be extra fiscally conservative than some friends, permitting them to retain additional earnings within the type of spillover (earnings).

This, together with the sturdy stability sheet places the BDC in a robust monetary place if portfolio corporations grow to be too pressured from larger for longer charges. On the finish of the quarter, they solely had 3 corporations on non-accrual standing, however this might rise within the close to future. However seeing by their well-laddered debt maturities, sturdy money place, and well-covered dividend, I fee the BDC a speculative purchase.