Iuliia Efimova/iStock via Getty Images

Seeking Alpha

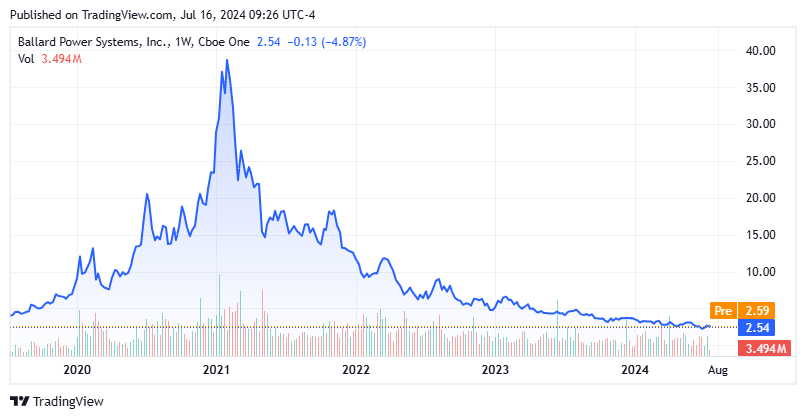

Today, we are going to take a deeper look at the fuel cell concern of Ballard Power Systems Inc. (NASDAQ:BLDP). As can be seen from the chart above, the stock has cratered by more than 90% since its highs early in 2021. However, losses are projected to be reduced in coming years, while revenues are expected to see accelerated growth. The company also is seeing solid growth in order backlog and has a huge new manufacturing facility, funded to a large extent by government grants, come online in 2027. An analysis follows below.

July 2023 Company Presentation

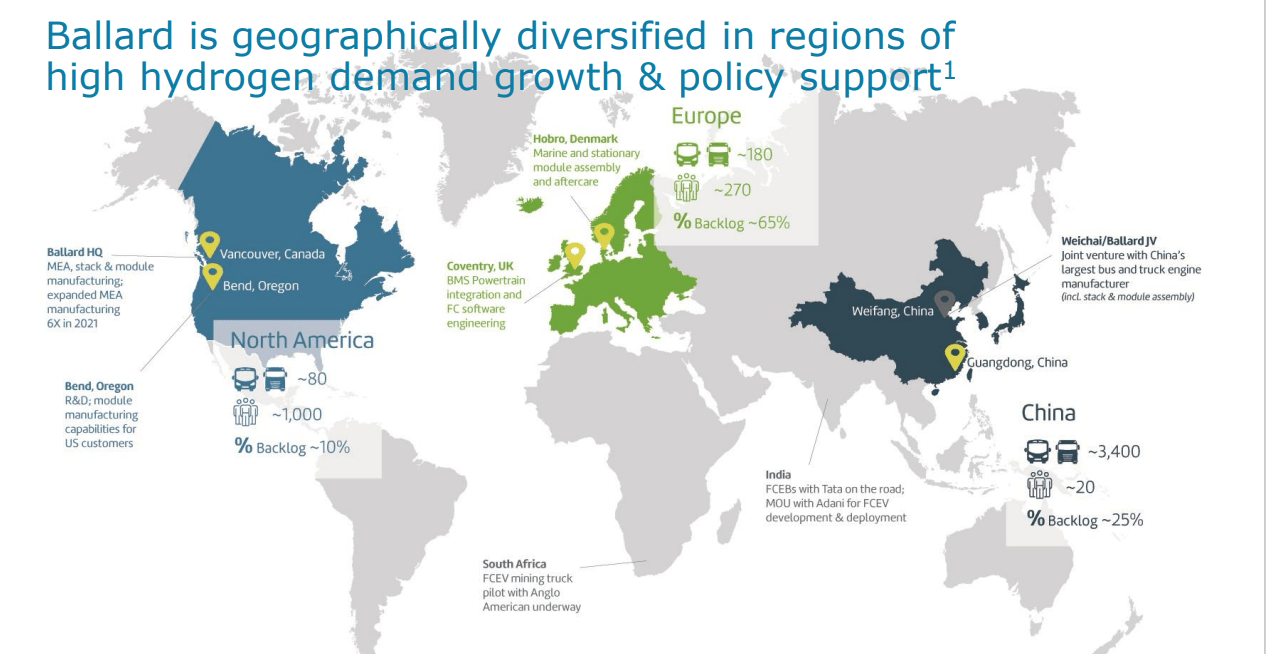

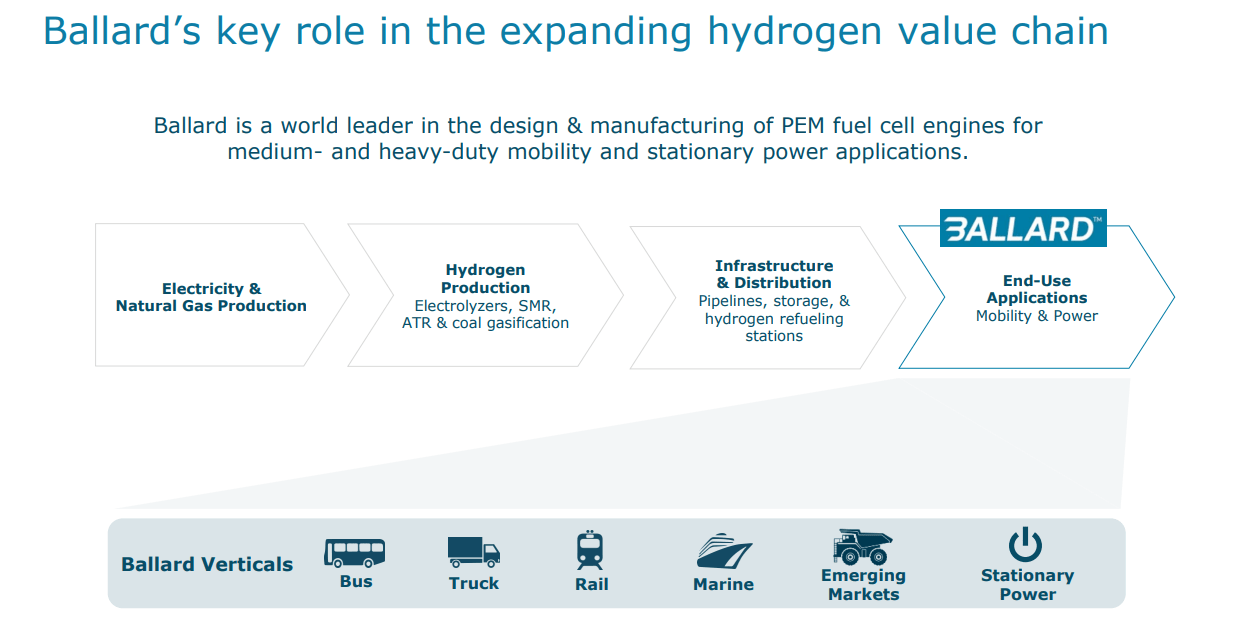

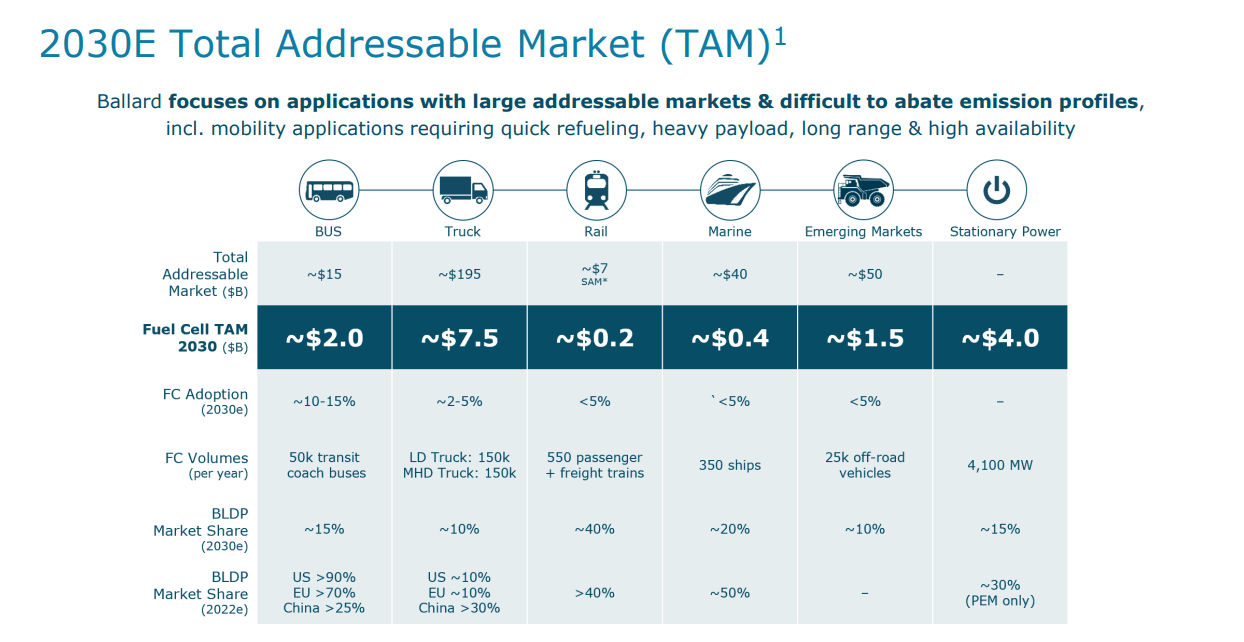

The company is headquartered in British Columbia, Canada, and is focused on the development and manufacture of proton exchange membrane (PEM) fuel cell products. These PEM fuel cells enable electrification of various vehicles including buses, commercial trucks, trains, and marine vessels as well as being able to provide stationary power. The stock currently trades near $2.50 a share and sports an approximate market capitalization of just north of $750 million.

July 2023 Company Presentation

Recent Results:

Ballard Power Systems posted its Q1 numbers on May 7th. The company delivered a GAAP loss of 14 cents a share, in line with expectations. Revenues rose nine percent on a year-over-year basis to $14.5 million, which missed the consensus by more than $3 million.

The one impressive part of the quarter was that the company added $64.5 million to its order backlog, on top of the $64.7 million in orders it received in the previous quarter. Key orders in the quarter came from fuel cell bus manufacturers and for renewable off-grid power generation. The company also announced it was going to build a new manufacturing facility just outside of Dallas with the capacity to build 20,000 fuel cell engines annually. This facility, dubbed Ballard Rockwall Giga 1, will sit on 22 acres and is supported partly by government grants (see section below) and is currently scheduled to come online in 2027.

Analyst Commentary & Balance Sheet:

The analyst community has little love for Ballard Power Systems at the moment. Since first quarter results hit the wires, nine analyst firms, including Piper Sandler, Wells Fargo and Jefferies, have reiterated Hold or Sell ratings on the stock. Lake Street seems to be the one big bull on the stock, maintaining a Buy rating and whopping $15 price target on the stock on May 7th. HSBC ($3.80 price target, down from $4.10 previously) also stuck with their Buy rating.

The company ended the first quarter with approximately $720 million of cash and marketable securities on its balance sheet after posting a net loss of $41.1 million for the quarter. Ballard burned through just over $30 million worth of cash in the first three months of the year. This is a similar cash burn rate to the same period a year ago. The company is benefiting from taxpayer largesse, it should be noted. During the quarter, Ballard garnered a $40 million award from the U.S. Department of Energy Hydrogen and Fuel Cell Technologies Office. The company also received an award valued up to $54 million that was funded by the Inflation Reduction Act (IRA) that was legislated in the summer of 2022.

Conclusion:

Ballard Power Systems lost 59 cents a share on just over $102 million in FY2023. The current analyst firm consensus is for losses to fall slightly to 52 cents a share in FY2024 on $112 million. They project a sales surge of 45% in FY2025, with losses of 47 cents a share.

July 2023 Company Presentation

The stock is trading for not much more than the cash on its balance sheet, and sales growth should pick up substantially in FY2025. Ballard Power Systems is also targeting some big end-user markets and is garnering considerable support from government programs. On the flip side, the stock is not well thought of in the analyst community and the company is still burning cash.

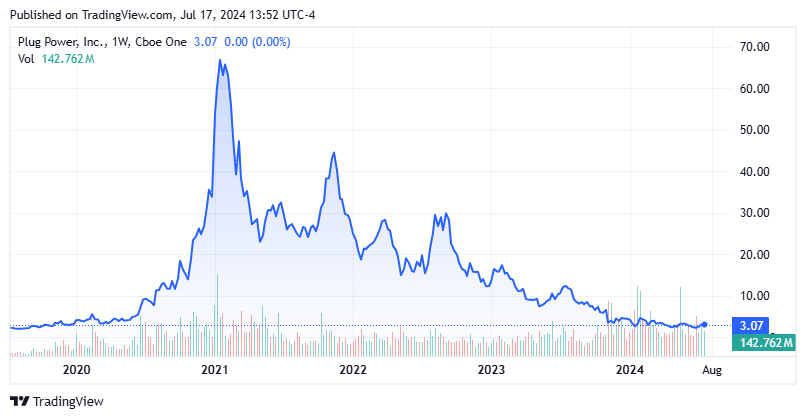

Apparently, even bullish investment sentiment can’t seem much of the alt-energy space. This part of the economy had a huge surge in 2020 through a good part of 2021 as easy money led to a massive IPO/SPAC wave in 2020/2021. Unfortunately, most of the alt-energy space failed to live up to its hype and, like most bubbles, suffered a huge implosion. And again, I am not picking on Ballard. Fuel cell competitor Plug Power (PLUG) is in the same boat, as can be seen in the chart below. The pattern is almost exactly identical to Ballard over the past few years, as the initial promise of fuel cells just haven’t lived up to their initial promises and hopes. Plug Power is on a similar earnings and revenue growth trajectory to Ballard, it should be noted. Plug’s losses are also projected to come down over the next few years as sales growth accelerates.

Seeking Alpha

The fact that the shares of neither Ballard Power Systems nor Plug Power can get much of even a ‘dead cat bounce‘ in one of the greatest and fastest sector rotations in my lifetime, also tells me both stocks are broken. Given how much shareholder value these equities have destroyed since the beginning of 2021, this is probably understandable. Therefore, until either management makes meaningfully progress to profitability, I am going to stay on the sidelines around both fuel cell names.