Joa_Souza/iStock Unreleased by way of Getty Photographs

In earlier articles outlining my funding thesis on Banco Santander (Brasil) (NYSE:BSBR), I’ve primarily targeted on the efficiency of the Brazilian financial institution’s shares, which have been affected by issues over mortgage defaults and credit score availability. These issues have considerably impacted the broader Brazilian banking sector, negatively affecting the effectivity and profitability of Santander Brasil in current quarters, the place the financial institution has maintained a notably low Return on Fairness (“ROE”) in comparison with its vital home friends.

Through the previous quarter, Q3, Banco Santander Brasil displayed promising enchancment in vital areas, resembling asset high quality, credit score origination, and a gradual profitability enhancement. This optimistic trajectory was mirrored within the efficiency of Santander Brasil shares, which witnessed a notable enhance of about 17% from Q3 to This autumn.

Nonetheless, complicating the evaluation of probably the most current This autumn outcomes, whereas the outcomes weren’t fully passable, there are nonetheless optimistic elements that may very well be pivotal for 2024.

The online earnings of R$2.2 billion underwent a notable 19% decline in comparison with the earlier quarter. ROE measured the profitability at simply 10.3%, sustaining low ranges in comparison with the financial institution’s historic efficiency and a few rivals. Notably, this determine can also be under the 12.4% reported by Santander Group (SAN), its controlling entity, in the identical quarter.

Consequently, the financial institution’s profitability, which had been on an upward pattern, regrettably worsened this quarter. Regardless of these challenges, as I observe Santander Brasil buying and selling at a premium a number of in comparison with its major friends and exhibiting rather more inconsistency in its fundamentals, I discover little purpose to undertake a extra bullish stance on the financial institution right now.

Santander Brasil’s This autumn Overview

Within the fourth quarter of 2023, Santander Brasil reported a recurring internet earnings of R$2.204 billion, falling under the market consensus, which had anticipated a revenue of R$2.87 billion. Regardless of a year-over-year revenue enhance of 30.5%, there was a notable lower of 19.2% in comparison with the second quarter of the identical yr.

Santander’s return on fairness (“ROE”) remained at 10.3%, indicating a persistent low degree in comparison with different trade friends resembling Itaú Unibanco (ITUB) and Banco do Brasil (OTCPK:BDORY), each boasting ROEs exceeding 20%.

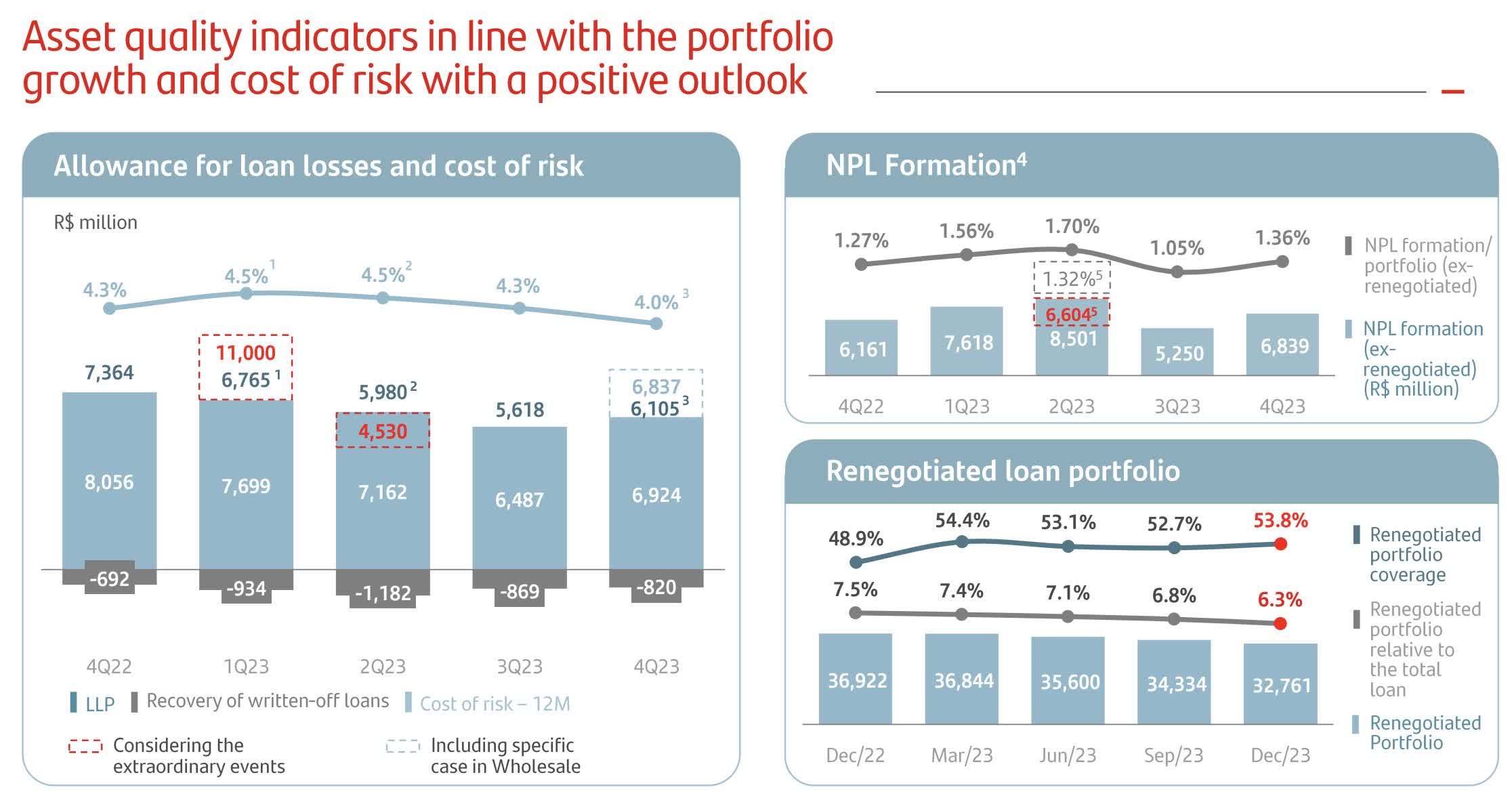

Key highlights from the quarter embody an enchancment in curiosity earnings (“NII”) and modest development within the credit score portfolio. Whereas non-performing loans remained secure and decreased within the brief time period, provisions for dangerous money owed raised issues, albeit influenced by sure one-off elements.

As of the top of September, Santander Brasil reported complete belongings of R$1.153 trillion, with shareholders’ fairness at R$86 billion. The next are key factors from Santander Brasil’s fourth-quarter outcomes segmented for readability:

-

Curiosity Revenue (“NII”) Enchancment: Notable optimistic efficiency in curiosity earnings.

-

Credit score Portfolio Development: Modest enlargement noticed within the credit score portfolio.

-

Non-Performing Loans: Stability and a short-term lower in non-performing loans.

-

Provisions for Unhealthy Money owed: Alarming provisions reported, influenced by sure one-off elements.

Modest Development in Credit score Portfolio

Banco Santander Brasil has reported a mortgage portfolio of R$516.6 billion, indicating a cautious quarterly development of two.8% and a yearly development of 5.5%. This development displays a barely extra favorable macroeconomic surroundings with decrease rates of interest. Moreover, it’s a consequence of a tentative enchancment in credit score high quality, permitting the financial institution to enterprise into higher-risk strains. If we exclude the trade charge impact, the quarterly development would have been 3.1%, with a extra substantial enhance of 6.2% year-over-year.

Banco Santander Brasil’s IR

The standout performer on this quarter was the person phase, experiencing development of three.1% throughout the quarter and 6% year-over-year. Client financing additionally contributed positively, exhibiting a rise of 5.5% within the quarter and a couple of.6% year-over-year. Small and medium-sized firms exhibited development of 5.2% throughout the quarter and a noteworthy 8.9% year-over-year. On the flip aspect, the massive firms line (Company R$139 billion) noticed a slight 0.1% decline year-over-year and a modest enlargement of 4.5% year-over-year.

A noteworthy improvement is that the brand new crops originated in January 2022, characterised by a extra applicable danger degree, now represent 67% of the full portfolio.

Curiosity Revenue (“NII”): Margin Enchancment

The financial institution’s curiosity earnings witnessed a quarterly enhance of 4.8% in comparison with Q3 and an annual rise of 12.3% in comparison with This autumn of the earlier yr. NII Shoppers (margin with shoppers) barely elevated by 1.1% quarter on quarter. The Margin with the market (NII Mercado) confirmed a damaging stability of R$263 million, a considerable enchancment from the damaging stability of R$827 million recorded in the identical interval final yr, indicating a gradual enchancment course of.

Banco Santander Brasil’s IR

The notable development in NII, considerably when outpacing the mortgage portfolio, signifies an enchancment within the internet curiosity margin. The online curiosity margin represents the distinction between the rate of interest obtained on interest-earning belongings (loans) and the rate of interest paid on interest-bearing liabilities (resembling deposits). A sooner development charge in NII in comparison with the mortgage portfolio suggests environment friendly administration of funding prices, funding in higher-yielding belongings, or favorable market situations.

Delinquency: Stability Rising After the Worst

Delinquencies over 90 days (administration view) exhibited a modest enhance of 0.1pp year-over-year and remained secure at 3.1%. This improvement is seen optimistically because it reinforces a extra favorable situation for the banking sector in Brazil, signaling that “the worst is over,” particularly contemplating the height at 3.3% recorded in June of the earlier yr. The fourth quarter was characterised by stability within the particular person phase however noticed a marginal enhance of 0.1pp quarter-over-quarter in giant firms and small and medium-sized enterprises.

Banco Santander Brasil’s IR

A optimistic facet in This autumn was the advance in short-term delinquency (15-90 days), exhibiting a quarterly decline of 0.2pp. This enchancment was attributed to the higher efficiency of recent vintages, with people experiencing a major contraction of 0.4pp throughout the quarter.

Asset High quality and Credit score Provision Bills

Upon preliminary examination, Santander Brasil’s asset high quality outcomes for This autumn could seem dire. Allowance for mortgage losses (“ALL”) reached R$6.8 billion, marking a quarter-over-quarter enhance of 21.7%, regardless of a year-over-year lower of seven.2%.

Banco Santander Brasil’s IR

The quarter confronted damaging impacts from three particular circumstances: (1) a provision of 20% for the Lojas Americanas case (a Brazilian retailer concerned in an accounting scandal), with 70% already provisioned; (2) the discharge of R$400 million to a Brazilian wholesaler in default; (3) a judicial restoration case within the drinks sector, leading to R$90 million for the financial institution.

Nonetheless, amidst the challenges, there have been optimistic elements. Notably, the availability was diminished with a reversal of R$392 million from the retail phase in Brazil. Moreover, a sale of $1.2 billion from a portfolio that had already been written off yielded a acquire of R$49 million. Consequently, the protection ratio ended at 222%, indicating a wholesome security margin regarding monetary expenses. Nonetheless, it declined by seven share factors within the quarter and eight share factors within the yr because of the talked about cost enhance.

Banco Santander Brasil’s IR

On the damaging aspect, Santander Brasil reported a rise in complete administrative bills, reaching R$7.9 billion, up 8.4% within the quarter and seven.6% within the yr. The quarter was significantly impacted by the September layoff final yr, leading to increased bills for technical providers, upkeep, and promoting.

Now, wanting on the intense aspect, Santander Brasil has been proactive in expense discount initiatives. They’ve been closing branches whereas sustaining secure workers, internalizing outsourced employees, and investing in monetary advisory providers. Moreover, the acquisition of brokerage corporations, resembling Toro, has been a part of the financial institution’s strategic efforts to reinforce its total effectivity and repair choices.

Valuation and Dividends

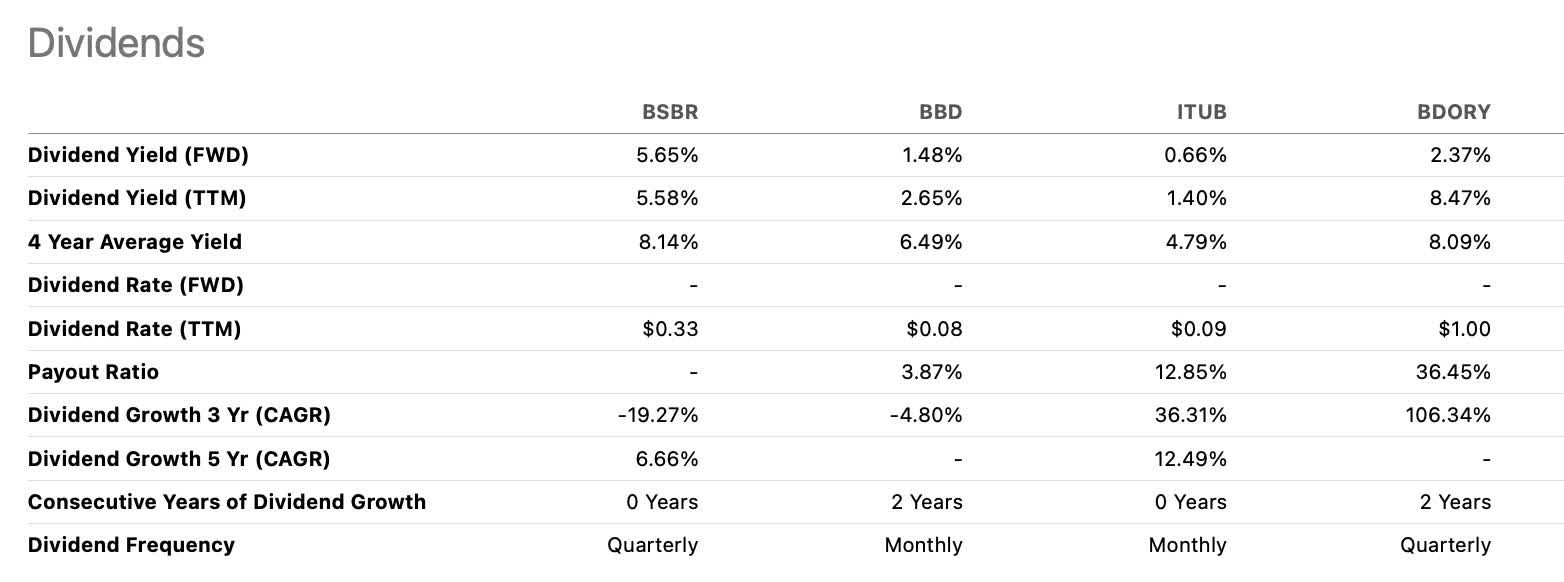

Banco Santander Brasil, underneath the management of Spain’s Santander Group, has persistently prioritized returning a good portion of its earnings by dividends, making its shares an interesting earnings inventory for a lot of traders over time.

Inspecting the dividend cost historical past amongst main Brazilian banks, Santander Brasil stands out favorably. It boasts a ahead dividend yield of 5.5%, second solely to Banco do Brasil, a state-owned financial institution. Moreover, Santander Brasil has maintained a mean yield of 8.1% over the past 4 years, surpassing all its trade friends.

Looking for Alpha

Nonetheless, a major a part of this attraction for dividends is clear within the premium valuation the financial institution persistently maintains in comparison with its friends. Banco Santander Brasil trades at a ahead P/E ratio of 10.9x, surpassing all different friends. Though its price-to-book ratio is 1.04, it’s second solely to Bradesco (BBD).

Looking for Alpha

In my perspective, Banco Santander’s present valuation appears difficult to justify solely based mostly on the attractiveness of its friends. Notably, Banco do Brasil, regardless of being state-owned, stories a Return on Fairness (“ROE”) virtually double that of Banco Santander Brasil. Moreover, Itau Unibanco, presently the financial institution with probably the most sturdy credit score and profitability indicators within the sector, trades at a extra discounted valuation in sure elements in comparison with Banco Santander Brasil. It is value noting that Banco Santander Brasil nonetheless reveals some weaknesses.

The desk under shows the symptoms of the principle Brazilian banks as much as Q3, apart from Santander Brasil, which contains This autumn outcomes.

|

Mortgage Portfolio (R$ bi) |

Delinquency Charge |

Expanded ALL (R$ bi) |

Protection Ratio |

ROE |

CET1 |

Basel |

|

|

Santander Brasil |

516.6 |

3% |

-6.8 |

222% |

10.3% |

11.5% |

14.5% |

|

Banco do Brasil |

1070 |

2.8% |

-7.5 |

199% |

21.3% |

12.4% |

16.2% |

|

Itaú Unibanco |

1163 |

3% |

-9.3 |

209% |

21.1% |

14.6% |

16.3% |

|

Bradesco |

877.5 |

5.6% |

-9.1 |

182.5% |

11.4% |

13.4% |

12.9% |

The Backside Line

Regardless of Santander Brasil’s fourth-quarter outcomes falling in need of expectations, marked by a major decline in internet revenue in comparison with the earlier quarter, persistently low ROE, and a halt within the upward trajectory of profitability, coupled with a PDD outcome strongly impacted by poisonous credit from Lojas Americanas (now 70% provisioned), there are nonetheless optimistic elements to think about for 2024.

The financial institution made strides in fortifying its stability sheet throughout this quarter by credit score provisions, doubtlessly assuaging the necessity for future provisions. Moreover, income strains are anticipated to rebound, pushed by development in segments with increased spreads and elevated service revenues. Whereas the This autumn outcome is probably not overwhelmingly optimistic, it may not be as bleak because it seems, particularly given the soundness and short-term lower in defaults.

I’ve maintained a impartial stance on Banco Santander Brasil for a substantial interval and discover it difficult to shift in the direction of a bullish outlook in mild of outcomes that proceed to lag behind the financial institution’s potential. The present valuation doesn’t essentially present a compelling benefit over friends buying and selling at extra discounted multiples and exhibiting extra sturdy outcomes.

Given these elements, I’m once more on the fence, awaiting extra wonderful stabilization, significantly in provisions, all year long. An enchancment in ROE would instill extra confidence in Banco Santander Brasil’s funding thesis earlier than contemplating a extra optimistic outlook.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a significant U.S. trade. Please pay attention to the dangers related to these shares.