DKosig

Welcome to another installment of our BDC Market Weekly Review, where we discuss market activity in the Business Development Company (“BDC”) sector from both the bottom-up – highlighting individual news and events – as well as the top-down – providing an overview of the broader market.

We also try to add some historical context as well as relevant themes that look to be driving the market or that investors ought to be mindful of. This update covers the period through the fourth week of May.

Market Action

BDCs were roughly flat in a mostly down week for income markets. MSDL underperformed – the stock has been very volatile, likely due to the relatively low number of shares trading publicly. More shares will be released after lock-up expiries.

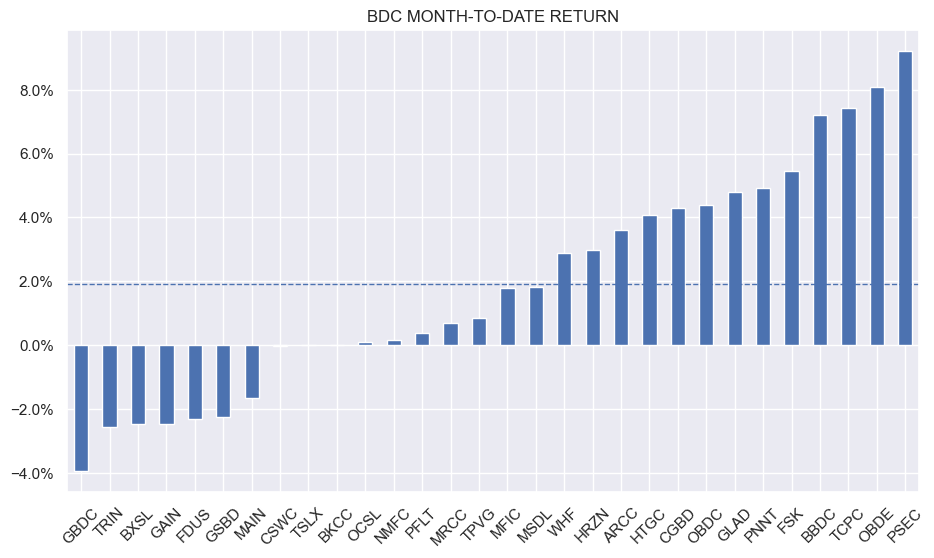

Month-to-date, the average stock in our coverage is up around 2%.

Systematic Income

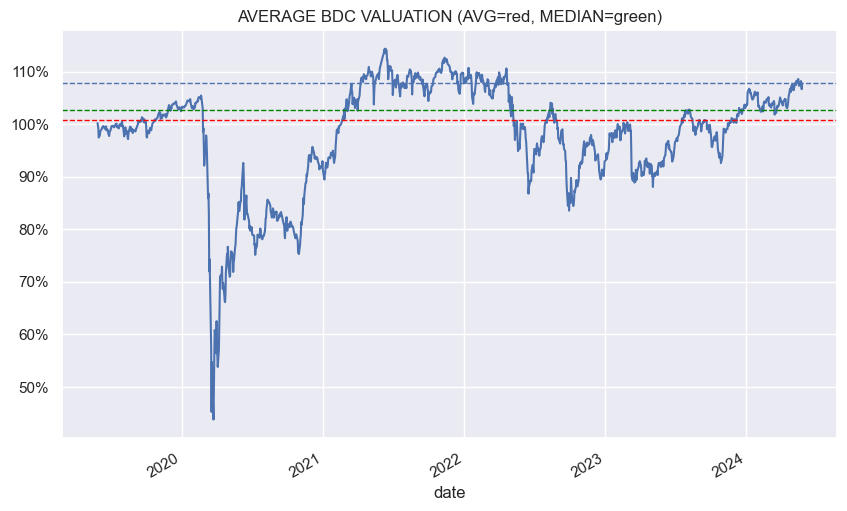

BDC valuations remain elevated. Although BDC valuations are not directly tied to net income, they are unlikely to rise further from current elevated levels in the face of falling net income levels that we have already seen in Q1.

Systematic Income

Market Themes

A subscriber passed on some worried BDC-related commentary. The view seems to be that because there are “trillions” pouring into private credit markets it could lower lending standards while higher base rates are squeezing borrowers which could lead to increased non-accruals and defaults in portfolios.

As far as the former worry, mathematically you can’t have trillions of dollars pouring into the private debt market if that market is only $1.7trn and it has taken 7 years to grow by $1trn. Moreover, if we look at the capital at the disposal of BDCs, it’s not growing all that much – it’s only growing organically through at-the-market issuance, an occasional public offering and retained income – single-digit growth rate at best for most BDCs.

As far as deterioration in fundamentals, you could have said the same thing in 2022 when base rates started rising and the macro picture looked bleak. And if you invested based on this view by avoiding BDCs you would have missed out on a tremendous run, for an average return of 32%.

Are non-accruals rising and are there defaults? Sure, in places, but, as always, we need to put things in context, which is that BDCs are still generating double-digit returns (i.e. total NAV returns) in spite of rising non-accruals and defaults. This is because of several levels of protection such as collateral, sponsor equity, work-out teams, restructuring help etc. And in fact, if anything, BDC managers are complaining that fundamentals are too good – lending spreads are very tight and loans are being repaid more quickly than expected, generating fewer opportunities which is why leverage has been falling across the sector.

Are there reasons to worry? Yes, but we would worry more about the fact that credit spreads are tight and BDC valuations are high than about nebulous things like “underwriting standards” or concerns about the future (who doesn’t have concerns about the future?). BDC managers aren’t dummies. They don’t want to have losses so they are not going to lend just because they have some capital.

Any sort of analysis that directly connects rates to defaults to BDC portfolio performance can sound smart but, in reality, it has little to no information value. Things can always go wrong. It’s more interesting to discuss why they haven’t gone wrong in the last 2.5 years as rates have risen than to ignore reality and keep saying that higher rates will just lead to poor BDC portfolio performance.

Analysis needs to be quantified (where are non-accruals rising, are they large enough to matter, are sponsors stepping up to support their companies, which BDCs have been most resilient, is higher BDC income sufficiently offsetting the added risk of defaults) and then marked-to-market (if rate rises lead to non-accruals and defaults why haven’t we seen a whole lot of it in the last 2.5 years).

The strategy of avoiding BDCs when rates are high suggests we should go all in when rates are low. This strategy would have loaded the boat at the end of 2021, precisely when BDC valuations were very high – even higher than today. That was not a good time to turn bullish as it was quickly followed by a steep drawdown – creating a much better time to add exposure, particularly as BDC net income levels were due to surge, as we highlighted at the time.

We are often asked what will happen to some asset class when rates rise or fall. Our answer is always – it depends why rates are rising or falling. If rates are falling because we entered a massive recession then, more likely than not, it will be very bad for most credit assets. If rates are falling because the economy is going through a disinflationary boom like we have had for the past year, then, more likely than not, it will be good for most credit assets.

Our view at this stage of the cycle is to hold some BDC exposure, with a particular focus on names that have been resilient through-the-cycle and those with modest leverage and a high allocation to first-lien loans. We have reduced our overall sector exposure in the last few months, but not because of a “higher rates = bad” rule of thumb but because valuations are not far off their historic highs. This value investing strategy is what has worked well in the past.

Market Commentary

Saratoga Investment (SAR) raised its dividend by a penny. The stock features very high dividend coverage so it has been happy adjusting its dividend higher every quarter. SAR features what looks to be the highest level of leverage in the entire BDC sector – at around 2x versus an average closer to 1x. It would be one thing if that leverage was cheap but about half its bonds cost more than 8% which, after fees, leaves little in terms of net investment income. The NAV has been wobbly as well with non-accruals at cost around 6%.

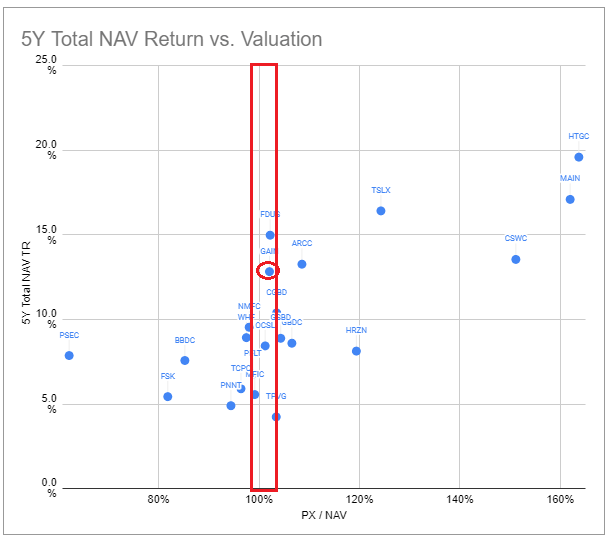

Gladstone Investment (GAIN) has stumbled recently, falling to a 2% premium to NAV this week – 6% below the average and 1% below the median. Out of all BDCs in coverage trading at a near-100% valuation only FDUS has a stronger 5Y total NAV return. GAIN is somewhat unusual given its low first-lien allocation and fairly undiversified portfolio, however, the historic performance speaks for itself.

Systematic Income BDC Tool

Stance And Takeaways

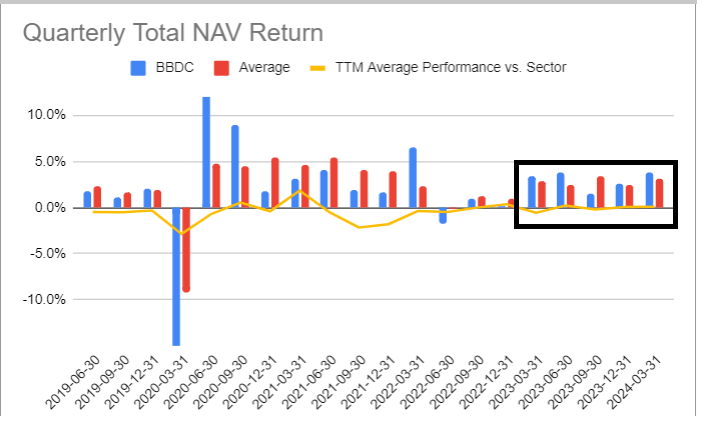

This week we added a position in the Barings BDC (BBDC). The stock has been performing in line with the sector over the past 18 months or so but continues to trade at a steep discount – at a valuation of around 20% below the sector average.

Systematic Income BDC Tool