We Are

We beforehand lined BHP Group Limited (NYSE:NYSE:BHP) in September 2023, discussing the unsure restoration within the iron spot costs as China’s portside stock declined and imports accelerated over the previous few months.

Nonetheless, with the demand for iron ore anticipated to average over the following few many years, it was unsurprising that the producer had pledged intensified capex in the direction of electrification metals, naturally impacting its variable dividend payouts.

On account of the uncertainty, we had most popular to price the inventory as a Maintain then, because it remained to be seen when the macroeconomic outlook would possibly enhance.

On this article, we will talk about why we’re rerating the BHP inventory as a Purchase regardless of the immense rally after the Q2/Q3’23 sideways motion, because of the surge noticed within the commodities’ spot costs.

With the inflation already cooling and the Fed open to a pivot by Q1’24, we might even see this optimism persist for a bit longer, with the property and EV demand prone to return ahead of anticipated, boosting the demand/ spot costs for iron ore and copper.

The Dynamic Commodity Funding Thesis Stays Strong

Iron Ore/ Copper Spot Costs

Market Insider

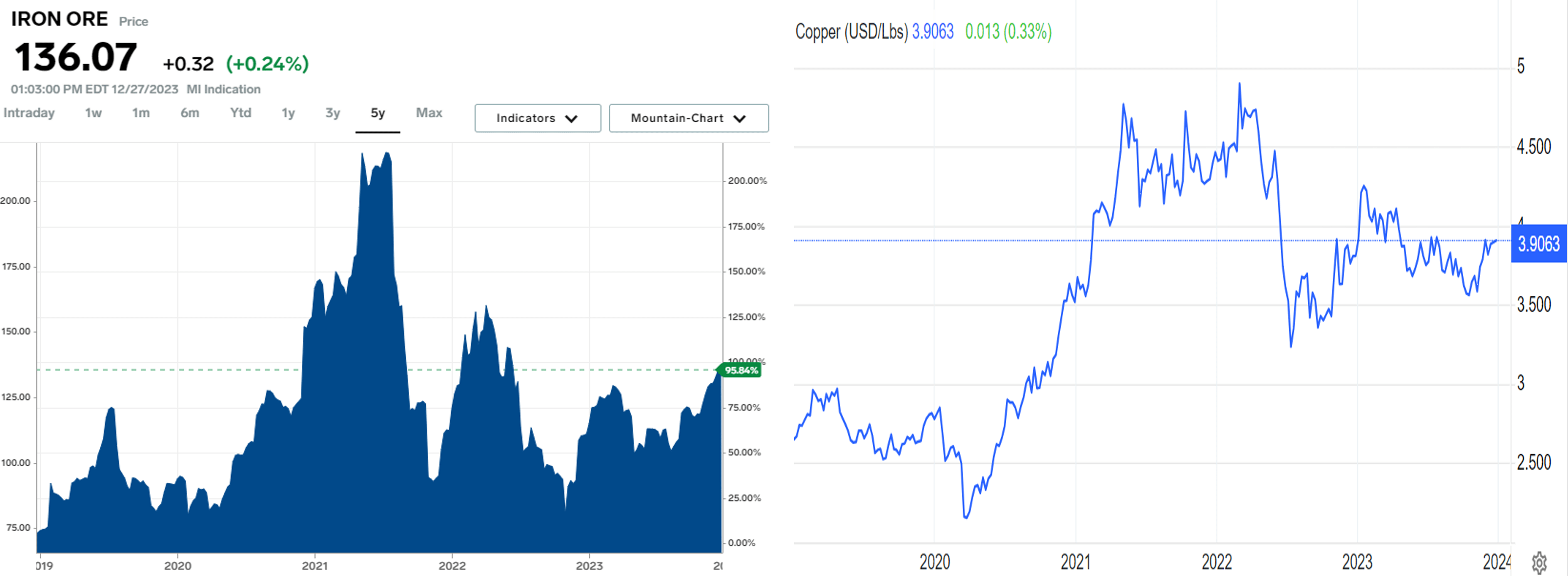

The iron ore spot price has continued to climb for the reason that earlier backside to file a brand new 2023 peak of $136.07/wmt on the time of writing.

Readers could wish to observe that that is properly above the 2019 averages of $90/wmt, BHP’s FQ1’24 common realized costs of $98.04/wmt (-1.8% YoY), and FY2023 average realized prices of $92.54/wmt (-18.1% YoY).

Iron ore can also be the producer’s backside line driver with $16.7B of adj EBITDA generated in FY2023 (-23% YoY), or the equal 59.8% (+6.4 factors YoY) of the general profitability.

Consequently, it’s unsurprising that Mr. Market has cheered on the current restoration in spot costs, because of the accretive affect on BHP’s near-term high/ backside traces.

The identical restoration has additionally been noticed within the copper spot costs, with the commodity buying and selling at $3.91/lb on the time of writing in comparison with $2.70/lb in 2019, BHP’s FQ1’24 common realized costs of $3.63/lb (-4.4% YoY) and FY2023 common realized costs of $3.65/lb (-12.2% YoY).

With it commanding $6.7B of the corporate’s total adj EBITDA (-21.7% YoY), or the equal 23.7% (+2.7 factors YoY), we could anticipate H1’24 to deliver forth wonderful high/ backside line numbers certainly.

China’s Iron Ore Portside Stock Degree

MacroMicro

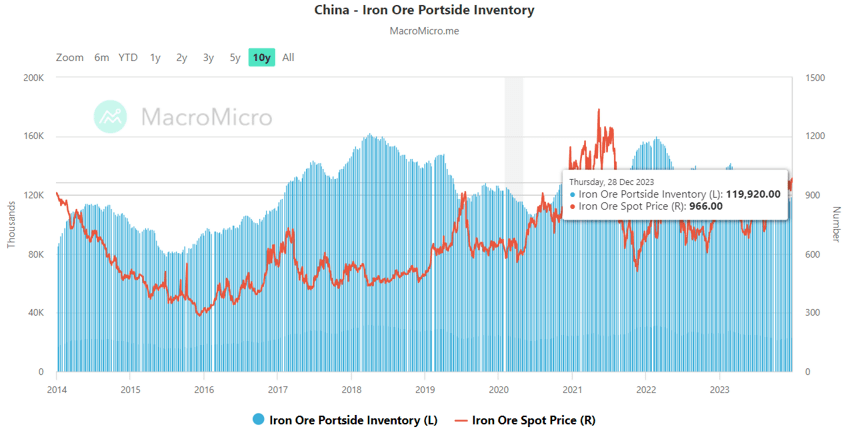

China’s lower portside inventory of 119.92K (-9% YoY) as of December 28, 2023 in comparison with the pre-pandemic averages of 131K additionally implies that iron ore spot costs could stay elevated for a bit longer, offering additional tailwinds to BHP.

The identical could happen for copper, attributed to the closure of First Quantum Minerals Ltd.’s (FM:CA) Cobre Panama mine, with the mine’s FY2022 manufacturing capability of 350.4K mt briefly negating the supposed supply surplus of 467K mt in 2024

BHP Valuations

Searching for Alpha

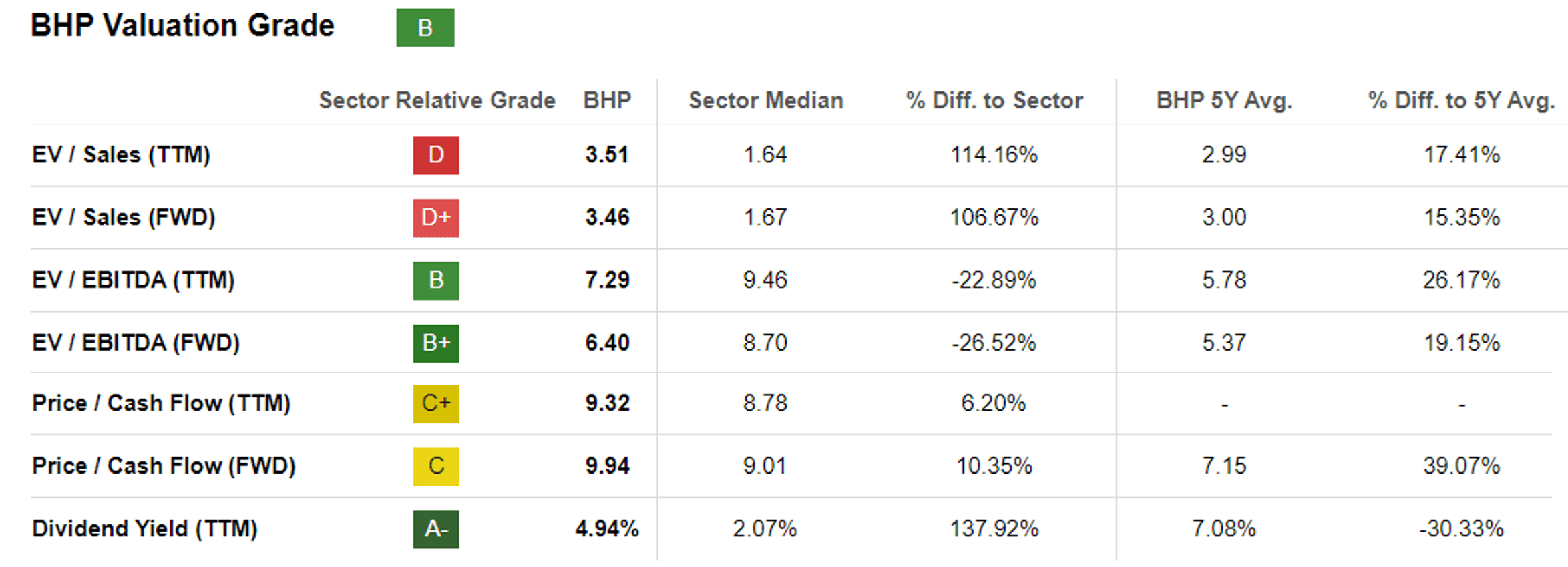

On account of these developments, we will perceive why BHP’s FWD EV/ EBITDA valuation of 6.40x and FWD Value/ Money Circulate valuation of 9.94x have recovered tremendously.

That is in comparison with its 1Y imply of 5.68x/ 6.80x, whereas lastly nearing its 3Y pre-pandemic imply of 6.12x/ 7.20x and the sector median of 8.70x/ 9.01x, respectively.

The Consensus Ahead Estimates

Tikr Terminal

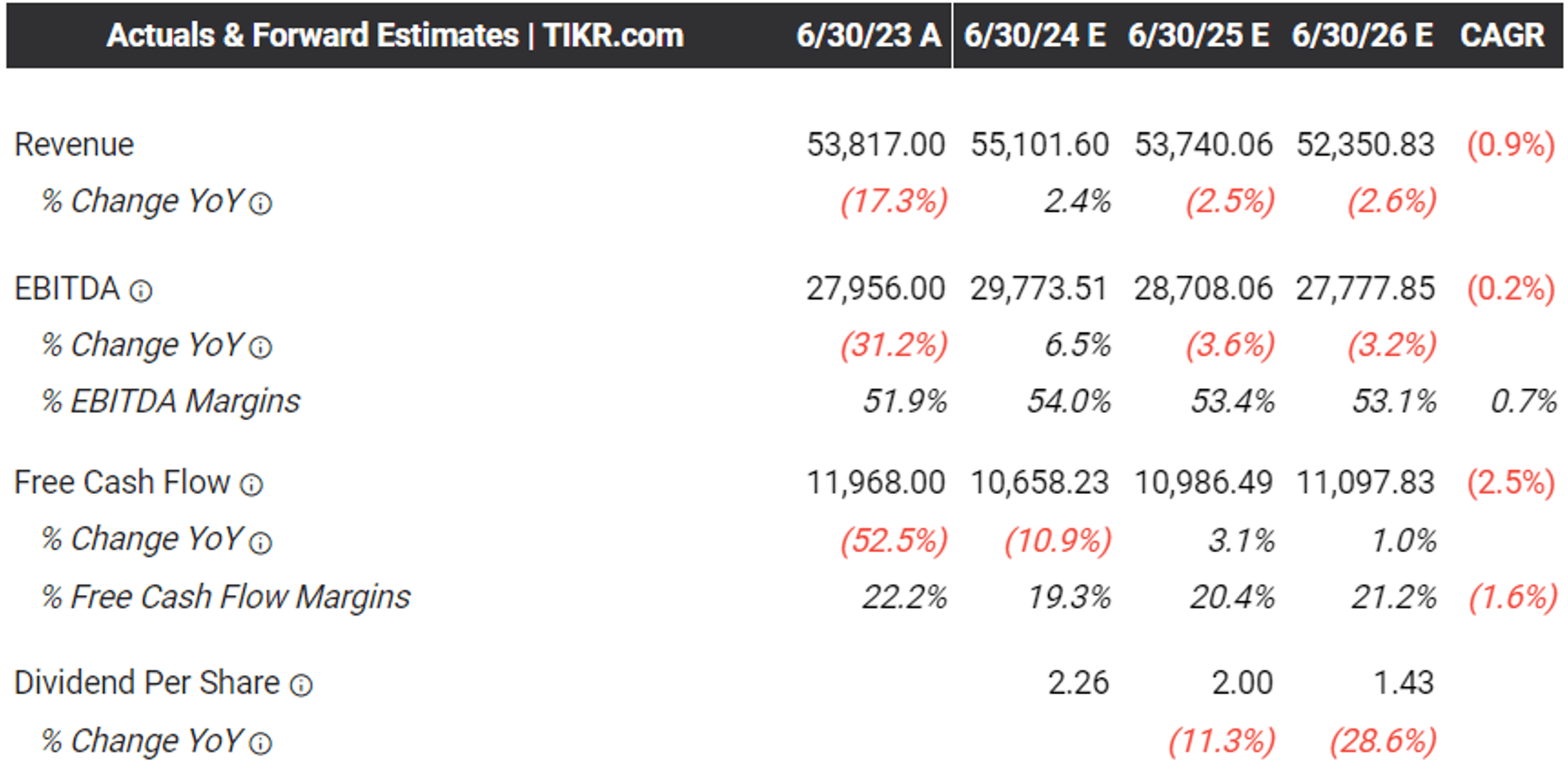

These valuations don’t seem inflated both, with the consensus nonetheless anticipating BHP to maintain its extremely worthwhile adj EBITDA margins of over 53% and FCF margins of over 19% by means of FY2026.

That is in comparison with its pre-pandemic averages of 49% and 23%, respectively, with the average decline within the FCF margins solely attributed to its intensified exploration capex for electrification metals equivalent to copper and nickel.

With BHP already guiding a superb development within the FY2024 copper manufacturing to 1,815 kt (+5.7% YoY) and nickel manufacturing to 82 kt (+2.5% YoY) on the midpoint, we consider that these expenditures will ultimately be accretive to its high/ backside traces within the long-term.

The administration has additionally guided a average enlargement in its annual copper manufacturing to 1,935 kt and a discount in its midpoint unit prices to $1.45 by FY2025/ FY2026, down from the present midpoint of $1.55.

This implies that BHP could ultimately generate improved adj EBITDA copper margins forward, up from the 47% reported in FY2023 (-4.1 factors YoY), additional boosted by the market analysts’ projection of the commodity’s larger spot costs of $4.985/lb by 2025.

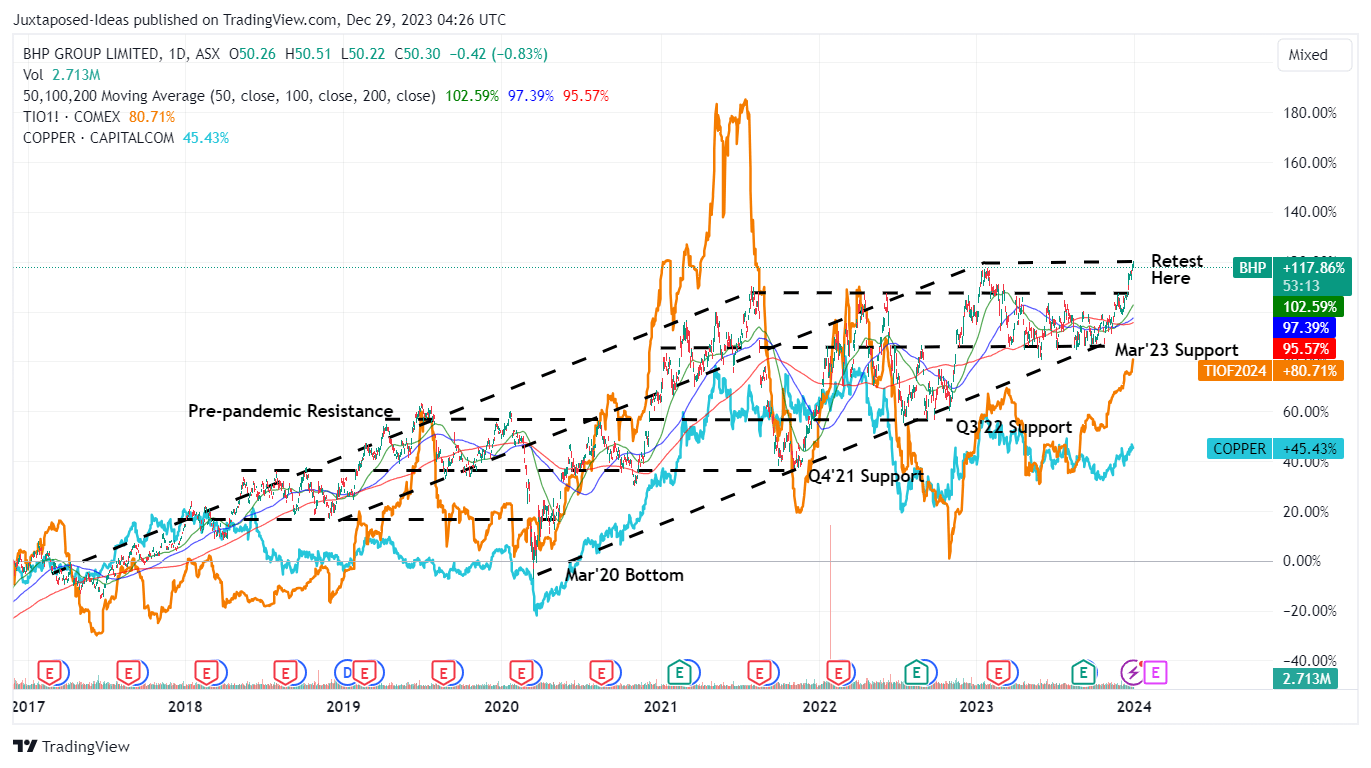

BHP 7Y Inventory Value

Buying and selling View

With BHP’s monetary efficiency inherently tied to the commodities’ dynamic spot costs, we will perceive why the inventory has additionally rallied because it has up to now, with it being properly supported by the notable premium over pre-pandemic spot costs.

So, Is BHP Inventory A Purchase, Promote, or Maintain?

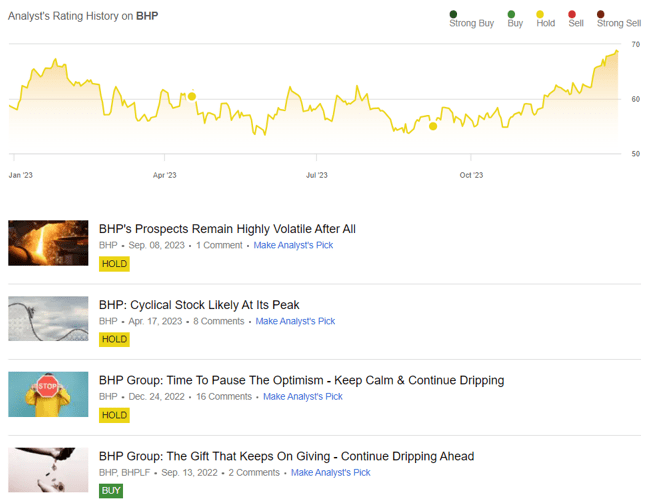

Writer’s Historic Score For The BHP Inventory

Searching for Alpha

Effectively, that is crucial query certainly. Our earlier Maintain ranking in September 2023 has confirmed to be unsuitable, with the BHP inventory already rallying by over +20% since then.

Most significantly, we admit that we had been grasping then, within the hopes of a decrease entry level of $52 for an expanded ahead dividend yield, with us already lacking the prepare.

Does this imply that we must always soar in right here? Not fairly.

The BHP inventory has quickly broke out of its 50/ 100/ 200 day shifting averages, with it at present retesting its January 2023 resistance degree of $70.

Assuming that the spot costs maintain its premium over the pre-pandemic averages, we might even see the inventory properly supported between $62 and $70s, providing buyers with a transparent buying and selling vary.

The BHP inventory’s current rally additionally leads to its decrease FWD dividend yields of 4.65% in comparison with its 4Y common of seven.62%, although nonetheless respectable in comparison with the US Treasury Yields of between 3.82% and 5.33%.

Its dynamic dividend funding thesis stays protected as properly, with a superb TTM Curiosity Protection Ratio of 25.21x and the administration dedicated to a 50% dividend payout coverage, regardless of the intensified capex over the following few years.

Consequently, we’re cautiously upgrading the BHP inventory as a Purchase, although with a caveat. Present shareholder could proceed dripping forward, permitting them to usually accumulate further shares on a quarterly foundation.

On the similar time, they could additionally average at any dips for an improved margin of security, relying on their greenback value averages, portfolio allocation, and threat urge for food.

With the inflation already cooling and the Fed open to a pivot by Q1’24, we might even see this optimism persist for a bit longer.

It goes with out saying that buyers who add BHP should achieve this as a part of a well-diversified portfolio, since its variable dividend payouts will not be appropriate for many who depend on common incomes.