justinecottonphotography/iStock via Getty Images

Note: All amounts discussed are in Canadian Dollars except when mentioned otherwise.

On our previous coverage of Birchcliff Energy Ltd. (TSX:BIR:CA), we laid out the facts. The company’s dividend policy was unsupported by its cash flows and was built on the hope of the 2025 natural gas pricing staying firm. We did not see the bull case and felt there were slightly better options for investors.

We maintain Birchcliff Energy Ltd. at a “hold” for now, but the risks are high if the 2025 strip weakens and the company insists on maintaining the dividend.

Source: That Dividend Might Need Another Trim

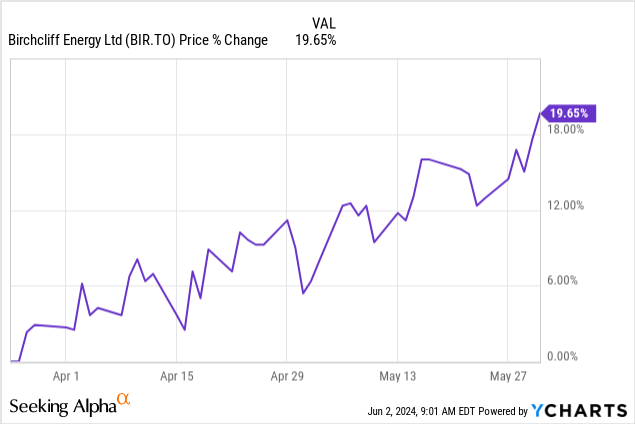

Obviously, the market had other ideas and the stock, like many other natural gas plays, had a rip-roaring rally.

Let’s look at the Q1-2024 results and see whether a more constructive outlook is indeed warranted.

Q1-2024

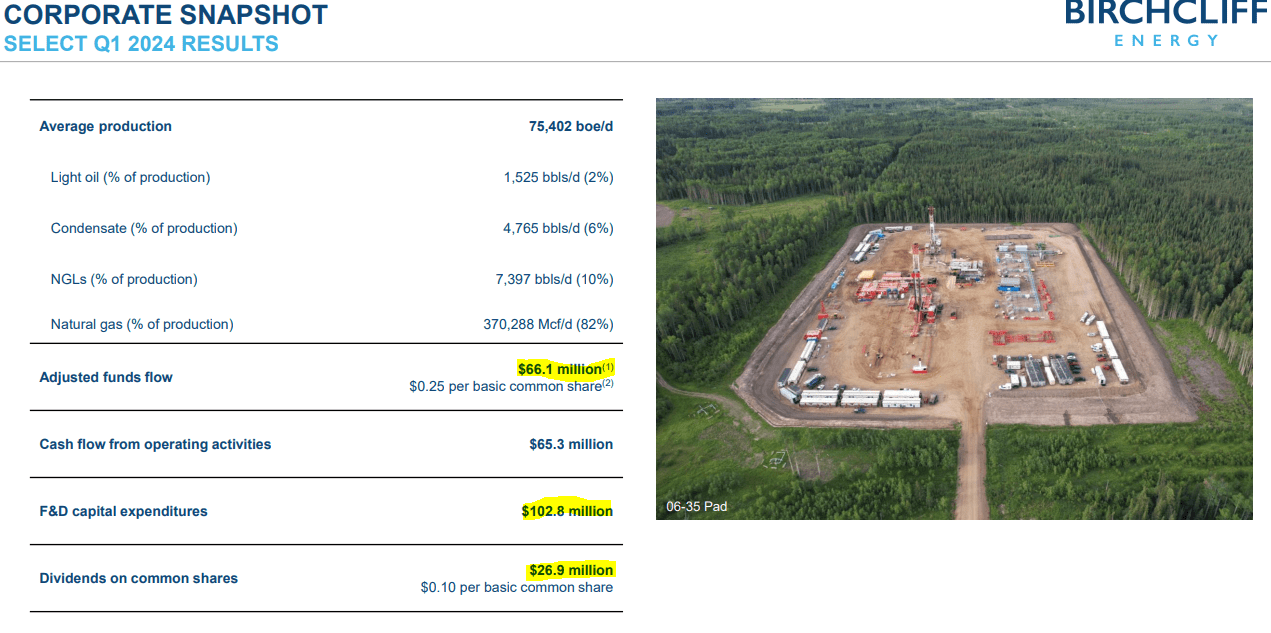

There were not a lot of surprises for investors in the most recent earnings report. With natural gas prices in the dumps and Birchcliff’s oil production looking close to a rounding error, it was apparent that the cash flow would be weak. With $66 million of adjusted funds flow, Birchcliff spent almost $103 million or about 155% of that. That amount and percentage is before dividends.

Q1-2024 Presentation

The total payout ratio for the Q1-2024 quarter was close to 200%. Obviously, the main nuance there is that capital spending does not follow a straight line through the calendar year. The second quarter in particular is extremely light as the snow melts in Canada and drilling activities are curtailed. There were a couple of positives in the report as well. Production came in about 1% ahead of consensus estimates. Birchcliff also updated their drilling guidance for 2024. There are two wells less joining the production stream in 2024 versus the previous communication. This will not impact the total expected production levels.

Q1-2024 Presentation

All in all, it was a good quarter considering how weak the pricing was for natural gas.

Outlook

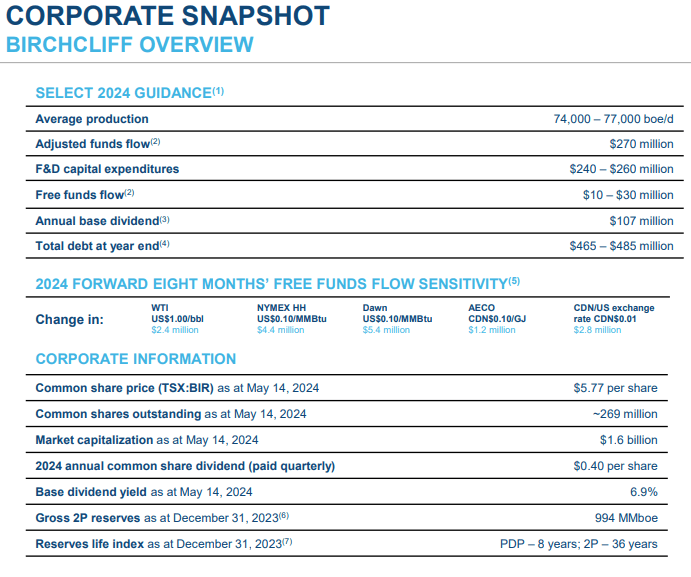

Birchcliff’s 2024 outlook shows adjusted funds flow of $270 million, capex of $250 million (midpoint) and a year end net debt of $475 million.

Q1-2024 Presentation

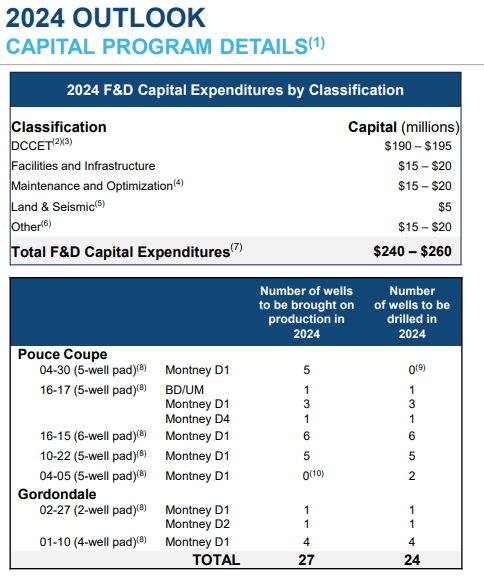

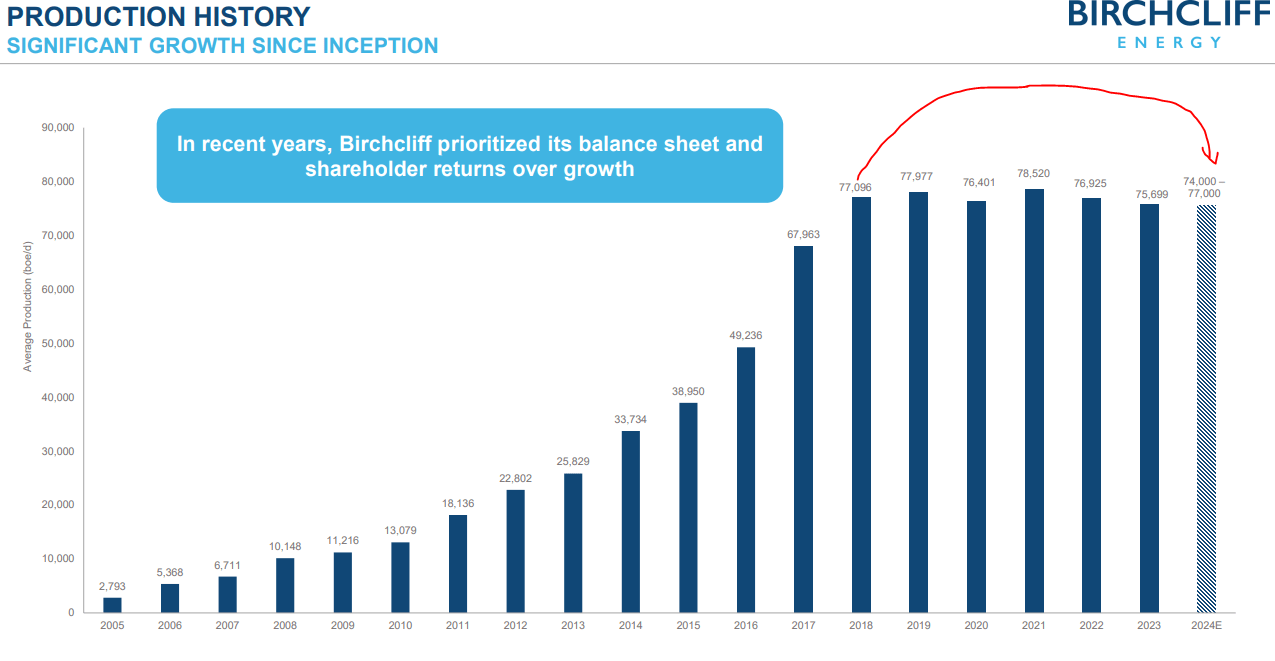

We have all moved past the strange setup apparently where 80%-90% of the dividend is financed using the balance sheet. That is in essence what is happening here. There is only $20 million leftover after the capex, and Birchcliff is still insisting on paying the $107 million dividend. Occasionally, you can break down the capex into growth and maintenance categories and argue that the dividend is “covered” if you strip out the growth component. Well, we, and the company, can assure you that there is no such thing happening here. At the midpoint of guidance, production will be slightly lower year over year for 2024. In fact. Birchcliff’s production has been flat since (brace for it), 2018.

Q1-2024 Presentation

We are not complaining about the flat production actually. If more companies had this discipline, then perhaps natural gas prices would not be so low. But the point at hand is that Birchcliff is insisting on blowing out its balance sheet. Also, in all likelihood, this could turn out to be worse than expected. The company is expecting the commodity deck for 2024 as follows.

With respect to Birchcliff’s 2024 guidance (as updated on May 15, 2024), such guidance assumes the following commodity prices and exchange rate: an average WTI price of USD$82.50/bbl; an average WTI-MSW differential of CDN$6.00/bbl; an average AECO price of CDN$2.05/GJ; an average Dawn price of US$2.15/MMBtu; an average NYMEX HH price of US$2.40/MMBtu; and an exchange rate (CDN$ to US$1) of 1.36.

Source: Q1-2024 Presentation

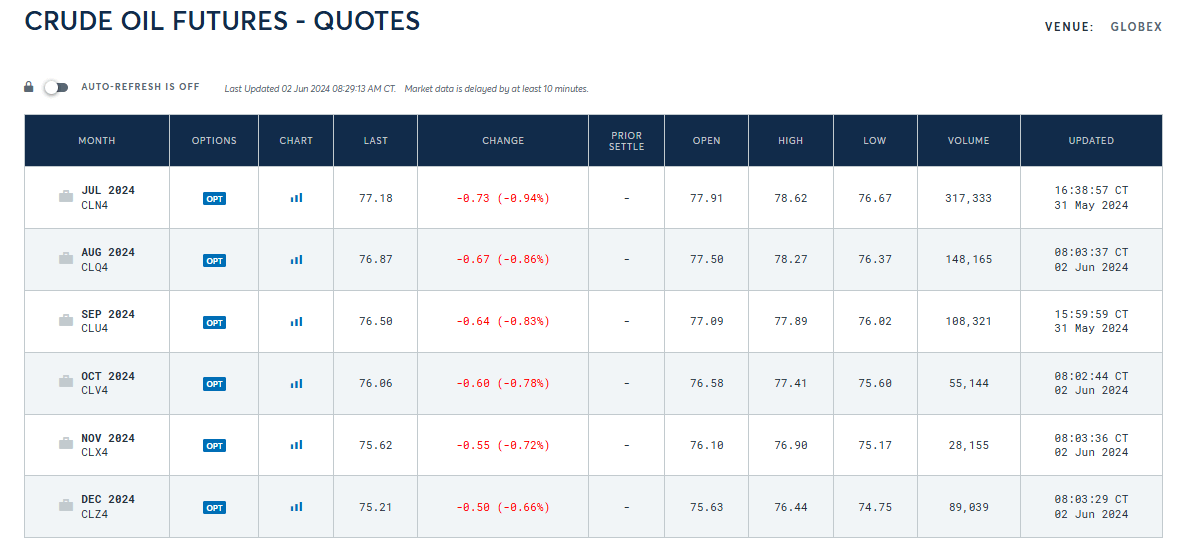

Oil forms a small part of the revenue base, but is a very high margin commodity for Birchcliff relative to natural gas. That pricing does not look like it is cooperating.

NYMEX

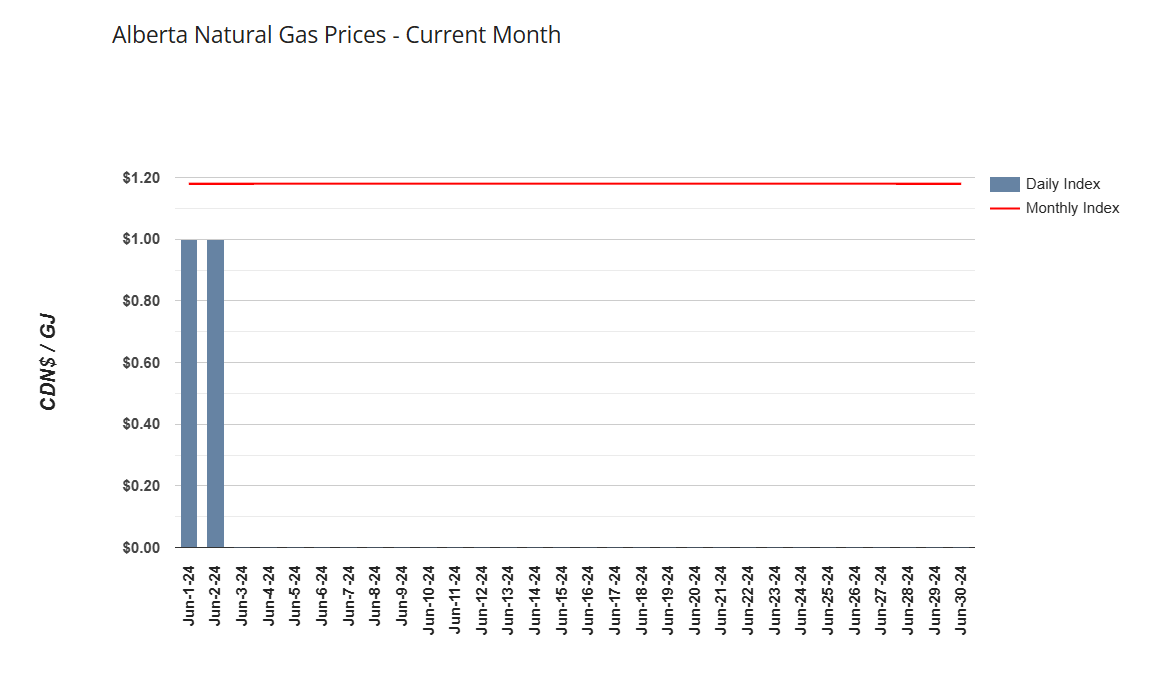

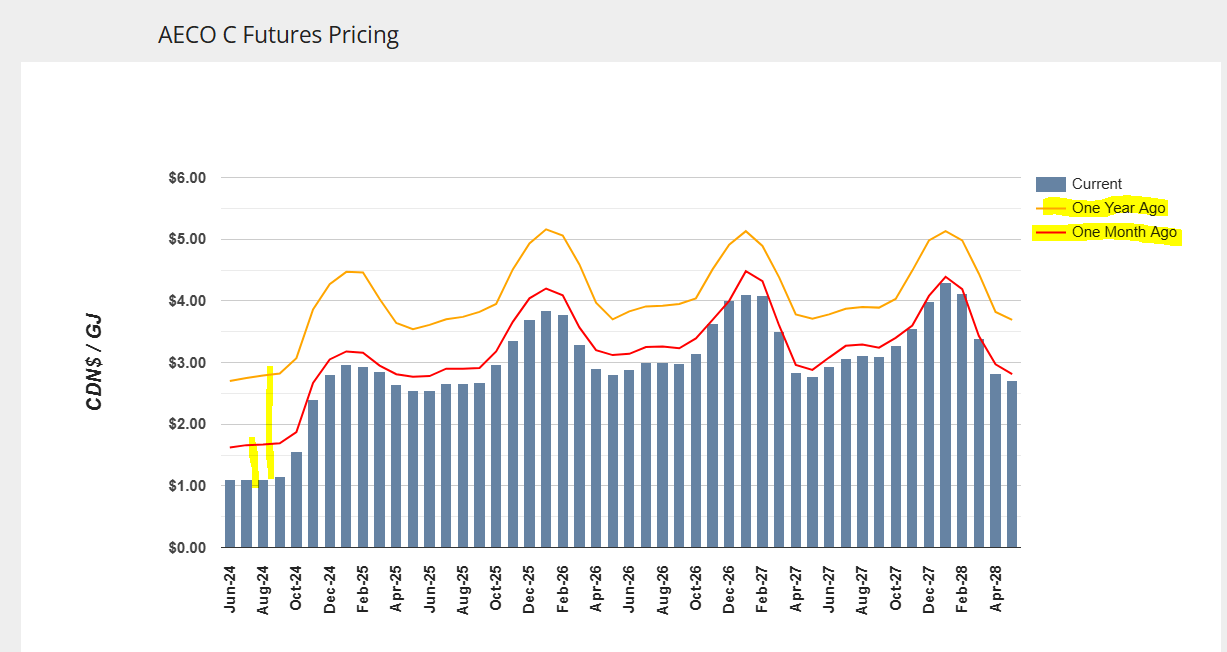

AECO prices look dead. Here are the numbers for the start of June.

Q1-2024 Presentation

The June to October strip has dropped from a month back and has been obliterated from levels seen a year back.

AECO

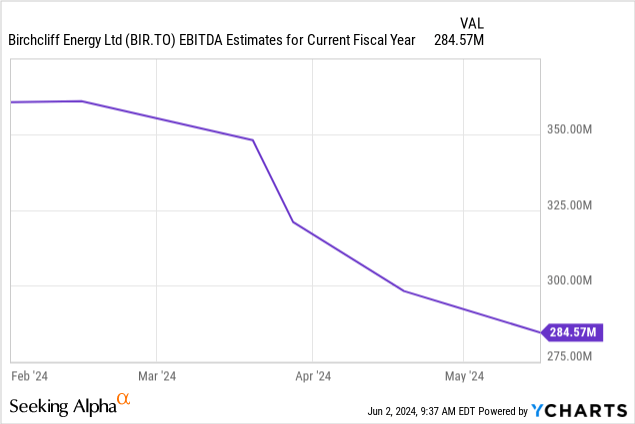

We will also draw your attention to the 2025 strip prices. They have weakened slightly compared to a month back, but the drop is significant compared to a year ago. We have also seen similar weakening in the NYMEX futures for 2025. So far, analysts have only adjusted the 2024 numbers to match this. 2025 estimates are still hovering near $450 million.

So the dividend continues to be resting on a lot of hope for price recovery down the line. We expect ending net debt for Birchcliff to cross $500 million at current strip prices, if the dividend is maintained.

Verdict

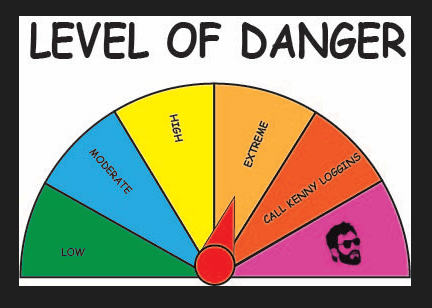

The numbers are the numbers. There is no room for “but management said” in that. You can, of course, embrace that natural gas prices are likely to go higher and pin your hopes on that. The reality has been that drilling in Canada has been more than adequate to hammer down and price increase. This, unfortunately, is symptomatic of the entire North American Natural Gas industry. They all get excited looking at demand projections. They also all act surprised when prices don’t go up after they drill more than enough to satiate demand. At least the ones with enough oil exposure and enough hedges deserve some added investor attention. Birchcliff has negligible oil exposure, and there are no hedges to talk about. They had their chance in 2022, when you had forward strips well over $3.50 on AECO. Now they will be lucky to get half that. We think the dividend cut is getting fairly close and if credit markets weaken, Birchcliff will take the dividend and chop it up. Birchcliff would get an “Extreme” level of danger of a distribution cut on our proprietary Kenny Loggins Scale.

Author’s Scale

This rating signifies a 50-75% probability of a distribution cut in the next 12 months. We rate this a Sell at this point.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult a professional who knows their objectives and constraints.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.