Bruce Bennett

The present scenario within the Center East in addition to current voluntary manufacturing limitations on the a part of main OPEC+ members strongly point out that BP (NYSE:BP) could possibly be set, not for a document 12 months in 2024, however for a strong 12 months when it comes to earnings nonetheless. After the escalation of the Israel-Gaza battle in October, Iran-backed Houthis have began to assault delivery within the Purple Sea and tensions with Iran additionally put in danger probably the most vital oil arteries on this planet: the Strait of Hormuz. Given this backdrop, I consider oil corporations typically might do effectively in 2024 and if OPEC+ continues to help product pricing all year long, BP might ship robust ends in 2024.

Earlier score

Solely pretty lately, in September, did I come round and upgraded shares of BP to buy within the context of OPEC+’s voluntary provide limitations. Shares of BP have declined 12% since, primarily because of falling petroleum costs. Saudi Arabia and Russia, two of the most important oil-producing international locations on this planet, determined to voluntarily restrict crude oil manufacturing: Saudi Arabia on the time curtailed its manufacturing by 1M barrels a day and Russia introduced a 300 thousand barrel a day export discount. Since then, nonetheless, OPEC+ members agreed to deepen manufacturing cuts and the safety scenario within the Center East has drastically deteriorated which I consider will in the end increase BP’s earnings potential. OPEC+ worth actions particularly are a purpose for me to double down on BP as the corporate is about from larger common petroleum costs. BP can be one of many least expensive manufacturing corporations within the large-cap vitality sector, with a P/E ratio of 6.5X.

Deteriorating Center East safety setup

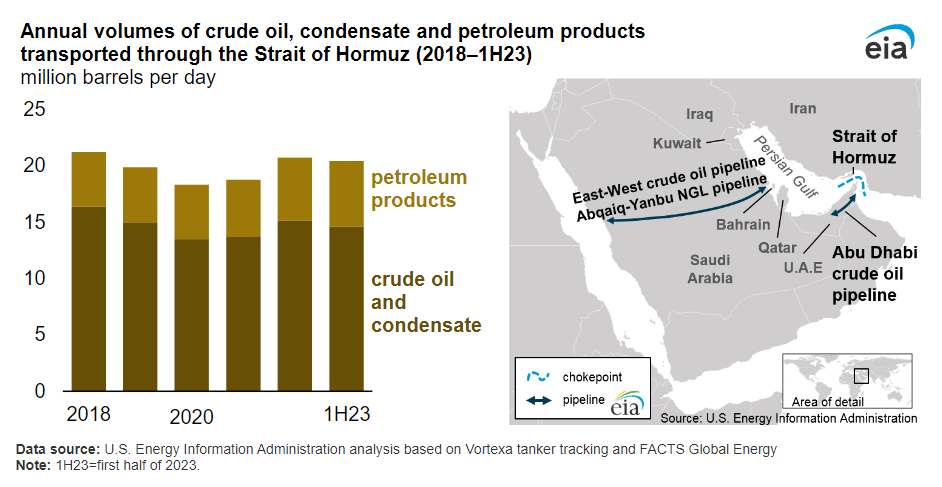

Quite a bit has occurred since I final labored on BP. Israel and Gaza are at warfare and Iran-backed Houthis are conducting assaults on container ships within the Bab-el-Mandeb Strait and the Purple Sea. Iran can be a risk to international oil provides by flexing its muscular tissues within the Strait of Hormuz, the strait that connects the Persian Gulf and the Gulf of Oman. The Strait of Hormuz is without doubt one of the most vital oil arteries on this planet and, in response to the Vitality Data Administration, the equal of 20% of worldwide petroleum liquids manufacturing passes by way of this strait.

EIA

Houthi assaults within the Purple Sea escalated because the group as the most important assaults on delivery on Tuesday. Clearly, escalating tensions within the Center East, which remains to be one of many world’s most vital geographies for petroleum manufacturing, is a possible catalyst for larger product costs. A barrel of petroleum at the moment prices about $72.68 which supplies vitality corporations like BP with the potential to develop their earnings if costs stay excessive all through 2024. The setup within the Center East is at the least favorable to such a situation in the intervening time.

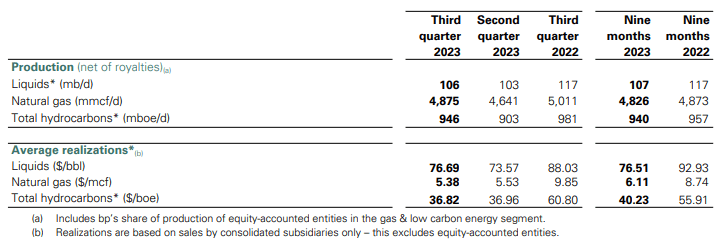

BP’s common petroleum worth within the third-quarter, for instance, was $76.69 per barrel which confirmed a decline of 13% in comparison with the year-earlier interval. BP’s quarterly worth breakdown was launched on the finish of October 2023 (Source). Nonetheless, with tensions within the Center East rising once more, there’s a appreciable likelihood for BP to learn from an uptick in pricing as effectively. Moreover, OPEC+ members reached an agreement in This autumn’23 to deepen manufacturing cuts till the top of Q1’24. My expectation for 2024 is that these output cuts shall be prolonged all year long with extra worth help measures seemingly ought to petroleum costs decline.

BP

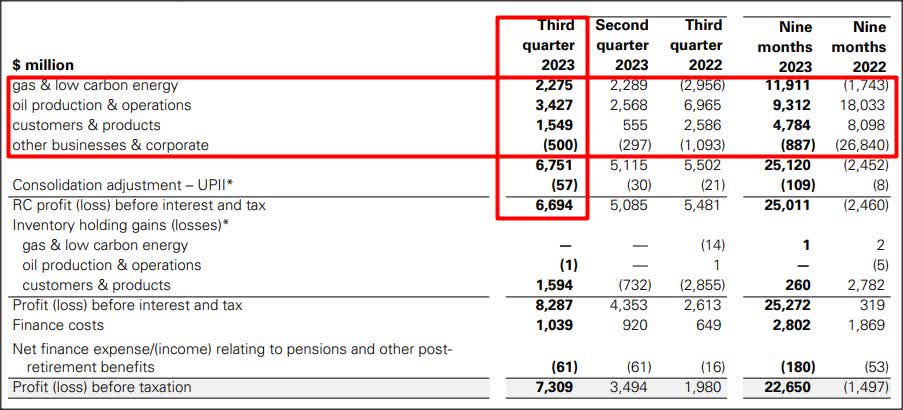

BP’s enterprise development improved within the third-quarter of FY 2023 because of a slight rebound in petroleum costs (the typical petroleum worth elevated 4% Q/Q in Q3’23). In complete, BP generated $6.7B in income (earlier than curiosity and taxes) within the third-quarter, the bulk coming from its oil manufacturing and operations phase ($3.4B). Clearly, BP is extensively worthwhile at a ~$73-74 worth degree which was about equal to the typical worth achieved for its petroleum merchandise within the second-quarter ($73.57). Throughout Q2’23, BP generated greater than $5.1B in earnings for its shareholders and the vitality agency has achieved a mean quarterly revenue of $8.3B in FY 2023 (up till September).

BP

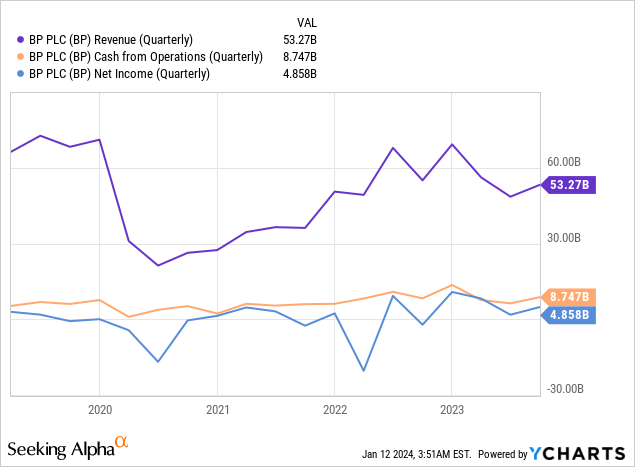

In the long run, BP’s revenues, money flows and earnings have confirmed to be extremely unstable… which is a mirrored image of broader market dynamics. BP’s earnings nose-dived through the pandemic, however they’ve since steadily recovered. The following bear market, nonetheless, could end in one more draw-down in BP’s revenues and earnings.

BP’s valuation vs. U.S. rivals

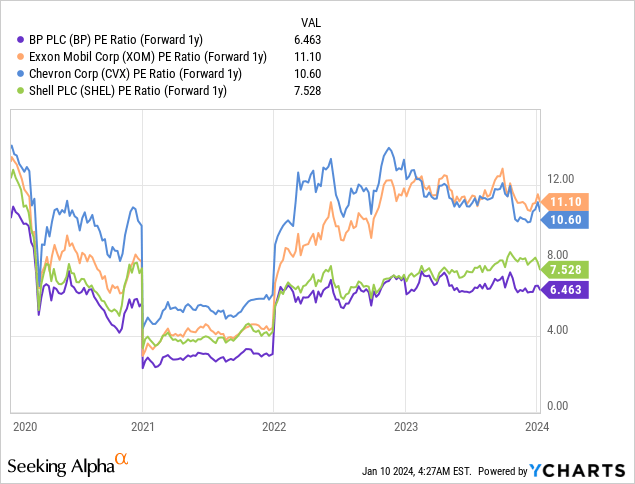

BP appears to be buying and selling at a very low-cost valuation multiplier. With excessive costs for petroleum merchandise boosting the vitality sector’s earnings, BP has seen a decline in its P/E ratio. Nonetheless, even into account of cyclically-inflated EPS, BP is buying and selling at a lovely price-to-earnings ratio of 6.5X, for my part, and the British vitality firm is even cheaper than Shell (SHEL) which has a 7.5X P/E ratio. BP is projected, on a consensus basis, to earn $5.35 per-share subsequent 12 months which underpins the valuation and the agency is predicted to develop its earnings ~5% yearly within the subsequent two years.

ExxonMobil (XOM) and Chevron (CVX), to incorporate the 2 greatest U.S. rivals out there, commerce at P/E ratios of 11.1X and 10.6X. I consider BP might simply commerce at 8-9X FY 2024 earnings given its excessive degree of quarterly profitability and assuming that petroleum costs stay excessive in FY 2024, which suggests a good worth vary of $42-47. My multiplier vary (8-9X) and honest worth estimate don’t change with brief time period fluctuations in petroleum costs. U.S. rivals additionally commerce at larger valuation ratios than BP, suggesting that the agency has revaluation potential as effectively.

BP may be undervalued relative to U.S. corporations because of their stronger dividend information and aggressive inventory buybacks which have supplied help for his or her share costs. U.S. corporations are additionally closely invested in U.S. shale areas which, at the least theoretically, provide the potential for quicker manufacturing development.

Dangers with BP, Outlook 2024

Petroleum costs are unpredictable and influenced by world occasions resembling terrorist assaults, wars, pure catastrophes and financial declines. Present tensions within the Center East particularly have the potential to result in a pointy uptick in petroleum pricing if the safety scenario additional deteriorates. Alternatively, a decision of the Israel-Gaza battle and particularly a much less aggressive posture of Iran within the Strait of Hormuz might result in a lot decrease petroleum costs and subsequently diminished earnings potential for BP.

Consequently, BP’s particular product pricing dangers translate into doubtlessly depressed profitability throughout a down-turn within the vitality market which then might cascade right into a slower tempo of dividend development or a decrease quantity of inventory buybacks that help BP’s inventory worth. Petroleum costs are clearly the most important affect on BP’s financials and given the worth help the OPEC+ has supplied right here most lately, OPEC+ output selections needs to be carefully adopted and monitored. My expectation is for OPEC+ to proceed to be price-supportive pressure in 2024. BP’s common costs within the manufacturing enterprise are additionally price following as a decline in pricing will instantly translate to decrease revenues and earnings.

If petroleum costs stay excessive, nonetheless, I might not be shocked to see inventory buybacks or doubtlessly even new acquisitions in 2024 and past. BP is subsequently, mainly, a capital return play for traders in a market the place OPEC+ could play a extra aggressive function going ahead.

Closing ideas

Center Japanese tensions, particularly in Israel-Gaza, the strait of Hormuz and the Purple Sea are regarding tendencies. An escalation of the Israel-Gaza scenario, which can draw Iran additional into the battle, can be a worst-case situation given the significance of the Strait of Hormuz for international crude oil provides, however seemingly favorable from a pricing viewpoint. BP remains to be extensively worthwhile at petroleum costs of $73 per barrel and I consider the present safety scenario within the Center East, a low P/E ratio relative to U.S. rivals and an aggressive OPEC+ group make BP general a high guess on petroleum markets in FY 2024!