PM Photos

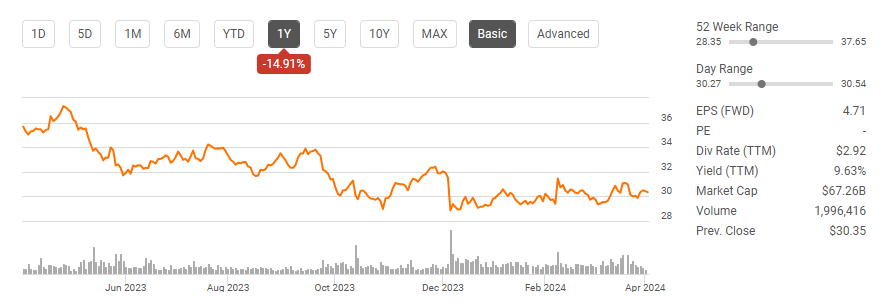

The earlier 12 months have not been type to British American Tobacco (NYSE:BTI) as shares have declined -14.91%, and it has been an excellent worse decade as shares have fallen -46.46%. The tobacco trade repeatedly finds itself beneath strain because it’s synonymous with well being dangers and authorities laws. Regardless of particular person opinions, the details are that BTI has exceeded $10 billion in operating income and free cash flow (FCF) on an annualized foundation since 2018 whereas producing massive single-digit dividend yields. Once I have a look at BTI from a enterprise perspective, it appears to be like tremendously undervalued, and I’ve not too long ago added it to my place. Similar to Altria Group (MO), I really feel the notion of BTI’s enterprise and never its precise operational efficiency is the rationale why shares haven’t caught a bid. Whereas expertise controls the narrative and has fueled the rally, I believe the broad market will catch up over the following yr, and BTI will likely be seemed again on as a chance that obtained away fairly than persevering with to be a worth entice. I’ll proceed including to my place at these costs and fortunately sit again and acquire the dividends whereas I watch for my funding thesis to unfold.

Looking for Alpha

Following up on my earlier article about British American Tobacco

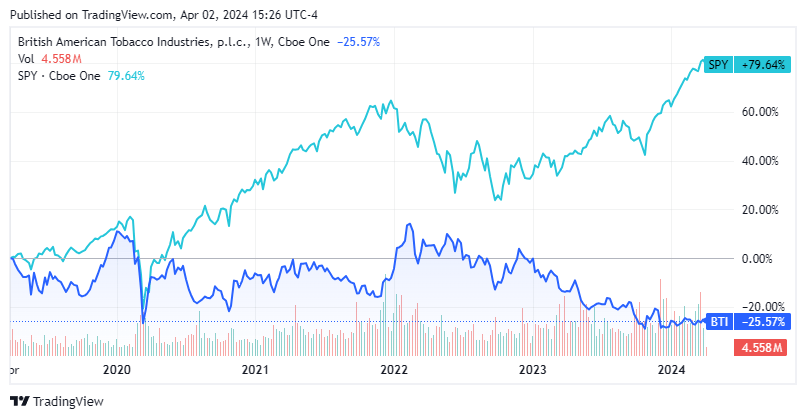

I have never written about BTI in a while, as my final article was printed on July 19th, 2021 (can be read here). Since then, shares of BTI have declined by -20.83% in comparison with the S&P 500 appreciating by 20.98%. I’ve been incorrect up to now, and Mr. Market has different plans for shares of BTI. Not even the big dividend yield has been capable of make shareholders entire. When the dividends are factored in, BTI has a complete return of -3.75% as an incredible quantity of worth has eroded from shares over the previous 2 ½ years. In that article, I mentioned BTI’s enterprise and why I felt its profitability would result in a greater valuation and a bigger dividend. Properly, I’ve been incorrect concerning the higher valuation, and whereas the dividend has grown, BTI hasn’t been an excellent funding. I’m following up with a brand new article to debate why I’m nonetheless bullish on BTI and really feel shares have bottomed.

Dangers to my funding thesis in BTI

BTI is not an funding for people who do not have a excessive tolerance for threat. The tobacco trade has been scrutinized for many years as the businesses throughout the sector must repeatedly adapt to evolving laws. The most recent from the U.S. Food and Drug Administration is that they’re proposing to ban menthol-flavored cigarettes within the U.S. BTI faces dangers from legislative authorities as well being considerations proceed to color a damaging stigma and drive adjustments to current legal guidelines. There was a big alternative price as a typical S&P 500 index fund has outperformed BTI over the previous 5-years, and there’s no expertise narrative round A.I. or cloud computing that may stimulate investor enthusiasm. BTI faces operational dangers from the worldwide economic system in addition to its rivals. If we endure unfavorable tobacco harvesting circumstances, then BTI may face a diminished provide and a lower within the availability of tobacco. As we transfer to a smokeless trade, BTI can even face enhanced competitors as Altria Group and Philip Morris (PM) allocate billions towards oral tobacco and heated tobacco merchandise fairly than flamable.

Looking for Alpha

Breaking down why I’m bullish on BTI whatever the damaging stigma on tobacco

A number of individuals have requested me how I can put money into tobacco corporations. Tobacco has been round for hundreds of years, and tobacco merchandise are authorized regardless of the correlation to well being circumstances. I’m wanting on the enterprise from a profitability standpoint, and till tobacco merchandise are deemed unlawful, I’ve no points investing in them if I really feel there’s a potential upside to allocating capital. At the moment, I’m viewing BTI as a worth play fairly than a worth entice and really feel there’s a vital alternative in its shares on a forward-looking foundation. Anybody can have a look at the chart and see that shares have been down nearly 50% over the previous decade, however it’s not about the place shares got here from; it is about the place they’re at present and the place they’ve the potential to go. This jogs my memory a whole lot of the MLP trade as shares plummeted for a lot of corporations, comparable to Power Switch (ET) and Enterprise Merchandise Companions (EPD), from 2014 – 2016 when the worth of oil quickly declined, then once more after the pandemic began. Whereas a gasoline transition narrative continued to be painted, buyers who began positions in ET and EPD throughout 2021 have generated vital earnings from the distributions and capital appreciation. I believe BTI is in an analogous state of affairs, and the basics are too robust for shares to commerce at this low valuation.

Beginning with the steadiness sheet, BTI has a robust basis beneath its working companies. BTI has $5.94 billion in money readily available, with one other $766.2 million in buying and selling asset securities. BTI has one other $2.66 billion in long-term investments, which brings the liquidity on its steadiness sheet to $9.37 billion. That is 20.86% of the $44.91 billion in long-term debt on its steadiness sheet. BTI has $151.34 billion in complete property and $67.01 billion in complete liabilities, which brings the corporate’s fairness to $67.48 billion. BTI additionally has a ebook worth of $29.08, which is a stable basis for its share worth of $30.32, which does not commerce at that enormous of a premium.

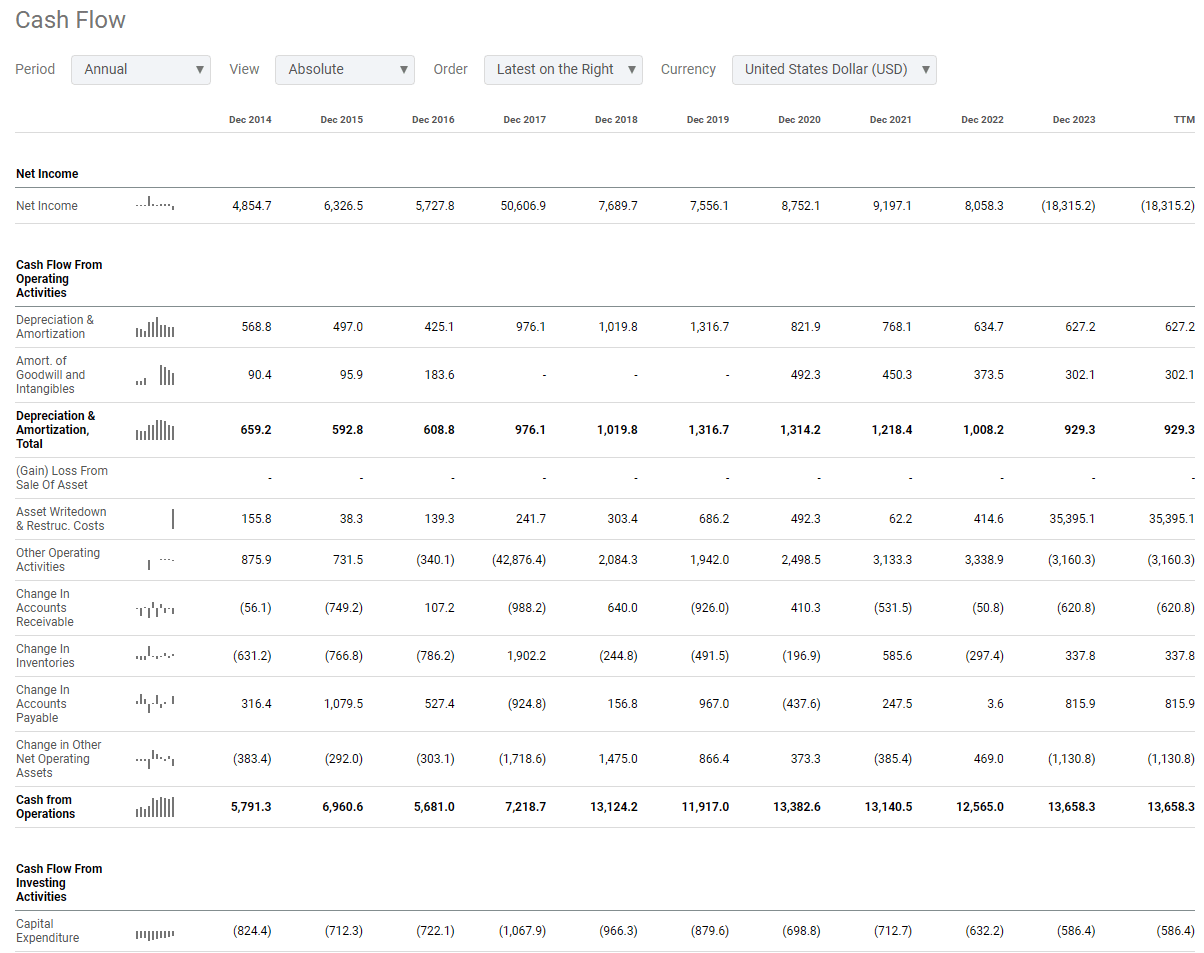

From an working standpoint, BTI is working a particularly worthwhile enterprise. After BTI acquired the remaining 57.8% of Reynolds American Inc. in 2017, its income and profitability considerably elevated. Whereas the income and profitability has been stagnant, BTI is producing tens of billions in each classes. In 2022, BAT generated $33.43 billion in income, and its income price was $5.81 billion. This left BTI with a gross revenue of $27.62 billion and a gross revenue margin of 82.63%. BTI operates on the similar ranges as SaaS corporations, and fairly truthfully, if this was a SaaS firm, I’d guess the valuation can be a lot totally different. BTI produced $14.96 billion in EBITDA, which is a margin of 44.75%. BTI’s FCF got here in at $11.93 billion for a margin of 35.69%, and its internet earnings in spite of everything taxes and curiosity funds was $8.28 billion for a revenue margin of 24.67%.

In 2023, BTI grew each class besides its internet earnings because of the affect of the non-cash impairment charge taken primarily in opposition to their acquired U.S. manufacturers. Because of this I have a look at each internet earnings and FCF as a result of FCF is not impacted by GAAP Accounting rules as a lot as internet earnings, it is merely money in minus money out. BTI grew its income by 4.01% to $34.78 billion YoY. Its gross revenue got here in at $28.55 billion, which was a rise of $921.8 million (3.34% YoY). This positioned BTI at an 82.07% gross revenue margin, and so they generated $16.92 billion in EBITDA and $13.07 billion in FCF. BTI took a cost of -$21.75 billion and had an -$3.66 billion earnings tax expense in 2023, inflicting its internet earnings to be -$18.09 billion. That is an anomaly because of the impairment, and looking out on the working earnings for 2023, which got here in at $16.11 billion, BTI is working like a well-oiled machine.

Looking for Alpha

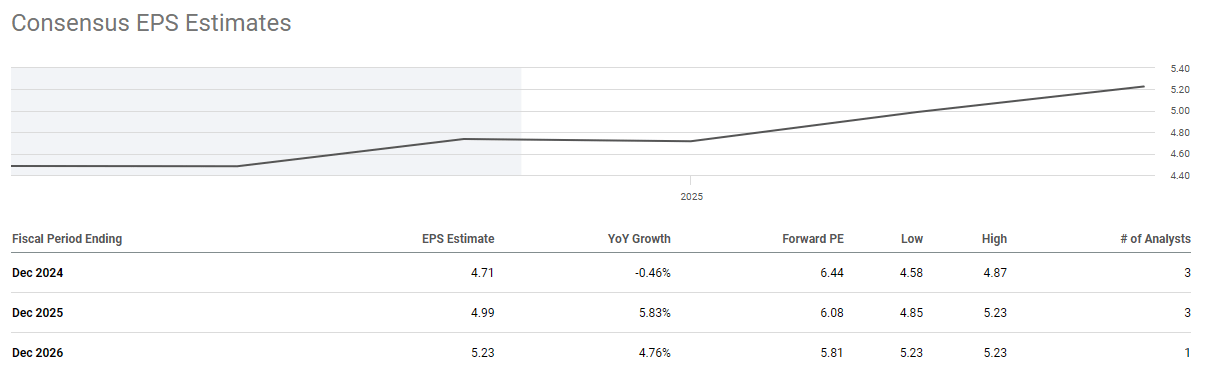

It isn’t usually which you can buy an organization at 6.44 occasions earnings, however in BTI’s case, that is the fact. The market is deeply discounting its profitability because of the trade during which it operates in. This may both be a purple flag or a chance, and I see this as a chance to amass shares of a particularly worthwhile firm for a low valuation. BTI is presently buying and selling at 6.44 occasions its 2024 earnings and 5.8 occasions its 2026 earnings. Over the following 2 years, BTI is predicted to develop its EPS by 11.04%. Whereas BTI appears to be like undervalued on this metric alone, it trades at a less expensive valuation in comparison with its friends of Altria Group and Philip Morris. Altria trades at 8.55 occasions 2024 earnings, whereas Philip Morris trades at 14.41 occasions 2024 earnings. I additionally checked out their worth to FCF to see what number of years it could take for these corporations to generate their complete market cap in FCF. BTI is buying and selling at 5.19 occasions its present FCF, whereas Altria trades at 8.48 occasions and Phillip Morris trades at 18.11 occasions. Whatever the trade that BTI is working in, this money cow generates billions upon billions in income and is even discounted in comparison with its friends.

Steven Fiorillo, Looking for Alpha

Steven Fiorillo, Looking for Alpha

Looking for Alpha

BTI is gearing up for an enormous capital allocation plan for shareholders

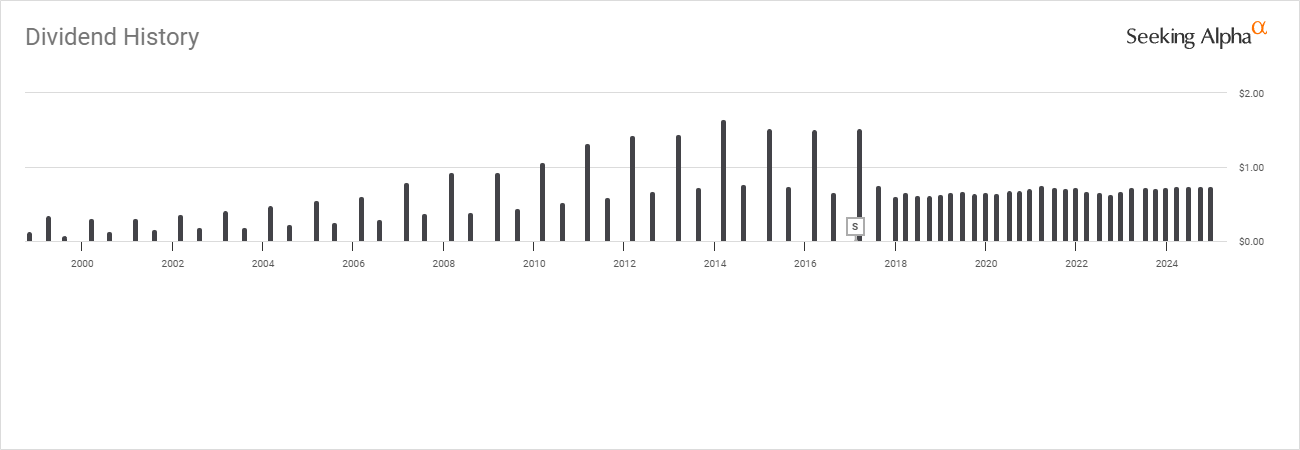

Along with producing massive income, BTI pays a dividend of $2.92, which is presently a yield of 9.63%. BTI has established a 20-year monitor report of progressive dividend development, and after the Reynolds American Inc. acquisition in 2017, BTI modified its fee frequency to quarterly fairly than bi-annually. In 2023, BTI paid $6.52 billion in dividends to shareholders, which was solely 49.87% of the FCF that was generated. There’s a whole lot of room for administration to proceed rising the dividend whereas discovering different methods to reward shareholders.

On the This autumn convention name, administration indicated that they ended the yr at 2.6 occasions adjusted internet debt to adjusted EBITDA, which is nearer to the center of their goal vary of 2-3 occasions. Administration additionally disclosed that after the center of its goal vary is reached, they’ll consider extra choices to return extra money to shareholders, together with discussing the introduction of a sustainable buyback plan. BTI is projecting that it’ll generate $43 billion in FCF earlier than dividends within the subsequent 5-years. If BTI will increase the dividend by 2% on an annual foundation, it can pay out round $34.61 billion in dividends over the following 5-years, and it could nonetheless have round $8.4 billion in FCF left. They might simply develop the dividend by 2% on an annual foundation and purchase again $1 billion value of shares yearly whereas using the remaining FCF to develop their enterprise.

Looking for Alpha

Conclusion

The tobacco trade has seen higher days, however it’s nonetheless a particularly worthwhile endeavor for trade leaders. Should you can look previous the trade, BTI appears to be like like a chance at at present’s ranges fairly than a worth entice. BTI is paying a dividend of 9.63% and trades for six.44 occasions its 2024 earnings. In 2023, BTI generated $13.07 billion in FCF, which locations its worth at 5.19x. The key threat is that laws proceed to evolve and make doing enterprise tougher for tobacco corporations. I’m prepared to simply accept that threat as tobacco corporations have been adapting to altering laws for many years and are nonetheless producing billions in income. BTI appears to be like extraordinarily undervalued by conventional requirements, and after I examine them to their friends, I see that they commerce at a reduced valuation. I really feel there is a chance to lock in a 9.63% yield on price at at present’s ranges and that there’s potential for capital appreciation on the horizon with BTI. They’re placing their capital to work, and if they’re able to implement a buyback program, its ahead EPS ought to enhance, and I believe it can grow to be an funding alternative that many won’t ignore. I’m lengthy BTI and including to my place.