RichHobson/E+ through Getty Photographs

Introduction

Depend me as one of many individuals who additionally suppose rates of interest will likely be lower someday quickly. When to be actual? Nobody is aware of, however I do suppose we’ll get one someday this 12 months. There’s additionally an opportunity we will get one other enhance earlier than cuts as seen by the newest CPI report.

So, which one is it? A elevate or lower? Both approach charges will finally decline and once they do, I feel traders ought to be invested in REITs to learn from their share worth appreciation potential. One REIT to think about is Broadstone Web Lease (NYSE:BNL). On this article I will focus on what I like about BNL and why they’re a top quality REIT it is best to think about in your portfolio.

Who’s Broadstone?

Broadstone Web Lease is an internally-managed REIT that was based in 2007 and IPO’d 13 years later in 2020. So, so far as a publicly traded firm, their observe report is fairly brief all issues thought of. However there are issues I actually like in regards to the firm. For starters, they take pleasure in an internally-managed construction.

Much like Enterprise Growth Corporations or BDCs for brief, REITs could be both externally or internally-managed. That is essential for some traders as most favor an internally-managed construction as they usually are extra shareholder-friendly in nature. Moreover, they often retain extra capital as they do not need to pay managers exterior of the corporate to handle the enterprise, therefore the title externally-managed.

A few of these charges could be fairly costly as some managers receives a commission a considerable quantity for his or her managerial expertise. Moreover, being internally-managed often permits the corporate to retain additional cash to both develop the enterprise organically, or go on to shareholders within the type of dividends. So, though they’ve a shorter observe report, I like the truth that they’re internally-managed, a plus for the REIT.

Portfolio Diversification

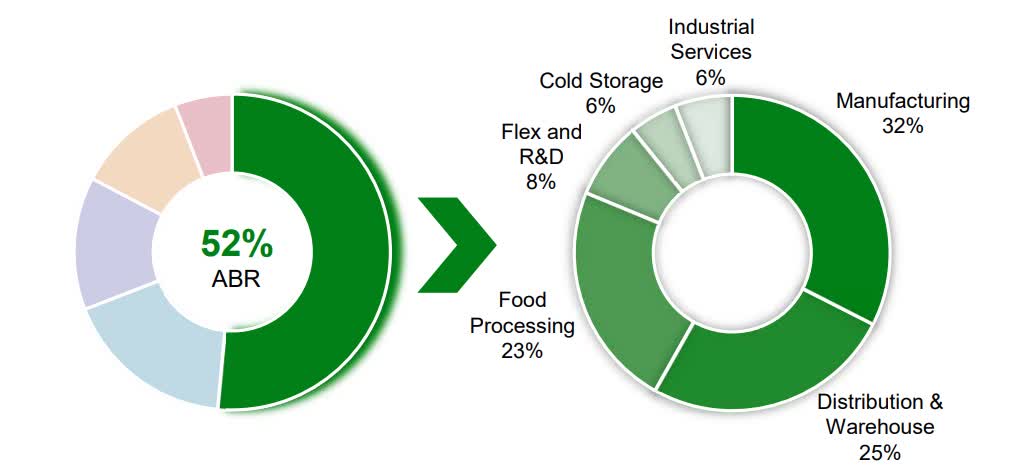

Apart from being internally-managed, I additionally like that they’re diversified with 796 properties throughout 44 states. Additionally they have properties in 4 Canadian provinces which is nice for traders trying to diversify exterior of the U.S. Moreover, BNL has 51% of their portfolio within the industrial section which accounts for 52% of annualized base hire.

BNL investor presentation

Apart from industrial properties, their portfolio can be wide-ranging throughout the retail, restaurant, and healthcare segments. These account for 18%, 13%, and 11% annualized base hire respectively. And a few of these tenants embrace MedVet, Outback Steakhouse, and Greenback Common (DG).

One thing else I like about Broadstone is their leases are usually longer than some friends at 10.5 years on common. That is compared to bigger, and extra widespread peer, Realty Revenue (O) whose common preliminary lease time period is 10 years. And smaller peer, World Web Lease (GNL) whose WALT is 7.6 years.

For a REIT of their measurement, 10.5 years is an effective benchmark as a result of it locks in steady earnings for a considerable period of time. So, traders trying to put money into REITs, longer weighted-average lease phrases are a optimistic and one thing to concentrate to when deciding to take a position or not. Close to or round 10 12 months lease phrases is one thing I often wish to see from my investments.

Apart from engaging lease phrases, their common hire escalators are also barely larger at a mean of two% vs 1% – 1.5% for friends like Agree Realty (ADC) and NNN REIT (NNN).

Moreover, they solely have a small quantity of their leases expiring within the subsequent two years at 1.2% and 1.8% respectively. After 2025, it rises fairly a bit to 4.3% and a mean of 6.2% for the subsequent 3 years. However most of their leases expiring happen a lot later in 2030. So, their earnings and income are more likely to be steady the subsequent few years with minimal lease expirations.

Stable Dividend Protection

The REIT’s present dividend of $0.285 can be well-covered by their AFFO. For the full-year BNL’s AFFO was stable giving them a dividend protection ratio of roughly 1.25x. BNL elevated the common dividend twice in 2023, first from $0.27 to $0.28 then from $0.28 to $0.285.

AFFO for the full-year averaged $0.3525. I might have preferred to see some development over the past three quarters the place this remained comparatively flat, however creeped up $0.02 from Q1.

And it did enhance barely year-over-year from $67.5 million in Q1 to roughly $71.3 million within the newest quarter. To shut out the 12 months, BNL’s present AFFO payout ratio is roughly 81% contemplating the 196,373 shares excellent. That is larger than administration’s focused vary of mid to excessive 70’s however seeing how REITs are required to pay out extra within the type of dividends by regulation, that is one thing that does not concern me.

I do nevertheless wish to see my REITs with a decrease payout ratio. Going ahead although that is one thing traders ought to be keeping track of as REITs usually difficulty extra shares to boost capital. The next payout ratio additionally permits much less room to retain capital to deploy into the enterprise to proceed development.

Properly-Laddered Debt

I favor REITs to have a payout ratio of lower than 80%, extra so within the 70% – 75% vary. However a better one like BNL’s is just not alarming, no less than for now as I beforehand talked about. However throw in an enormous debt load, and you’ll see why this might doubtlessly turn into an issue sooner or later if it certainly turns into too excessive.

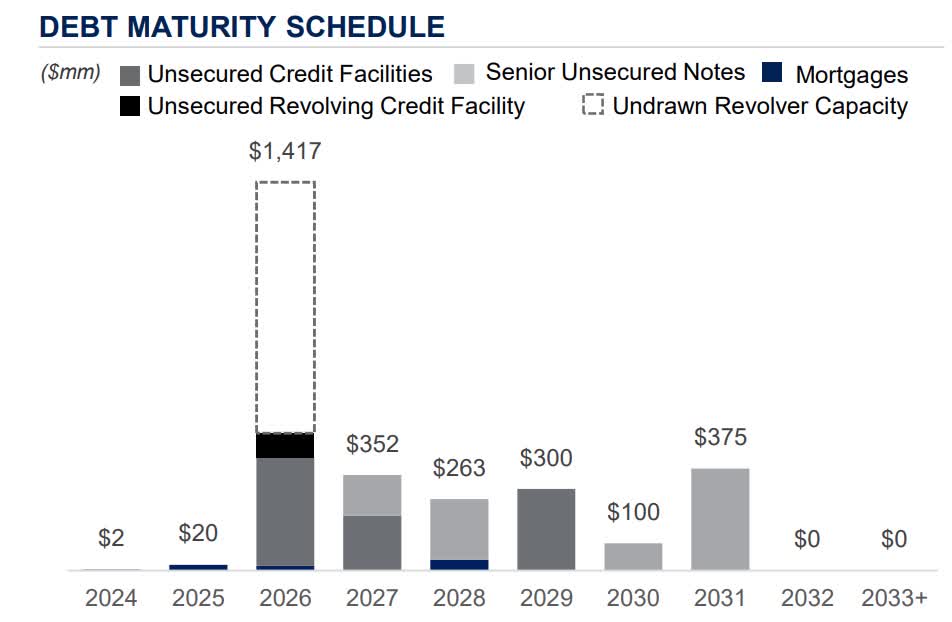

Good factor is BNL’s stability sheet stays robust with a net-debt-to-EBITDA ratio of 5x. This additionally decreased from 5.2x on the finish of 2022. Their fixed-charge protection ratio was additionally wholesome at 4.5x they usually at present have a BBB credit standing. Moreover, the corporate has little debt maturities to fret about for the subsequent two years. As you’ll be able to see within the chart under and acknowledged beforehand, most of their debt maturities are available 2026.

BNL investor presentation

By then I think rates of interest will likely be a lot decrease than present ranges. Their liquidity additionally stays robust with practically $1 billion out there. This offers them ample capital and adaptability to deploy it, benefiting from funding alternatives sooner or later.

Valuation

On the present worth on the time of writing, BNL’s P/AFFO ratio of 11.1x is decrease than the typical 14.3x for retail friends. It is also decrease than the sector median’s 13.52x. The REIT additionally trades decrease than its book value giving them a P/B ratio lower than 1x, signaling they could be undervalued in the mean time.

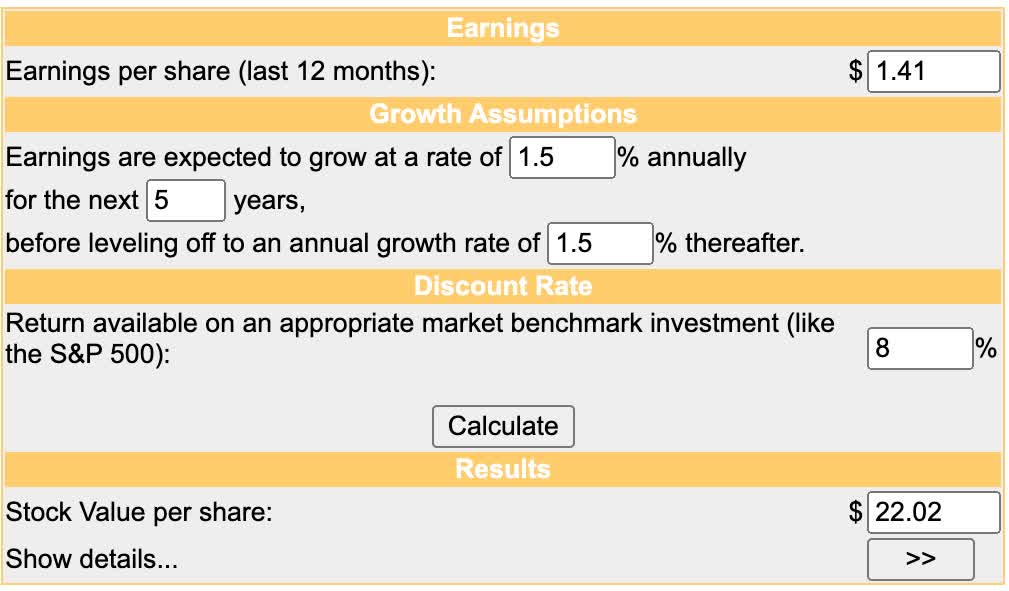

Wall Avenue at present charges the inventory a purchase with an average price target of $19.17 and a excessive of $22. Utilizing the Discounted Money Stream Technique I’ve the same worth goal at roughly $22. This offers traders double-digit upside from the present share worth. And seeing as charges are anticipated to say no someday within the close to future, Broadstone could also be a REIT deal with for some capital appreciation.

moneychimp

Dangers

Though BNL enjoys longer leases and has basically no debt to fret about paying or refinancing within the brief time period, as a result of their decrease publicity to investment-grade tenants, they’re extra inclined to financial downturns. On the finish of their This autumn their investment-grade exposure was simply 15.3%, a lot decrease than friends like Agree Realty and Realty Revenue.

Moreover, their occupancy score dropped barely quarter-over-quarter from 100% to 99.4%. If the economic system experiences a sudden downturn comparable to a recession, BNL’s occupancy might see a major drop, doubtless affecting the corporate’s financials. Once more, their present publicity is just not an finish all be all for myself, however some traders could favor a better publicity as a result of susceptibility.

Backside Line

Traders trying to bounce into the REIT sector in anticipation of rates of interest declining ought to think about Broadstone Web Lease. The REIT, regardless of their brief observe report, sports activities a diversified portfolio with a excessive occupancy of 99.4%. That is spectacular contemplating the difficult macro atmosphere and their decrease publicity to investment-rated tenants.

Moreover, the corporate’s stability sheet energy is spectacular contemplating they haven’t any substantial quantity of debt maturing for the subsequent two years. Their dividend protection additionally stays stable and appears sustainable for the foreseeable future. Most significantly, their upside potential might be probably the most engaging standards as they commerce under their present ebook worth. Though they’re thought of extra dangerous with a shorter observe report and lesser recognized tenants than some friends, I charge BNL a speculative purchase at present.