dem10

Brookfield Infrastructure (NYSE:BIP) (NYSE:BIPC) buyers have remained steadfast, regardless that BIP has underperformed the S&P 500 (SPX) (SPY) since my final replace in December 2023. New buyers in BIP are inspired to seek advice from my December article as a primer on Brookfield Infrastructure’s central thesis.

Brookfield Infrastructure’s high-quality portfolio capitalizes on regulated and long-term contracted investments to underpin its secure money flows. Nonetheless, I additionally inspired BIP buyers to think about ready for a pullback earlier than returning so as to add extra models. That warning has panned out, given its marked underperformance since then, even because the market notched its best Q1 efficiency since 2019.

Traders will doubtless be shocked by the market’s lukewarm reception about lifting BIP larger after its battering since bottoming out in October 2023. Brookfield Infrastructure posted a reasonably strong fourth-quarter earnings launch in early February 2024. Nonetheless, that hasn’t proved adequate as BIP continues to hover beneath the $32 resistance zone, failing to achieve sufficient shopping for momentum to realize a decisive breakout.

As a reminder, Brookfield Infrastructure has guided for a strong 12 months in 2024 because it appears to be like towards recycling $2B in capital. As well as, it nonetheless anticipates a distribution development of between 5% and 9% yearly. Its latest quarterly distribution per unit improve of 6% has supplied extra confidence to buyers. Moreover, with an FFO payout ratio of 66%, it is properly inside Brookfield Infrastructure’s long-term goal of 60% to 70%.

BIP’s focus on the three Ds (digitalization, deglobalization, and decarbonization) has continued to underpin its strategic capital allocation. Brookfield Infrastructure noticed sharp positive factors in FFO in its utilities (up 19% YoY) and transport (12% YoY) segments. These two segments should be rigorously watched as they’re the primary driving forces of BIP’s FFO accretion. Accordingly, these segments have benefited from indexation and quantity development, underscoring the steadiness in its FFO development trajectory. Brookfield Infrastructure’s midstream phase was impacted by the “normalization of market-sensitive revenues.” Nonetheless, that should not be shocking because the underlying weak point within the power markets was broad-based in 2023.

Brookfield Infrastructure is predicted to accentuate its footprint in its growing information phase. The secular development in 5G and generative AI has spurred larger demand for these information infrastructure belongings. Brookfield Infrastructure’s resolution to accumulate American Tower’s (AMT) ATC India belongings underscores BIP’s confidence in its international growth efforts in telco. Because of this, I consider Brookfield Infrastructure’s information phase continues to be within the early innings of its growth. Furthermore, Brookfield Infrastructure administration telegraphed its emphasis on constructing this phase, because the “data platform is expected to grow the fastest.” Consequently, unitholders ought to anticipate “the largest amount of new capital will be deployed towards the data platform” as Brookfield Infrastructure prepares to seize the quickly increasing alternatives.

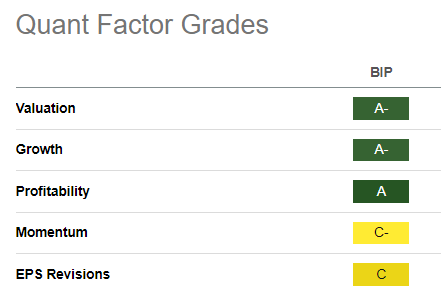

BIP Quant Grades (Searching for Alpha)

BIP’s engaging “A-” valuation grade suggests the market hasn’t absolutely appreciated Brookfield Infrastructure’s burgeoning drivers. Coupled with an “A” development grade, it appears to indicate a discernible valuation dislocation relative to BIP’s sector friends.

Nonetheless, I assessed that BIP administration appropriately recognized a few of the most important headwinds hampering its re-rating potential in 2023. Accordingly, Brookfield Infrastructure administration identified that “the price of Brookfield Infrastructure securities was affected by macroeconomic factors” in 2023. Given BIP’s deal with revenue buyers, unfavourable sentiments affected “yield-oriented companies like Brookfield Infrastructure.” Because of this, it is paramount for buyers to think about the prevailing Treasury yields relative to BIP’s ahead distribution yields to evaluate their relative enchantment.

The excellent news is that the Fed seems increasingly likely to decrease rates of interest in 2024. Fed Chair Jerome Powell did not “rock the boat” in a latest commentary. Because of this, BIP unitholders needs to be assured that final 12 months’s hammering doubtless marked BIP’s long-term backside.

BIP is valued at a ahead distribution yield of 5.5%, above its 10Y common of 4.8%. Nonetheless, the 2Y (US2Y) final printed at 4.37%, which may dampen its near-term enchantment, contemplating an applicable unfold to replicate dangers.

My evaluation suggests the $32 resistance zone will doubtless be a big hindrance in opposition to an extra re-rating for BIP within the close to time period. Nonetheless, as we transfer nearer to the Fed’s supposed price cuts, shopping for momentum ought to enhance because the market positive factors extra readability over the Fed’s dovish stance. With BIP’s strong execution and valuation bifurcation, I view the latest pullback as a gorgeous alternative for BIP unitholders so as to add extra publicity.

Score: Improve to Purchase.

Vital be aware: Traders are reminded to do their due diligence and never depend on the data supplied as monetary recommendation. Think about this text as supplementing your required analysis. Please all the time apply impartial pondering. Word that the ranking is just not supposed to time a particular entry/exit on the level of writing except in any other case specified.

I Need To Hear From You

Have constructive commentary to enhance our thesis? Noticed a vital hole in our view? Noticed one thing necessary that we did not? Agree or disagree? Remark beneath with the purpose of serving to everybody locally to be taught higher!