wdstock

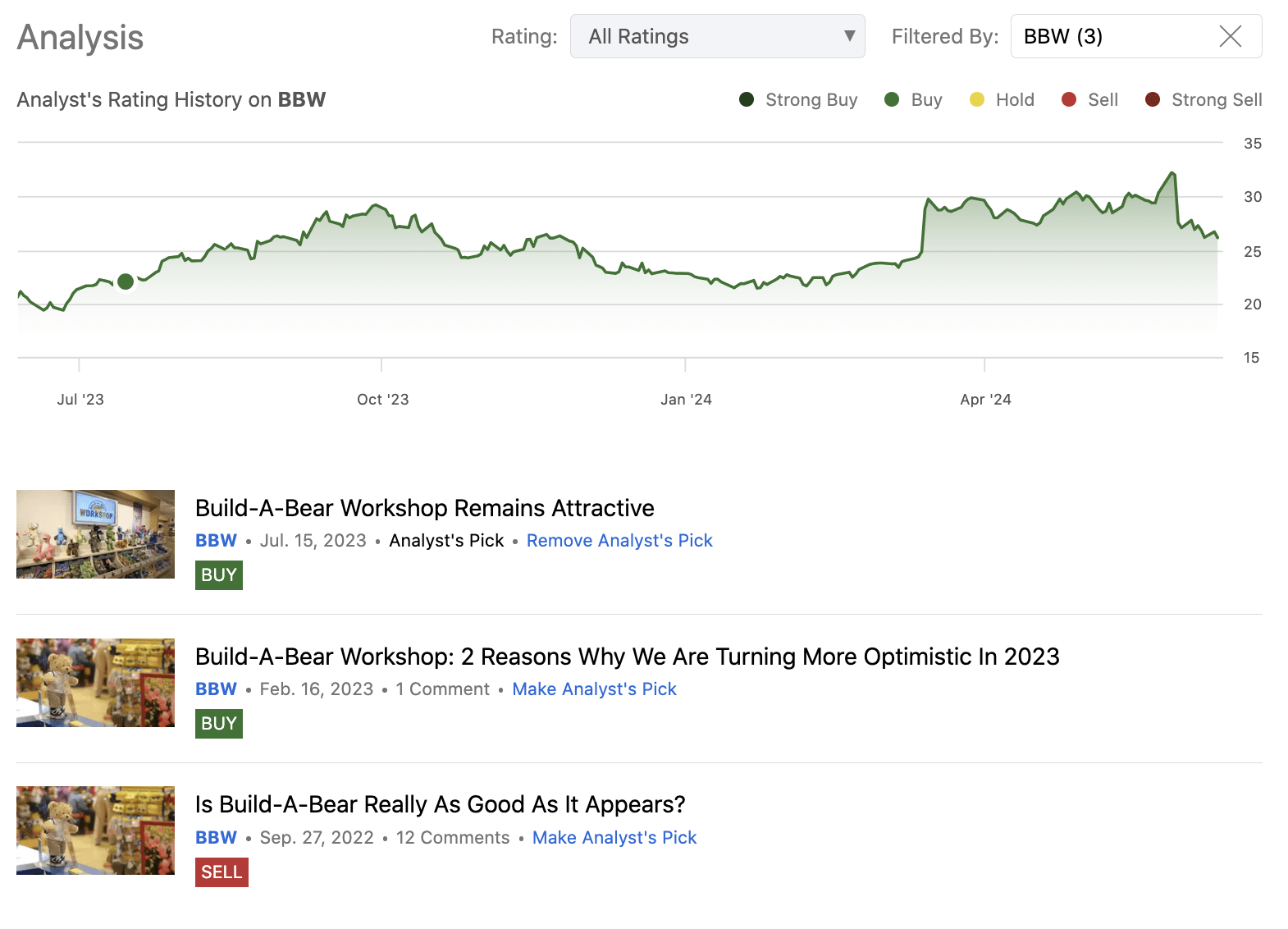

Build-A-Bear Workshop, Inc. (NYSE:BBW) operates as a multi-channel retailer of plush animals and related products in the United States and internationally. We first wrote about BBW in September 2022, when we assigned a bearish rating to the firm, primarily due to the unstable macroeconomic environment as well as the firm’s capital allocation decisions. Shortly after our writing, we were proven wrong. Stock price has substantially increased and the firm’s financial performance has remained strong. In February 2023, we have upgraded BBW to a “buy” and we reiterated this positive view in July 2023.

Analysis history (Author)

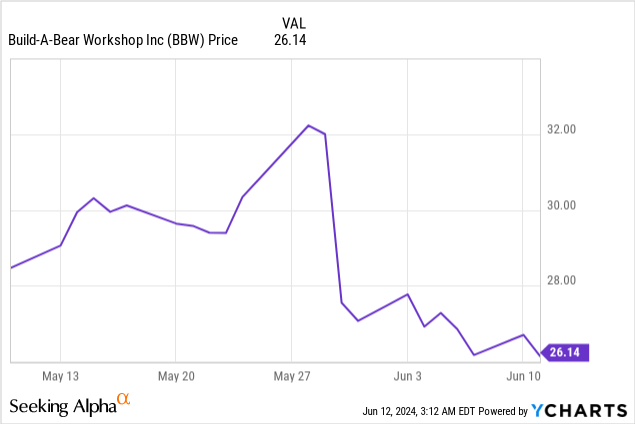

The aim of our article today is to highlight the key points from the firm’s latest quarterly results, which we were released on the 30th of May. We will discuss whether initiating a new position or adding to an existing one at the current price levels could be attractive or not and how the current macroeconomic environment may impact this decision.

Quarterly results

BBW has reported quarterly earnings results on the 30th of May, missing both top- and bottom line estimates. As a result, the stock price has fallen significantly.

To understand whether this price drop is justified or not, we have to take a closer look at the results.

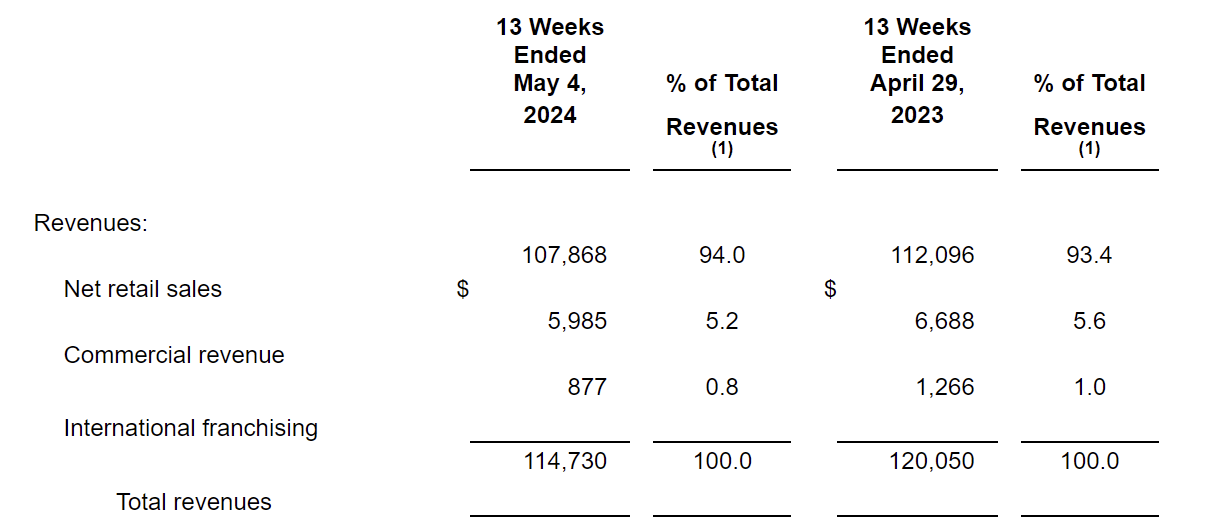

Revenue

Revenues have declined 4.4% year-over-year, totaling in $114.7 million. Net retail sales have shown an only 3.8%, while consolidated e-commerce demand has fallen at a significantly higher rate – at 11.3% – year-over-year. Commercial and international franchise revenues combined have also been declining at a double digit rate – at 13.7% – compared to the same period in the prior year. These segments, however, contributes only $6.9 million to the total revenues, therefore its impact is not so severe.

Revenues (BBW)

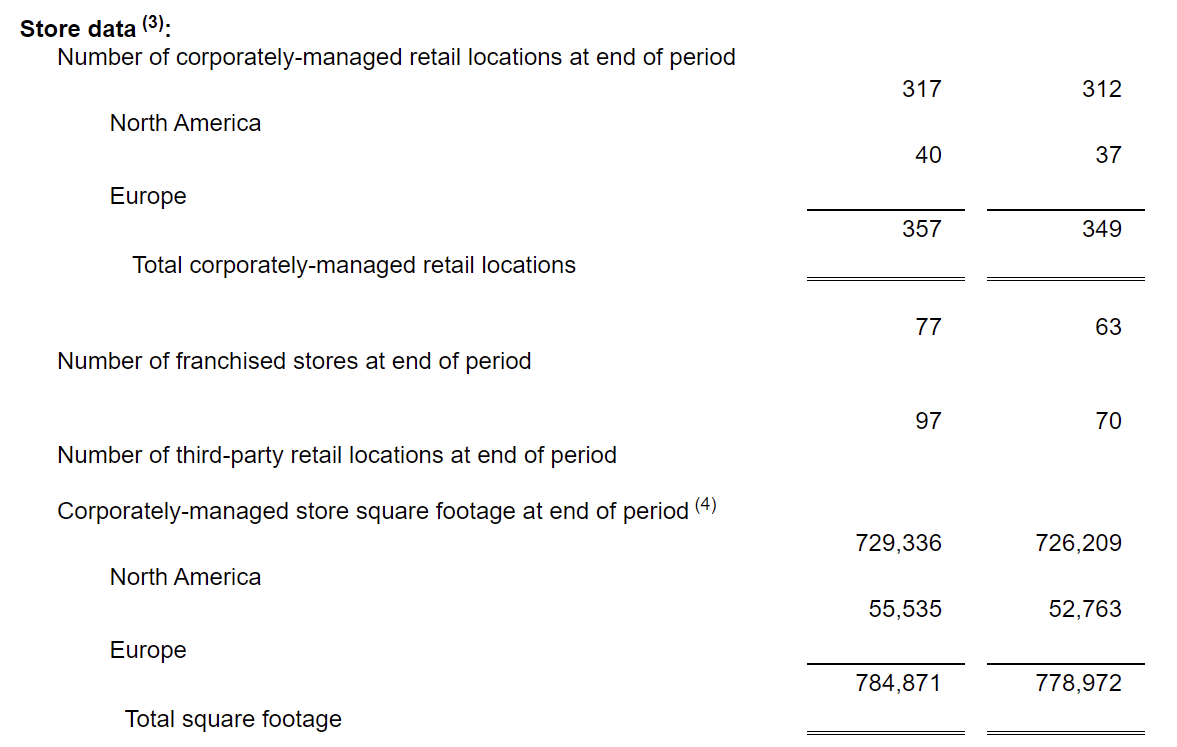

These results become even slightly worse, when we take a look at the store count. During this period, store count and total square footage have even increased, but it has not led to higher revenues.

Store count (BBW)

So how do we interpret these figures?

In our opinion, these results show that the demand for BBW’s products is weakening and people are becoming more reluctant to spend on these discretionary products.

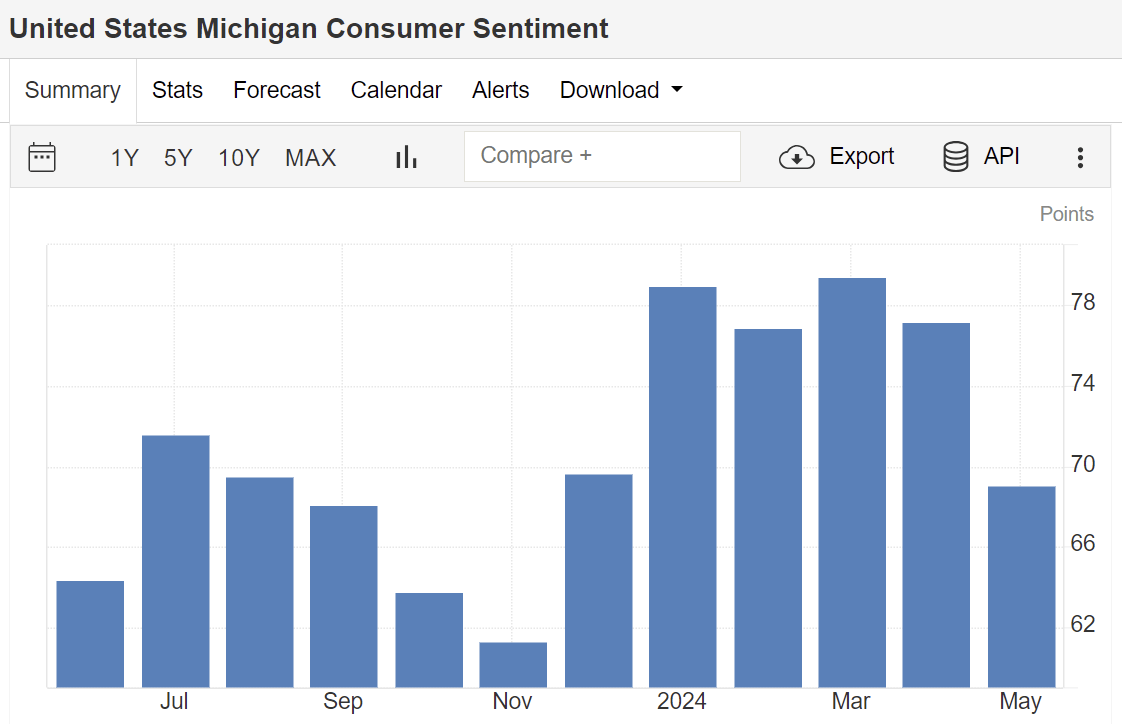

If we take a look at the consumer confidence in the United States, we can see that it has been gradually weakening over the past months. This could be a reason, why people are becoming more cautious with spending. In general, we believe that the driver of the company’s poor financial performance is mainly the macroeconomic environment, and not necessarily microeconomic factors.

U.S. Consumer Confidence (tradingeconomics.com)

Looking forward, we expect the weakness to continue for the next months. The actions of the Fed and the elections in the United States in the near future could have significant impacts on the macroeconomic environment, however we do not believe that it would fuel an immediate improvement of the financial figures. On the other hand, the firm’s management is somewhat more optimistic. They expect the revenue for the full year to grow at a low- to mid-single digit rate. Additionally, at least 50 new locations are expected to be added to BBW’s existing store count.

Bottom line

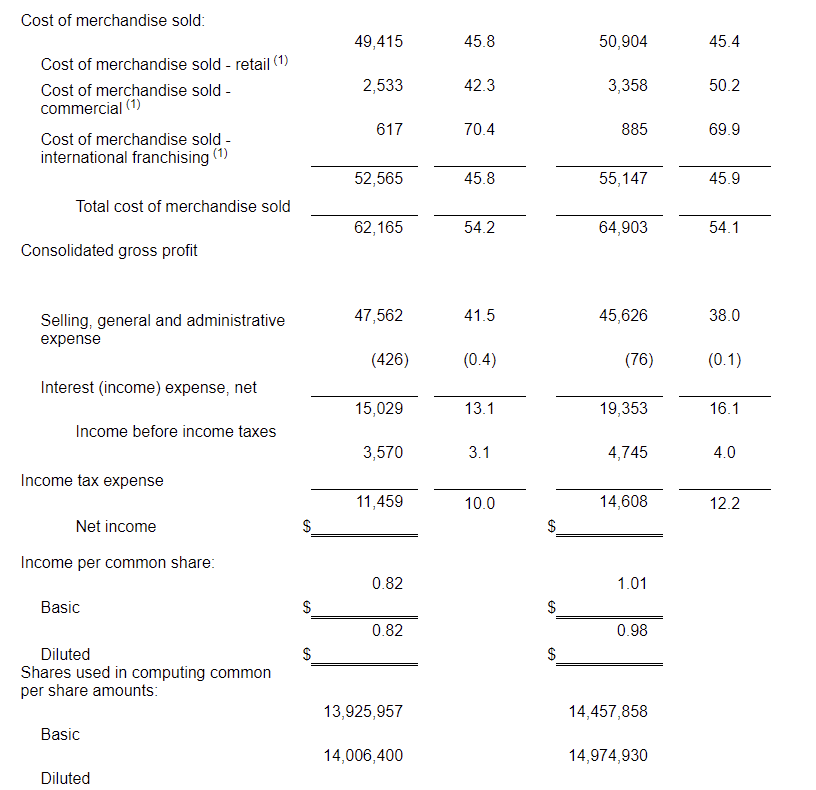

When we look at the bottom-line results, we can see a significant deterioration compared to the prior year. Diluted EPS have fallen to $0.82 from $0.98, which is a more than 16% decline. One of the key drivers of this deterioration has been the increase in SG&A expenses compared to the prior year. This has led to a lower operating income and has cascaded down all the way to the bottom of the income statement. SG&A expenses have increased mainly due to higher wages, inflationary pressures and unfavorable expense timing.

Income statement (BBW)

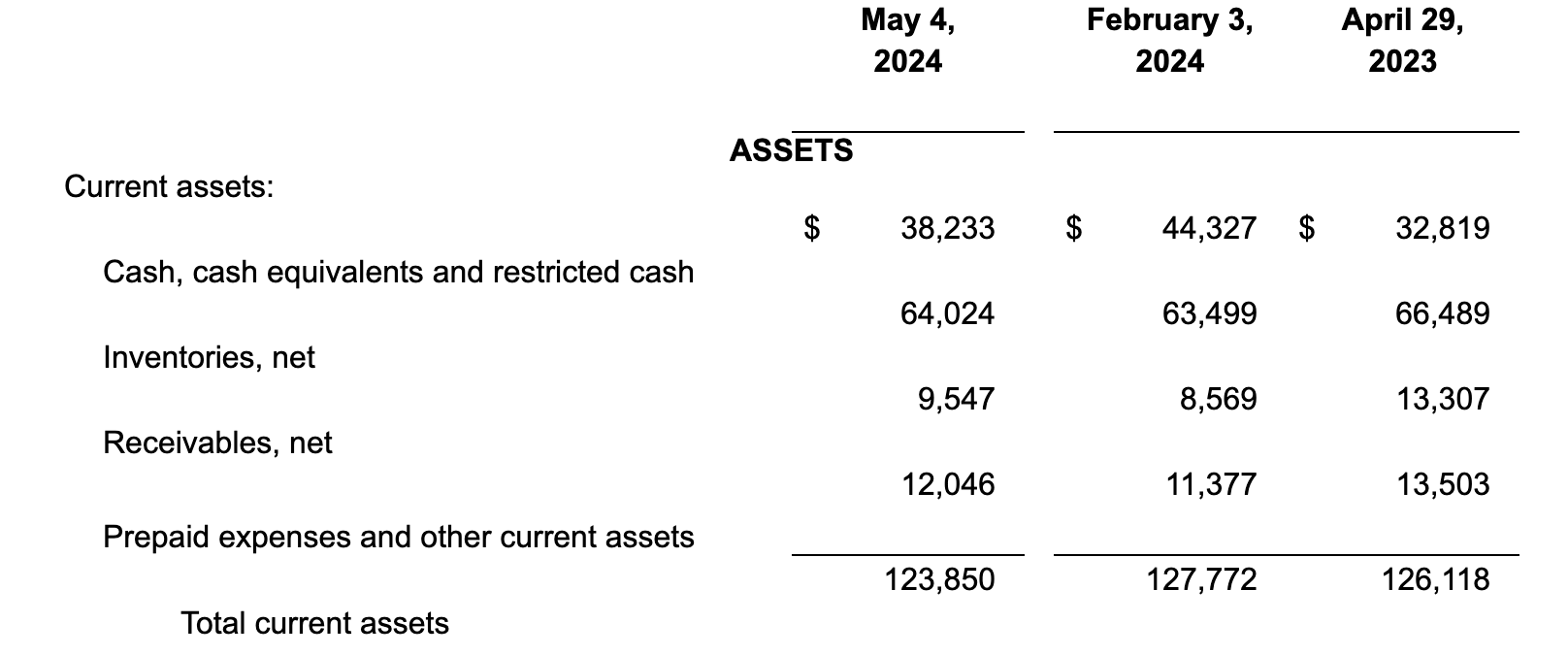

On the positive side we have to mention that with declining sales and earnings, inventories and accounts receivable have also decreased. In our opinion, this indicates that despite the lower demand, BBW is not likely to have significant problems with excess or obsolete inventories, which could lead to excessive discounting and deteriorating profitability. The lower accounts receivable also shows that the firm is not trying to pull demand forward from future periods, to cover up the current weakness in demand.

Current assets (BBW)

Looking forward, the firm expects pre-tax income to grow at the same, low- to mid-single digit, rate, as revenues.

Return to shareholders

BBW utilizes both quarterly cash dividends as well as share buybacks to return value to its shareholders. The majority of the return in the past quarter has been the share buybacks. The firm has spent more than $9 million to buy its shares back, while it has only spent $2.9 million on dividends. These payments are more than covered by the company’s cash flow from operation, even when we account for the CAPEX spendings. We actually like that BBW is spending more on buybacks than on dividends as this form of return may be more advantageous from a tax perspective in some jurisdictions, and it also gives more flexibility to the firm.

Previously, we have critiqued the firm of spending too much on dividends and share buybacks and maybe not enough on growth. At that point, we have been proven wrong because the business has been growing actually at a quite high rate, despite this allocation strategy.

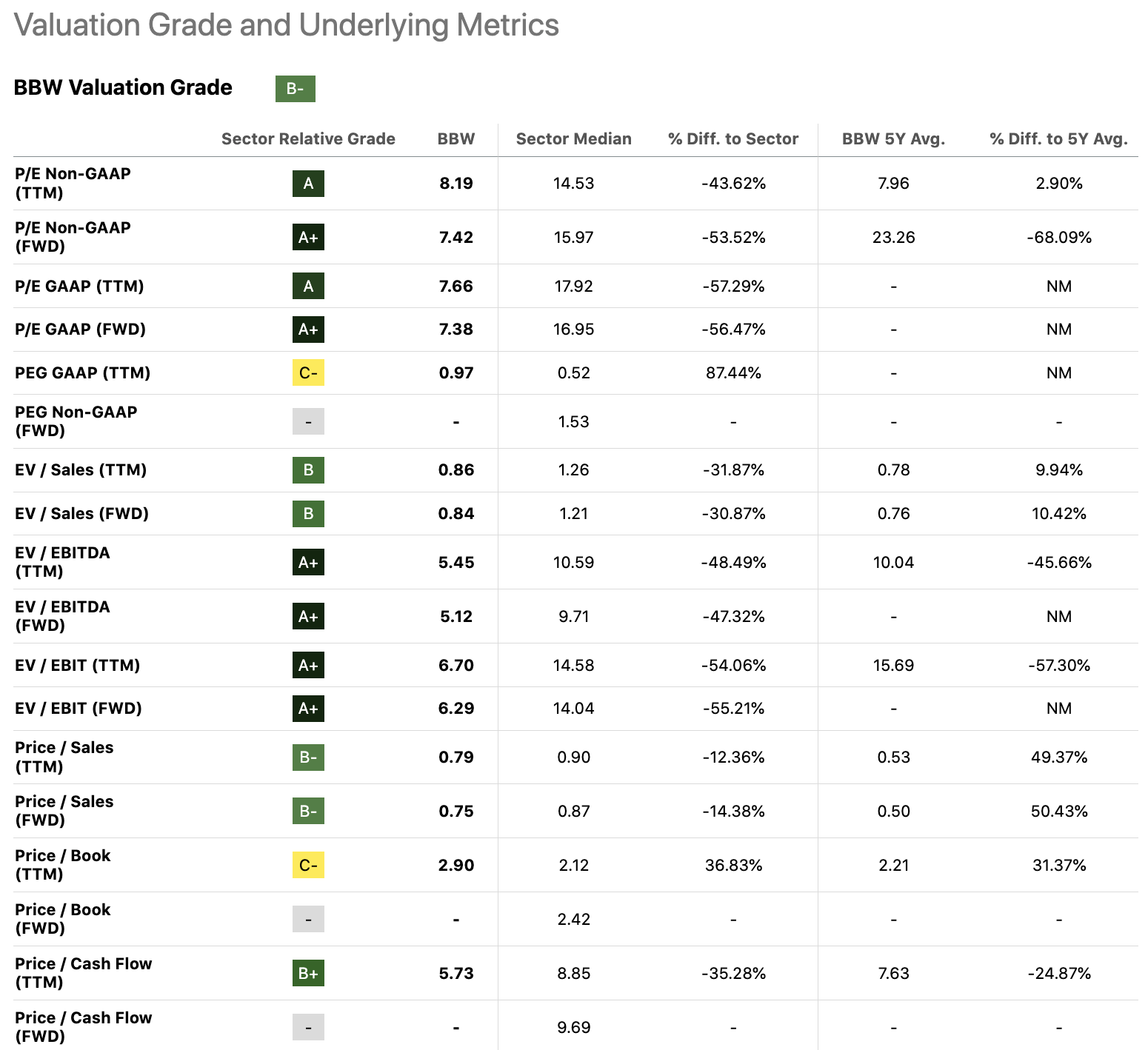

Valuation

To assess whether BBW could be an attractive buy at the current price level, we are going to take a look at a set of traditional price multiples.

Valuation (SA)

While BBW appears to be trading at a significant discount compared to the consumer discretionary sector median, this may be somewhat misleading. The consumer discretionary sector contains many companies that have significantly different business models/ products from that of BBW. If we compare the current financial metrics with BBW’s past metrics, the valuation does not appear to be that appealing anymore.

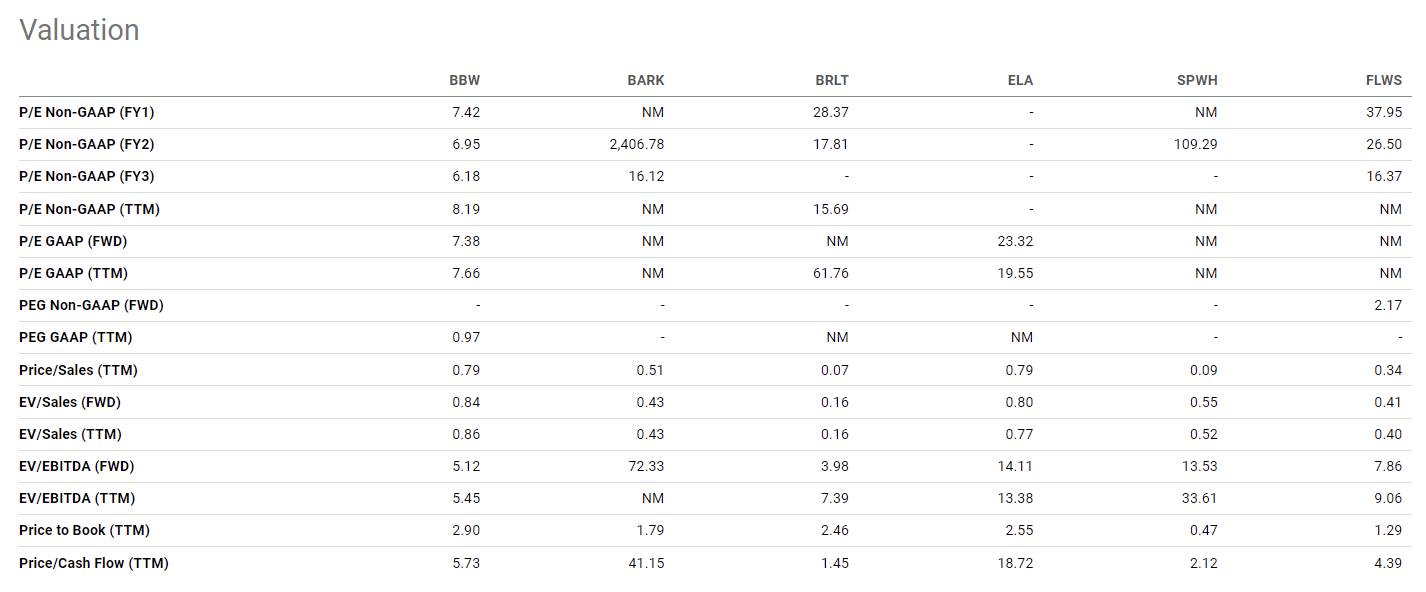

If we narrow down the peer group to a few companies in the other specialty retail industry, we can see that BBW is not trading at a significant discount compared to them. While this indicates that BBW’s stock is not likely to be significantly undervalued, we have to check a few other metrics to understand whether the current price could still be attractive or not.

Valuation (SA)

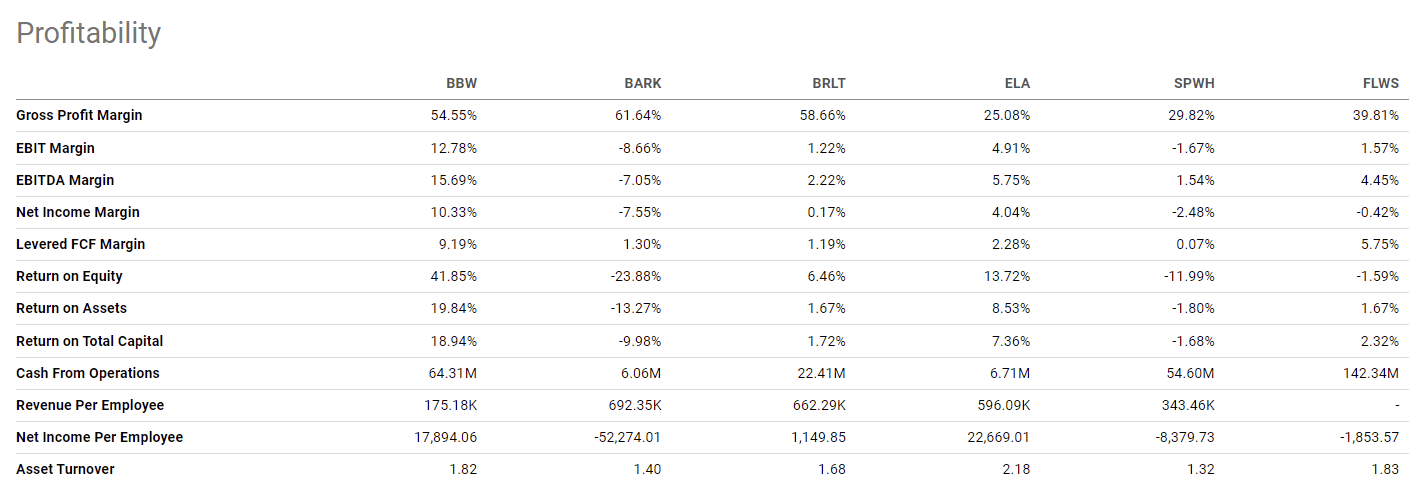

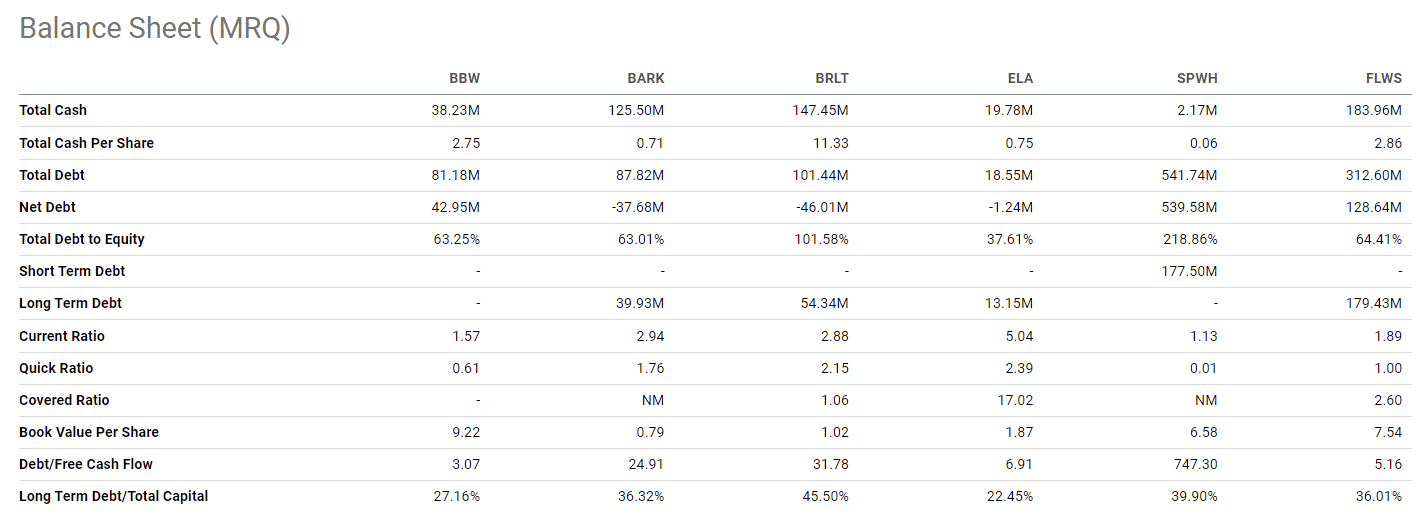

Normally, we like to compare profitability and liquidity metrics to get a better idea of the quality of the business. Stronger liquidity and higher margins normally justify higher multiples. The following tables show that BBW is definitely stronger than the other firms from a profitability perspective, but they are less robust from a liquidity point of view, despite the current ratio being well above one.

Profitability (SA)

Balance sheet (SA)

For these reasons, however, we believe that BBW’s stock is currently fairly valued and we do not expect the company to outperform the broader market in the coming months.

Conclusions

BBW has missed both top- and bottom line estimates in the previous quarter, leading to a significant stock price decline.

Revenues, operating income and net income have all declined, despite the increasing store count.

From a valuation point of view, despite the low multiples, BBW does not appear to be significantly undervalued.

Due to the deteriorating financial performance and the unstable macroeconomic environment, we are becoming somewhat more cautious on the firm and therefore we downgrade from “buy” to “hold”.