ArtistGNDphotography

Fast be aware earlier than studying: I wrote on Builders FirstSource (NYSE:BLDR) again in March 2022 in my article “Builders FirstSource: Management Guidance Suggests 46% Upside.” Since then, the inventory has risen 154% (outperforming the S&P 500 by ~134%). It’d make sense to learn that first after which bounce into this piece to provide a full overview as to my ideas just a few years again vs how I am fascinated about the corporate now.

Funding Thesis/Enterprise Overview

Builders FirstSource manufactures and provides constructing supplies to properties round the USA. The corporate additionally supplies skilled set up providers to owners seeking to do remodels, additions, or construct new properties. To place it extra broadly, the corporate helps house building tasks.

And that is the place the chance is, in my opinion. The USA wants extra house building tasks to treatment the scarcity of 4 million properties in the USA (in line with The Hill). Builders FirstSource is a direct beneficiary of that.

Moreover, the corporate has already benefited from the current pullback in mortgage charges, with single household house begins surging in current months. An accommodative Fed this yr may also result in decrease rates of interest which can in flip create extra housing exercise – with BLDR appearing as the principle beneficiary.

On account of the above elements talked about, I forecast robust Income, EBITDA, and Free Money Move progress over the following 5 years, and my DCF mannequin presently exhibits the inventory has 22% upside from present ranges.

Income Development Drivers

As I discussed in my opening paragraph, the US is presently quick 4 million properties, and with the current inflow of immigration, this quantity is probably going set to extend. Due to this fact, put merely, we have to construct extra properties. And that’s the place Builders FirstSource advantages. The corporate builds properties, does add-ons, and customarily helps building tasks.

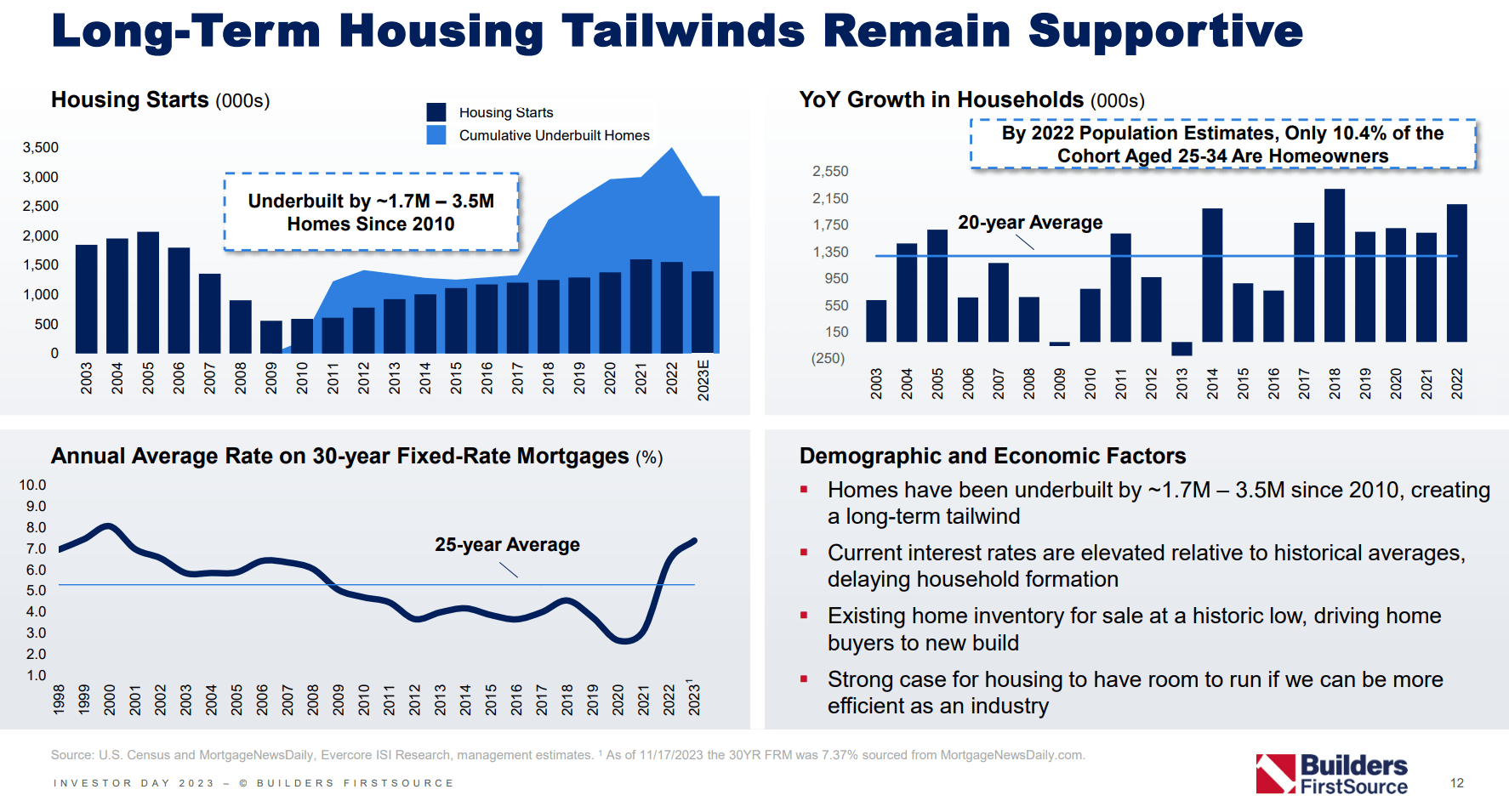

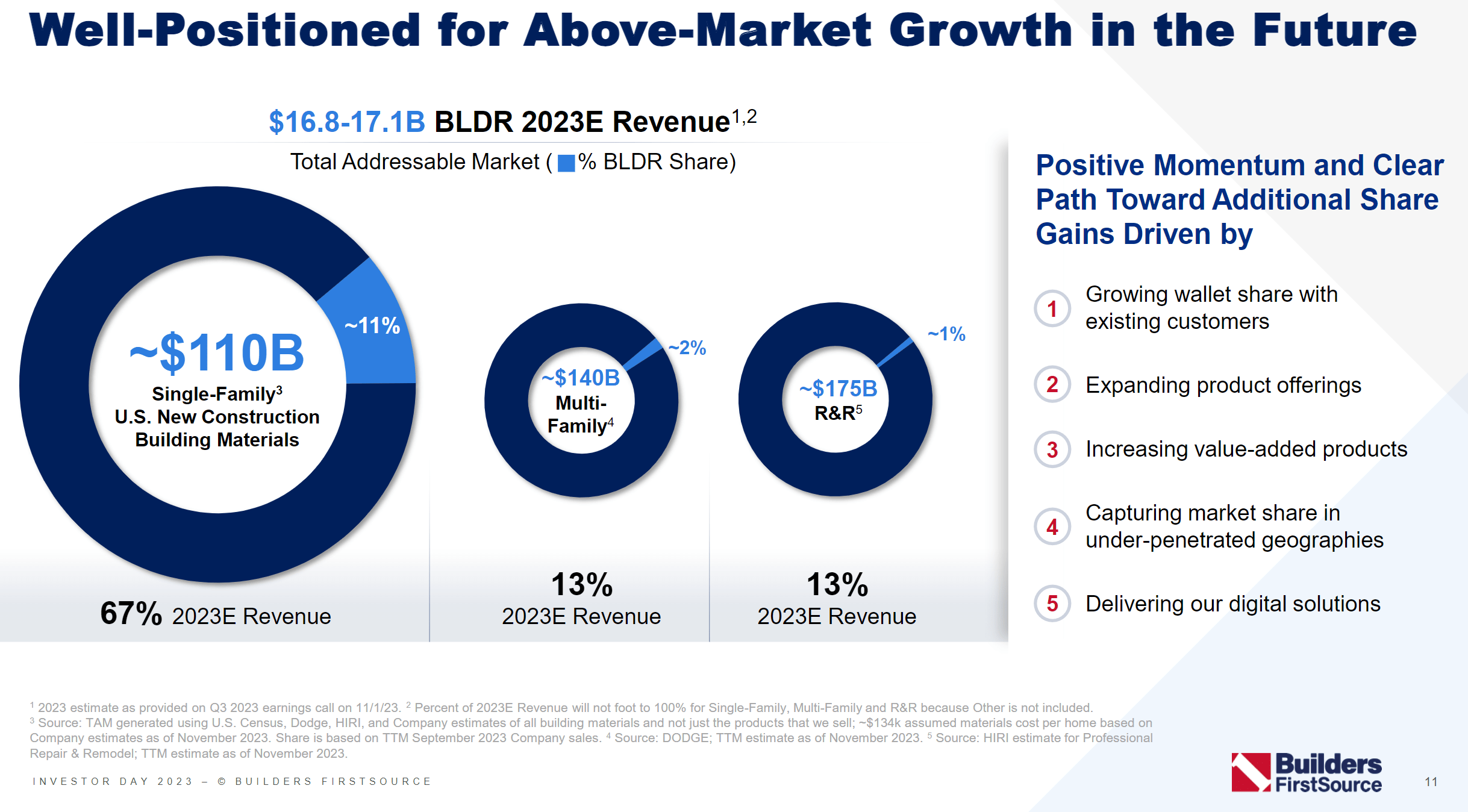

I believe this slide in Builders FirstSource’s Investor Day Presentation does an incredible job of illustrating the structural demand I’m speaking about.

Lengthy-term housing tailwinds supportive for BLDR (10K Filings, The Black Sheep )

Whereas “The Hill” studies the USA is 4 million properties quick, and Builders FirstSource studies 1.7-3.5 million properties quick, the purpose nonetheless stands – the USA wants extra properties.

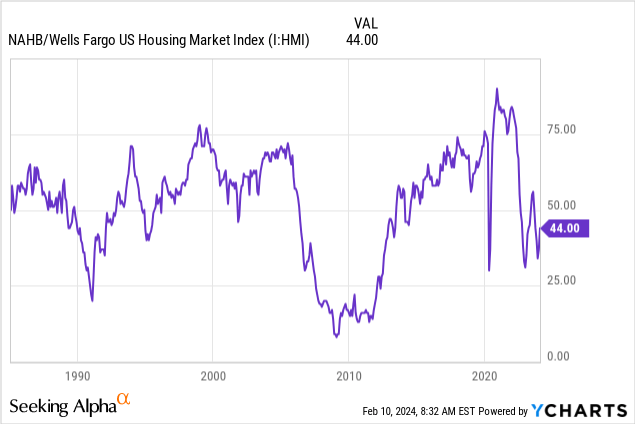

One other tailwind that I foresee this yr is an accommodative Fed. Rates of interest surged over the previous few years, curbing housing exercise in the USA.

Check out the NAHB US Housing Market Index indicator above, which is nicely beneath its highs of ~80 in mid-2020.

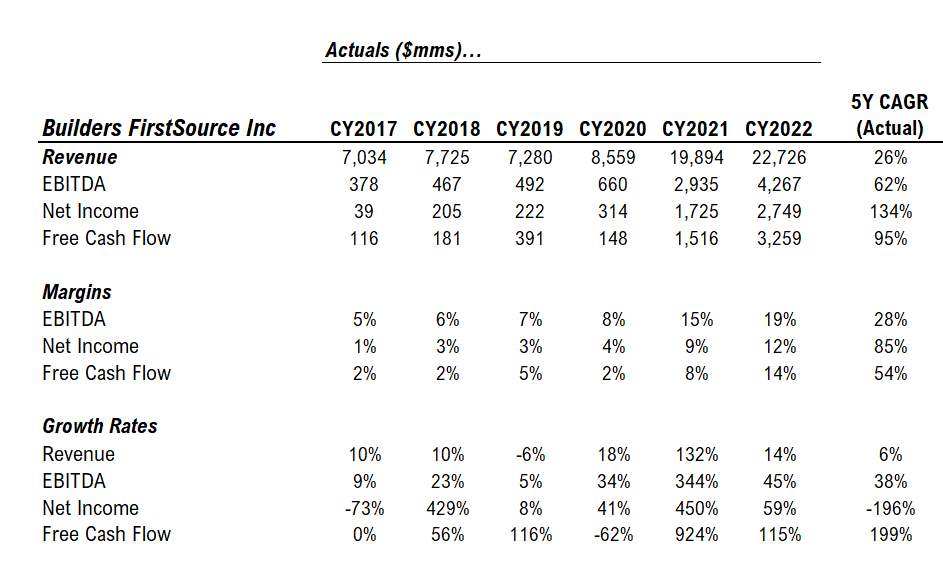

Nonetheless, Builders FirstSource was in a position to develop its revenues and income markedly.

10K Filings, The Black Sheep

The 5Y CAGR of the next line objects are beneath:

- Income: 26%

- EBITDA: 62%

- Internet Earnings: 134%

- Free Money Move: 95%

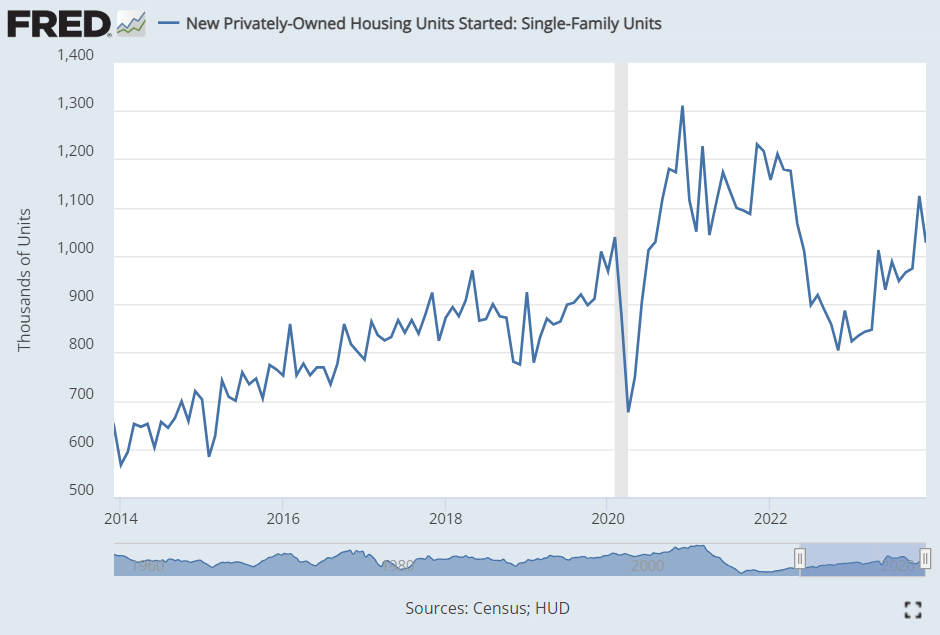

Housing begins are additionally beginning to choose up for single-family models. Check out the chart beneath.

FRED

Single-family properties is one in every of Builders FirstSource’s largest income turbines. Check out the slide beneath from the corporate’s investor presentation.

Builders FirstSource Investor Day Presentation

The corporate says it’s well-positioned for above-market progress and seeks to seize extra market share throughout the single-family US new building constructing supplies business.

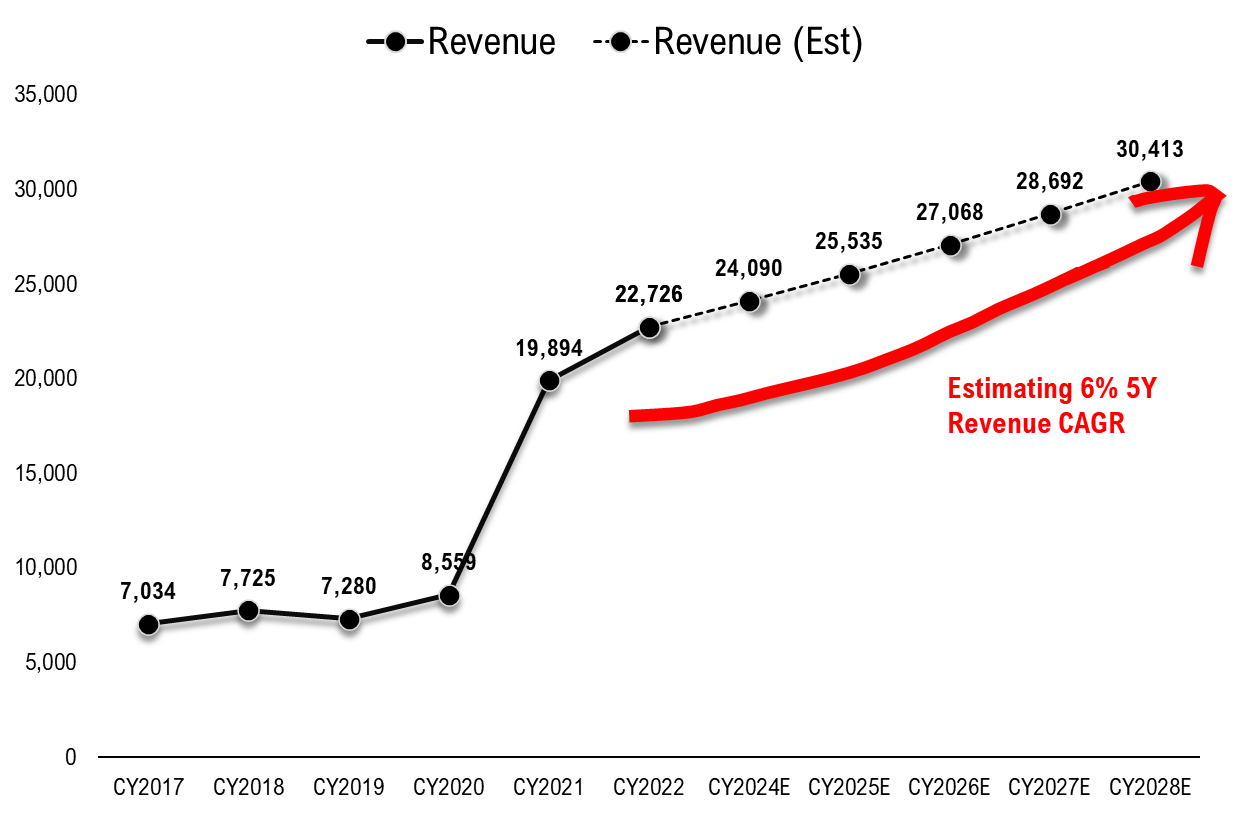

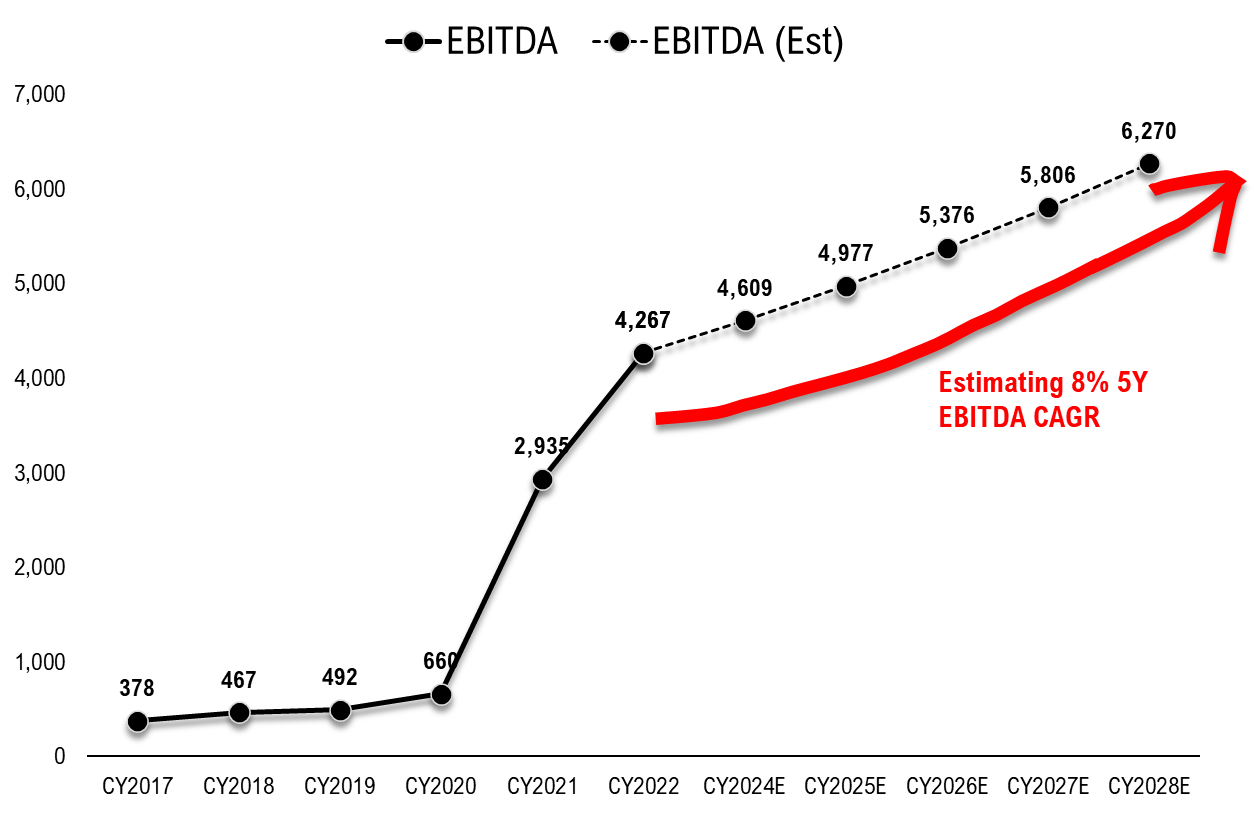

Given the income progress drivers I discussed above, these are my income and EBITDA, income, and free money circulate forecasts over the following 5 years.

10K Filings, The Black Sheep

I anticipate income climbs at a 6% CAGR over the following 5 years attributable to robust tailwinds in single-family unit building, falling mortgage charges spurring housing demand, and a extra accommodative Fed which can finally result in extra exercise within the housing market.

10K Filings, The Black Sheep

I see EBITDA rising at an 8% clip over the following 5 years as a result of firm’s resilient margins (which I’ll define later on this article).

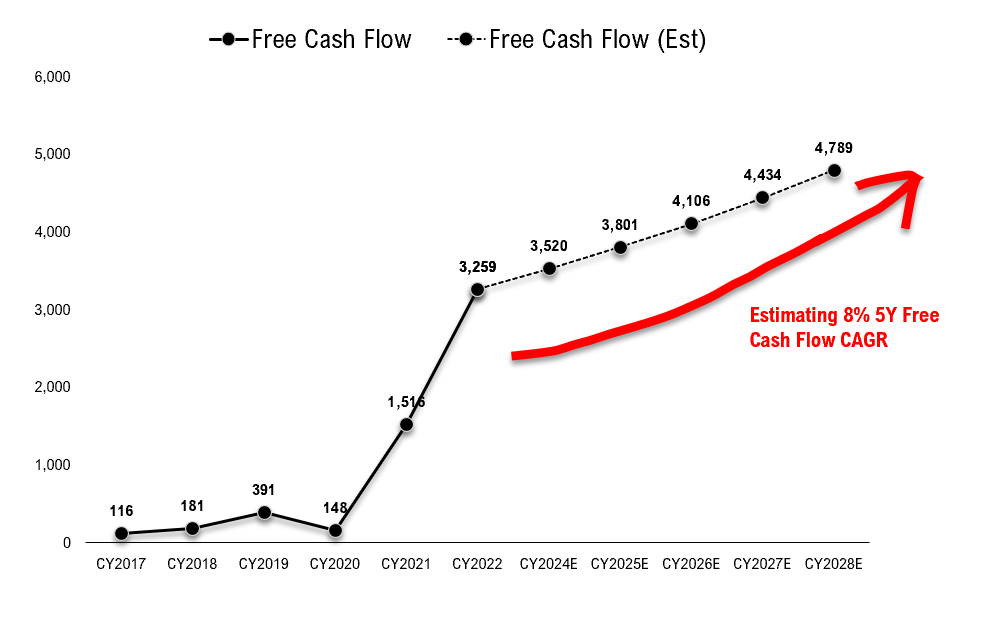

The Black Sheep Free Money Move Development Forecast (10K Filings, The Black Sheep )

And this may lend itself, in my view, to robust Free Money circulate progress over the following 5 years (I see rising at 8% 5Y CAGR).

Profitability

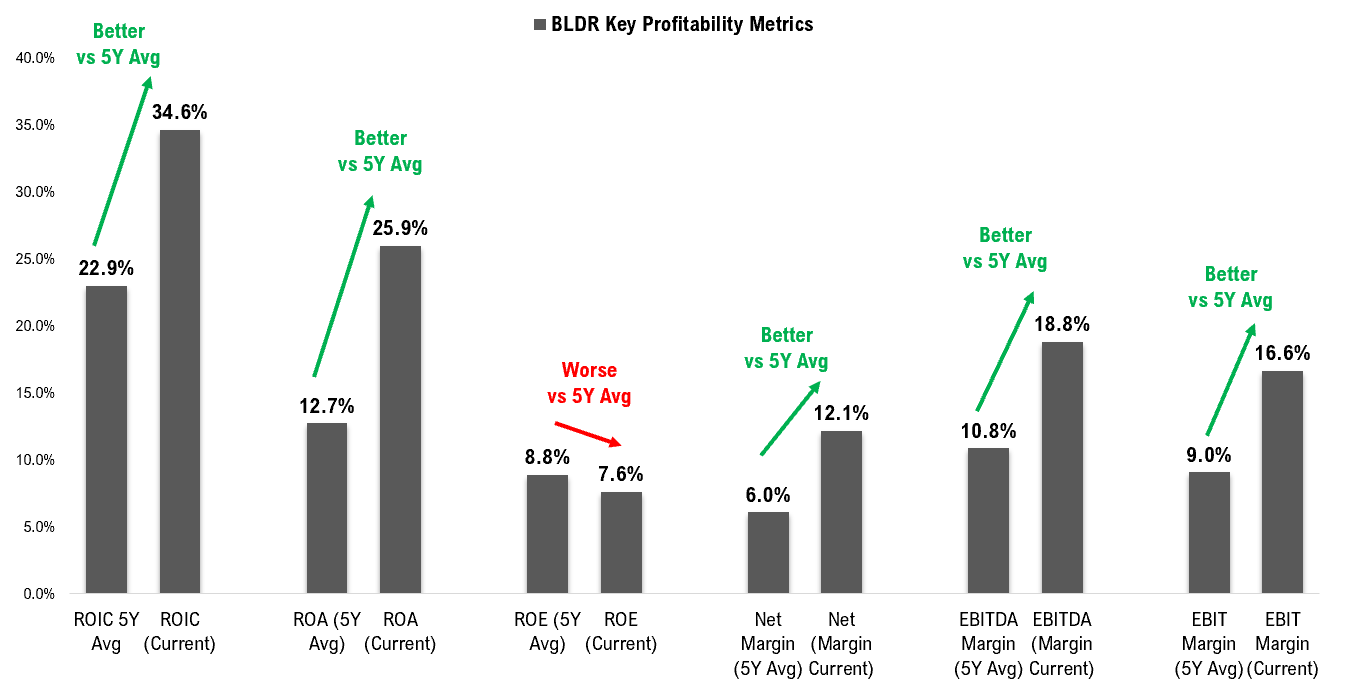

When it comes to profitability, 5 out of 6 of the important thing profitability metrics I monitor are presently above their 5-12 months averages, respectively. The 6 metrics are ROIC, ROA, ROE, Internet Margin, EBITDA Margin, and EBIT Margin.

10K Filings, The Black Sheep

Of those 6 key metrics, the one that has gotten worse is ROE. The corporate has been in a position to enhance on the opposite 5 metrics which exhibits its means to generate income even in unsure financial occasions (Covid-19 + current inflationary interval).

One merchandise I need to spotlight is Internet Margin, which has doubled from 6.0% (5Y Avg) all the way in which to 12.1% presently. That’s explosive progress, and I see no motive why the corporate shouldn’t be in a position to proceed to keep up these margins, particularly as inflation continues to fall and enter supplies develop into cheaper.

Valuation/Peer Evaluation

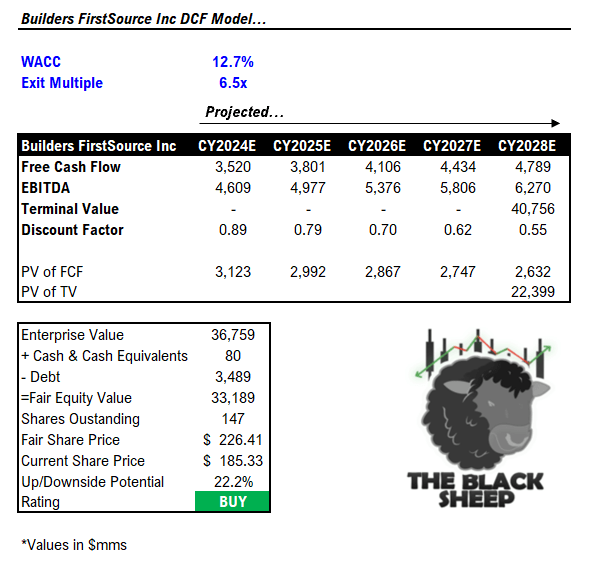

When it comes to valuation, my DCF mannequin might be discovered beneath.

10K Filings, The Black Sheep

I assume robust free money circulate progress, EBITDA progress, a WACC of 12.7%, and a conservative exit a number of on fifth yr EBITDA of 6.5 (beneath the median EV/EBITDA of its peer group).

After correctly discounting the free money flows, terminal worth, and normalizing for web debt, I come to a justifiable share worth of $226.41. That is 22.2% larger than the present share worth of $185.33.

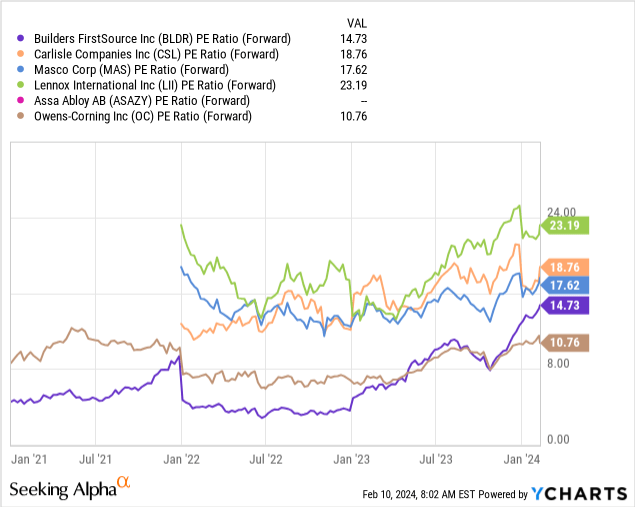

And given this robust anticipated progress, one would assume the inventory is pricey.

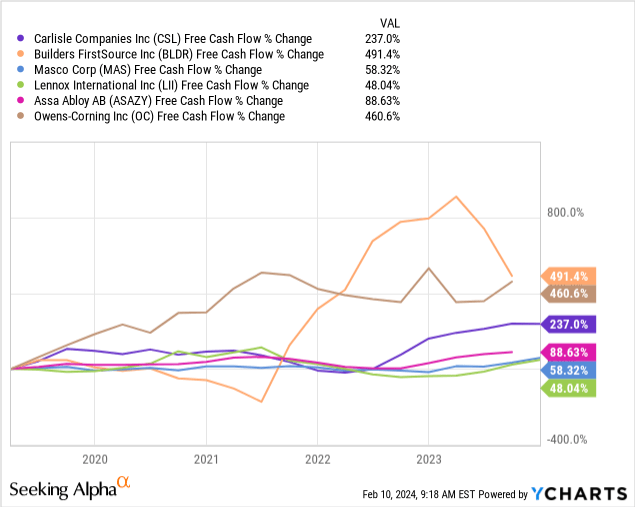

That isn’t the case. Have a look beneath at BLDR vs its peer group. The corporate is buying and selling on the lower-end of its peer group when it comes to NTM PE ratio, regardless of its potential to capitalize on the secular tailwinds within the housing market.

And vs its friends, the corporate is main in free money circulate progress (491% in previous 5Y).

This robust progress and low valuation vs its friends are two major the reason why I’m a proponent of BLDR.

Steadiness Sheet

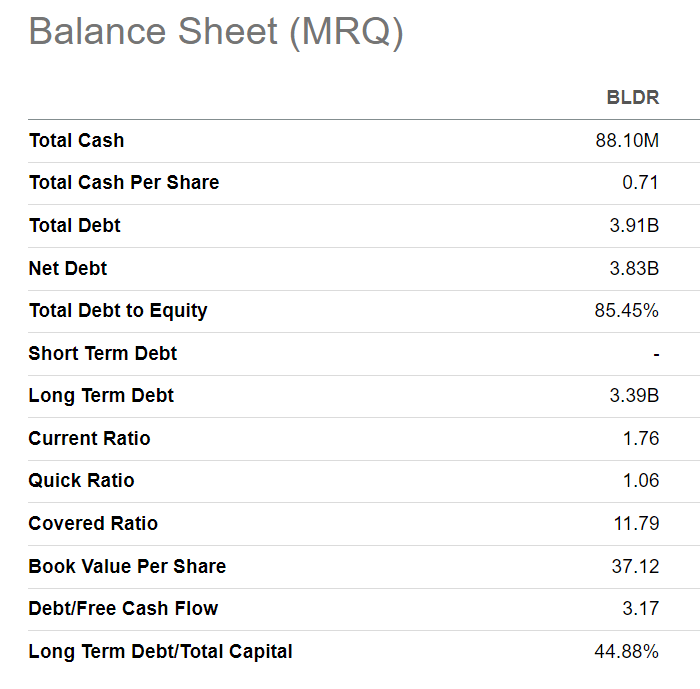

BLDR has a robust steadiness sheet. Under I’ve included among the firm’s key steadiness sheet objects.

Steadiness Sheet Objects for BLDR (In search of Alpha )

The principle strains I need to spotlight are the short-term debt, present ratio, and fast ratio.

- Quick-term debt: The corporate’s short-term debt is 0, that means all of its debt is bundled into long-term debt (simpler to handle for a corporation like BLDR whose income is particularly cyclical, and a constructive to me).

- Present ratio: >1 is at all times good to see, and BLDR has a present ratio of 1.76

- Fast ratio: Additionally >1, which is a constructive.

Largest Dangers

The most important threat that I see for BLDR can be a Fed that’s “higher for longer.” This could alter the trajectory of mortgage charges again larger and doubtlessly decelerate enterprise for BLDR. Moreover, a threat to my thesis can be that the financial system falls right into a recession, however given inflation is slowing quickly and actual GDP got here in stronger than anticipated in This fall, I don’t see a recession on the horizon.

Conclusion

Total, I see BLDR as an incredible long-term play because it advantages from the structural housing scarcity in the USA. The corporate is well-capitalized, is a free money circulate machine, and continues to execute regardless of the underlying macro backdrop. It’s also not “expensive” vs its friends from a relative valuation perspective. For these causes, I like to recommend the inventory as a robust purchase and see 22% upside potential for the inventory over the following yr given my DCF mannequin that’s based mostly on robust income, free money circulate, and EBITDA progress.