Deepak Sethi/iStock by way of Getty Pictures

Introduction

I’ve at all times preferred Buyers Title Firm (NASDAQ:ITIC) as I think about property title insurance coverage to be a low-risk business. That is not only a private impression: the full quantity of provisions for claims is often only a fraction of the full quantity of the premium revenue. However after all this additionally means ITIC’s efficiency is carefully tied to the housing market and the quantity of transactions as a property proprietor and/or mortgagee solely have to insure the title upon a transaction. This additionally implies that when mortgages charges are excessive and the full quantity of transactions is low, ITIC’s efficiency can be struggling.

2023 can be a comparatively weak 12 months for ITIC

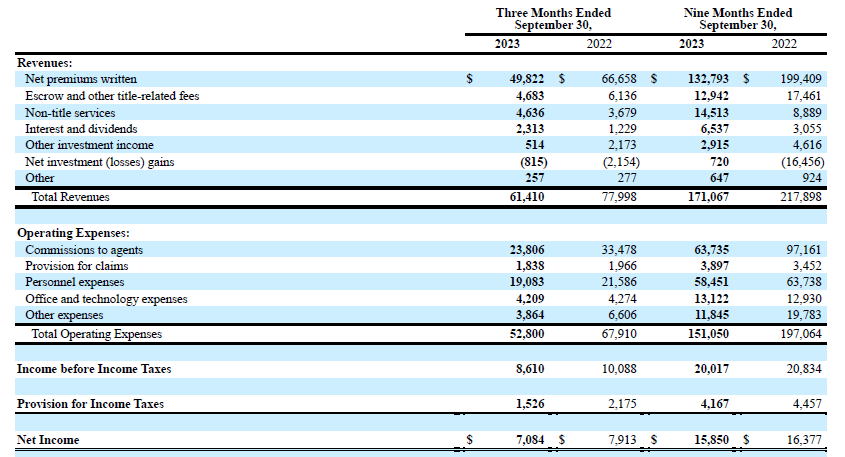

Wanting on the Q3 and 9M 2023 outcomes, the influence of the decrease transaction quantity on the true property markets is very clear. The corporate reported a 25% lower amount of net premiums written, however fortuitously this additionally means the full fee payable to brokers got here in decrease as nicely. The revenue assertion beneath shows a total revenue of $61.4M of which the bulk is clearly generated by the title insurance coverage premiums. That being stated, ITIC is slowly benefiting from the rising rates of interest as its funding portfolio is doing fairly nicely. The overall quantity of curiosity and dividends has doubled in comparison with the identical quarter of final 12 months and that positively helped to mitigate the influence of the decrease transaction volumes.

ITIC Investor Relations

The overall quantity of working bills did lower by simply over $15M, primarily because of a decrease fee expense and a barely decrease personnel expense along with decrease ‘different’ bills as nicely. This resulted in a pre-tax revenue of $8.6M and a web revenue of slightly below $7.1M. As there are slightly below 1.9M shares excellent, the web revenue per share was $3.75.

Wanting on the 9M 2023 outcomes, the corporate generated an EPS of $8.37 which is just barely decrease than the $8.63 in 9M 2022 however this might be defined by the $16.5M funding loss recorded within the first 9 months of final 12 months. Excluding that funding loss, ITIC’s pre-tax revenue would have been nearly 80% larger.

Buyers Title pays a quarterly dividend of $0.46 per share but additionally has a behavior of paying a really beneficiant dividend within the last quarter of the 12 months when it has a greater concept of its monetary outcomes for the 12 months. Earlier this quarter, ITIC introduced a special dividend of $4.00/share which can deliver the annualized dividend to $5.84 per share and this represents a dividend yield of 4%. Not dangerous in what arguably is a really weak 12 months for mortgage and actual property transactions. Moreover, let’s not overlook the full-year EPS will probably are available in at round $11-11.5/share (barren any unexpected surprises within the last quarter of the 12 months) which suggests the payout ratio is roughly 50%.

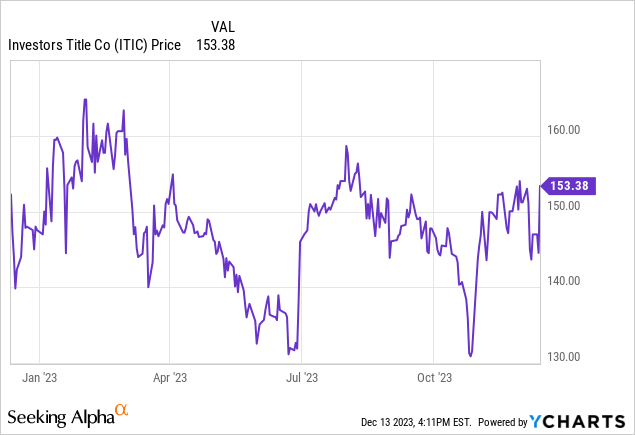

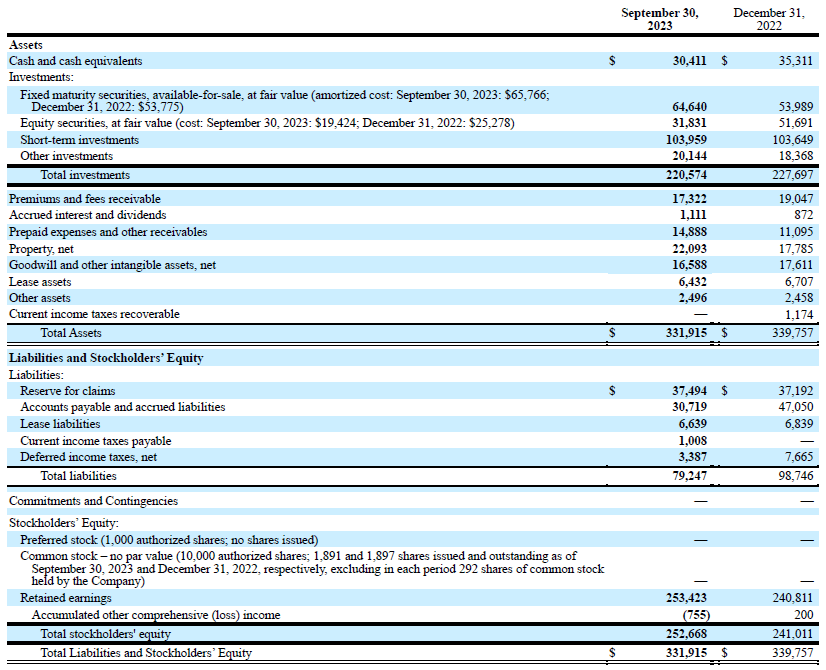

The rest of the revenue is retained on the stability sheet and as of the top of September, the corporate had a complete e-book worth of $252.7M representing nearly $134/share. It will drop by the top of this 12 months because the dividends payable in This autumn will probably be larger than the EPS.

ITIC Investor Relations

Goodwill and intangible account for $8.78 per share which suggests the tangible e-book worth per share is roughly $125 and I anticipate a year-end TBVPS of round $123/share after accounting for the particular dividend.

The corporate maintains a portfolio of securities and on the finish of September, it had about $65M in debt securities (marked to market as they’re held on an ‘out there on the market’ foundation) and slightly below $32M in fairness securities. These are additionally marked to market as the unique price foundation of the securities is simply $19.4M.

Moreover, ITIC has nearly $104M in short-term investments which primarily consist of cash market accounts invested in short-term funds, US Treasury Payments and business paper.

Funding thesis

Given the low-risk nature of the title insurance coverage enterprise, I’m wonderful paying 13 occasions earnings throughout a downcycle. As a reminder, the EPS in 2022 and 2021 was respectively $12.60 and $35.38, however each years had been impacted by substantial adjustments within the funding portfolio. Adjusting the EPS for these adjustments, the adjusted EPS in 2022 and 2021 would have been roughly $25.2 and $29.17/share.

And this makes ITIC one in all my most popular automobiles to wager on decrease rates of interest and a better transaction quantity on the true property markets. I at present haven’t any place in ITIC however can be constructing my place within the subsequent few weeks and months.