Bloomberg/Bloomberg through Getty Photographs

Tech corporations which might be decelerating and have been tossed into the penalty bucket have one fast technique of escape: curiosity from a non-public fairness purchaser. And potential rumors are the principle ingredient behind DocuSign’s (NASDAQ:DOCU) latest restoration rally, with the inventory capturing up greater than 40% because the begin of November.

Although M&A chat is the principle catalyst for DocuSign’s day by day swings proper now, I might argue that traders have many causes to concentrate on DocuSign’s fundamentals themselves. Even absent a buyout supply, I feel DocuSign nonetheless stands on agency floor from a valuation standpoint, and in an costly market this yr, that is precisely the type of “growth at a reasonable price” firm I might lean in on.

Buyout or not, the bull case for DocuSign stays shiny

I final wrote a very bullish article on DocuSign in September, when the inventory was buying and selling nearer to $50 per share and earlier than a real M&A frenzy had actually kicked in. Since then, the corporate has already loved a rumor-driven restoration rally, and as such, I am dropping my ranking on the corporate one notch to only bullish – however am nonetheless holding onto this inventory for additional positive factors.

Here is the essential thesis: none of us can predict what is going to occur with DocuSign’s buyout, however even within the occasion that DocuSign continues as a standalone agency, I discover loads of causes for the inventory to be a gorgeous purchase at present ranges. Exterior of the takeover chance, right here is my rundown of the core causes to be bullish on DocuSign:

- Trade chief that’s synonymous with e-sign. Even if pandemic tailwinds are “over” for DocuSign, distant work has solely proven us how reliant we’re on digital to facilitate mainly all the things. At the moment, many swaths of trade stay caught in legacy processes; and big sectors like actual property and healthcare stay ripe for expertise disruption. In different phrases, DocuSign nonetheless advantages from an enormous greenfield marketplace for its digital agreements merchandise. DocuSign can also be designated as an trade chief by Gartner, arguably essentially the most influential software program reviewer.

- Enterprise focus. Although churn has been extra concentrated amongst smaller shoppers, DocuSign continues to signal main enterprises, which is the place its renewal and growth base comes from.

- Buyer diversification. DocuSign is a very “horizontal” software program product that’s relevant to prospects of any trade, with none useful modifications wanted to its product. On the time of its IPO in 2018, DocuSign had solely ~400k prospects; right this moment, that quantity has greater than tripled to greater than 1.3 million, reflecting the power of DocuSign’s go-to-market growth.

- $50 billion TAM. DocuSign addresses a $25 billion market alternative in pure e-sign and a further $25 billion alternative for add-ons, which suggests the corporate’s present ~$3 billion income scale has solely achieved single-digit penetration into this general market.

- Wealthy margins result in immense scalability. DocuSign has 80%+ professional forma gross margins, among the many highest within the enterprise software program sector and permitting for vital working leverage at scale. It additionally generates 30%+ FCF margin.

There are dangers right here, in fact. DocuSign’s billings have slowed, and its development charges are paling compared to similarly-sized friends (Adobe’s (ADBE) Doc Cloud product continues to be seeing double-digit development charges). In my opinion, nonetheless, it is a moderately commoditized market and DocuSign nonetheless has a well-oiled gross sales and advertising and marketing machine that may seize greenfield gross sales alternatives in a broad, multi-billion greenback TAM.

Exterior of any acquisition information, the following main catalyst for DocuSign is its Q4 earnings release, anticipated in early March.

Rising profitability is offsetting slower development

The core concern that traders have with DocuSign: its development charges are paling, a pattern that continued into its third-quarter earnings launch. However for my part, we aren’t giving DocuSign sufficient credit score for its large growth in margins, which is resulting in wholesome free money movement. And ultimately, it is that profitability that’s attracting PE patrons to DocuSign’s door.

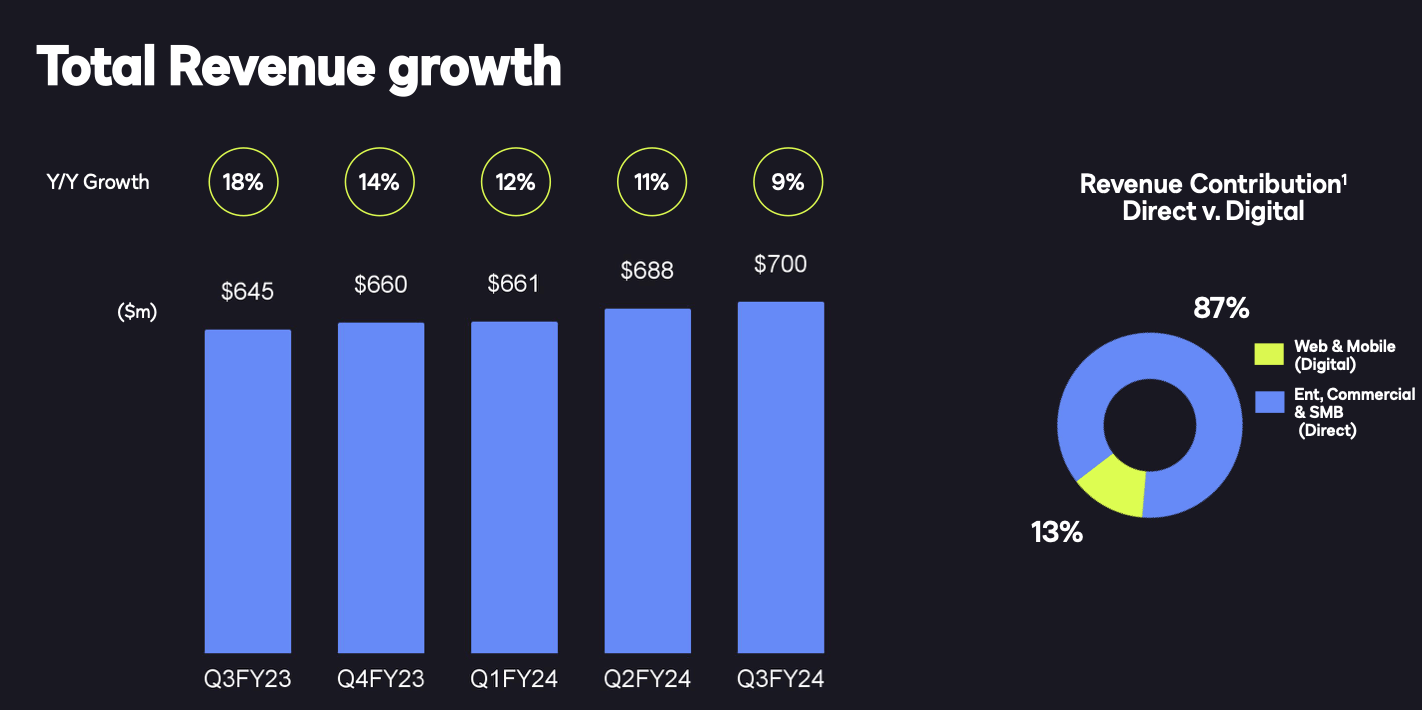

DocuSign income tendencies (DocuSign Q3 earnings deck)

As proven within the chart above, DocuSign’s development slowed to 9% y/y in Q3 to $700 million, although within the firm’s protection, that did are available properly forward of Wall Road’s expectations of $690 million (+7% y/y). It took just one yr for DocuSign’s development to slide from the excessive teenagers to single digits.

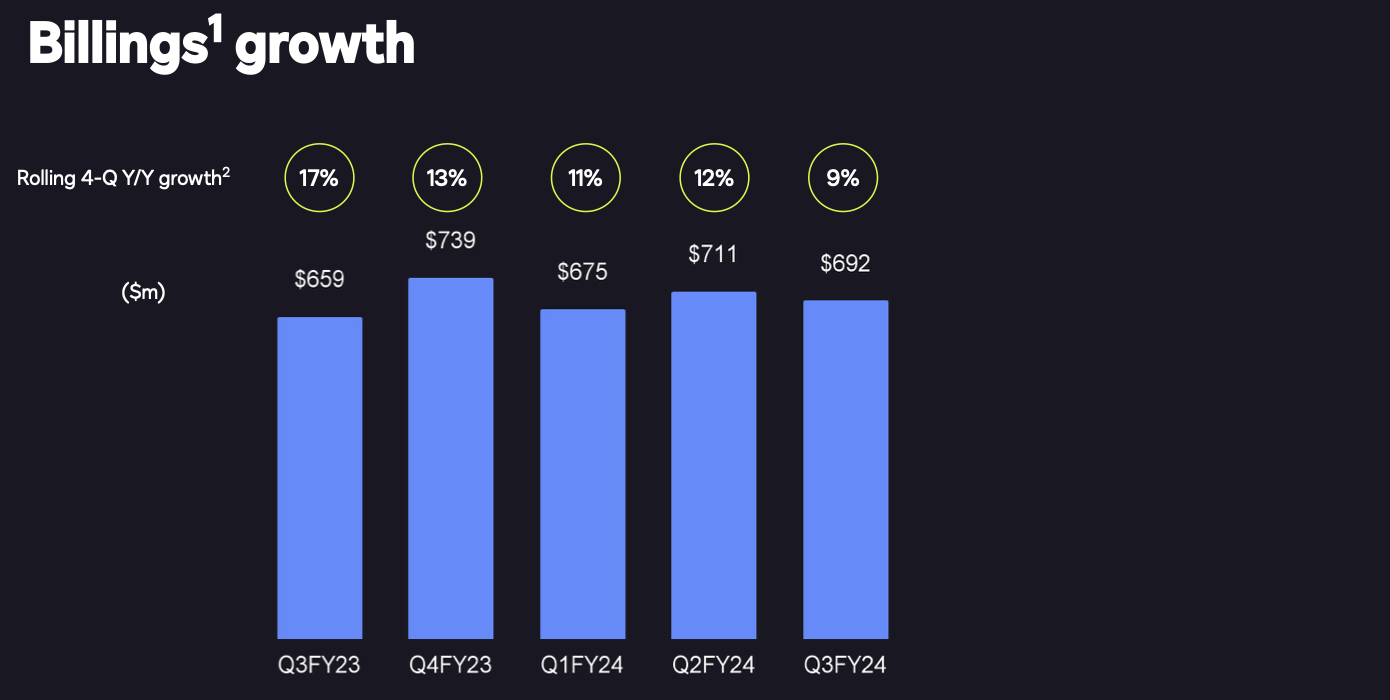

An analogous story is taking part in out in billings development, which as seasoned software program traders are conscious is the most effective forward-looking indicator of a subscription firm’s development trajectory. Trailing twelve-month billings development additionally decelerated three factors q/q to 9% – although this does assist to recommend that income development could stabilize within the 9% neighborhood, as billings and income development charges are lastly in line.

DocuSign buyer tendencies (DocuSign Q3 earnings deck)

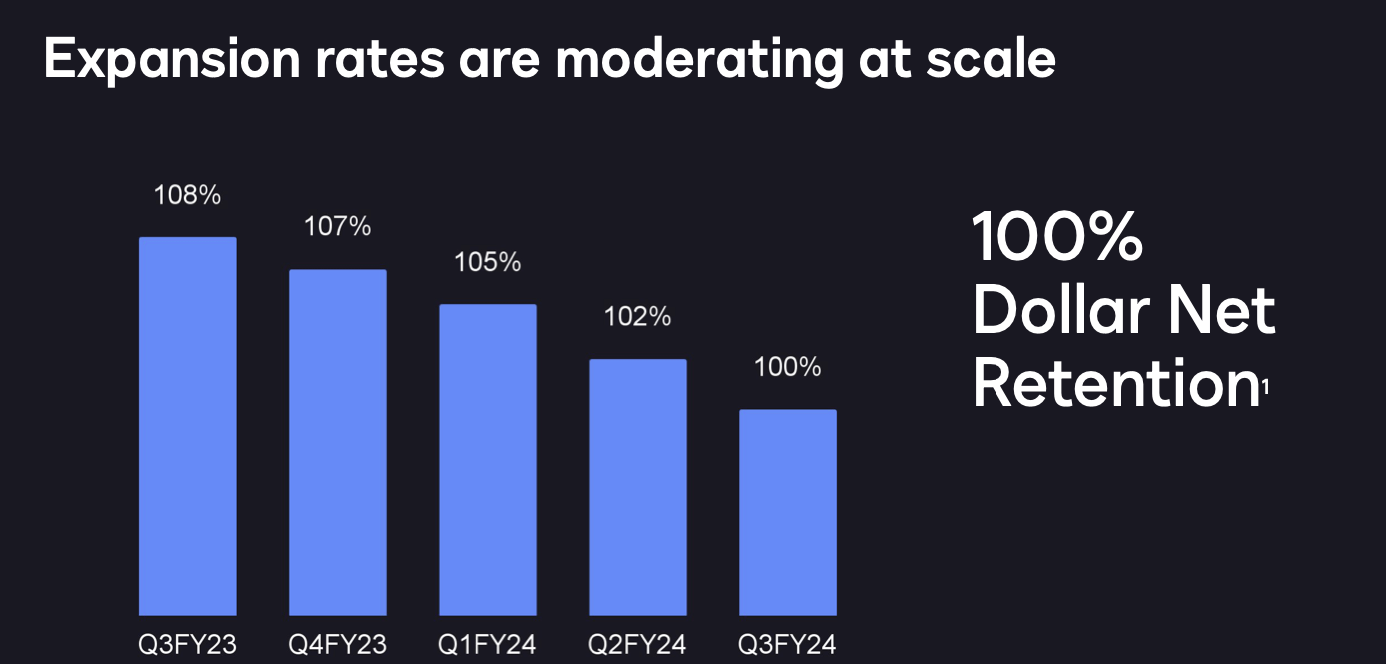

One of many core points here’s a slowdown in growth tendencies. Web income retention charges dropped to a report low of 100% within the quarter – indicating that seat growth and upsells are being utterly offset by churn. This, in flip, has been the results of an elongated macro-driven discount in enterprise budgets.

DocuSign growth tendencies (DocuSign Q3 earnings deck)

The excellent news: DocuSign is seeing indicators of stabilization, although the corporate does count on internet retention charges to get worse in This fall earlier than they get higher. Per CFO Blake Grayson’s remarks on the Q3 earnings call:

As anticipated, growth headwinds continued to influence year-over-year billings development. These dynamics are additionally seen in our greenback internet retention, which was 100% in Q3. Enlargement charges proceed to be tempered by spending optimization and IT funds scrutiny. We count on greenback internet retention to pattern downward in This fall.

That stated, we’re inspired by just a few early information factors evident in our outcomes this quarter. First, we noticed year-over-year consumption stabilization or enchancment in quite a lot of verticals, together with enterprise providers, expertise and insurance coverage […]

Second, we’re happy with the early progress we’re seeing from our investments within the omnichannel go-to-market efforts. Pushed by our direct gross sales efforts, the enterprise phase confirmed some early potential relative to efficiency in earlier quarters.”

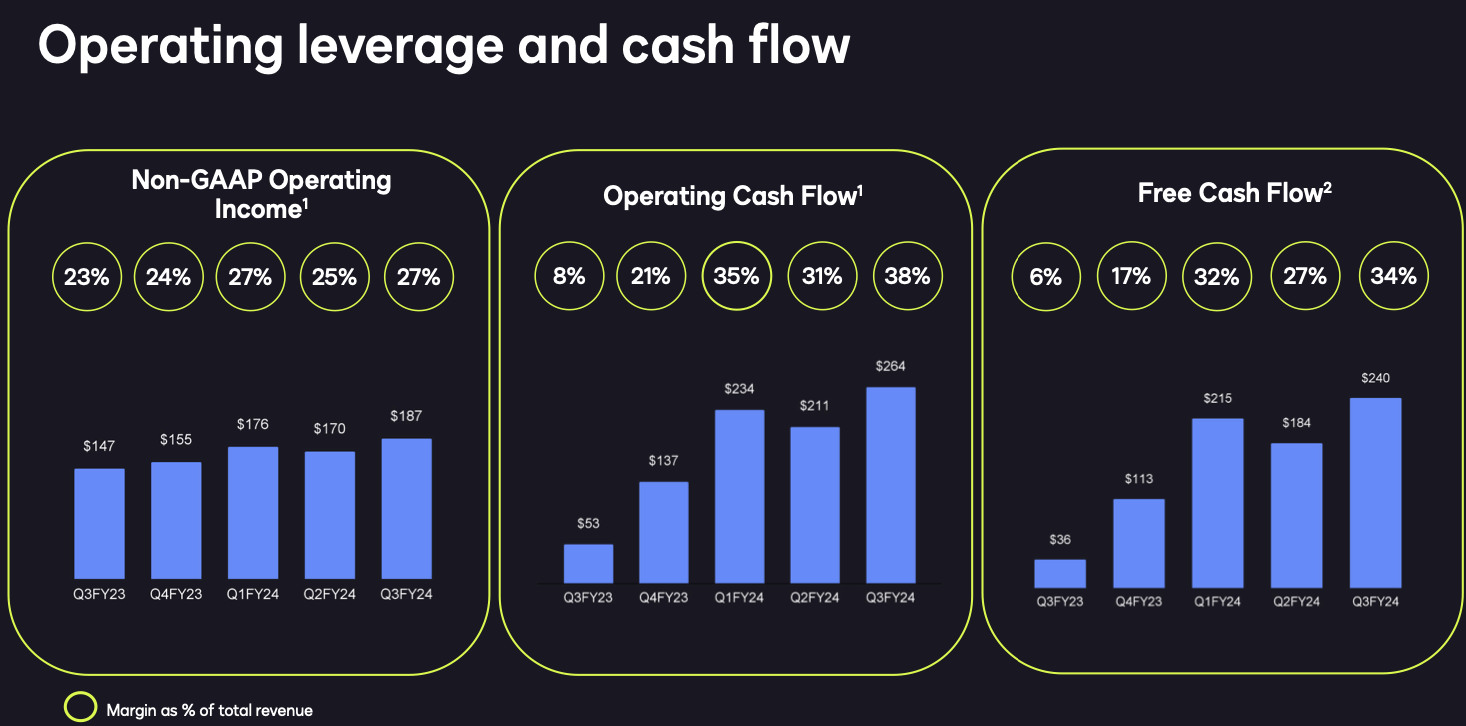

The offset here, though, is massively improved profitability. The company has been right-sizing its workforce, having cut out 10% of its workforce mid-last year. As a result of this, pro forma operating margins rose to 27% in Q3, up four points from 23% in the year-ago Q3:

DocuSign margins (DocuSign Q3 earnings deck)

In addition to that, year to date (through Q3) free cash flow of $639 million more than doubled y/y. DocuSign may not be exhibiting startup-like growth anymore: but at 80%+ pro forma gross margins and a very elastic opex base, it is producing enviable profits.

Valuation and key takeaways

At current share prices near $58, DocuSign trades at a market cap of $11.85 billion, and after we net off the $1.65 billion of cash and $0.69 billion of debt on its most recent balance sheet, DocuSign’s resulting enterprise value is $10.89 billion.

Meanwhile, for the next fiscal year FY25 (the year for DocuSign ending in January 2025), Wall Street analysts are expecting DocuSign to generate $2.91 billion in revenue or 6% y/y revenue growth.

Now, there are a number of reasons that outlook may be conservative. FY25 comps against a very rough and macro-impacted FY24. As enterprise budgets recover, so too might DocuSign’s billings – and we may see a reversion to seat expansion trends within the enterprise. International sales momentum may also help to provide a lift to revenue growth.

But just taking consensus estimates at face value, DocuSign trades at just 3.7x EV/FY25 revenue. And if we apply DocuSign’s YTD 31% FCF margin against that revenue profile, FY25 FCF would be $902 million, and DocuSign’s cash flow multiple is just 12.1x EV/FY25 FCF.

At these costs, it is no small surprise that PE corporations are sniffing at DocuSign’s porch. And regardless of acquisition rumors, the inventory nonetheless stays at modest multiples (and I might be prepared to stay invested on this firm standalone at these costs, too) – so I might advocate shopping for right here earlier than extra agency information hits the headlines.