chinaface/iStock by way of Getty Photographs

WHD Stays On The Steadiness

In my earlier article on September 13, 2023, I mentioned Cactus, Inc.’s (NYSE:WHD) enterprise and methods. As a result of precipitous fall in pure fuel costs, WHD faces a comparatively unsure vitality market atmosphere. The upstream operators will possible reply with rig reductions, which can weaken the corporate’s near-term outlook. It has additionally deferred its investments within the Center East to decrease prices and shield the margin. I feel its outlook on the margin entrance has improved since my final article, though the topline stays slippery.

Not too long ago, WHD has rolled out modified frac valves, lowering the variety of repairs and resulting in elevated potential demand within the coming months. The spurt of inquiries for frac rental tools can be encouraging for its prospects. The inventory in all fairness valued in comparison with its friends. Backed by bettering money flows and strong liquidity, I recommend traders “hold” the inventory for average medium-term returns.

Why Do I Preserve My Name Unchanged?

I thought-about WHD a “hold” in my earlier September 13, 2023 article. By the top of Q2 2023, I believed the inventory would keep on the steadiness. In the meantime, subdued US drilling exercise would strain its Stress Management topline, decrease enter prices, and provide chain diversification would decrease its value construction, retaining the margin regular. I wrote:

The provision chain prices have been deflating, releasing the strain of high-cost stock on the working capital. It plans to diversify within the Center East and expects to finalize its funding construction and document its first buyer order in late 2024. To keep up a light-weight value construction, it has deferred its investments within the Center East.

Given the consolidation within the upstream vitality market and low pure fuel costs, I nonetheless see some headwinds persist. Alternatively, the corporate witnessed elevated inquiries for frac rental tools. It additionally retains its value construction tight with environment friendly product introductions. Its money flows and steadiness sheet stay strong because it pays dividends. So, I retain my “hold” tackle the inventory.

Methods Defined

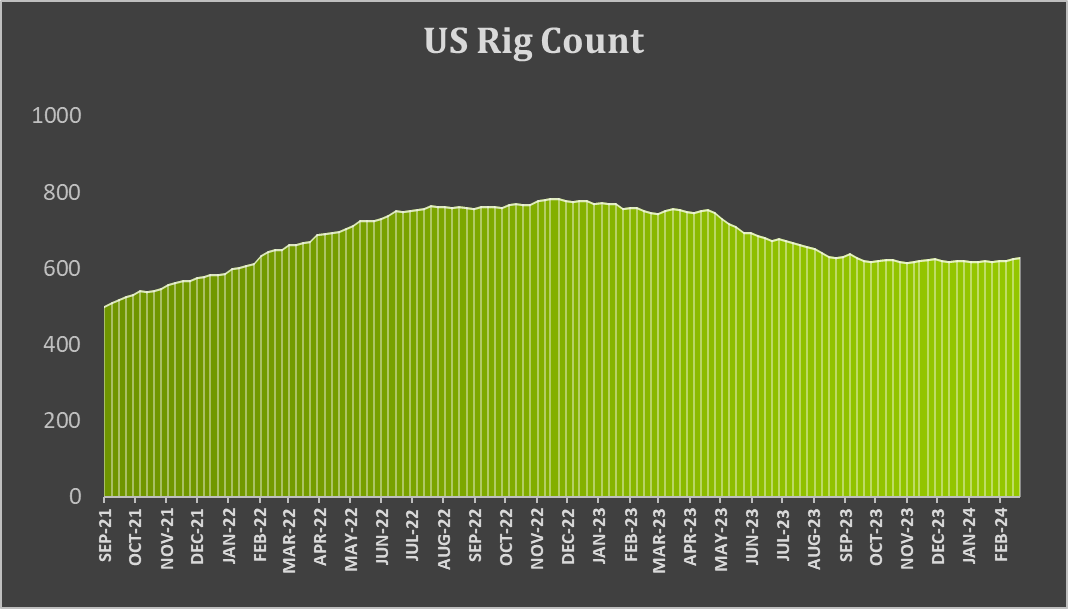

Baker Hughes rig rely information

WHD is about to roll out new wellhead and valve merchandise. The brand new merchandise will exchange its stock within the following months and will enhance its monetary outcomes. As a result of valves are torn down after a frac job, it sometimes includes giant restore prices. The rollout is a modification of the present frac valve, considerably lowering the variety of repairs. WHD can be evaluating alternatives concerning its enlargement plans within the Center East.

After the present M&As of upstream operators, effectivity has grow to be the first focus of oilfield companies corporations. WHD primarily caters to comparatively large-sized prospects who make investments by means of the commodity cycles. Though the near-term impacts of the consolidation are unclear, the administration expects a discount within the US land rig rely by the top of 2024. Given the weak spot in pure fuel costs, operators will possible reply with rig reductions. Nonetheless, I count on such a situation will strengthen the significance of high-grade drilling and drilling efficiencies.

How Does The Q1 Look?

WHD’s Filings

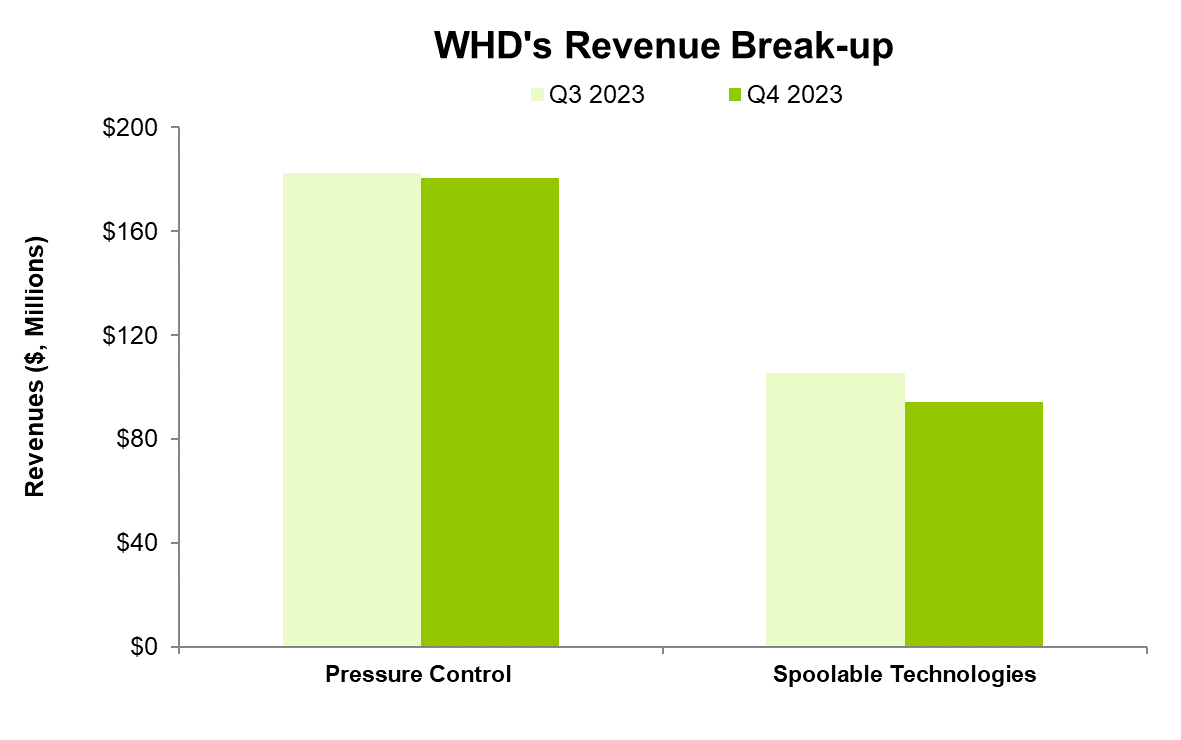

The corporate’s administration estimates that the Stress Management section revenues can lower by “mid-single digits” in Q1 in comparison with This fall 2023. It expects an analogous fall within the Spoolable Applied sciences section revenues. It additionally expects the adjusted EBITDA margins within the Stress Management section to lower by 180 foundation factors (on the steerage mid-point), whereas the adjusted EBITDA margin of Spoolable Applied sciences can deflate by 360 foundation factors.

In my opinion, the section’s efficiency will rely largely on the rig rely. Since I count on a marginal drop in rig rely as a consequence of low pure fuel costs, I feel the corporate’s administration has made a good estimate concerning the Stress Management section Q1 outlook. Beginning Q2, the section will possible enhance following elevated inquiries for frac rental tools.

Within the Spoolabe Expertise section, elevated enter prices will dent its margin in Q1. Nonetheless, the corporate may have tailwinds following larger demand for FlexSteel’s merchandise from worldwide and midstream prospects. Buyers might be aware that WHD acquired Flexsteel in March 2023, which helped improve set up velocity, cut back possession prices, and enhance effectivity.

Analyzing This fall Drivers

In search of Alpha

From Q3 to This fall (as launched in its FY2023 earnings on February 28), WHD’s revenues within the Stress Management section decreased marginally by 1.1% because of the decline in US onshore exercise. EBITDA margin expanded by 120 foundation factors as a consequence of decrease rental tools restore prices following the adjustments in frac valve design.

In Spoolable Applied sciences, revenues decreased by 10.4% as upstream exercise decreased. Nonetheless, larger bills ensuing from the remeasurement of the FlexSteel earnout legal responsibility improved its margin. The adjusted EBITDA remained regular from Q3 to This fall. Nonetheless, decrease gross sales quantity resulted in reductions in working leverage, partially offsetting some features.

Money Flows and Steadiness Sheet

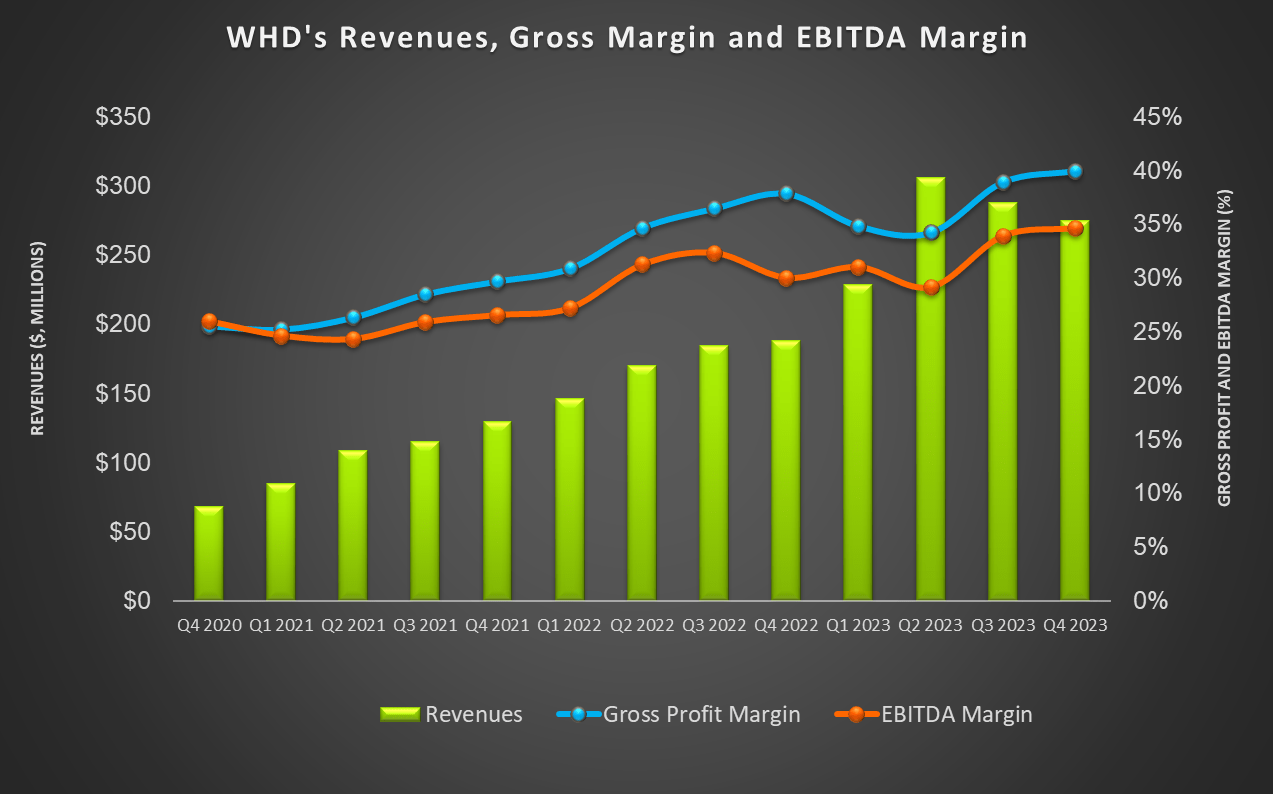

Cactus’s money move from operations improved by 1.9x in FY2023 in comparison with a 12 months in the past. Greater revenues, decrease stock, and better collections of receivables are the principle causes for the money move rise. Free money move additionally elevated 2.3x in FY2023. Its FY2024 capex steerage ($45 million-$55 million) means capex will improve from FY2023.

As of December 31, 2023, WHD’s liquidity (money steadiness plus accessible credit score facility) was $350 million. Strong liquidity ensures few monetary dangers. In This fall, it paid a dividend of $0.12 per share and is permitted to maintain the dividend unchanged for the March fee.

What Does The Relative Valuation Suggest?

Creator Created and In search of Alpha

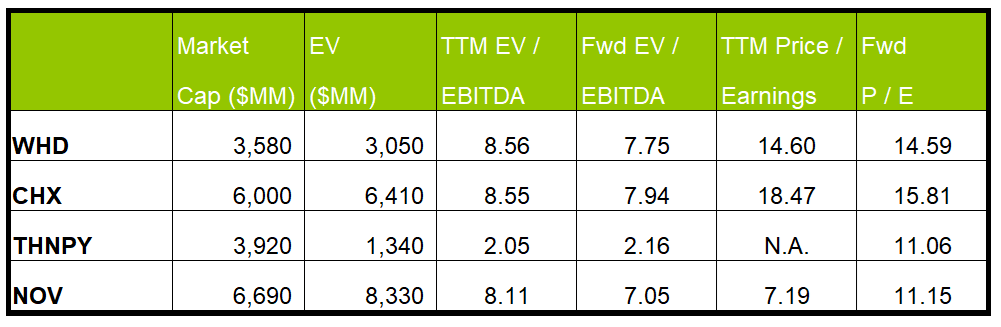

WHD’s ahead EV/EBITDA contraction versus the present EV/EBITDA a number of is steeper than some friends. This sometimes leads to a better EV/EBITDA a number of. The corporate’s EV/EBITDA a number of (8.6x) is larger than its friends’ (CHX, THNPY, NOV) common (6.2x). The present a number of is beneath its five-year common EV/EBITDA of 13.2x. So, the inventory seems to be fairly valued in comparison with its friends.

If it trades on the previous common, it may possibly climb 29% from the present stage. If it trades on the business common, it may possibly drop by 37%. Since my final publication in September, the place I steered a “hold,” the inventory has declined (down roughly 8%). Whereas the rig rely was comparatively robust after I final revealed, it has grow to be unsure not too long ago. Nonetheless, demand from worldwide and midstream prospects has improved. General, I feel traders’ sentiments concerning the inventory will stay unchanged. Subsequently, I count on it to hover across the present value (inside a $44-$48 band).

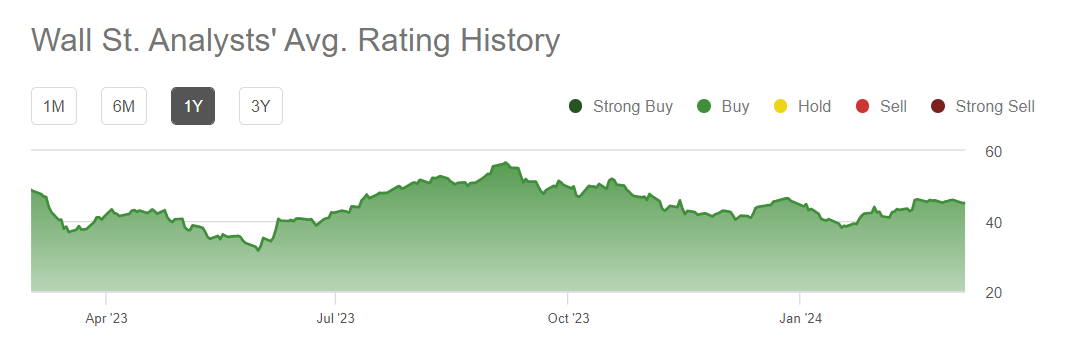

Wall Avenue Ranking

In search of Alpha

Previously three months, 4 sell-side analysts rated WHD a “buy” (together with a “strong buy”), 5 analysts rated it a “hold,” and one rated it a “sell.” The consensus goal value is $52.9, suggesting a 17% upside on the present value. I feel the sell-side traders are barely extra optimistic in regards to the returns than its outlook actually displays.

Threat Components

EIA

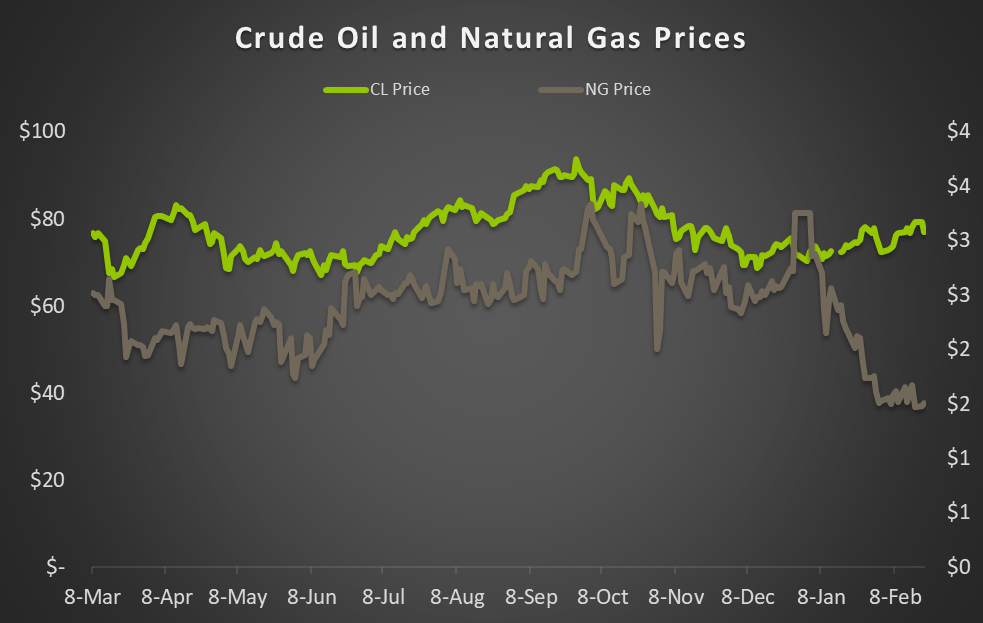

From Q3 to This fall 2023, the crude oil value declined by 15%. Throughout this era, the US rig rely remained practically unchanged. For the reason that begin of Q1 2024, the crude oil value and rig rely have remained regular. I feel that pure fuel costs will largely decide the rig rely’s motion, however a gradual crude oil value will act as assist within the near-to-medium time period.

Vitality costs have an effect on oil and fuel business exercise and oilfield companies’ efficiency. Pure fuel costs have been risky not too long ago. Over the previous 12 months, pure fuel costs have crashed by ~40%, whereas crude oil costs have remained regular (~2% up). A weakened pure fuel value can additional cut back vitality operators’ capital budgets and drilling exercise, retaining WHD’s topline and money move underneath strain within the close to time period.

What’s The Take On WHD?

In search of Alpha

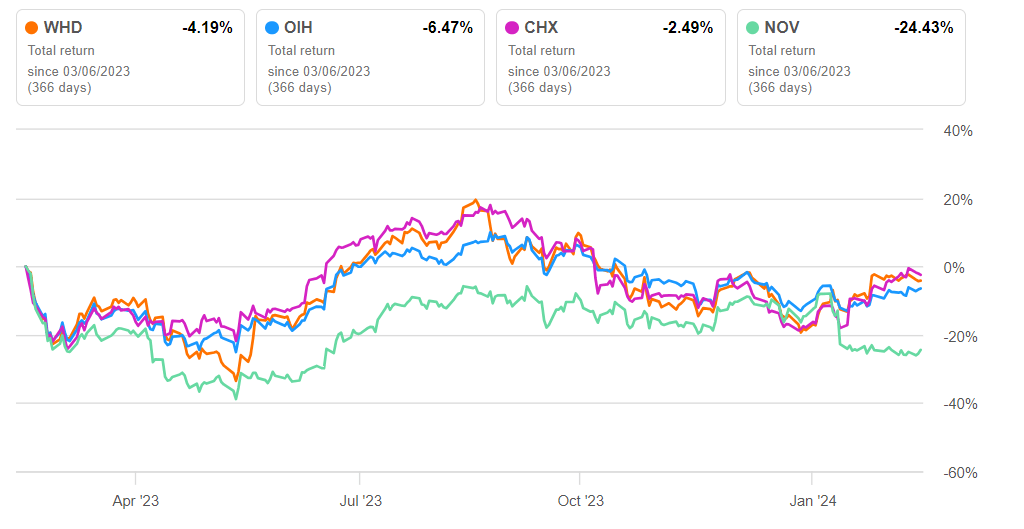

The introduction and renewal of wellhead and valve merchandise and the corporate’s enlargement plans within the Center East have led to improved effectivity. Given the altering situation within the vitality business, upstream operators will possible pay a premium for extra environment friendly merchandise. The elevated inquiries for frac rental tools might be encouraging for the corporate. It continues to profit from the earlier acquisition of FlexSteel in 2023 by means of improved velocity and extra environment friendly merchandise. So, the inventory marginally outperformed the VanEck Oil Providers ETF (OIH) previously 12 months.

Nonetheless, elevated enter prices will dent the margin of the Spoolabe Expertise section. The corporate’s money flows turned constructive with stock value reductions in FY2023. Its steadiness sheet is powerful, with ample liquidity. Given the relative valuation multiples, traders would possibly need to “hold” the inventory.