Its not an ideal analogy however its clse on many knowledge units. Chris Stein/DigitalVision through Getty Pictures

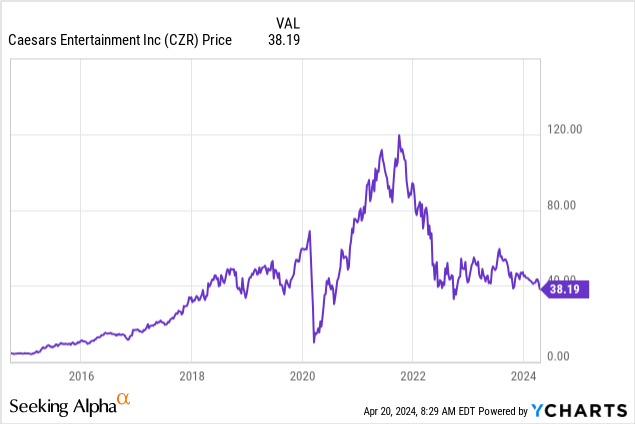

Premise: We carried out a SWOT evaluation (Strengths, Weaknesses, Opportunities, Threats) with our consulting associates in an effort to worth the shares of Caesars Leisure, Inc. (NASDAQ:CZR) relative to friends. Our previous view was that CZR had fallen far under what we thought-about honest worth. Final December, CZR traded at $48 once we posted a value goal of $66 for a while later this 12 months.

Our thesis was that on all fronts at the moment, CZR revenues had been deep right into a post-covid restoration cycle that had numerous ramp forward. Again in July of 2023, CZR traded at $57. What occurred? By any measure, the corporate was doing nicely.

CZR income was deep in restoration. The lodges had been jam packed, significantly the Vegas properties. REVPAR was excessive, gaming win forward each in slots and desk video games. And the sports activities ebook was transferring towards optimistic EBITDA. (It has certainly achieved black ink going ahead). Administration’s concentrate on addressing its large debt overhang was robust. Together with FCF offering the money, debt was starting to say no.

I used to be joined in a bullish outlook by some analysts, who cited related tailwinds. So what occurred to CZR that we didn’t see coming, nor a number of others for that matter? Whether or not it was a handful or a broad consensus, our steerage did not matter. Mr. Market shrugged off the bullish takes.

Looking for Alpha and different high monetary websites current opinions throughout a broad spectrum from extremely bullish to bearish daily. And among the many nice calls, all of us have our share of misses – many by contributors with in any other case positive monitor data. So it was time we did a primary SWOT evaluation on CZR to search out how their forensic enterprise fashions work in a altering world.

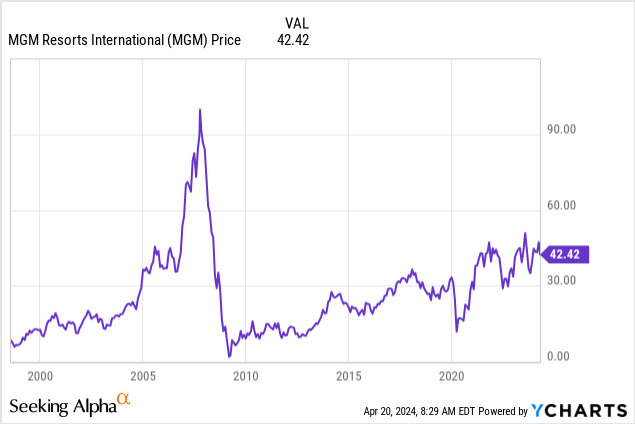

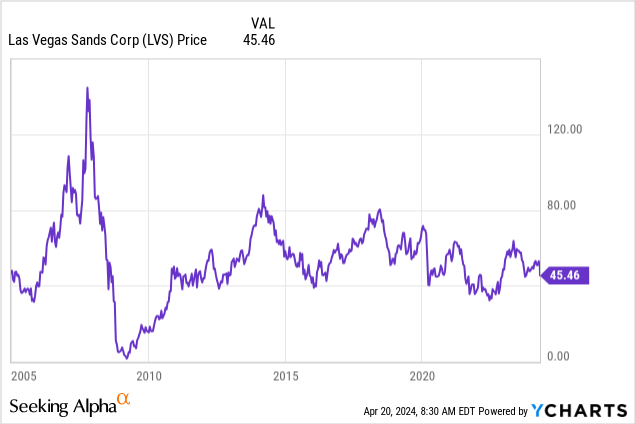

A great way to start was to check CZR with its two most necessary aggressive friends: MGM Resorts (MGM) and Las Vegas Sands (LVS). And in that course of, we uncovered what, we consider, is a hidden worth story for all three.

Our SWOT evaluation constructed off the Harvard MBA mannequin produced no surprises. CZR led in database energy, (65m) property protection, its key weak spot was no Asia footprint, alternatives in versatile motion of many property. MGM was tops in digital with its #3 place in sports activities betting income, the widest world outlook for development, and LVS for its highly effective Asia restoration. However lack of publicity to the US market after the Vegas property gross sales was questionable. Total, the three operators shared much more SWOT traits in frequent than variations.

The takeaway – the three corporations could possibly be valued as a single large, with weaknesses of 1 compensated with strengths from the opposite. The clear shock: They could possibly be de facto one firm within the eyes of traders, with a mixed ahead development arc that alone wouldn’t be as engaging.

Welcome to the Gaming Trio purchase vs. Walt Disney

In understanding the comparative virtues or lacking items of CZR and its two key friends, we unearthed a much more intriguing set of info. The similarities between the three gaming giants had been wonderful. A lot so {that a} thoughts experiment steered itself instantly. What if the three corporations had been folded right into a mini-portfolio? No, we do not presume to have discovered the holy grail of cannot lose, positive factor. We do suppose traders searching for yield in instances like this have to consider different methods.

And what if we in contrast the trio’s mixed value with that of, say, Disney (DIS), which alone trades at the very same value? On a pure cash in returns out foundation, what appears to be like like a much better guess for the cash? Whenever you choose shares, you principally consider the percentages based mostly on efficiency. This method is the equal of the cash line guess – easy win or lose.

In fact, this isn’t an apples to apples analogy. The trio is within the enterprise of entertaining adults. DIS is within the enterprise of entertaining households and kids – or it’s alleged to be. However a big part of the enterprise of each is the income reaped from visitation to its brick and mortar properties. The trio runs 104 properties in whole within the Vegas strip, US areas, Macau and Singapore.

Complete US/world guests to key prime Disney parks: 72m in ’23

Complete guests (est) to US and Asian casinos: 110m in ’23.

The income of each is fully generated by arrivals of whole company, each day trippers and in a single day guests. So in essence, they’re each additionally within the enterprise of physique technology.

Clearly, the place the comparability stops is within the multitude of DIS verticals in digital leisure and movies. The disparity of annual revenues makes a distinction, for positive. But DIS whole income is ~$98b, whole income of the trio is $40b, But when we isolate DIS parks alone, the income is $33.6b – remarkably shut when it comes to the stay visitation solely.

The trio’s debt is a mixed $70b vs. DIS at $45b, however traders are inclined to see debt as related proof of monetary self-discipline or recklessness. Its vote on administration weighed relative to general firm efficiency.

Our thoughts experiment: Recognizing the variations and similarities in lots of knowledge factors, are you able to make the case {that a} buy-in of our trio makes higher sense than one on DIS?

We probed a bit additional:

When merging the promoting value of the three shares, we got here to a complete worth of $113 at writing. We stated this could possibly be a uncommon case of the entire value excess of the components.

That posed a what if?

What if the three on line casino friends had been one firm?

CZR: $39

MGM: $42

LVS $50

Complete: $113

Assume shopping for 200 shares whole all three on the costs proven for one 12 months’s maintain.

Here is the 2023 EPS COMPARATIVE:

DIS $1.28

THE TRIO: $8.90

In different phrases, the trio earned 7X what DIS did in the identical 12 months. Is that this completely dispositive that your funding in, say, 200 shares of the trio vs. the identical purchase for DIS was far and away a better funding selection? Not essentially, however our level right here is that this: You may guess that on sentiment alone, the overwhelming majority of traders would most likely purchase the 200 of Disney than roll the cube on a trio of on line casino shares. Our thoughts experiment merely challenges that typical knowledge.

It’s clear that each propositions are corporations which have equally borne the headwinds of covid and its longer-term penalties. Each face a sword of Damocles swinging above them in a doable recession that will represent an enormous time headwind to any retail operation tied to physique technology. Add to that the disruption in streaming and theatrical attendance for DIS and the hovering labor and insurance coverage prices plaguing the on line casino operations and, for each, the debt balances too huge too lengthy.

Conclusion

Our thoughts experiment raises the notion that traders could make their very own little hedge funds with mini packages of shares inside related sectors, whole up the price, and level the bundle price in opposition to a equally valued sector inventory that sells for 3 to 5 instances as a lot to the same value.

This isn’t to suggest that completely different headwinds can besiege every inventory over a given period. However making a pure money-on-money resolution on extremely related shares packaged might be a superb alternate technique in markets in turmoil or calm. What counts ultimately are returns.

On this thoughts experiment, we see the trio as outperforming DIS throughout the identical timeframe when it comes to EPS now and doable projections over the approaching years.